BYDDY - We Like NIO But Here's Why The Rally Likely Won't Sustain

2023-07-10 14:06:28 ET

Summary

- NIO Inc. stock has been on a gradual uptrend over the past month, gaining almost 20% in value despite ongoing challenges in the pricing environment and modest Q2 delivery volumes.

- Rising competition and a deteriorating macroeconomic environment in China are expected to worsen the challenges facing NIO's target premium segment in the near term.

- Delivery declines observed in Q2 relative to resilience observed at its mass market rivals also underscore a waning demand environment that prioritizes affordability.

- Looking ahead, re-acceleration in volumes - especially for the newly introduced NT 2.0 vehicles - will be a key value accretive factor to drive further upside potential and overcome near-term headwinds on profit margins.

NIO Inc. ( NIO ) stock has regained some ground over the past month, with staying power in the $10 range despite relatively weak second quarter delivery numbers released last week that suggested lagging growth behind domestic rivals Li Auto ( LI ) and BYD Company ( BYDDF / BYDDY ). In our previous coverage , we had discussed a few immediate-term headwinds facing NIO, counting a weakening post-COVID recovery in China that risks tempering the demand environment for its premium offerings, rising competition, an escalating price war, stalling penetration in its target higher-tier cities, and barriers to entry in lower-tier cities (e.g., affordability; lack of public charging facilities). While our firsthand observations suggest that NIO vehicles are no longer a rare sighting on the roads, with its brand awareness being no less than both foreign and domestic leaders like Tesla ( TSLA ) or BYD, the continued divergence of its relative growth story in recent quarters underscore affordability and EV range anxiety as key headwinds to adoption still, which have been exacerbated by deteriorating economic conditions and recurring price cuts across the auto industry in the region this year.

But the stock's resilience at current levels, which is corroborated by the gradual uptrend despite modest second quarter delivery numbers and the swift recovery after Thursday's (July 6) steep (-7.6%) intra-day declines, is likely a result of market's cautious optimism on early signs of easing price cuts and potential for further economic stimulus to buoy the Chinese EV market. Acknowledging the underlying risks to China's pace of economic recovery, both the central government and public agencies at the regional level have been especially supportive of the EV market with policy support spanning tax breaks and other fiscal financial incentives.

In the latest development, the Ministry of Industry and Information Technology ("MIIT") has also worked with the China Association of Automobile Manufacturers ("CAAM") in an aim to arrest the ongoing EV price war, encouraging 16 automakers to join hands in a " truce ." Unlike a regulatory overhaul, however, the joint agreement does not levy constructive controls on pricing, but instead, conveys the government's disapproval over the aggressive price cuts that have led to instability in the EV market's demand environment.

While the agreement is unlikely to bring immediate respite to price-driven pressures on NIO's performance in the near term, we think the company still has some levers up its sleeves - including the recent launch of upgraded all-new trims for its flagship ES6 and ES8 SUVs - to complement reduced prices and shore up delivery volumes in the meantime. But we expect NIO's top- and bottom lines to be further pressured in the near term by price reductions and uncertain macroeconomic conditions, nonetheless, exacerbating ramp-up costs of recently introduced models. This could potentially push NIO's timeline to GAAP net income further out into the future, and dampen sentiment on the stock, weakening the durability to its latest gains.

NIO Delivery and Pricing Update

NIO finished the second quarter with deliveries of 23,520 vehicles (-6% y/y; -24% q/q). The results were within management's earlier guidance for delivery of 23,000 to 25,000 vehicles for the second quarter, albeit on the lower end, but represents both a y/y and sequential decline. This continues to imply a diverging growth story from its better-performing domestic peers such as Li Auto and BYD, as discussed in our previous coverage on the stock. It also puts NIO's earlier aspirations to sell 250,000 EVs this year further out of reach.

