WFC - Warren Buffett Messed Up With Wells Fargo

2023-07-30 06:15:31 ET

Summary

- Berkshire Hathaway sold a substantial stake in Wells Fargo, after owning the stock for numerous years.

- The company made numerous ethical mistakes, and it's still undergoing the resulting punishments.

- Despite this, the company's operations are highly profitable, and the company is one of the few banks that can drive strong double-digit returns.

Wells Fargo ( WFC ) saw its share price suffer after a major scandal, where the company opened accounts for users without their authorization. The company saw its size limited by the Fed, a limit that remains in place . The company has worked to comprehensively fix its problems, but in the meantime, its share price has mostly recovered.

As we'll see, with its strong financials, the company can drive substantial returns.

Wells Fargo 2Q 2023 Results

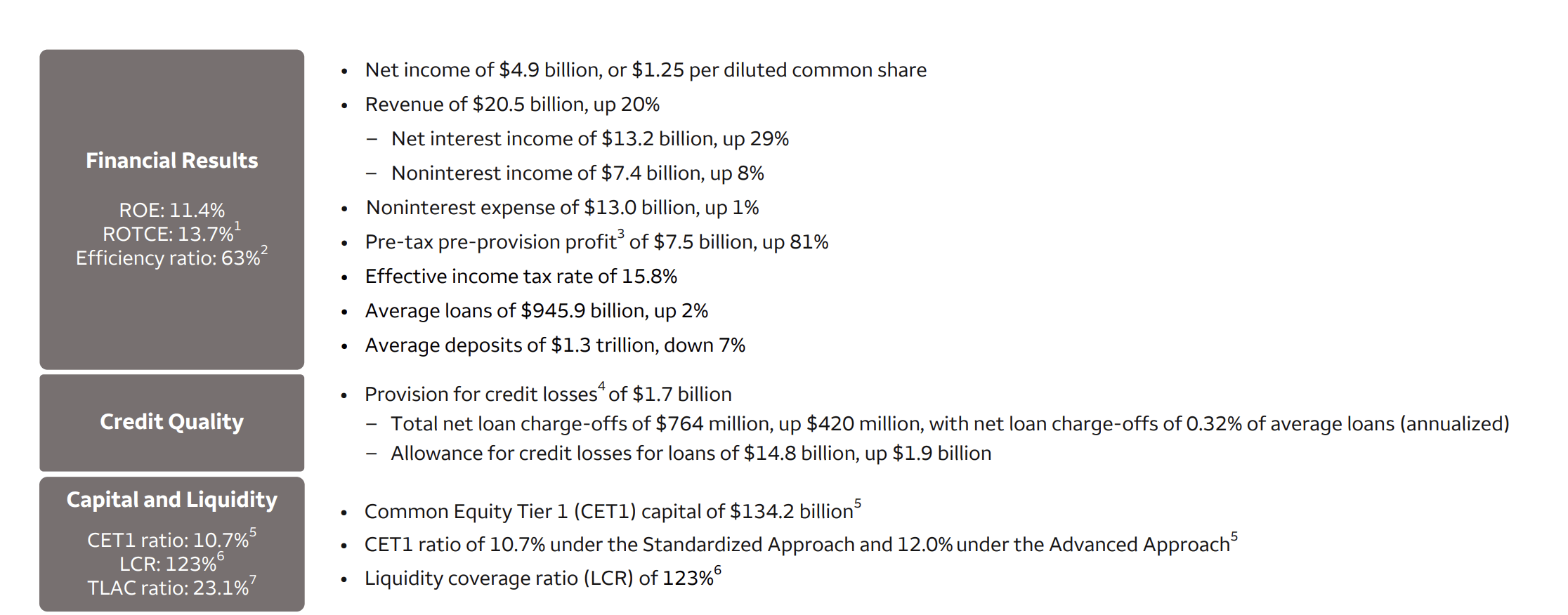

The company managed to achieve strong 2Q results, highlighting its financial strength.

{kind=link}

The company earned $4.9 billion in net income, or $20 billion annualized (a high single-digit P/E ratio). The company earned $20.5 billion in revenue, supported by rapid growth in the company's net interest income. At the same time, the company managed to keep its expenses low, supporting its pre-tax profit increase.

The company has continued to keep average loans and deposits low, with its size limited by the Fed. The company CET1 ratio of 10.7% remains more than manageable and its liquidity coverage ratio remains low. The company does have the risk that new standards moving through the Fed could increase its required capital ratio.

Like all banks, even with a strong amount of capital, it's not immune to a run on the bank.

