WBD - Warner Bros. Discovery: The Economics Of Streaming Will Get A Lot Better

2023-10-06 04:52:51 ET

Summary

- Streaming economics will improve over time through increases in subscriber prices, longer-term plans to reduce churn, and reduced growth in content spend.

- Warner Bros. Discovery has best-in-class content and one of the most comprehensive streaming options in the market, making it well positioned for the shift to streaming.

- The decline of linear will eventually start to matter less as cable and streaming become more comparable in terms of value.

- The ad market will eventually recover.

- This might take years to play out, but I expect that patience will be rewarded for WBD investors.

Investment Thesis

Streaming is more than a decade old but still has a long way to go as far as how the economics of the business could evolve. The cost to consumers of streaming is paltry and unhinged from the value that it provides. If there was no reason for that to change, then depressed valuations in the sector would be warranted. But there are already changes underway, with subscription price increases and re-bundling just being the first indications of what's possible in the long term.

Warner Bros. Discovery Inc. ( WBD ) is well-positioned for what's to come. The timeline might be longer than what a short-sighted market would prefer, but as far as I can tell, Max 's combination and depth of scripted, unscripted, news , and sports , makes it one of the more, if not the most, complete streaming options. Recent operational improvements with the merger, breakeven or cash flow positivity with D2C already in 2023H1, long-term fixed-rate debt , and the continued stock price pullback make WBD a buying opportunity, in my opinion.

Present and Future Improvements in Streaming Economics

Streaming has been much maligned for its high levels of churn, unprofitability, and vulnerability to the dominance of Netflix ( NFLX

) and Big Tech. But many major services have only been in their current form for a few years or less.

With subscriber levels plateauing, t

he following developments in pursuit of profitability have already been unfolding, or have

been discussed in calls and commentary

:

- Further increases in streaming prices , particularly month-to-month.

- Re-bundling of a given company's separate services (e.g., WBD's Max, Paramount's ( PARA ) Showtime and Paramount+ ).

- Crack-downs on account sharing.

- Introduction of ad tiers.

- The licensing of content to other platforms.

- Less promotional effort to boost subscriber counts.

- Moving beyond peak investment .

- Industry consolidation through M&A .

This suggests a strong appetite to improve profitability, multiple levers to use, alignment across the industry, and a live-and-let-live attitude. In the case of churn, it wasn't a priority to address this during the high growth phase of streaming. But higher monthly subscriptions (versus an annual plan) are an obvious first measure to incentivize more subscriber commitment:

Generally, what you'll see from us is more upward pressure on the monthly subscriptions, trying to get people to commit for the longer term because you still have this weird dynamic whereby you could sign up for a subscription VOD service today and spend two or three weeks, you're going through an enormous amount of content and then move on. That's something that I think the entire industry is aligned in their incentives to work on that.

- CFO Gunnar Wiedenfels , September 2023

All of the above points to improvements in industry economics over time. But it probably won't stop there. Looking further over the next decade, the evolution of streaming could extend to the following:

- Re-bundling across services of different companies.

- Increased ads. Ad-lite options often only have around 4 minutes per hour (e.g., Disney ( DIS ), WBD ) -- much less than linear.

- An outright end to month-to-month subscriptions, whereby subscribers can only sign up for a year or more to some tiers.

- Enhanced tiers of access, e.g., where more content like premium sports and newly-added movies are add-ons, or where a basic subscription only covers new/recent content, and the back-catalogue requires a higher tier.

Admittedly, if subscription prices keep going up and/or plans become locked-in, consumers would likely reduce their number of services, on average. But once consumers are more incentivized to stick around longer, it should be easier to get content spend under control. Even with the biggest content glut in history, North American consumers have often subscribed to 4-7 streaming services -- they are so cheap that you could forget you had half of them. Higher prices and less content leads to another possibility -- re-bundling:

The unbundling comes at a price from the perspective of the user experience or the viewer experience. So I do think consumers would benefit from some form of rebundling. And I think a lot of people are thinking about that, and there are a lot of different models how that could be set up.

I think it's going to be -- that's not an easy thing to pull off. There are so many questions on how exactly you would structure a product like that, how exactly you would structure the economics. It's very hard to get perfectly aligned interests in a setup like that.

