WBD - Warner Bros. Discovery Q3 Earnings Show Progress But It's Still Not A Buy

2023-11-08 09:15:35 ET

Summary

- Warner Bros. Discovery, Inc. has delivered consistent progress in recent quarters, with sustained free cash flow growth driven by improved scale in the direct-to-consumer business to compensate for secular declines in linear TV.

- Despite the slight earnings miss, the company grew adjusted EBITDA by 22% y/y, with free cash flows exceeding $2 billion in Q3, which is supportive of its deleveraging goals.

- While it's still a race against time to scale DTC opportunities and offset accelerating linear TV declines, the Q3 results lessen concerns over the achievability of Warner's near-term financial targets.

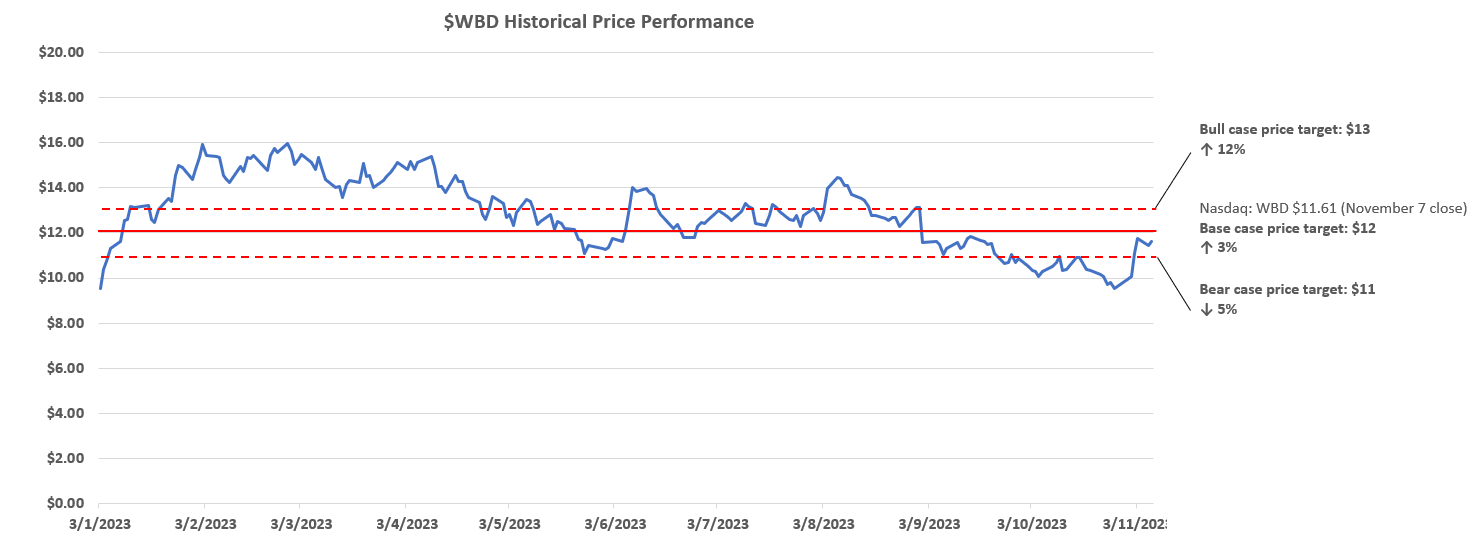

Warner Bros. Discovery, Inc. ( WBD ) stock has posted a steep rebound in recent weeks, highlighting its sensitivity to changes in the rate environment – and reasonably so, given its highly leveraged capital structure. Although much of WBD’s debt is at a fixed rate, which partially shields the company from recent fluctuations in the borrowing cost environment, its highly leveraged balance sheet continues to subject the stock to an elevated risk profile and, accordingly, multiple compression risks stemming from ongoing macroeconomic uncertainties, nonetheless.

