VITL - Vital Farms: I Like The Business But Not The Valuation

2023-10-27 15:51:02 ET

Summary

- Vital Farms operates in a promising niche of the health-conscious food industry with strong revenue growth momentum.

- The company's revenue growth has been impressive, but it has yet to achieve sustainable profitability.

- The stock is currently fairly priced with limited upside potential, leading to a neutral "Hold" rating.

Investment thesis

Vital Farms ( VITL ) is one of the beneficiaries of the changing trend in America for more health-consciousness. My analysis suggests that the company indeed operates in a very promising niche of the large good industry, and its financial performance has been strong so far. The company demonstrates a solid ability to absorb positive secular shifts. Still, it has yet to achieve sustainable profitability, which is why I am not ready to pay a premium for the stock. According to my valuation analysis, the stock is approximately fairly priced at current levels, and there is very limited upside potential. That said, I give VITL a neutral "Hold" rating.

Company information

Vital Farms is a food company specializing in products sourced from animals raised on family farms, including shell eggs, butter, hard-boiled eggs, liquid whole eggs, and ghee.

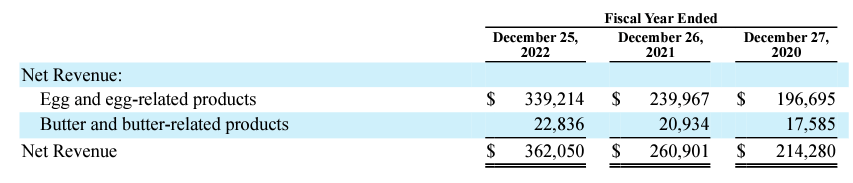

The company's latest fiscal year ended on December 25. VITL disaggregates its revenues by primary product: eggs and butter. According to the latest 10-K report , eggs and related products contributed 94% of all sales in FY 2022.

{kind=link}

Financials

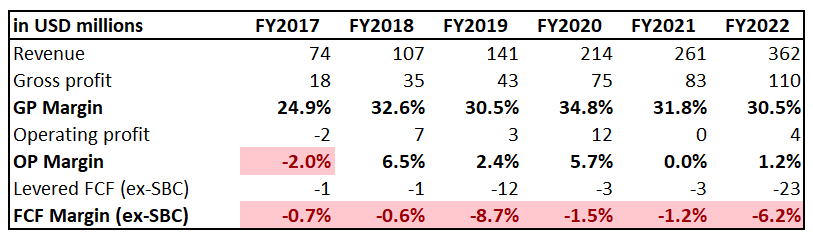

The company's financial performance is publicly available only from FY 2017 because VITL went public relatively recently, in 2020 . VITL demonstrated massive revenue growth over the last six full fiscal years with a 37% CAGR, meaning that the top line skyrocketed by almost five times. The gross margin demonstrated notable expansion due to the revenue growth, but the operating margin has been very volatile. Despite its staggering revenue growth over the long term, VITL's free cash flow [FCF] margin ex-stock-based compensation [ex-SBC] has been consistently negative.

{kind=link}

I do not consider the company's negative FCF margin a big problem since it is in the early stages of its development, and having positive dynamics in the gross margin is already a good sign. Moreover, it is important to understand that the company's balance sheet is strong thanks to the favorable IPO timing of massive stock market recovery in the second part of 2020. The company's solid $84 million net cash position means VITL is well-positioned to fuel further growth, given the fact that a negative FCF margin is relatively narrow, and the business model looks asset-light.

Seeking Alpha

The latest quarter's earnings were released on August 3 , when the company topped consensus estimates. Revenue demonstrated strong growth momentum with a 28% YoY increase. The company continues to benefit from the economies of scale effect, as its gross margin expanded by a notable five percentage points on a YoY basis. As a result, the operating margin expanded YoY by almost seven percentage points, though it shrank by about 150 basis points sequentially. Improvement of profitability metrics allowed to generate $0.15 in terms of the adjusted EPS, which is a massive improvement from last year's Q2 zero EPS.

Seeking Alpha

The upcoming quarter's earnings are scheduled for November 2. Quarterly revenue is expected by consensus at $110 million, meaning a projected 19.5% YoY growth. The adjusted EPS is expected to double YoY from $0.02 to $0.04.

