SOL - Volume Breakout Report Update: Buy Eton Pharmaceuticals

Summary

- A number of VBR "green energy" picks have popped higher in January, pulling investment returns for the group of past picks strongly higher.

- A performance review of 46 previous selections since late June is discussed.

- I continue to refine the search and formula ideas for identifying future big winners using heavy-volume buying as the main criteria, often rising out of lower-volatility basing price patterns.

- Eton Pharmaceuticals fits my new VBR technical sort criteria, at the same time as strong growth is projected in sales and operating income for 2023.

I thought I would write a quick update on the performance of my initial Volume Breakout Report picks made between June 25th and September 18th, 2022. As a group, some 46 selections (45 names, with one picked twice in different weeks) have been mildly “outperforming” the Russell 2000 and S&P 500 indexes. The January Effect of unusual Wall Street interest in small caps (from a seasonal calendar perspective) has helped returns to bump up a little bit. Often, investors including institutions redeploy capital from losers in December (locking in tax losses) to new ideas in January.

I will also discuss a new VBR pick: Eton Pharmaceuticals ( ETON ). The company is a minor pharmaceutical enterprise witnessing heavy-volume accumulation by investors, alongside a strong operating expansion forecast by Wall Street analysts in 2023.

Performance Update

The +5.9% mean average return of all the picks, using a simple buy-and-hold decision, has beaten the peer small-cap index iShares Russell 2000 ETF ( IWM ) by +2.73% on a total return basis (including price appreciation and dividends, but excluding trading costs), when measured from the Friday closing values before VBR updates posted each weekend into Friday, January 13th's close. Also, the small-cap Russell has performed somewhat stronger than the S&P 500 in price since late June. So, the VBR lists have actually gained even better, outperforming the SPDR S&P 500 ETF ( SPY ) by +5.67% for a mean average, over periods ranging from 4 months to slightly more than 6 months held. (On a per pick basis, the average equivalent total return IWM gain has been +3.17% vs. SPY’s +0.23%).

Below I have graphed each weekly VBR list. Of course, the first week has turned out to be the worst selection group in the whole process (as luck would have it). In terms of changes and mistakes, I did specifically talk about selling Li Auto ( LI ) a month after the VBR buy signal, and have mentioned generally taking losses at the -20% to -30% level to reduce portfolio risk, while increasing overall returns. In addition, not mentioning Target Hospitality ( TH ) sooner was a mistake that cost another 1% in the total return calculations above.

A final note in calculating performance vs. the charts below is LGL Group ( LGL ) split the company in half in early October. For whatever reason, YCharts is not adjusting LGL value for MtronPTI ( MPTI ) shares received properly. LGL's stockholders of record received one-half share of MtronPTI's common stock for every share of LGL's common stock on October 7th. I have adjusted for this YCharts performance graph error in my calculations above.

VBR Pick Performance - September 16th, 2022 VBR Pick Performance - September 2nd, 2022 VBR Pick Performance - August 26th, 2022 VBR Pick Performance - August 19th, 2022 VBR Pick Performance - August 12th, 2022 VBR Pick Performance - August 5th, 2022 VBR Pick Performance - July 29th, 2022 VBR Pick Performance - July 22nd, 2022 VBR Pick Performance - July 15th, 2022 VBR Pick Performance - July 8th, 2022 VBR Pick Performance - July 1st, 2022 VBR Pick Performance - June 24th, 2022

Eton Pharmaceuticals

Today, I want to talk about a buy proposition experiencing heavy-volume accumulation based on some positive long-term news for the company. Eton is a small patented-drug company, focused on orphan and rare diseases. This subset is defined as health conditions affecting a minority population of patients, often less than 200,000 a year in the U.S. As such, revenue and profits are harder to deliver to shareholders vs. the blockbuster variety of drugs producing billions in annual sales. So, managers have to really watch spending and investments in this area of medical research.

The good news is niche sectors of medical care, where Eton focuses its attention, have far fewer competitors. For example, in early January Pfizer ( PFE ) announced it was closing or outsourcing most of its orphan and rare disease drug research because the financial accounting profit potential is not worth its time, energy, and capital investment. Returns from larger population diseases and health issues provide a smarter long-term profit incentive.

Anyway, Eton’s equity market capitalization currently is only $88 million, with $13 million in cash held at the end of September vs. $10 million in total liabilities. Wall Street analysts are projecting the company will move from sizable operating losses in 2022 to slight profitability in 2023 as revenues roughly double to $41 million. If present estimates prove out, there will be no need to raise capital for the business as currently configured, assuming cash flow numbers jump markedly in future quarters.