But WBDs Q3 results continues its streak of tangible fundamental improvements in recent quarters, especially on free cash flows critical to hitting its deleveraging goals (< 4x gross leverage by end of 2023; 2.5x to 3x gross leverage by end of 2024). While the cord-cutting trend continues to impact its core linear networks business, WBD’s progress in driving the direct-to-consumer (“DTC”) segment to sustained adjusted EBITDA breakeven is expected to bring some alleviation to its bottom-line within the near-term. We expect the addition to live sports content to the Max streaming service, alongside the continued ramp-up of ad sales to be key drivers of DTC margin expansion at scale over the longer-term.

However, it remains a tough endeavor for WBD to find balance between intensifying streaming subscription and ad sales competition amid ongoing macroeconomic impacts on the consumer, and accelerating secular declines in the core linear TV business. Coupled with the company’s highly leveraged balance sheet still, execution risks remain on deck. As the elevated cost of capital in recent quarters is offset by continued fundamental improvements observed at the company, we remain hold-rated, with our base case price target unchanged at $12. Achieving its target of under 4x gross leverage by the end of the year, and between 2.5x to 3x by the end of next year, alongside sustained DTC segment breakeven will be critical next steps to unlocking incremental upside potential for the stock.

Cash Flows in Focus

WBD has continued to make progress in expanding its free cash flows critical to supporting its ongoing deleveraging goals, while also ensuring a balanced growth investment profile to scale the increasingly competitive DTC business. Specifically, the company generated $2+ billion in free cash flows in Q3 , up 18% from $1.7 billion in Q2 and a substantial improvement from -$930 million in Q1. This has contributed to incremental debt payments in the third quarter, bringing total repayments to $11.8 billion since the merger completed in April 2022.

Much of the improvements continue to be driven by disciplined spend management and continued scale of DTC opportunities and seasonal sports broadcasting tailwinds, offset by continued lumpiness in studios segment revenues, as well as secular declines in the linear networks business. This has resulted in adjusted EBITDA of almost $3 billion in Q3, up from $2.1 billion in Q2, which tracks favorably to management’s revised guidance for the metric of between $10.5 billion to $11 billion due to impacts from the Hollywood strikes.

Studios

The flood of Barbie and Ken costumes during Halloween 2023 is almost reflective of the Squid Game phenomenon in 2021, which largely marked Netflix’s ( NFLX ) inflection from the post-pandemic slowdown. This has largely translated to the expected studios segment outperformance during the quarter, though the results have likely been considered in the stock at current levels already. The segment’s revenue grew 4% y/y to $3.2 billion in Q3, which drove adjusted EBITDA expansion of more than two-fold sequentially to $727 million during the same period.

However, the results continue to highlight the inherent lumpiness of revenue recognition for the segment. For instance, Dune: Part 2 would have set the beat for WBD’s Q4 results, given its originally planned release for November 2023. But the ongoing Hollywood strikes have delayed the picture’s release to March 2024 instead, which we see as one of the offsetting factors that is poised to limit near-term upside potential for the stock.

Looking ahead, we expect the studios segment to remain a key contributor to WBD’s cash flows despite its inherently lumpy pace of revenue recognition. Albeit a volatile growth profile, studios segment revenues are expected to be primarily driven by content and distribution sales, in line with management’s intentions to optimize the windowing strategy on tentpole IPs. This is expected to maintain scale for the segment, and contribute to steady, though modest, expansion in adjusted EBITDA at a five-year CAGR of 0.8%.

{kind=link}

Linear Networks

Meanwhile, the linear networks segment continues to show increasing signs of impact from the cord-cutting trend as expected. Networks revenue dropped -7% y/y in Q3 to $4.9 BILLION, led primarily by weakness in the segment’s core advertising sales due to the combination of cyclical and secular headwinds. Specifically, cord-cutting is expected to outpace the rate of linear TV subscription adds “for the first time” this year, highlighting accelerated deterioration in WBD’s core cash generator, which dials up the urgency to drive scale in the compensating DTC business. This is in line with current market forecasts that predict a -7% y/y decline in “non-cyclical linear ad sales” (i.e., ex-summer Olympics and Presidential election impact) in 2024, which harbingers a headwind to both volumes and pricing at WBD’s next upfront.

