CA - Waste Connections: A Decentralized Operation With High Revenue Quality

2023-10-13 06:30:14 ET

Summary

- Waste Connections is the third-largest solid waste services company in North America, known for its decentralized operating model and swift decision-making capabilities.

- The waste management industry demonstrates stability and resilience, with consistent demand for waste collection and recycling services.

- Waste Connections focuses on balanced growth through price and volume, complemented by strategic acquisitions, making it an attractive choice for value investors.

Waste Connections (WCN) stands as the third-largest solid waste services company in North America, operating efficiently through five geographic segments as a decentralized organization. Their swift decision-making capabilities enable them to promptly meet customer needs and secure contracts in secondary and rural markets. What sets them apart is their balanced approach to growth, focusing on both price and volume, complemented by strategic tuck-in acquisitions. In my assessment, Waste Connections emerges as a high-quality company, making it an excellent choice for value investors. Based on my model, the fair value of their stock price is $145 per share, leading me to assign a 'Buy' rating.

Industry Analysis

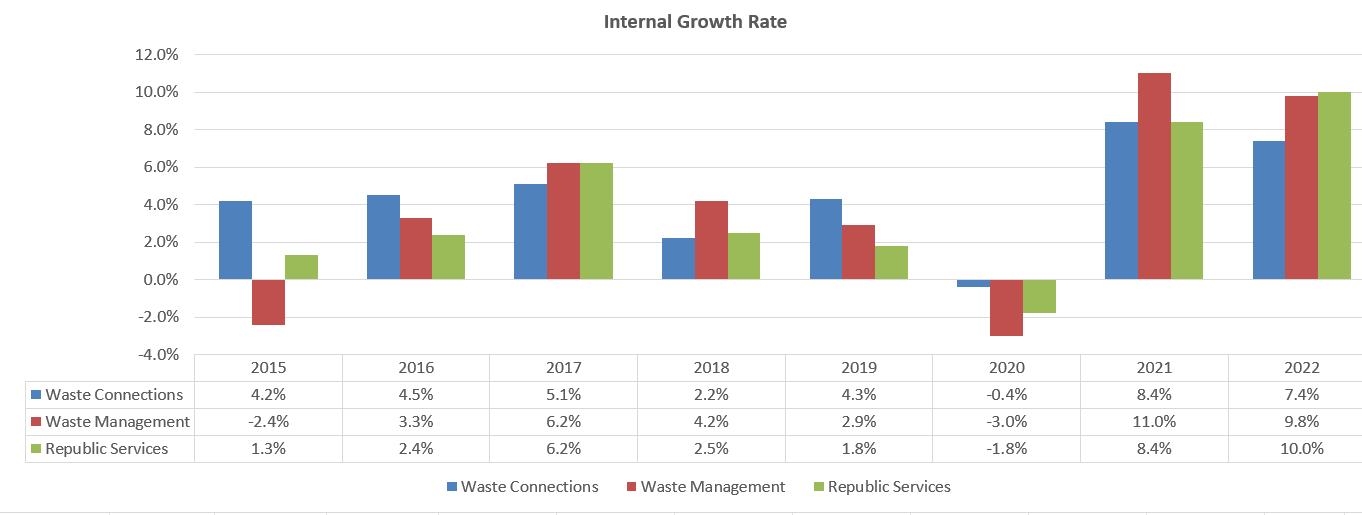

The top three waste management companies, Waste Management (WM), Republic Services (RSG), and Waste Connections, have experienced significant internal growth in both volume and price over the past few years. Their businesses demonstrate remarkable stability and resilience across different economic cycles. Regardless of the economic environment, the demand for waste collection, transfer, landfilling, and recycling remains constant, making their operations consistently essential.

{kind=link}

The waste management industry faces volatility in diesel fuel prices, which significantly impacts companies due to their heavy reliance on diesel fuel. The positive aspect of this situation is that waste management companies are able to pass on these fluctuating fuel costs to their customers. Essentially, their core internal growth is primarily influenced by core price growth and volume growth, minimizing the impact of fuel price volatility on their overall operations.

Decentralized Operating Model

Waste Connections operates on a decentralized basis, granting significant decision-making authority to local managers without the need for pre-approval from the head office. The company divides its operations into six distinct geographic segments: Eastern, Southern, Western, Central, Canada, and Mid-South, each of which possesses ample autonomy to manage its regional businesses.

This decentralized approach offers several key benefits. Firstly, it facilitates a rapid decision-making process, enhancing customer satisfaction by swiftly resolving issues and complaints. Secondly, local decision-making enables the company to adjust prices at the regional level, considering varying cost structures in different regions. This flexibility is essential because a universal pricing model isn't suitable for waste management companies operating in diverse environments.

Lastly, the decentralized organization creates strong incentives for the local management teams. Their incentives are directly tied to regional performance and the profit and loss statements of their respective regions, fostering a sense of ownership and accountability. This alignment between local incentives and regional outcomes motivates managers to optimize operations and drive overall company success.