Seeking Alpha Table – Eton Pharmaceuticals, Analyst Estimates for 2022-23, January 15th, 2023

Excuse for Bull Rush of Investor Interest

Eton now sells three FDA-approved products in ALKINDI SPRINKLE , Carglumic Acid tablets, and Betaine Anhydrous for oral solution. In addition, three late-stage pipeline candidates are under development with dehydrated alcohol injection, ZENEO hydrocortisone autoinjector, and ET-400. The company also receives royalties on three FDA-approved inventions and is entitled to receive milestone payments on other products. Essentially, this small outfit runs a relatively diverse asset mix not easily found elsewhere by pharma investors, with new products coming in the next couple of years.

On January 11th, the FDA announced one of Eton’s late-stage inventions would be reviewed and considered for approval by late June,

… the U.S. Food and Drug Administration (FDA) has accepted for review the Company’s New Drug Application (NDA) response for dehydrated alcohol injection for the proposed indication of methanol poisoning. The FDA has assigned a Prescription Drug User Fee Act (PDUFA) target action date of June 27, 2023.

“We are excited to be one step closer to bringing this much needed product to patients and we have begun working with our commercial partner to prepare for a potential near-term launch,” said CEO Sean Brynjelsen .

Eton’s application has previously been granted orphan drug designation for the indication of methanol poisoning and if approved, the Company expects the FDA to grant the application seven years of orphan drug exclusivity. Based on IQVIA data, trailing 12-month sales for dehydrated alcohol injection were $74 million …

Technical Chart Breakout

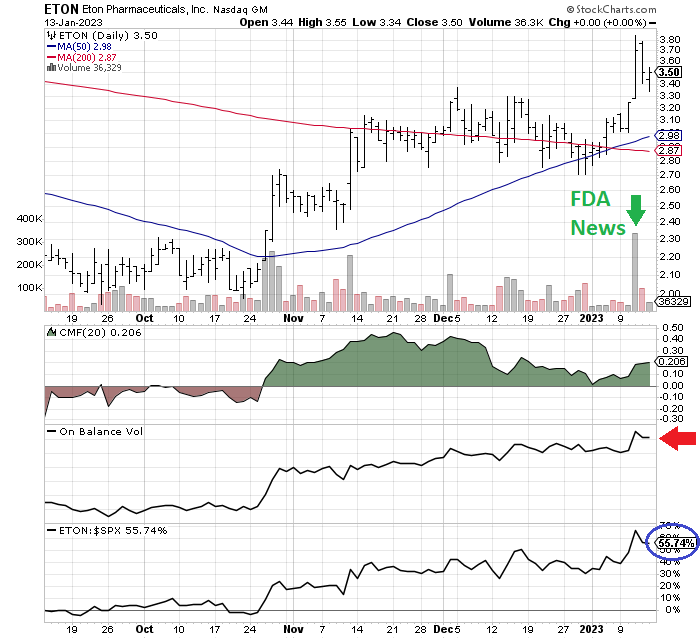

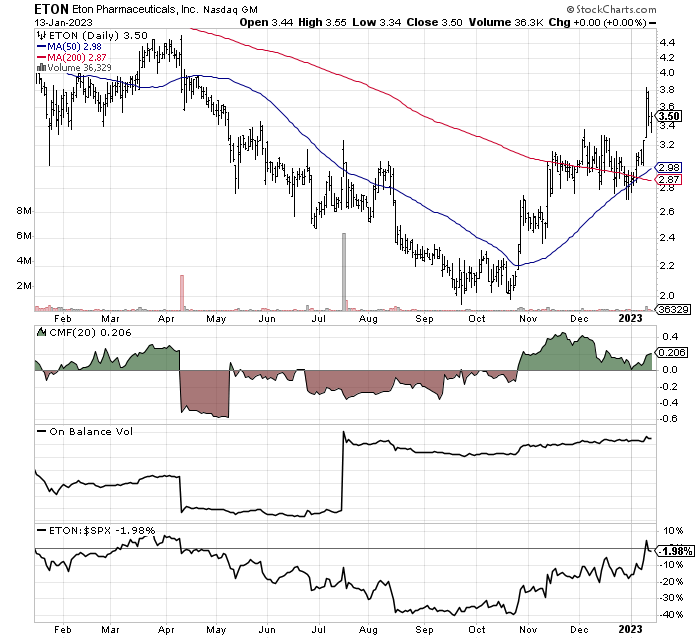

The main reason for my interest - Eton appears to have turned the corner on my trading charts, transitioning from a steady decline in share value and pricing to a rising trend. Over the last four months, upside momentum has been gaining strength off its 52-week low.

On the charts below of daily price and volume changes, you can see price is now above both the 50-day and 200-day moving averages of session closing values (among many other MAs I track). The FDA news from several days ago may be the catalyst to generate even greater gains from today, marked with the green arrow.