However, the return of the fall sports season has likely helped mitigate some of the impact on Q3 results (offset by weakness in sports sublicensing in international markets) and keep the current quarter’s prospects in check for now. This is largely consistent with expectations given improved volumes and prices at WBD’s recently completed upfront in the U.S., despite the soft ad demand backdrop due to the industry’s inherent sensitivity to macroeconomic uncertainties. Taken together, we expect linear networks revenue to decline at a five-year CAGR of -2.2%, driven primarily by an average annual decline of -3.9% in advertising sales over the forecast period. This will accordingly drive an average -2.0% annual headwind to adjusted EBITDA in the networks segment, which in our opinion keeps WBD’s execution risks elevated due to the heightened urgency to scale its DTC opportunities.

{kind=link}

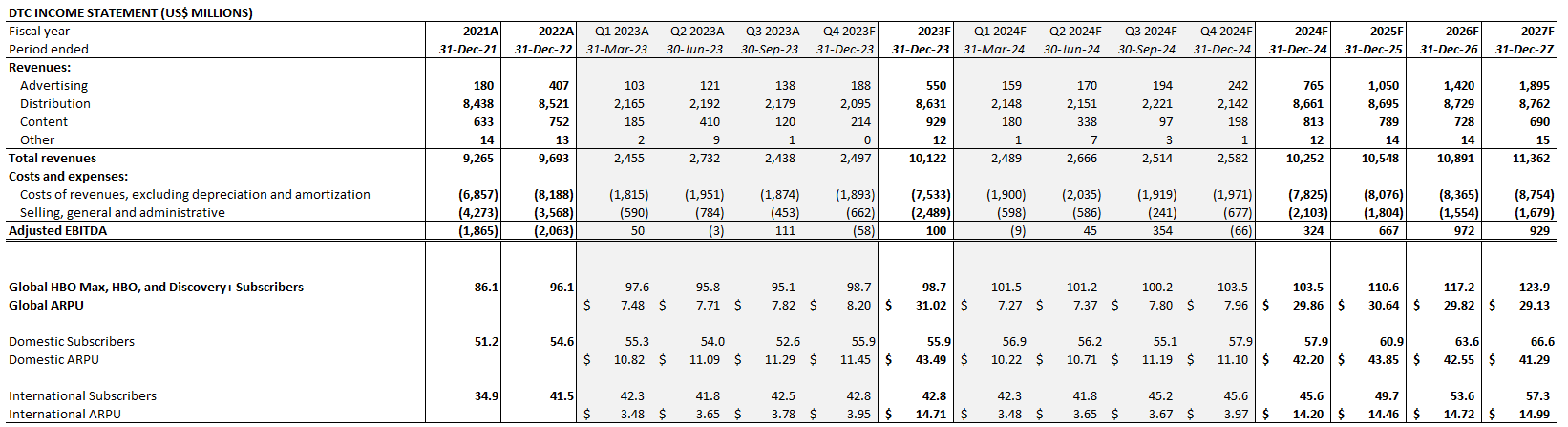

DTC

The DTC segment continues to progress positively, which is in line with our foregoing analysis that the pickup in pace of secular declines in linear TV has heightened the urgency for a compensating cash flow stream. And WBD has continued to deliver results on this front in Q3, assuaging some of investors’ concerns over the visibility of its longer-term growth trajectory.

The segment posted 700,000 global paid subscriber net losses in Q3, driven primarily by moderation in domestic market demand, offset by resilience in international markets. Global paid subscribers totaled 95.1 million at the end of Q3, which is largely in line with expectations given the recent completion of tentpole content such as Succession and The Last of Us, alongside the continued impact of churn related to the combination of Discovery+ and HBO Max into Max. Looking ahead, paid subscriptions are likely to get a boost in the current period with the potential launch of Barbie in Max later this month , alongside the integration of live sports content introduced earlier this month.