However, management has been optimistic for a stronger second half regarding volumes, helped by the introduction of new models including the updated ES6 and ES8, and EC7 coupe SUV based on the NT 2.0 platform, as well as its line-up of sedans including the latest ET5 Touring. In addition to the recently introduced premium sedans, NIO has started delivering the EC7 Coupe SUV in April, the all-new ES6 based on the NT 2.0 platform in May, as well as the all-new ES8 and ET5 Touring - also based on the NT 2.0 platform - in late June.

The new model introductions have likely been a key driver to m/m growth in SUV sales during the second quarter, in line with earlier concerns that "internal cannibalization or competition" - particularly on older versus newer models - might have stifled sales. Specifically, management has expressed optimism for the production run-rate on said models to collectively reach 20,000 units per month starting in July, with expectations for incremental increases to delivery volumes in the second half based on robust reservation orders observed to date:

Regarding the ET5, ET5 Touring and ES6 overall volume, we believe there is opportunity for us to still achieve 20,000 units in one month…After the delivery of EC7, we can see the demand is actually quite stable. As for the ES6, just now I have mentioned that we are very confident about the sales performance of ES6 after the product ramp-up. And then, for this year, we are very confident of our speaking for all the new products we launched this year, including the ES8. We're about to start the delivery of the ES8 in the near term. And currently, we can see that the reservation order performance is actually higher than our expectations.

Source: NIO 1Q23 Earnings Call Transcript .

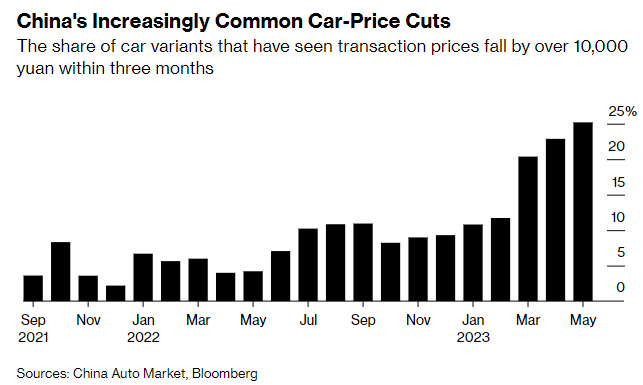

Meanwhile, on the pricing front, MSRPs across NIO's line-up have dropped lower in June compared to levels earlier this year, underscoring the persistent pressure of an ongoing price war in the broader Chinese auto market. The company "slashed prices on all of its models in China by [RMB 30,000]" in early June. And based on prices listed on NIO's sales website, the declines equate to 6% on average as of early July compared to early June when we last covered the stock.

Data from nio.cn

This implies that the recently introduced all-new ES6 and ES8 models are now selling at an even lower price than the legacy variants, potentially countering management's earlier goals to alleviate pressure on vehicle gross margins by leveraging sales of the new, higher-priced models based on the NT 2.0 platform:

…with the delivery of our NT2.0 product with higher price from Q2 and Q3, the average selling price and gross profit margin per car will recover. So, we are confident that the gross profit margin will start to recover to double-digits in Q3 and over 15% in Q4.

Source: NIO 1Q23 Earnings Call Transcript

And not only will the price reductions weigh on the second quarter's average selling price - especially given the greater share of SUV sales in NIO's consolidated revenue mix during the period - but also further incentivize prospective buyers to wait for incremental discounts, effectively taking advantage of intensifying competition amongst the Chinese automakers.

A Potential "Truce" in the Chinese EV Price War

In the latest development, NIO, alongside 15 other automakers in China - including Tesla - have collectively agreed to stop the implementation of unreasonable pricing strategies under the demands of the MIIT and CAAM. The pact outlines four major initiatives to "help stabilize growth and avoid risk" in the Chinese auto market:

- comply with existing industry regulations to ensure fair competition without the implementation of "abnormal pricing";

- abstain from exaggerated or false marketing;

- prioritize quality in products and services offered to customers; and

- contribute responsibly to "maintaining steady growth, strengthening confidence and preventing risks" in the Chinese auto market.