Seeking Alpha

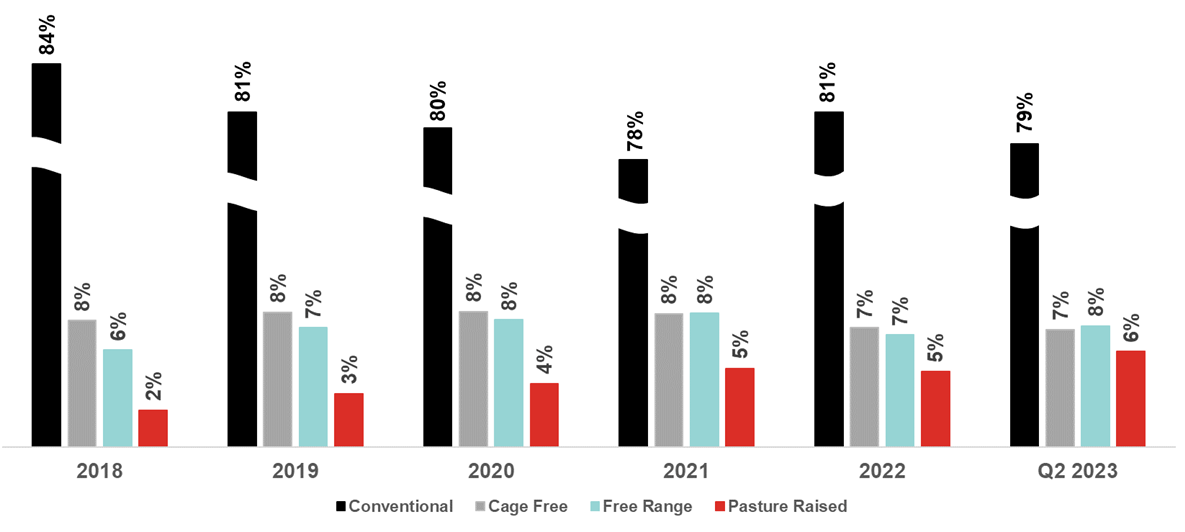

Overall, I think the company operates in a promising niche of pasture-raised foods. According to Texas Health , younger generations are more health-conscious than previous generations. The more health-conscious people become, the more they care about their nutrition. Pasture-raised eggs are much healthier than conventional, as they contain multiple times more essential nutrients to sustain health. At the same time, the share of pasture-raised eggs in the overall eggs market is still insignificant, despite a solid positive trend in recent years. That said, there is still vast room for this niche's growth as people become more health-conscious.

{kind=link}

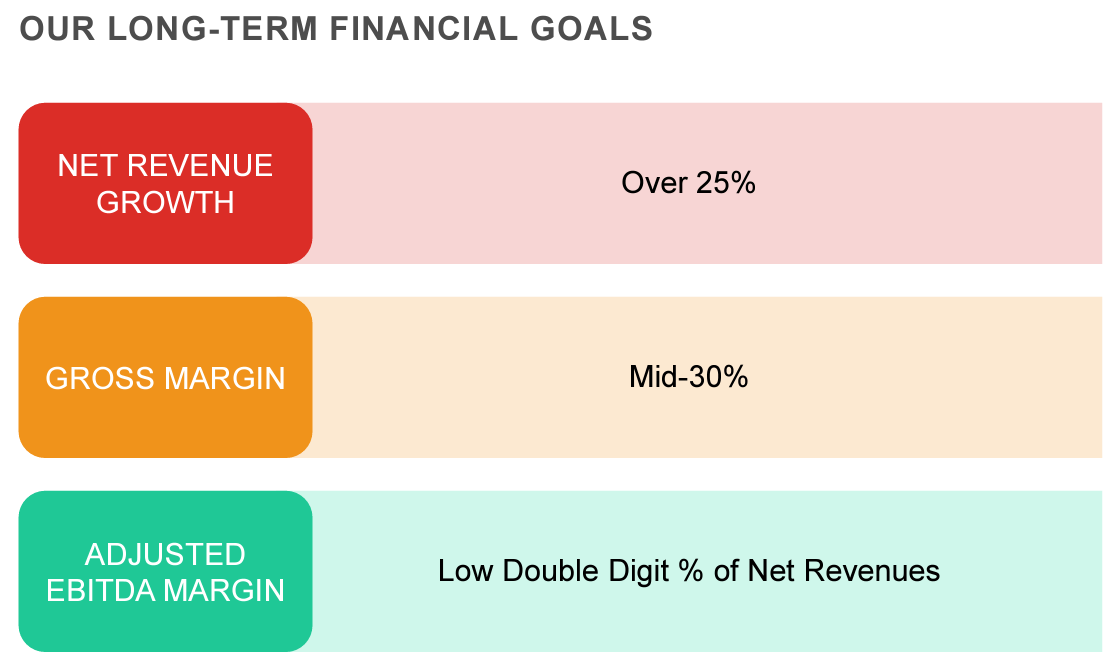

The American eggs market is estimated at about $14.5 billion by statista.com , meaning that every 5% increase in pasture-raised eggs' market share means an additional $725 million market opportunity for companies like VITL. According to the same resource, the overall U.S. eggs market is expected to compound by 7.9% yearly, which is a solid industry tailwind for VITL. Given the expected solid overall egg market growth multiplied by the secular shift to healthier nutrition, I believe Vital Farms will likely achieve its management's long-term revenue growth goals.