In Q2 FY23's earnings call , Waste Connections' management team reaffirmed the significance of their decentralized operating philosophy, which has long set them apart. Coupled with their servant leadership-oriented culture, this approach has been a key differentiator for the company. Notably, they expanded their regional segmentation to six by incorporating Mid-South, a move attributed to their acquisition of Arrowhead . Despite this expansion, they expressed confidence in their leadership team's ability to effectively nurture relationships with local operations, underscoring their strategic positioning within the industry.

Balanced Volume and Price Growth

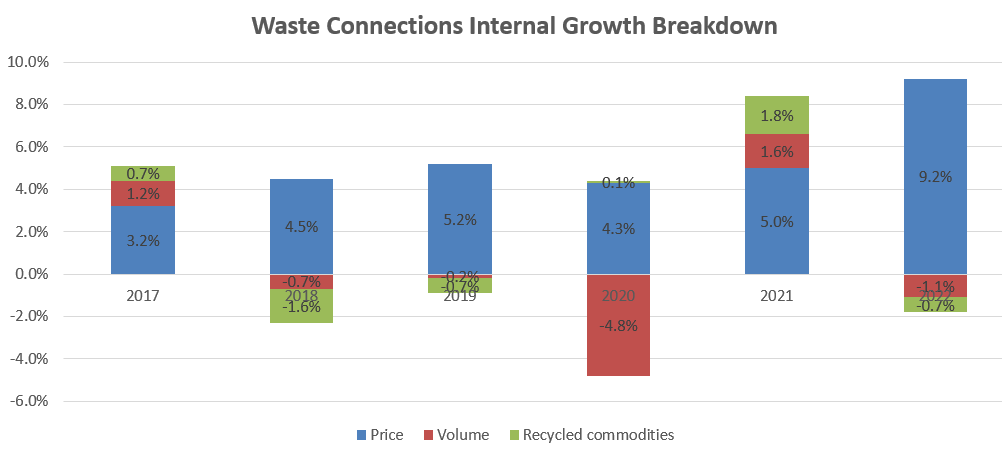

Waste Connections' internal growth is driven by three primary factors: price, volume, and recycled commodities. Over the past eight years, their internal growth rate has averaged around 4.5%. When excluding the pandemic year, their average internal growth rate increases to 5.2%. This figure reflects a commendable growth rate, especially for a waste management company.

{kind=link}

{kind=link}

It's worth highlighting that Waste Connections' volume growth experienced declines, with -1.1% in FY22, -0.2% in FY19, and -0.7% in FY18. These declines were a result of the management's strategic decision to discontinue certain low-margin contracts. This move was part of their focus on optimizing profitability and cash flow. In Q2 FY23, the management emphasized that negative volume growth, when paired with decreasing margins and cash flow, should raise concerns. However, if negative volume growth occurs alongside expanding margins and cash flow, it is viewed as a positive for the company.

I agree with their perspective on this matter. There are numerous low-margin municipal contracts for waste collection that lack profitability and fail to generate sufficient cash flow. It's entirely reasonable to walk away from these contracts. Allocating resources primarily to high-profit exclusive contracts makes strategic sense. Waste Connections' robust core price growth in recent years validates the effectiveness of this approach, demonstrating the company's benefit from this strategic focus on profitability and sustainability.

Secondary and Rural markets Focus

Waste Connections strategically targets secondary and rural markets, allowing them to attain substantial market share in these areas. These regions offer the advantage of lower competition compared to larger cities and urban markets. Waste Connections employs tuck-in acquisitions as a method to expand their services in these secondary and rural regions. For instance, their recent acquisition of Arrowhead enables them to extend their coverage to states like Tennessee, Kentucky, Alabama, and other rural areas.

According to their disclosures , 40% of their revenues come from exclusive franchise markets, indicating their strong presence and market control. Additionally, 60% of their revenues are generated from rural or secondary markets where they have achieved significant market share. Based on their current strategy and acquisition plans, it's foreseeable that they will continue to expand their footprint in these rural and secondary markets. This expansion will likely be facilitated by integrating newly acquired regional businesses under the same organizational umbrella, ensuring a cohesive and streamlined approach to their operations.

Financial Analysis and Outlook

Waste Connections has demonstrated a strong historical performance, boasting commendable gross margin and operating margin figures. Additionally, their ability to convert operating cash flow into cash is noteworthy, with an impressive 28% operating cash flow margin and a 15.4% free cash flow margin in FY22.

In terms of capital allocation, the company strategically deploys cash generated from operations in various ways. They allocate resources towards dividends, ensuring shareholders benefit from the company's profitability. Furthermore, they invest in share buybacks, indicating confidence in their own financial stability and future growth prospects. Additionally, Waste Connections utilizes funds for tuck-in acquisitions, a strategic move aimed at expanding their services in rural and secondary markets. This multi-faceted approach to capital allocation reflects their commitment to enhancing shareholder value while also investing in strategic initiatives for future growth.

Waste Connections 10Ks

On the balance sheet, Waste Connections reported a gross debt leverage of 3.3x in FY22, falling within their targeted range of 2.5x to 3x gross debt leverage. Given that Waste Connections is a non-cyclical company, the 3.3x gross debt leverage is manageable, and there doesn't appear to be any significant concerns in this regard.

