WBD - Warner Bros. Discovery: Seriously Undervalued Media Giant With A Great Entry Point

2023-12-11 11:01:19 ET

Summary

- Mario Gabelli's stock picks in the media/entertainment sector had mixed results, with one stock increasing and the other decreasing in value.

- Warner Bros. Discovery, Inc. is focused on reducing debt and cutting costs, while Paramount Global is facing uncertainty due to potential sales.

- Warner Bros. Discovery, Inc.'s long-term outlook is positive, with potential for doubling or tripling its stock valuation.

The blessed memory of the late Mr. Charlie Munger moves us to quote from his treasure chest of common sense acquired over years of spectacular returns with partner Warren Buffett.

“Without the method of learning you’re like a one-legged man in an ass-kicking contest. It’s just not going to work very well….”

Examining all the methods of learning about how to make the most possible money in the stock market over time, one inevitably comes upon a single conclusion: Think of the business as a business first, not a set of metrics about a given stock which do not always reflect true value . If you do, you are clearly ass-kicking with two legs.

Reviewing the media/entertainment stocks for a client I have gone through a veritable Tower of Babel of data and opinion from many sources including SA. Some of it has been very thoughtful, some of it just more blah blah between endless graphs and charts.

Mr. Mario Gabelli weighed in last January when Barron’s asked him and other top analysts for their top forward picks for 2023. Among his choices were two in the media/entertainment sector.

Here are his picks and the results measured by 6/30/23:

Company 1/30/23 6/30/23 +(-) %

WBD $11.32 $12.54 10.8%

Paramount Global 19.33 15.91 (16.4%)

We cite this as an example of the perception of a highly successful stock picker over time. Clearly Gabelli could not have known about what lay ahead for Paramount Global (PARA) this week.

His thesis last January: Warner Bros. Discovery, Inc. (WBD) has repaid $12b in debt hung on them from the AT&T (T) debacle, standing now at $44.8b. This, plus the relentless cost cutting that has included movie and show cancellations, is the key basis for Gabelli believing the stock could double or triple within the next 3 years. He rightly saw WBD as a transaction-focused company up ahead.

Paramount remained mired in far too many questions about the intentions of Shari Redstone until this month. Rumblings about the possible sale of the company to operators Red Bird Capital and/or Skydance Media surfaced just this week sending the shares up over 16% to $16.85. The market now presumes those would-be buyers would seek to unload much of Para’s verticals and just hold on to the studio.

At the same time, WBD traded at last closing at $11.47 flat to the Gabelli call last January. And that is precisely where our high-conviction strong buy guidance on WBD is based. Gabelli saw value in the company’s serious pursuit of cost controls and balance sheet clean-up. WBD has an enterprise value at this writing of $70b. Prior to last week’s news, the Para price action since January was negative.

WBD, on the other hand, does not appear to be gaining positive sentiment regardless of its success in rationalizing its verticals and slashing its debt. This is why we believe the market is lagging in recognizing WBD as cheap in the hands of a management tightly focused on bringing order to the chaotic AT&T mess it inherited.

3Q23 highlights have won little market enthusiasm thus far

- Revenue: $9.979m up 1% y/y (ex-FX)

- Net loss $(417) mostly linked to non-recurring costs relating to amortization including $269m of lingering acquisition expenses. Total one-time costs $1.758b.

- FCF: $2.059b

- The company repaid $2.4b in debt in the quarter bringing its total long-term debt to ~the aforementioned $44b.

- Its global streaming customer base was essentially flat with an ARPU of $7.82 a 6.6% increase y/y (ex-FX).

- Barbie : The blockbuster grosses hit $1.5b, the single highest revenue of any WB film in its entire history.

- 4.2X net leverage with $2.4b cash on hand that will grow.

- Zaslav and Malone believe 2024 will produce $5b in FCF.

- The average weighted cost of debt for WBD is 6.4% with maturities stretched out to 2062. So the attack strategy against the debt burden makes great sense here.

