CA - Waste Connections: Impressive Growth But Looming Risks

2023-07-26 06:22:24 ET

Summary

- Waste Connections, a waste management company, has reported strong financials despite a 1.3% dip in volume due to severe weather conditions.

- The company has been investing in green projects and expects these to add $200m to EBITDA by 2026.

- The company's Q1 revenue was $1.901bn, a 15.4% increase from the previous year. The adjusted EBITDA for Q1 was $567m, constituting 29.8% of revenue.

- The projected EBITDA for Q2 is estimated at $615m.

- Blended P/E ratio of 35.52x, possibly overvalued compared to industry average of 15.00x.

Thesis

In this article, I examine the performance and prospects of Waste Connections ( WCN ), a leader in the North American waste management industry by exploring the company's impressive financials and strategic expansion, driven by a balanced growth approach and timely M&A activities. However, my analysis also uncovers potential risks and headwinds, including possible overvaluation, a lower-than-average dividend yield, and susceptibility to external factors. Despite strong EBITDA margins and proactive investments in sustainability, these concerns suggest a cautious approach for potential investors.

Company Overview

Since 1997, Waste Connections, Inc. has branched out far beyond its Canadian roots to carve an impressive footprint in the waste management landscape across the United States and Canada. It caters to a spectrum of clientele that spans residential, commercial, and municipal sectors, not forgetting to serve the industrial realms and those venturing into exploration and production (E&P).

Strong Financials and Strategic Expansion

Waste Connections churned out commendable numbers for the first quarter . Marked by a hearty pop in solid waste prices and volume - 10.5% to be precise, and a total price boost of 11.8%, the figures highlight the company's nimble, analytical approach to taming cost pressures.

Despite some rough weather rocking the boat - leading to a 1.3% dip in volume due to severe conditions on the West Coast, the company managed to cushion the blow through a timely rise in activity related to hurricane cleanup in Florida. When it comes to revenues outside of the solid waste realm, they tracked expectations pretty accurately, although the commodities, landfill gas, and renewable energy credits segments were not so lucky, experiencing a 40% year-on-year contraction.

The M&A bandwagon rolled on with fervor during the first quarter, adding $45 million in annualized revenue to the books. According to management, this energetic pace is likely to be sustained, with the spotlight firmly on attractive solid waste businesses promising a future rich in value.

Lastly, in its quest for a more sustainable future, Waste Connections continues to invest in green projects, including multiple renewable natural gas facilities. These endeavors are forecasted to pump an additional $200 million into EBITDA by 2026. And to facilitate this journey, a fairly-solid balance sheet, with leverage dipping below 2.9 times, offers the flexibility for strategic business expansion and streamlined debt repayment.

Outlook

{kind=link}

Waste Connections is scheduled to report their Q2 next month , but in the meantime, management outlined their outlook and they anticipate revenue for the next quarter rounding off at an estimated $2 billion , a figure attained by knitting together several components:

A sizable chunk of this revenue estimation, around 8% to be exact, can be traced back to the growth in both the price and volume of solid waste. This increase, coupled with a core price growth of roughly 10%, underscores a solid demand environment and potential benefits from favorable pricing dynamics.

E&P waste revenue—a smaller, yet significant player in the overall revenue story—stands at an estimated $50 million. While it doesn't constitute the lion's share of the revenue, any shifts in this segment could impact the overall financial health.

The projected Adjusted EBITDA for Q2 is pegged at an estimated $615 million, forming approximately 30.8% of the expected revenue.

Transitioning to expenses, we see an estimated depreciation and amortization expense that is likely to account for roughly 12.5% of revenue for the upcoming quarter. The incorporation of approximately $39 million in amortization of intangibles, or about $0.11 per diluted share net of taxes, further deepens the depreciation landscape.

Interest expense, net of interest income, presents another element in the Q2 fiscal story with a projected figure of about $66 million.