{kind=link}

Valuation

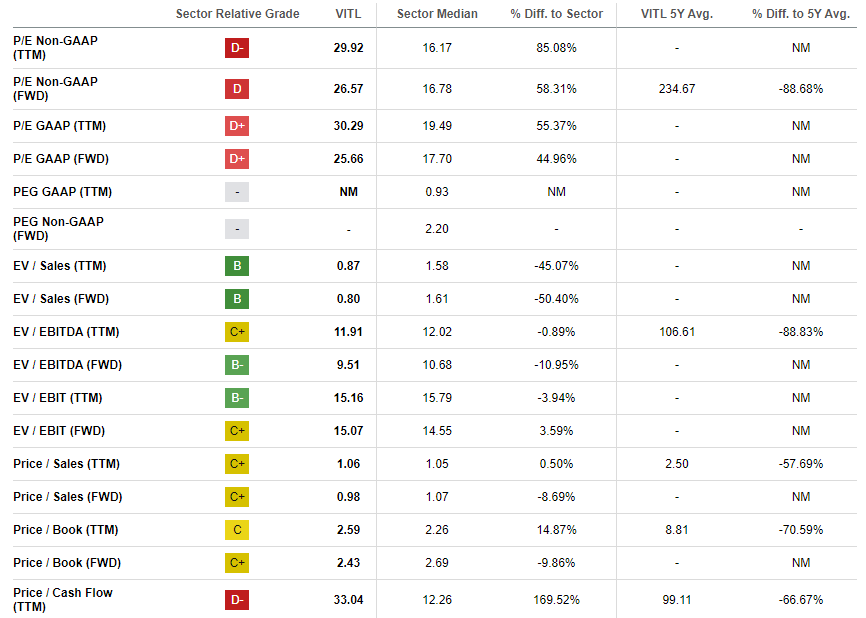

The stock demonstrated a 25% year-to-date price decline, significantly underperforming the broader U.S. market. Seeking Alpha Quant assigns the stock an average "C+" valuation grade, meaning the stock is approximately fairly valued. Indeed, most of the current valuation ratios are substantially lower than the company's five-year averages. On the other hand, from the price-to-earnings perspective, the stock looks substantially overvalued.

{kind=link}

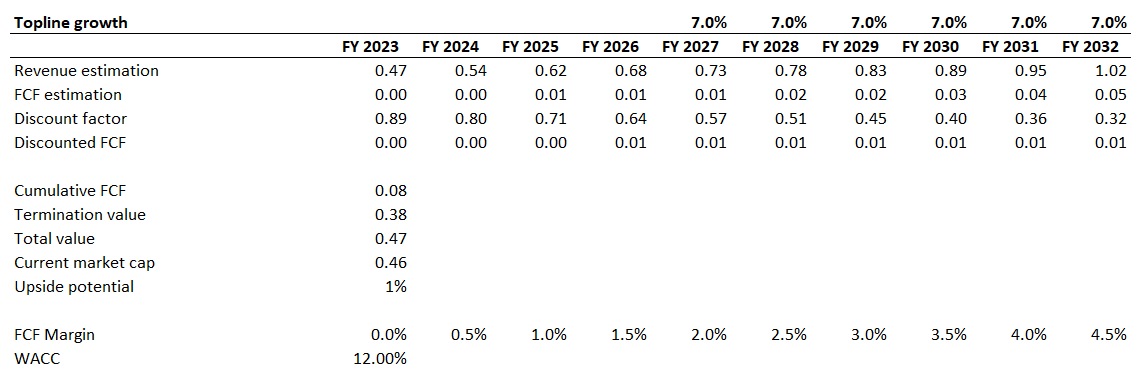

Valuation ratios analysis provides mixed outcomes, so I need to conduct another approach. I proceed with the discounted cash flow [DCF] simulation, since VITL is a growth company. Due to the company's small scale and profit instability, I use an elevated 12% WACC. I have revenue consensus estimates available up to FY 2026 and expect a 7% revenue CAGR for the years beyond. I expect zero FCF margin for my base year and further forecast a 50 basis points yearly expansion.

{kind=link}

According to my DCF simulation, the current market cap of VITL is very close to the business's fair value. I ignore the company's outstanding net cash position for my valuation analysis because this year, the company struggles to generate positive FCF ex-stock-based compensation [ex-SBC], and it is highly likely to be utilized partially.

Risks to consider

VITL faces substantial concentration risks. In FY2022, two customers represented 37% of all sales, which means substantial dependence of the company's earnings on just two customers' financial health and preferences.

{kind=link}

Another big risk is raising commodity prices, which affect the company's bottom line. While the company is still young and pasture-raised foods are the young trend, VITL might not be able to exercise substantial pricing power, and it might take longer to achieve the desired level of profitability.

Bottom line

To conclude, VITL is a "Hold". The business looks promising given the staggering revenue growth profile and positive secular shifts in food consumption directed towards more health-consciousness. The company is still to achieve sustainable profitability, but its balance sheet is strong enough to finance multiple more quarters to fuel further growth, as the company already demonstrates signs of the business model's economies of scale effectiveness. However, my valuation analysis suggests there is almost no upside potential, and I am not ready to pay a premium to the fair value given the uncertainty regarding profitability timing.

For further details see:

Vital Farms: I Like The Business, But Not The Valuation