Specifically, WBD has added a Bleacher Report Sports Add-On service starting October 5 for current U.S. subscribers at no additional charge through the end of February 2024. The live sports tier will include “live events from MLB, the NHL, the NBA, NCAA [March Madness], and U.S. soccer.” After the free trial period, the add-on will be priced at an additional $9.99 per month on top of any base Max subscription – which starts at $9.99 for the ad-supported tier. The latest development continues to highlight the fundamental role that sports plays in attracting viewership and, inadvertently, engagement critical to adjacent ad sales.

Sports programming have continued to be a fundamental lifeline to linear TV viewership and ad performance despite secular declines, which highlights the latest B/R Sports Add-On feature’s potential for complementing Max’s increasing reach to consumers. This also marks a key strategy and competitive advantage for WBD, given its ability to leverage existing sports rights to fend off emerging rival streaming services from deep-pocket big tech players like Apple ( AAPL ), which has also observed market share gains from its recent offer of the MLS Season Pass .

We expect resilient consumer demand for sports content to be key in mitigating impending recession risks on the DTC segment’s near-term prospects as well. Specifically, American households are already subscribed to 3.7 streaming services on average, fueled primarily by a combination of cord-cutting dollars moving online and the increasing availability of different platforms to choose from. Meanwhile, intensifying competition is also coupled with deteriorating household income and savings , tightening credit conditions, and ballooning household debt in WBD’s core U.S. market, which further limits the amount of discretionary income that consumers can allocate to the ever-growing number of streaming platforms available. But we view the addition of live sports content to Max as a key compensating strategy to the looming competitive and macroeconomic headwinds – especially with the almost six-months free go-to-market strategy likely to increase the paid subscription base and complement price increases implemented earlier this year.

The anticipated tailwinds to paid subscriptions is also expected to bolster DTC ad sales – which is the bread and butter of the business. DTC ad sales grew 30% y/y to $138 million in Q3, with continued acceleration underscoring adequate capture of rolling-off linear ad dollars, in addition to emerging digital ad opportunities. This is also consistent with management’s disclosure of DTC ad volume improvements in recent quarters, which was up 50% y/y in the marketplace as reported in the first half of the year, with cost-per-mille (“CPM”) improvements “positioned to drive scale” for WBD over the longer-term. The results were also in line with continued secular tailwinds observed in AVOD ad demand, which is predicted to expand by 12% y/y in 2023 and 11% y/y in 2024.

We also expect incremental tailwinds from the recent price increase implemented by Discovery+ for the first time since its launch in 2021. The service’s monthly subscription rate has increased by almost 30% from $6.99 to $8.99 for the ad-free tier, while the ad-supported tier’s monthly rate remains unchanged at $4.99. The price increase is expected to be a key compensating factor for anticipated churn coming out of the addition of Discovery content into Max earlier this year. Recall that Discovery+ is already profitable, which means the latest price increases are expected to be accretive to profit margins and contribute further to the DTC segment’s roadmap to sustained positive adjusted EBITDA.

Taken together, we expect a more evident impact on P&L growth in 2024 as ad demand and paid subscriptions ensuing from the newly introduced B/R Sports Add-On and Discovery+ price increases continue to scale alongside existing Discovery+ and Max offerings. This is expected to be critical in supporting DTC segment adjusted EBITDA breakeven, which management expects to become more durable in 2024. Although the segment is not expected to be GAAP-based profitable and self-sufficient for a while longer, achieving sustained adjusted EBITDA breakeven remains a key milestone that brings some alleviation to the capital-intensive transition from linear to streaming, nonetheless. We think the next key focus area will be on the durability of this achievement, which will be reinforced by continued scale of subscription adds and DTC ad sales to offset the relevant growth costs – particularly on sports rights integration and content investments.