Wells Fargo Losses

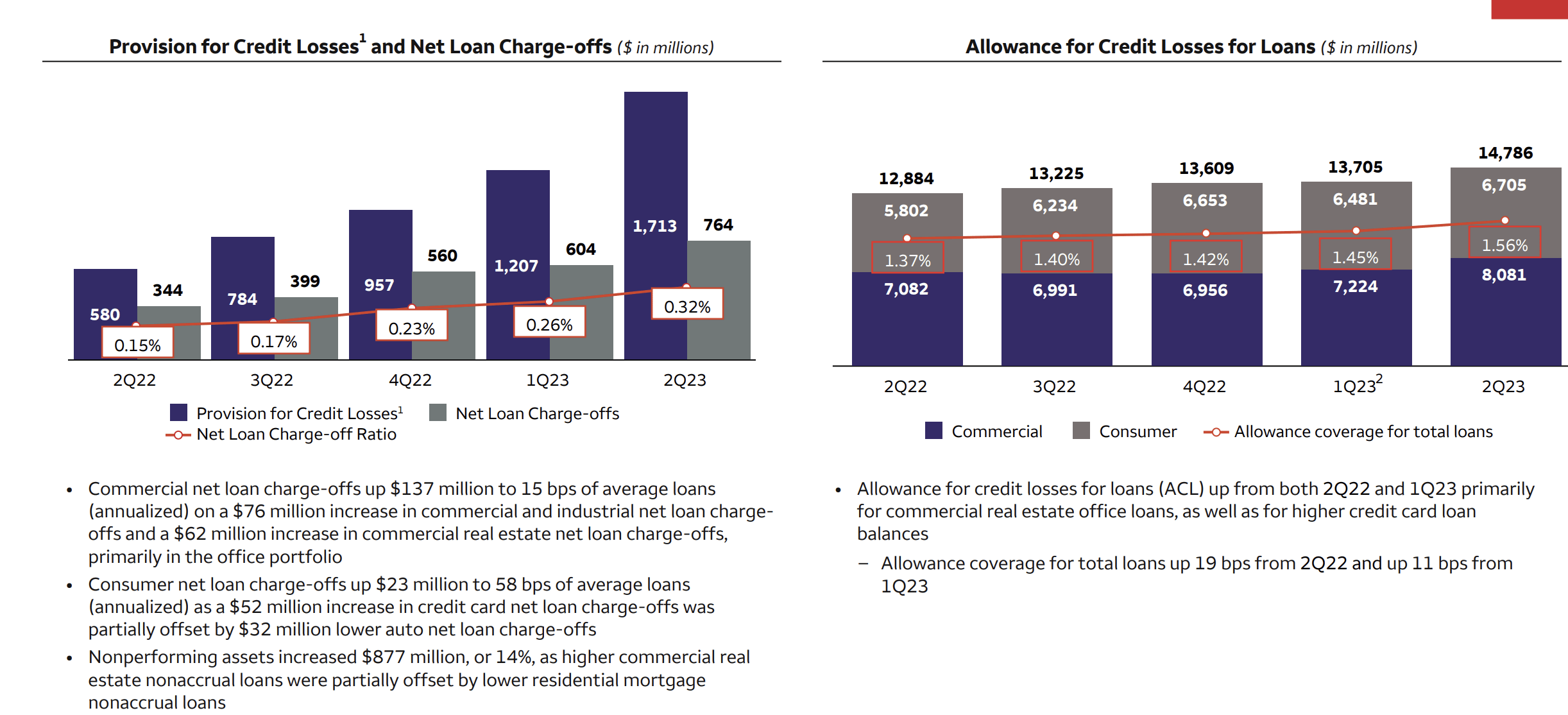

Rising interest rates have impacted the company, partially pushing up losses.

{kind=link}

The company has had to increase its provision for credit losses substantially, as interest rates have risen. In the most recent quarter, that provision was $1.7 billion, as the company had $760 million in net loan charge-offs. That's a 0.32% ratio, one that the company can comfortably afford. Its total allowance is 1.56% with the commercial allowance growing even faster.

A potential rise in losses from high interest rates remains a risk to the company, especially as the spread between the rates it earns and what it has to pay to depositors tightens. That spread is based on the cost of operations much more than the prevalent interest rates, while default rates are more based on the prevalent interest rates.