The 20-day Chaikin Money Flow reading has been super-positive since late October, which signals buyers have been overwhelming sellers for order flow. On Balance Volume has been a straight line moving in the bullish direction (red arrow). Plus, relative price strength vs. the S&P 500 has been outstanding, at a rate +55% better (blue circle) measured from the middle of September.

StockCharts.com - Eton Pharmaceuticals, Daily Price & Volume Changes, Author Reference Points, 4 Months StockCharts.com - Eton Pharmaceuticals, Daily Price & Volume Changes, 12 Months

{kind=link}

{kind=link}

Eton Roundup

My thinking is a diverse product-mix company with a new drug approval on the horizon, forecast to outline strong revenue growth and earnings growth, is worth far more than an enterprise value of $80 million. If sales during 2024 are $60 million and EPS in the $0.30 to $0.50 area, a clear path to a double or more from today’s $3.50 share quote exists in calendar 2023.

Eton’s CEO purchased 10,000 shares at $2.10 near the low of the year in September. There have been no other insider trades reported to the SEC over the past 12 months.

Seeking Alpha’s Quant Rank is now top notch, with an #82 position out of a universe of 4767 equities. Momentum building in its chart pattern and operating results beating analyst expectations during late 2022 are the reasons.

Seeking Alpha Table - Eton Pharmaceuticals Quant Rank, December 15th, 2023

What are the risks? The first one that comes to mind is the June FDA announcement may not be a decision of full approval for its dehydrated alcohol injection for methanol poisoning. Other risks include potentially weaker sales of existing drugs than expected, which can be hard to predict in advance. The discovery of adverse drug reactions and lawsuits over side effects are always lingering risks in the drug sector. Eton was trying to enter a new market, but lost a patent trial last year. And, the company does add new assets on occasion (through cash, debt and equity changes).

In the end, operating risks are the ones I consider most likely to keep the share price down. The company is so small and its products laser-focused on rare diseases, I do not really worry about general stock market direction or recession forecasts as having an outsized effect on Eton’s future.

I am modeling theoretical downside in price back to $2.50 per share, if the new drug application is rejected this summer. A diverse and expanding list of drugs on the market, with royalties received from various products sold by outside organizations, gives Eton a better foundation than peers in the medicine industry mostly riding a single product or two for operating results.

Upside could be in the $7 to $10 range in 12-18 months, if the treatment for methanol poisoning is approved by the FDA and sales for this product and other drugs impress on the upside. In conclusion, my risk/reward analysis balances theoretical total return downside of -30% against upside in the +100% or stronger range for calendar 2023. I rate Eton Pharmaceutical shares a Buy .

Final Thoughts

I am working overtime improving my quant-sorting formulas (actually creating many new ones as variations) that may be used in future Volume Breakout Reports, all an effort to better locate the really big winners while eliminating more of the losers. I have traded a large number of the new picks as tests, without writing about them. My goal is to eventually bring back more VBR articles, or perhaps even start a newsletter product on Seeking Alpha focused on the idea. We will see where 2023 leads me.

I continue to own (or may trade this upcoming week) as many as 10 equities on previous VBR lists. Exceptionally positive share price changes in Broadwind ( BWEN ) and CVD Equipment ( CVV ) over the past week have appeared on growing "green energy" demand for their products. Having a few large gainers is important to portfolio progress and is one of the goals of my research in the small-cap area of Wall Street.

For stat geeks, the "median" average gain for the VBR choices is closer to +0.9% vs. the +5.9% mean. Basically, having outlier gainers is what generates the outperformance. For a distribution, greater than +10% gainers have numbered 17, measured against -10% or worse returns from 14 picks. Again, theoretically cutting losses with stop orders at a generic 30% level would have improved overall average total returns by about 0.8% to +6.7% for a mean average.

If new to the Volume Breakout Report series, you can read previous articles to get a better understanding of this research effort. The July 9th update is a good place to start, with strategies on how to use VBR picks. High-volume advances in price are just one part of the system and proprietary formulas. An old Wall Street adage is “volume precedes price.” Daily computer searches that utilize as many as 15 indicators of technical trading momentum are ranked against thousands of equities, to find the best opportunities. Then, a review of company fundamentals and growth prospects narrows each list to the picks I write about.

A diversified basket of selections (at least 20-30 names) is the smartest way to reduce portfolio risk, as smaller companies can experience wild price swings. All told, minor dollar trading amounts are able to move marketplace equilibrium quickly. By the time good news events are released to the public, insiders and knowledgeable long-term investors in each company have often purchased shares before the typical retail investor can act. The VBR is an early signal tool for investors looking for a trading edge.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

Volume Breakout Report Update: Buy Eton Pharmaceuticals