So I do think it's compelling to think about some form of rebundling, but I don't think it's an easy thing to pull off, and I certainly don't expect anything to happen short term here.

- CFO Gunnar Wiedenfels , May 2023

Maybe not all of this will happen, and it won't happen in the near future. Each competitor will keep an eye on what others are doing, as is usually the case. However, it points to a lot of room for improved economics down the road. Skeptics might point to Netflix as the disruptor that will continue to resist such changes. But Netflix has already changed its tune with advertising and password sharing . As the competition like WBD hits its stride, and especially if Netflix subscriber growth remains slow and its stock price stagnates, I expect that it will follow suit, as well.

As streaming prices increase and cable adds more streaming to its bundles, the two may eventually become more comparable, value-wise, somewhere in the middle between where the two are currently. The decline of cable will either slow down and/or start to not matter any more for legacy media, relative to streaming. Even if this means less profitability relative to the heyday of cable, this can perhaps be partially offset by the global opportunity of streaming, and should be put in context of WBD's depressed stock price.

The Market Can't Tell the Difference Between Secular and Cyclical Factors

Pessimistic views of WBD and other media companies often don't bother to mention the cyclical nature of the advertising

downturn

that started roughly a year ago. This ad market downturn has been leading up to the longest-anticipated recession that I can remember -- one that might not even occur

. Whether it's because of momentum-based trading, short-term market incentives, the fear of other peoples fear, or just obliviousness, cyclical downturns seem to often get priced as if they're quasi-permanent.

Given the disruption in the industry, though, one can still wonder if there has suddenly been a permanent reallocation of advertising dollars elsewhere. A few reasons suggest otherwise:

- The entire media sector has been similarly affected .

- The ad market was already recovering, coming out of the pandemic, before stalling.

- Ad market pullbacks are the norm in the lead-up to a recession. The current pullback is not unusual given the level of macroeconomic uncertainty.

- Online advertising companies like Meta ( META ) and Google ( GOOGL ) have reported a recovery in revenues. But this has apparently come at the expense of lower selling prices and arguably ad quality and user experience .

- Digital ads seem to cater to a lower bar of advertisers, on average (including annoying pop-up ads, clickbait, etc.).

- Marketing budgets dipped from 2022 to 2023, from 9.5% to 9.1% of company budgets in North America and parts of Europe, versus pre-Covid levels of close to 11%.

- Digital ads tend to fare better in a downturn because of being lower in the marketing funnel , i.e., closer to conversion into a sale.

Top-of-funnel ad campaigns to build brand awareness are longer-term investments, with harder-to-measure results, but help to drive the effectiveness of the rest of the funnel. For example, it might be hard to tell if a car is "desirable" purely from a digital ad, but through prior brand awareness the digital ad could be effective.