{kind=link}

Fundamental and Valuation Considerations

Taken together, we expect net improvements to WBD’s return-on-capital profile. This will be key to reinforcing its cash flow growth story and lessening concerns that brewing consumer weakness and secular declines in the core linear networks business could disrupt the company’s deleveraging target of 2.5x to 3x gross leverage by the end of 2024.

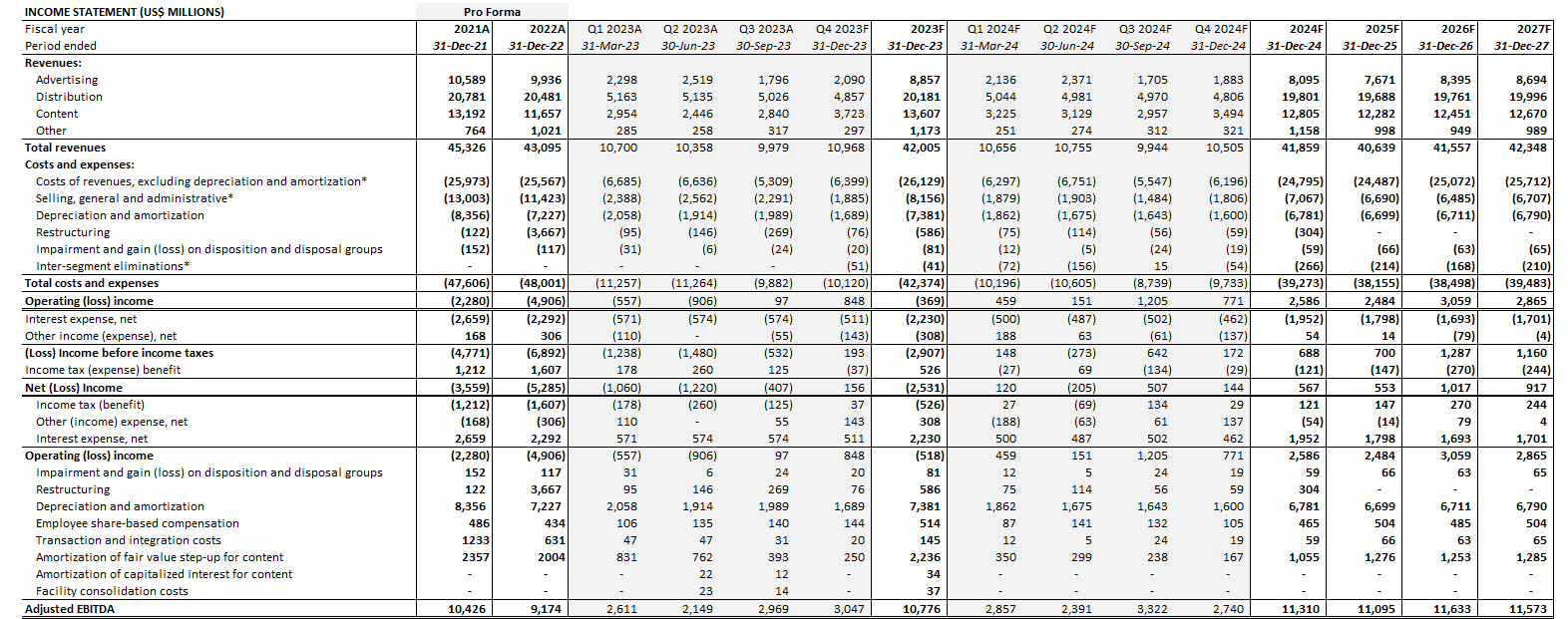

Adjusting our previous forecast for WBD’s actual Q3 performance and forward prospects based on the foregoing discussion, we expect a slowed revenue decline of -2.5% y/y to $42.0 billion for full year 2023, alongside adjusted EBITDA of $10.8 billion in line with management’s guidance. And over the longer-term, we expect modest revenue growth at a 0.2% five-year CAGR through 2027, with improving scale at the DTC and studios segments to drive operating leverage and adjusted EBITDA expansion at an annual average rate of 1.4% over the forecast period.