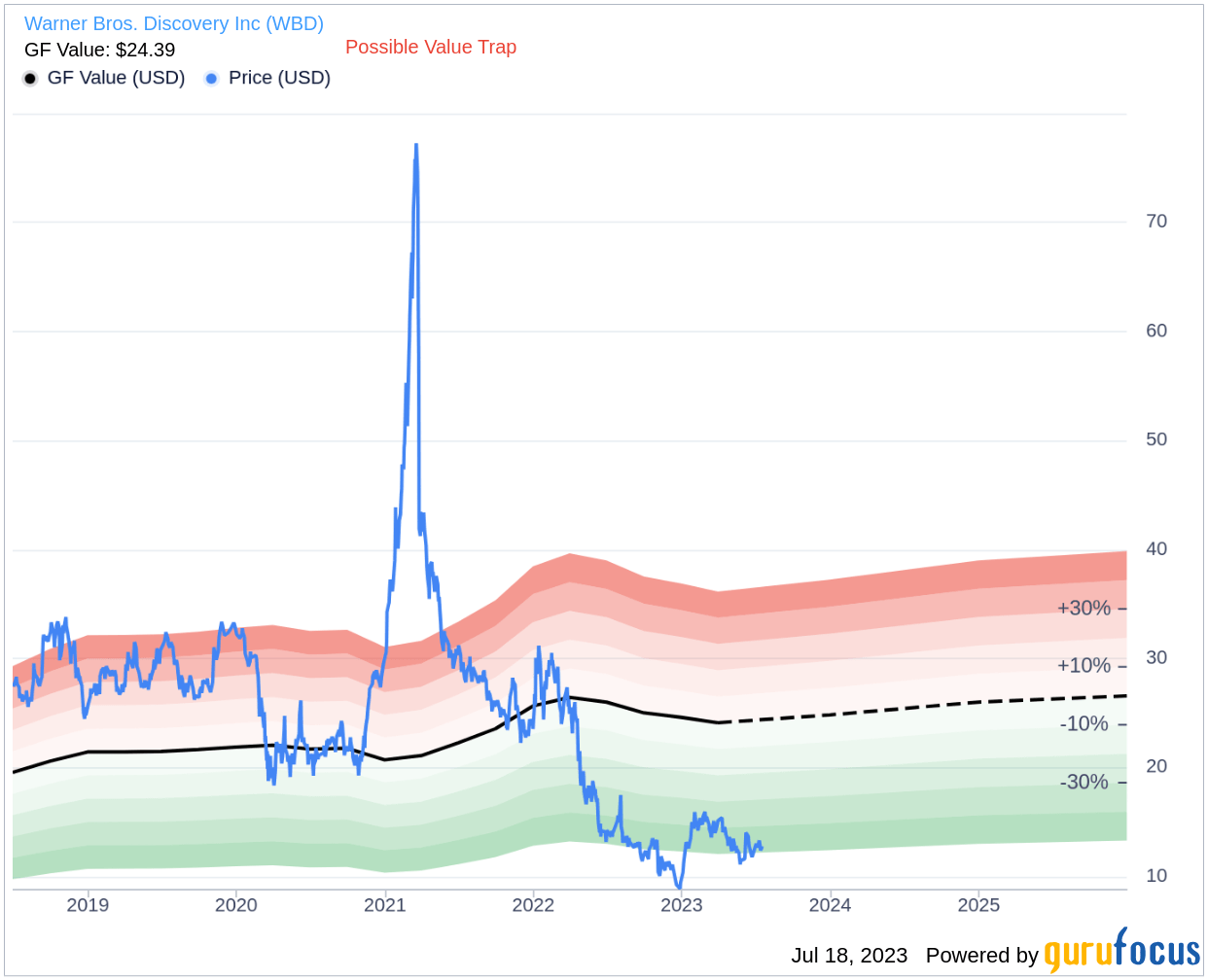

{kind=link}

Above: A fallen angel or a Phoenix about to rise from the ashes that still gets little love from Mr. Market.

The point is that with every $2b WBD can repay, they are saving ~$120m in cash theoretically falling to the bottom line. Compare that to say a competitor focused on streaming growth scores 1m new subs in a quarter that Mr. Market gets giddy about and bids up the shares. At an average monthly value of say $7 that comes to $84m gross per year with an unknown churn rate after the opening special price subscription expires.

Clearly the sex appeal in the sector arises from either rising numbers of streaming customer news, e.g., Disney ( DIS ). or intimations of a deal, i.e., Para last week. Even the Barbie blockbuster was not enough to spike the trading range of WBD out of its dead pool range since the start of the year.

What’s the point the market may be missing here?