However, the signing of the pact - nor the four points listed within - is not expected to drive constructive improvements to the lingering pressure on prices across the Chinese auto market. Not only is the agreement non-binding - which means it is only symbolic of the government and the industry's official acknowledgement of an intensifying competition-driven price war - there is also a lack of structural regulatory order to hold automakers accountable for their aggressive pricing strategies.

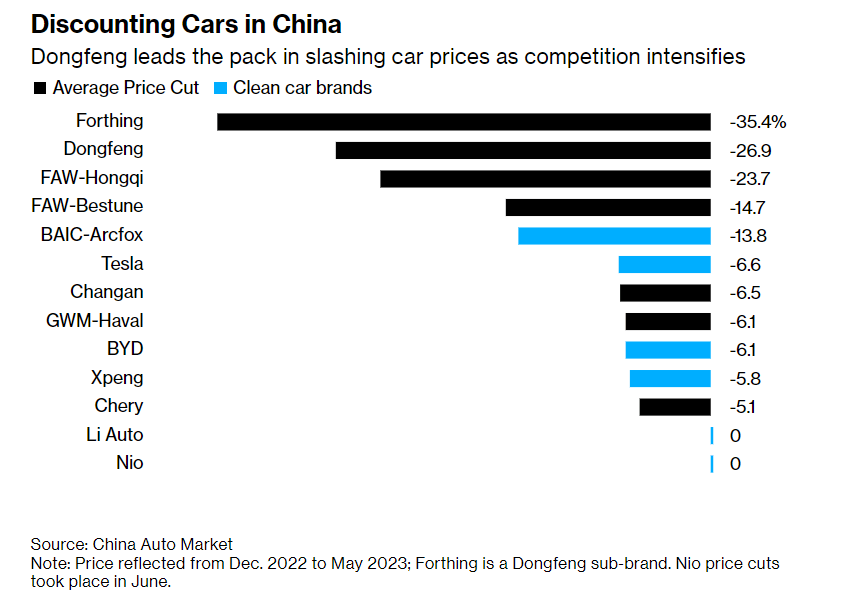

Limitations to the pact's effectiveness in stemming the price war is further corroborated by the CAAM's retraction of the agreement's reference to "pricing" just two days after the initial signing ceremony, citing the term's incompliance with China's antitrust regulations. The development underscores the complexity of stemming a competition-driven price war that has some automakers slashing their MSRPs by as much as 35% this year. The latest development is almost like a repeat of the CAAM's warning to the industry earlier this year that price cuts do not represent a "long-term solution" for shoring up auto sales, and demanded automakers to "return to normal order as soon as possible", which has done little to stop aggressive discounting campaigns from popping up across the Chinese auto market to date.

{kind=link}

{kind=link}

While some automakers like BYD and Tesla have implemented upward price revisions to some of its better selling models during the second quarter, much of the related activities have been driven by their respective fundamental strength rather than in response to calls from regulatory bodies in the industry. Meanwhile, the majority of domestic names such as NIO have yet to seen a structural recovery in take-rates that would allow upward adjustments to vehicle prices, especially amidst a deteriorating demand environment and intensifying competition.

Affordability and Performance Remain Keys to EV Adoption

Admittedly, the combination of intensifying competition within the broader EV market, alongside deteriorating economic conditions are likely to bode unfavorably for NIO in the near term, as prospective car buyers prioritize affordability and usability on discretionary big-ticket purchases. This is consistent with better-than-expected volumes observed at rivals Li Auto and BYD, likely due to their respective business strategies' effectiveness in addressing the two core consumer demands amid the slowing Chinese economy. However, NIO's recent release of upgraded models across its line-up on the latest NT 2.0 platform, complemented by discounted sticker prices, could potentially better address increasing calls for affordability, especially in economically sensitive lower-tier cities where future EV opportunities will become most concentrated.