{kind=link}

Warner_Bros._Discovery_-_Forecasted_Financial_Information.pdf

We are maintaining our base case price target of $12 for Warner Bros. Discovery, Inc. stock. Despite the elevated risk-free normalized rate environment, we see WBD’s improving cash flows and progress to deleveraging its balance sheet as an offsetting factor. However, we remain mindful of allocating an incremental premium to the stock’s current levels given execution risks remain. Specifically, Warner Bros. Discovery, Inc. has yet to demonstrate a company-specific competitive advantage in ensuring DTC market share gains can scale faster than the pace of secular declines in linear TV, and overcoming intensifying competition in the market.

{kind=link}

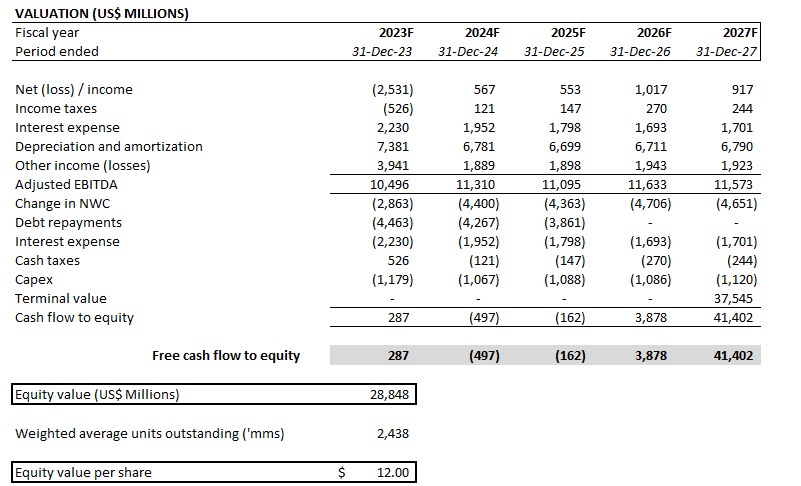

Our base case price target of $12 is computed under the discounted cash flow approach, which takes into consideration projections made in conjunction with our fundamental forecast for WBD as discussed in the foregoing section. A WACC of 11.9% is applied in line with WBD’s capital structure and risk profile relative to an upward adjusted normalized risk-free rate environment. The terminal value is determined by a 1.5% implied perpetual growth rate in line with the company’s prospects relative to the pace of economic expansion within its core operating regions.

{kind=link}

Final Thoughts

Admittedly, Warner Bros. Discovery, Inc. has made consistent progress in growing cash flows and contributing to its deleveraging target in recent quarters despite ongoing macroeconomic and industry-specific headwinds such as the Hollywood strikes. Notable areas coming out of its Q3 earnings include DTC’s continued growth at scale, which is driving margin improvements and putting sustained adjusted EBITDA breakeven within sight. Although lumpiness in studios revenue recognition remains given its uncertain content slate, which has been exacerbated by the ongoing SAG-AFTRA strike, the Barbie phenomenon observed over the summer is expected to remain a lifeline for now. Specifically, the application of the traditional windowing strategy on the title – in line with expectations for Barbie’s potential launch on Max later this month – is likely to keep the segment’s prospects afloat leading up to the release of Dune: Part Two in theatres in March 2024.

However, this does not mean the stock is totally out of the woods yet. While Q3 underscores progressions in the right direction to offset accelerating declines in the traditional linear business, there is still much work left to do at WBD to ensure sufficient and sustained cash flow generation critical to supporting not only its deleveraging goals, but also the company’s longer-term growth opportunities. As a result, we see limited near-term upside potential for the stock at current levels, as investors are likely looking to build confidence on further evidence supportive of sustained DTC breakeven and deleveraging progress in later 2024.

For further details see:

Warner Bros. Discovery Q3 Earnings Show Progress, But It's Still Not A Buy