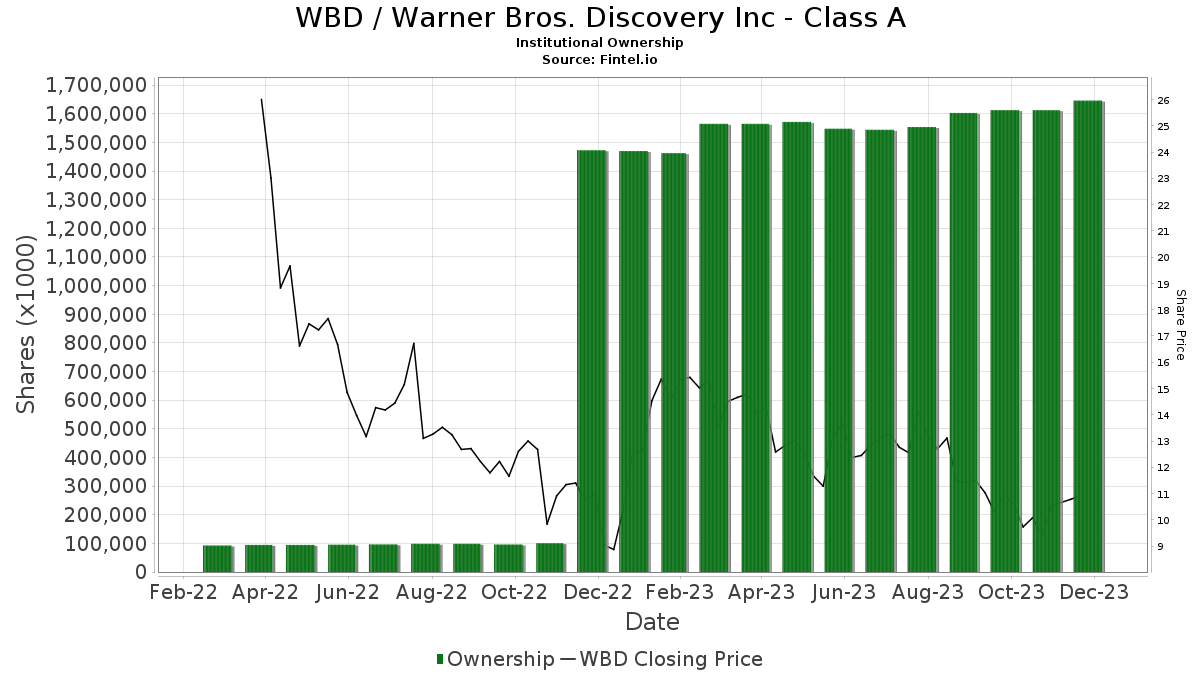

{kind=link}

Above: Clear proof that the market either doesn't like nor get the WBD story as laid out by Zaslav and Malone.

Whether you buy into the WBD strategy or not, here’s the clear goal expressed by CEO Zaslav and his partner, Liberty Media’s John Malone.

The prime WBD focus will be slashing costs and reducing debt to bring its FCF up and debt service cost down. They believe that valuations in the media/entertainment sector will continue to be cheap for a deep pocketed acquirer. The possible move on Para proved this point this week.

So what Messers Zaslav and Malone see is a WBD flush with cash, with a far more solid debt profile going into the market and scooping up companies and adding to their scale at cheap prices. It’s a transactional mentality versus what we believe to be a wishful thinking goal among many streamers. One sees from sector competitors a vision not entirely shared by WBD as a nirvana in creating new content “our customers will love ” at lower costs as do competitors.

I also see WBD unloading some of its present verticals in exchange for new ones bought at knockdown prices. There will be skeptical investors who may think of this strategy as a smoke screen by Zaslav and Malone. They could see an effort to hide the fact that they have few other choices. It may be one way to keep the stock from falling even lower. But thinking this through, we cannot see any long term recovery in valuations of media verticals. If WBD is right, and valuations remain cheap, they clearly have the best shot in the sector to move their shares big time long term from its present low.

WBD appears also to be stuck with many overhanging, overvalued verticals from the AT&T mess. But given the hard truth of what the sector is facing in the out years from rising costs, AI challenges, etc. we come down to this simple question:

{kind=link}

Above: The big guys apparently get it despite the swoon in valuations.

Do consumers really need 600 streaming shows to choose from every day?

Question one : Right now, there are about 600 programs available on streaming services. Yes, they cover the gamut of every conceivable genre and sub-genre. They also offer countless documentaries, cooking shows, tons of sports, old movies, new movies, good movies, bad movies, studio products and the all too often inane TV product of too many independent producers who probably should be bagging groceries for a living given their terrible output on the services. How many crime shows featuring detectives with messed-up personal lives who still soldier on to catch the bad guys can viewers endure?

So, the logic of 600 programs on at any given time escapes me. Yes, I realize it’s all a game hoping that having so much product will result in your never having to miss a pair of eyeballs looking to focus on some esoteric genre. It’s the old throwing, you know, what against the wall hoping something would stick marketing dead end at work here.

How many of those shows are dogs with fleas we don’t know about because the streamers don’t disclose viewing numbers? (They will have to under the new WGA contract). How many shows and movies were green-lit with DEI agendas that vastly underperformed? We are told by industry insiders they are many. But that’s a discussion for another forum. What is key here is that salvation for the streamers seems a tough contract to spring just from new, cheaper to produce, compelling content. WBD is already content rich and can buy new IP at cheaper prices into the intermediate term at least.

We like the reality-based long-term outlook of Warner Bros. Discovery, Inc. It makes a strong case for a future that could hold the doubling or tripling of the valuation of WBD stock that Gabelli has posited last January.

We’re looking at a revised price target of $19.75 before the end of 1Q24 supported by improving earnings, an even stronger debt profile, and a near doubling of free cash flow for the year.

For further details see:

Warner Bros. Discovery: Seriously Undervalued Media Giant With A Great Entry Point