Wells Fargo Businesses

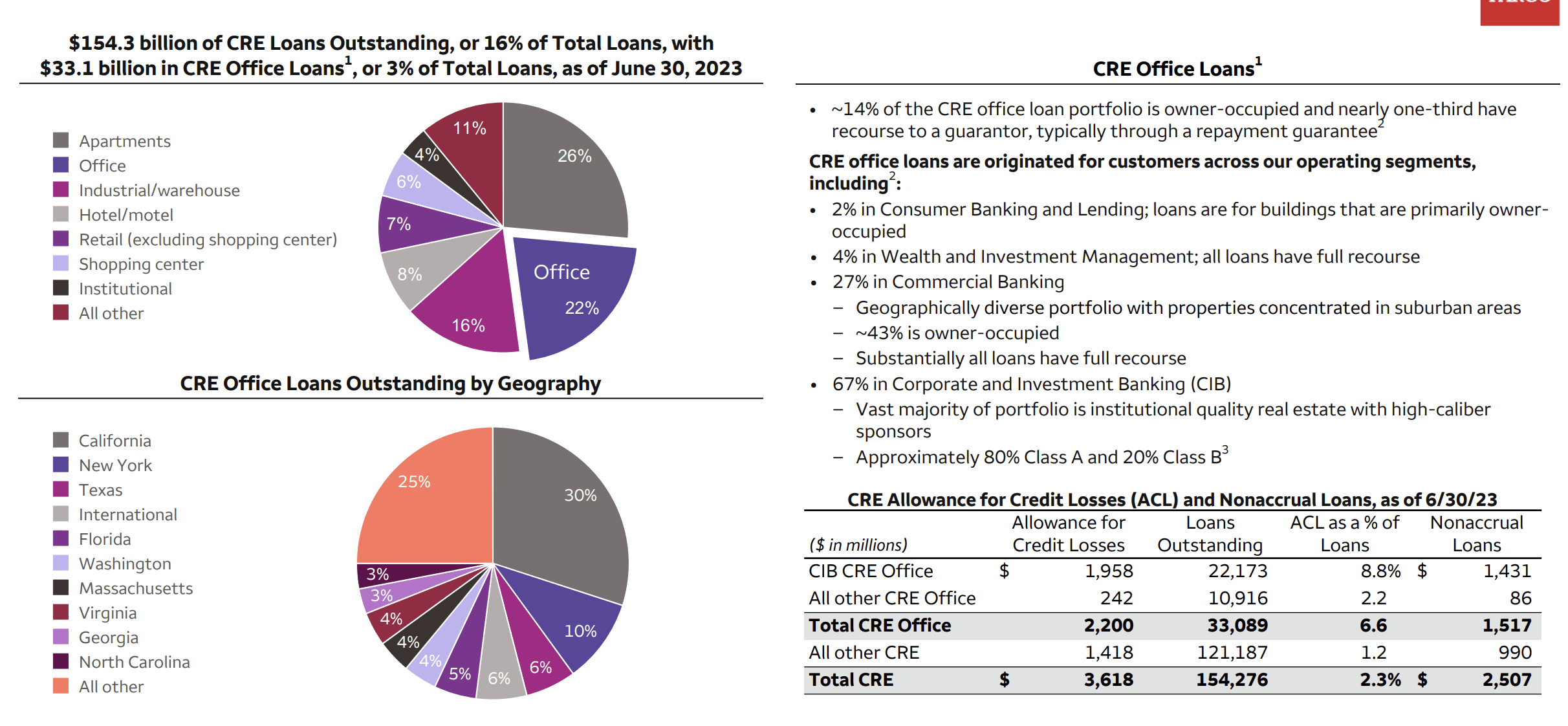

The company has built up an impressive portfolio of assets, with a strong diversified business.

{kind=link}

The company continues to operate a well-diversified portfolio, but a major risk is a continued $33.1 billion in CRE office loans, a market that is starting to show some cracks. The company has picked high quality class A customers here, but the cracks are visible through the much higher allowance for losses (currently 6.6% total across the portfolio).

That rate is already much higher than the rest of the company's portfolio and makes up ~15% of its total allowance for losses despite being a mere 3% of its total loans. We expect the company to make better decisions in that segment in the future, but an increase in losses here could heavily impact profits for several quarters.