Despite the government's introduction of favorable financial incentives for the EV sector earlier this year, including " credit support " for eligible purchases, alongside industry-wide promotional campaigns, EV sales have been tepid in the first half of 2023 compared to the same period last year. New energy vehicle sales in the first five months of 2023 increased by 41% y/y, decelerating from 120% y/y growth observed in the same period last year. Meanwhile, June NEV sales are likely to have decelerated further to growth of 26% y/y, representing a stark slowdown from the 130% y/y growth observed in the prior year when demand improved on the back of Shanghai's emergence from COVID-induced lockdowns at the time.

Specifically, the relative outperformance in take-rates observed across Li Auto and BYD, which offers competitively priced premium offerings across popular vehicle segments and easier to adapt powertrains, implies consumers' heightened focus on affordability in their purchase decisions, while also amplifying range anxiety as prominent barrier to EV adoption. This is also in line with expectations that much of Chinese EV sales growth going forward will likely be driven by the release of pent-up demand across lower-tier cities, which are more price sensitive with relatively limited accessibility to public charging infrastructure needed to support the emerging form of transportation - two factors that BYD and Li Auto's business models can effectively address.

However, we expect NIO's introduction of new models to be a better structural solution in overcoming said challenges and restoring delivery volumes in the second half. While prices of the new models have become more competitive than they were earlier this year, which could weigh further on NIO's ASP and, inadvertently, profit margins, they could potentially incentivize better take-rates by enabling capitalization of potential pent-up demand from prospective buyers who were not only holding out for the upgraded variants, but also looking to take advantage of the current discounts.

For instance, the all new ES6 five-seater - which has reduced its starting price from the previous RMB 368,000 to currently RMB 338,000, and represents NIO's lowest-priced SUV offering - makes a much better competition against rival BYD's newest Denza N7 five-seater SUV and Li Auto's Li L7 six-seater SUV, both of which are priced in the low RMB 300,000 range, in terms of affordability and performance. The lowest priced ET5 sedan based on the NT 2.0 platform, which features advanced functions spanning dual motors and ADAS in the standard trim, is also gaining traction as corroborated by its dominant sales mix since launch, underscoring end market demand for affordability and performance. And the latest introduction of the ET5 Touring, which boasts the same starting price as the standard ET5 at RMB 298,000, is expected to further the model's appeal to a broader end market and diversify NIO's end market exposure as competition intensifies:

As the world's first smart electric tourer, the ET5 Touring is designed to cover diversified scenarios for both individual and family users, significantly improving our competitiveness in the premium family vehicle market…This is going to help us to improve our overall product competitiveness, because we believe ET5 Touring can cater to the diversified needs of individuals and the family users and this can help us to boost our competitive -- of our product competitiveness in this specific market segment.

Source: NIO 1Q23 Earnings Call Transcript.

And the anticipated recovery in volumes, helped by the latest introduction of newer, competitively priced models, could also contribute towards economies of scale and drive incremental production cost efficiencies to compensate for the near-term pricing challenges, mitigating NIO's exposure to impacts of deteriorating economic conditions and intensifying competition in China. This is expected to drive a more evident positive impact on NIO's margin expansion efforts when cyclical tailwinds return to support realization of the higher price prospects of NT 2.0-based models over the longer-term.