In Q2 FY23 , the company demonstrated strong financial performance, with an 11.3% increase in revenue and an 11% rise in adjusted EBITDA. This robust performance led to an update in their full-year guidance, indicating positive momentum and a favorable outlook for the company's future.

{kind=link}

In Q2 FY23 , Waste Connections experienced a significant core price growth of 9.8%, although there was a negative volume growth of -1.9%. The company clarified that this decline in volume growth was a deliberate move, driven by their strategy of shedding lesser quality accounts and opting not to renew specific municipal contracts intentionally. Moreover, in their acquired businesses, they are actively evaluating the revenue quality.

As previously discussed, Waste Connections' strategic focus on high-quality contracts appears to be a smart and prudent approach. This strategy not only ensures a more stable revenue stream but also aligns with their commitment to delivering value to their shareholders. By concentrating on contracts that are financially sound and offer sustainable profitability, Waste Connections is positioning itself for long-term success in the waste management industry.

Key Risks

Recycled commodity prices play a role in Waste Connections' revenue, accounting for approximately 3% of their total sales. However, these revenues are susceptible to fluctuations based on changes in commodity prices, which are often influenced by economic conditions. Given the unpredictable nature of commodity prices, accurately predicting the contribution of recycled commodities to the company's overall revenue is challenging. Moreover, the waste management industry faced challenges due to policy changes, such as the Chinese government's ban on the importation of solid waste and recyclables starting from January 1, 2021, affecting the transportation of waste and recyclable scrap.

Additionally, the waste management sector, as reported by EURACTIV , is vulnerable to corruption. Small waste management companies sometimes resort to bribery attempts involving local officials to secure collection contracts. Instances of corruption have been discovered, such as the 2021 case where three trash disposal companies serving San Francisco, subsidiaries of Recology Inc., were charged in federal court with conspiracy to commit honest services fraud. These challenges underscore the complexities and ethical concerns within the waste management industry, necessitating vigilant oversight and ethical business practices.

Valuation

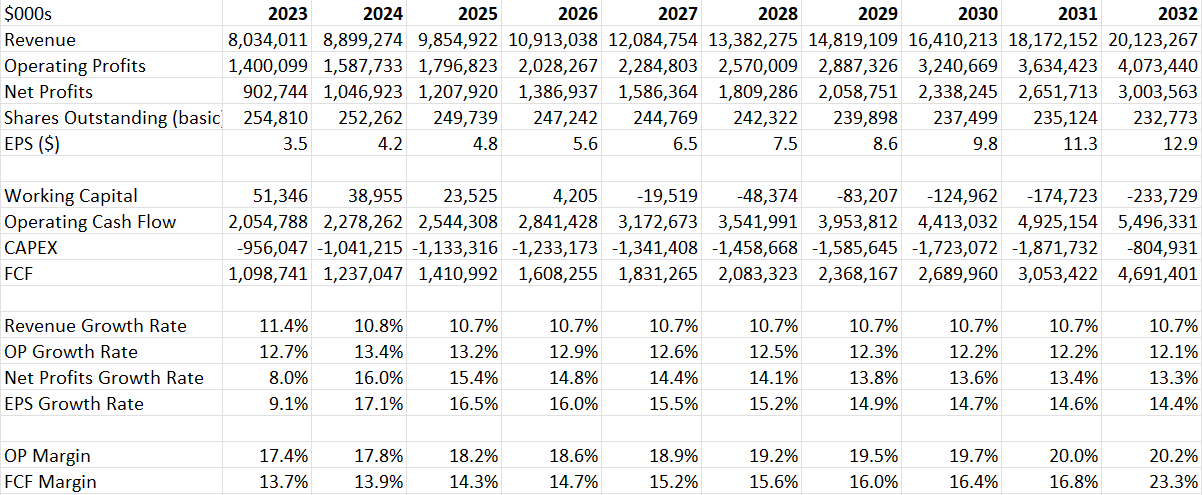

In the DCF model, I assume their internal growth rate to be 5.2%, the average figure from FY15 to FY22 excluding the pandemic year. At the same time, I expect they are deploying 10% of their revenue on tuck-in acquisitions, a conservative assumption compared to their track record. These acquisitions could add around 5.5% of top-line growth as per my calculation. Therefore, the normalized revenue growth is projected to be 10.7%. As the company is executing its revenue quality initiatives, I expect their revenue mix to shift more towards high-margin contracts. In addition, they can benefit from operating leverage; thus, I predict their margin to expand by around 30 basis points annually.

{kind=link}

The model employs 10% discount rate, 4% terminal growth rate and 23% tax rate. After discounting all the free cash flow, the fair value of their stock price is calculated to be $145 per share.

Verdicts

I consider Waste Connections to be a high-quality decentralized organization, making it a suitable choice for value portfolios. In my assessment, the stock appears to be slightly undervalued at its current price, leading me to assign a "Buy" rating.

For further details see:

Waste Connections: A Decentralized Operation With High Revenue Quality