{kind=link}

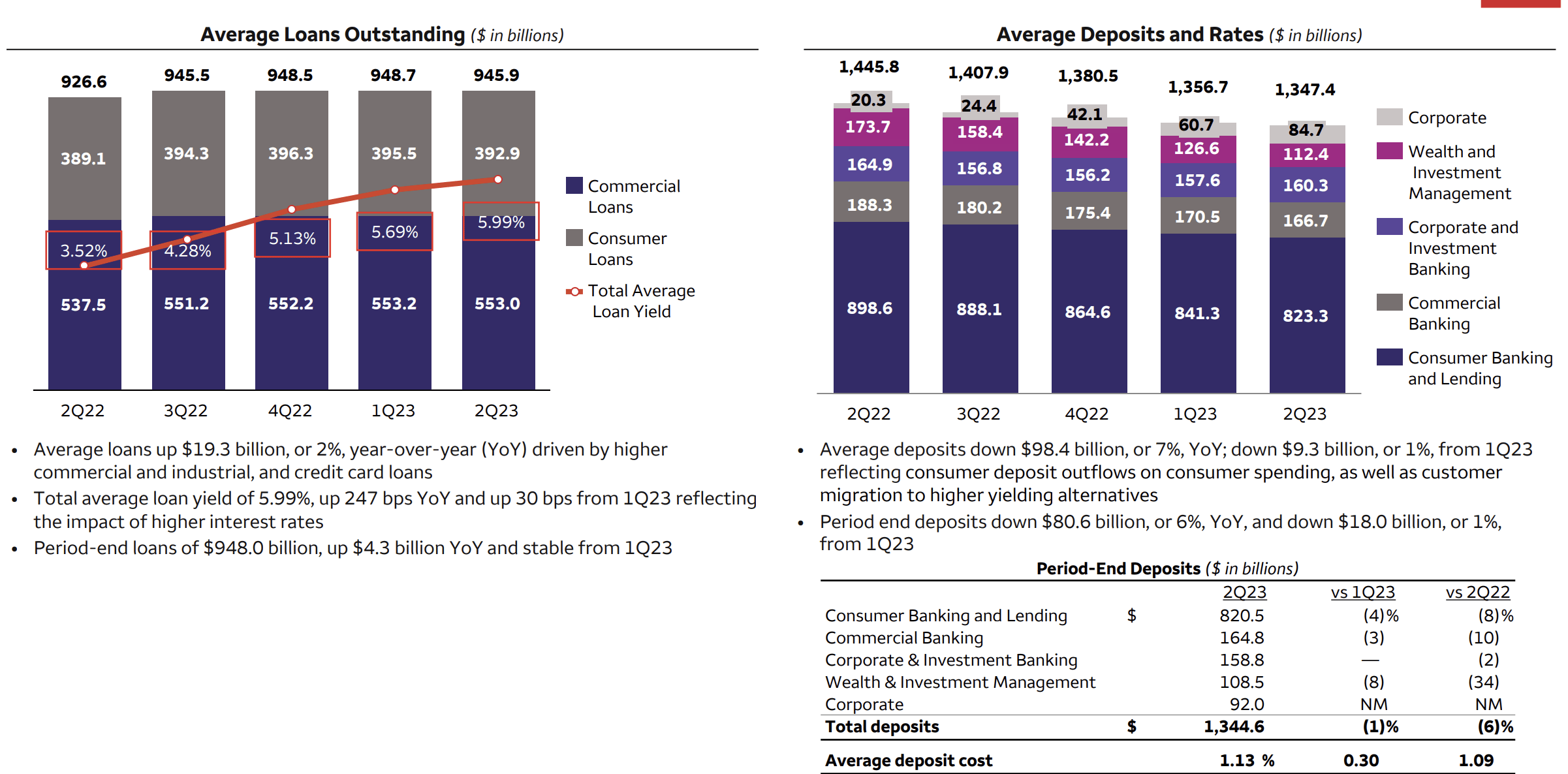

Overall, the company has roughly $946 billion in loans outstanding, a number it's had to keep fairly flat given size limitations. At the same time, average deposits and rates have trended down to $1.35 trillion, as depositors look for higher-yield opportunities. The company's average deposit cost of 1.13% is a fraction of even short-term treasury rates, and increases the chance of additional migrations.

The company has an average 6% yield on its portfolio, up from 3.52% a year ago, a 2.5% increase. We expect the company's current spread of 4.85% to tighten substantially, pushing down its interest revenue and profits in its business. Despite that, we expect the company's overall profits to remain quite strong.