Valuation

Meanwhile, WCN's blended P/E ratio of 35.52x (see chart below) is significantly higher than the average P/E of 15.00x that we typically benchmark in the waste management industry and even surpasses their historical normal P/E of 31.78x which could suggest that the stock is somewhat overvalued. However, the adjusted operating earnings growth rate is 11.37% - a healthy figure and one that suggests that Waste Connections is churning out solid earnings growth, a favorable sign for investors.

{kind=link}

The EPS yield of 2.81% is fair, albeit not exceptionally high, but it provides some cushion against fluctuations in earnings. However, the dividend yield of 0.73% seems a bit meager, especially for income-focused investors. There's room for growth here if Waste Connections wants to attract a broader income-investor base.

Risks & Headwinds

Starting with Waste Connections sector valuation, I wanted to point out some areas that add to their overall grade which sits at an 'F', placing them in a precarious position within the industrials sector (see data below). Looking at the P/E ratios, both non-GAAP and GAAP, both on a trailing twelve months ((TTM)) and forward basis, we see WCN trading significantly higher than the sector median and its five-year average.

{kind=link}

Shifting to enterprise multiples, both EV/Sales and EV/EBITDA are starkly above the sector median - by 227.18% and 58.90%, respectively. Elevated levels for these ratios often indicate that a company is overpriced, suggesting WCN might not be a bargain buy at this stage.

And another red flag that stands out for me is the aforementioned low dividend yield at 0.69%, a massive 51.69% lower than the sector median and 2.46% lower than its 5-year average.

Further scrutiny reveals certain areas of concern within their revenue structure. We see that their revenue from recycled commodities, landfill gas, and renewable energy credits - what we might call the greener side of their operations - took a substantial hit of about 40% on a year-over-year basis. This downturn is no small worry; it points towards possible vulnerabilities within these segments. From a sustainability standpoint, these are crucial areas where the company needs to be on firm footing to meet growing demands for green practices within waste management. If they're unable to address these weaknesses, we could witness a widening gap between their conventional waste management and their sustainable operations.

We then see exploration and production waste activity levels on a downward trajectory by about 8% sequentially. This decline might be a bellwether of an impending bearish trend. In the waste management industry, E&P waste activity is a crucial component. This sector revolves around managing and disposing of waste from oil and gas exploration and production. A downturn in this area might suggest a broader industry slowdown or perhaps more concerning, the company's dwindling efficiency in managing this particular waste stream.

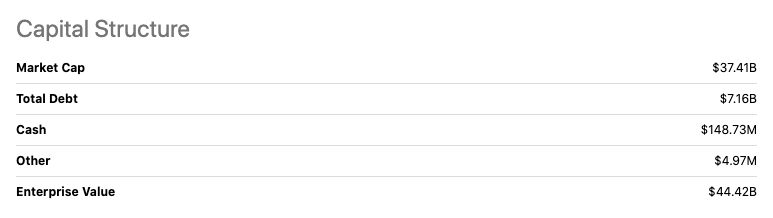

Lastly, the company has seen a surge in interest expenses due to an increase in total borrowings, a direct offshoot of their acquisition-driven growth strategy. While expansion is generally viewed as a positive stride, the growing interest burden could become a financial albatross if not managed properly.

{kind=link}

Higher leverage can add stress to their financials, particularly in an environment of potential rising interest rates. This growing debt burden could restrict the company's agility in capital deployment, thus potentially hindering future growth opportunities.

Final Takeaway

I'd rate Waste Connections stock as a "hold". The company has recently delivered impressive financials, however, several concerns temper my enthusiasm. These include a substantial contraction in revenue from some sectors, a significant P/E ratio that suggests overvaluation, and a below-average dividend yield. External factors like weather have impacted performance, highlighting potential vulnerabilities, and growing interest expenses due to an aggressive acquisition strategy could pose challenges in a rising interest rate environment. Therefore, while the company is fundamentally strong, these risks warrant caution for new investors looking for a better entry point.

For further details see:

Waste Connections: Impressive Growth But Looming Risks