Observations on Valuation

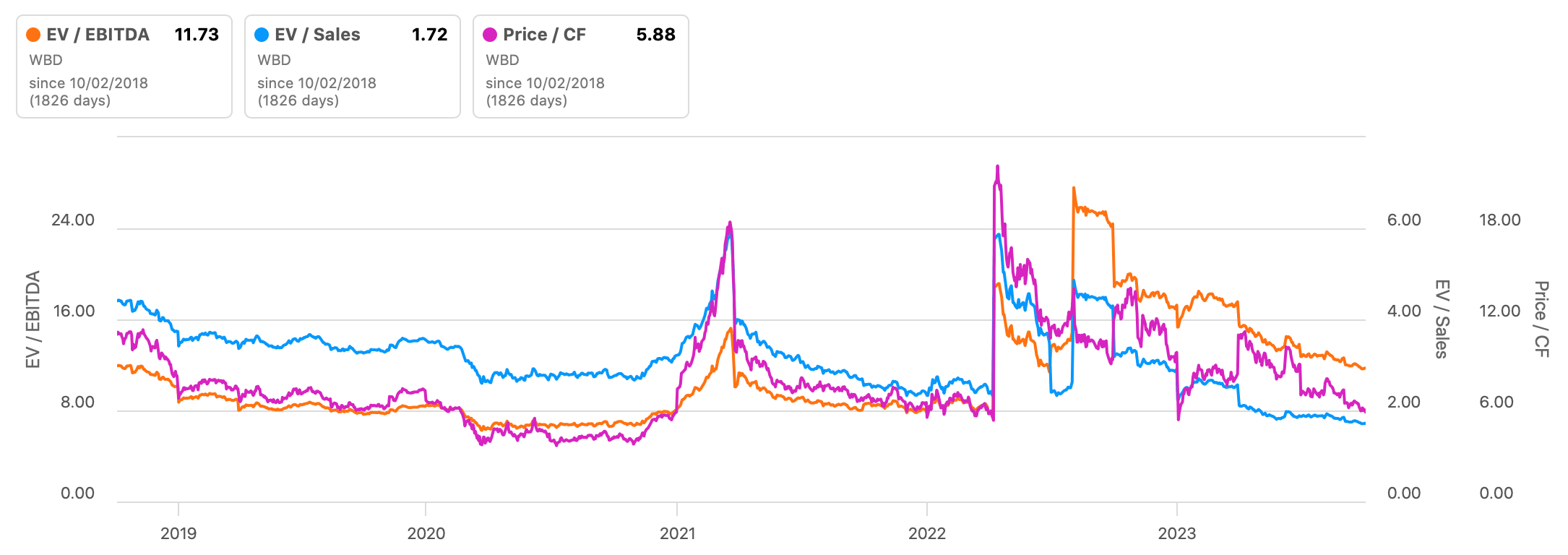

It's tricky to get a grasp on WBD's valuation given the frictions with the Warner Brothers and Discovery merger and the ad market pullback. EV/sales is near all-time lows at <2x, while EV/EBITDA has been more impacted by Warner Bros.' reduced profitability coming out of AT&T ( T ).

WBD valuation metrics (Seeking Alpha)

{kind=link}

One way to look at the situation is that Discovery on its own in 2021 earned $2.4B in free cash flow . And CFO Gunnar Wiedenfels apparently keeps finding more synergies with the combined company -- "we've taken the synergy target up. We've got $3B in the bag , already raised our expectation to $5B plus now". Presumably that should mean that the Warner Brothers segment returns to cash generation after its time in AT&T-land? If they did eventually achieve their original $14B adjusted EBITDA target , WBD would be trading at around 5x EV/EBITDA.

Risks

Of course, the risks with WBD are elevated, as seen by its volatility in the past few years. Some of the risks could include the following:

- Less pricing power than anticipated, if consumers are more willing to reduce their number of services

- Faster decline of linear.

- A continued arms race in content spend, once the Writers' and Actors' strikes have both ended (these essentially acted as a cease-fire in the content arms race).

- Competitors like Netflix and Amazon ( AMZN ) can take advantage of greater D2C scale and have no exposure to linear.

- WBD's high debt level, which would compound any business performance issues.

Factors that mitigate risk for Warner Bros. Discovery include its long-term 94% fixed-rate debt, progress on meeting debt pay-down targets, and consumer preferences for content that don't change that quickly. The disruption of Netflix and entry of Big Tech are no longer unknown wild cards and all major potential entrants have already entered the market. Both have also been increasing their emphasis on profitability. And if WBD's market cap remains below $30B, at some point in 2024 or beyond it could generate interest as an acquisition target.

Conclusion

The streaming industry is emerging out of a phase of scorched earth competition to amass subscriber numbers. There are clear avenues for improving profitability and an alignment across the industry to follow through on that. The delivery of content is changing, but not the underlying value to consumers, so I expect that over time, WBD and others will find ways to charge consumers more or get longer term commitment. Longer-term commitment will also open the door to reduce growth in content spending.

The ad recession is cyclical and will clear up eventually. If the market has any confusion between the cyclical and secular decline affecting traditional media, then an ad market recovery will undoubtedly help to resolve that. With the launch of WBD's combined streaming platform, Max, and once price increases get absorbed, there might even be a return to global subscriber growth. The timeline for all of this is unclear but I expect that patience will be rewarded for WBD investors.

Let me know if you disagree –– I look forward to your comments.

For further details see:

Warner Bros. Discovery: The Economics Of Streaming Will Get A Lot Better