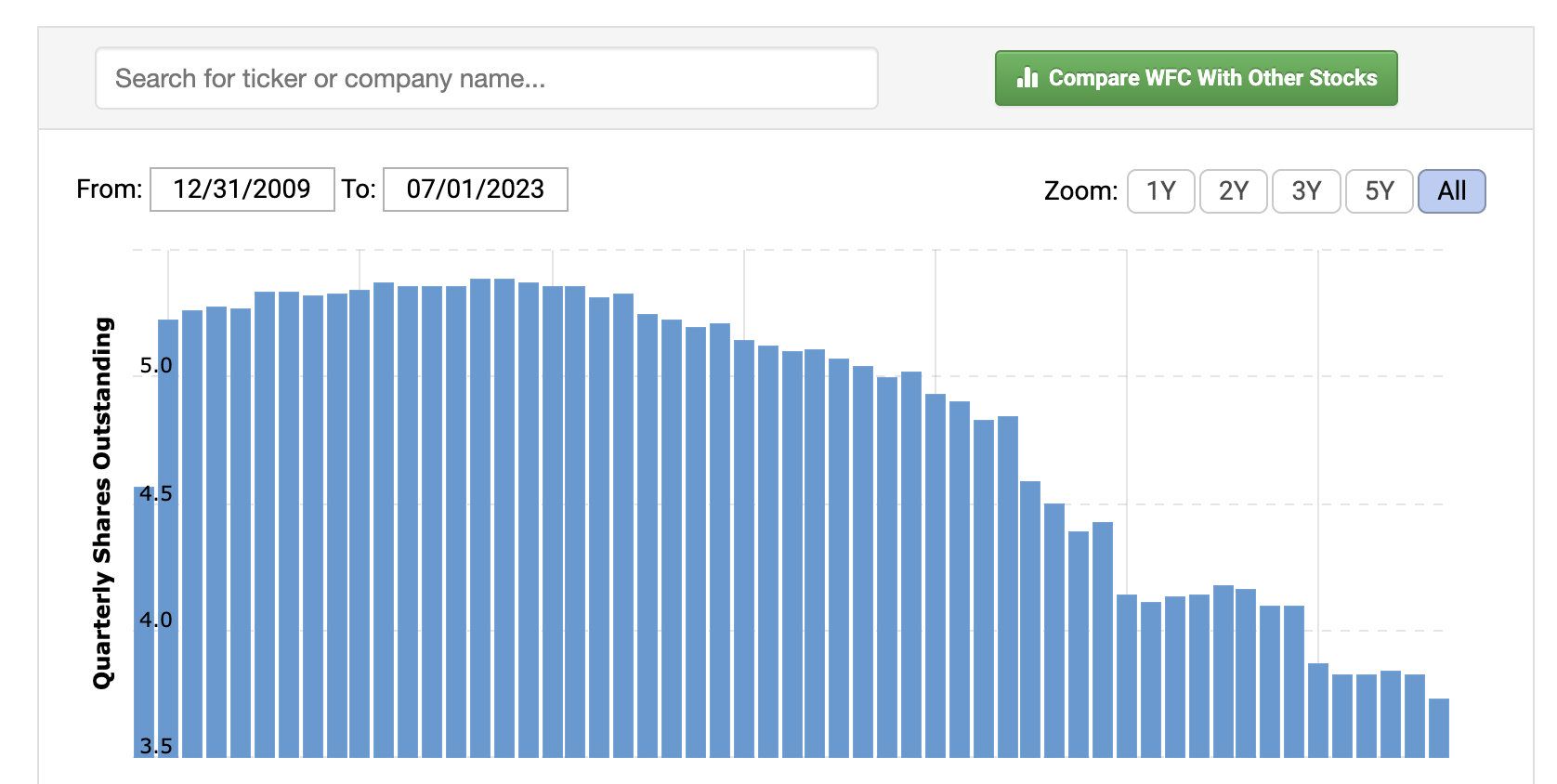

Wells Fargo Shareholder Returns

Wells Fargo remains committed to shareholder returns. The company repurchased roughly 3% of outstanding shares in the most recent quarter, and remains profitable.

{kind=link}

The company has managed to steadily reduce shares outstanding over the past decade, taking advantage of low prices . The company recently announced an increase of its dividend to $1.4 / share, pushing the forward yield to more than 3%. The company also announced another $30 billion share repurchase, enough to repurchase almost 20% of its outstanding shares.

The company trades at a single digit P/E based on its recent quarter earnings, showing a continued ability to drive double-digit shareholder returns.

Thesis Risk

The largest risk to our thesis is the company's NIM (Net Interest Margin). The level in the most recent quarter (3.09%) was the lowest of the company's last 3 quarters. As depositors request higher rates, that spread will continue to face pressure, on a rate that was just under 2.4% a year ago. That pressure could hurt its income substantially.

Conclusion

Wells Fargo remains cheap. The company has a single digit P/E ratio. The Fed has imposed limitations on the company, as the company continues to face punishment for a spate of bad decisions. We expect that punishment to remain in place for the next 1–2 years. In the meantime, the company remains profitable, which it can direct to returns.

The company has a dividend of more than 3% that it can comfortably afford. At the same time, the company has recently announced $30+ billion in share buybacks, enough to easily purchase a double-digit % of its stock. We expect the company to continue driving strong returns at its low valuation, making it a valuable investment.

For further details see:

Warren Buffett Messed Up With Wells Fargo