Fundamental Analysis

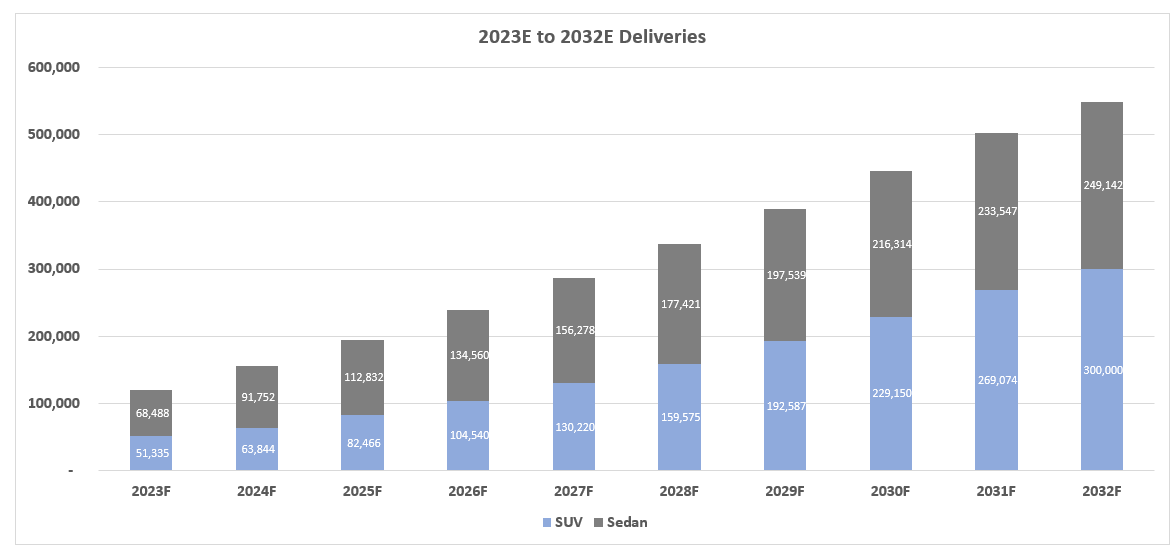

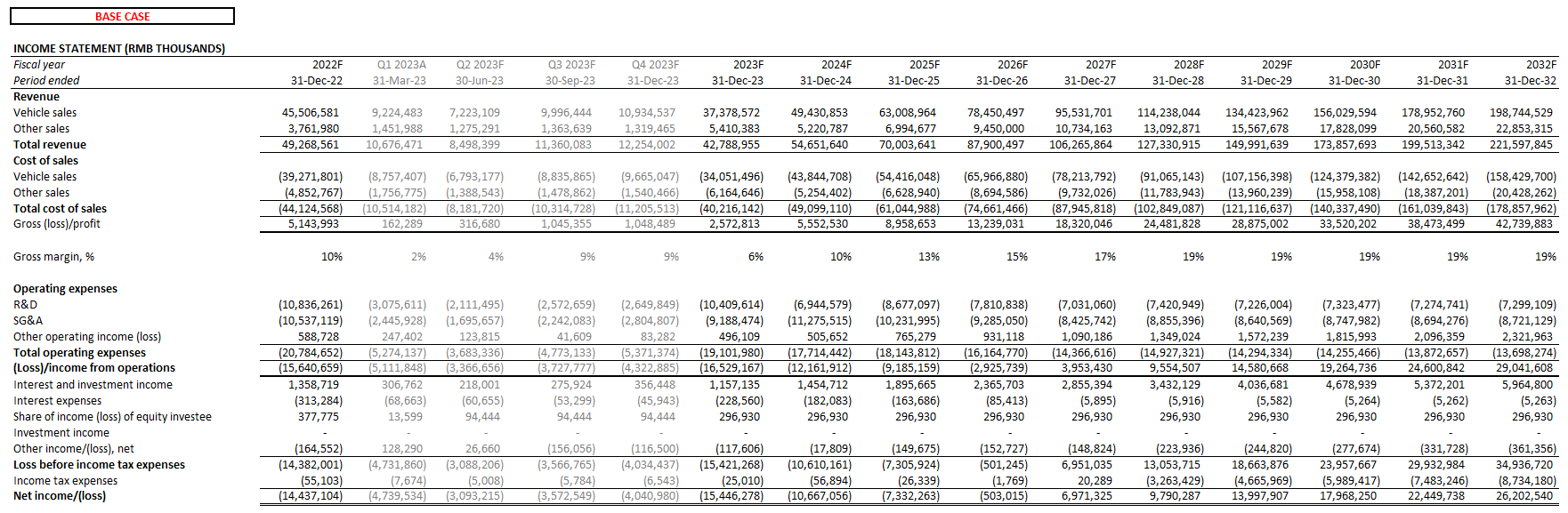

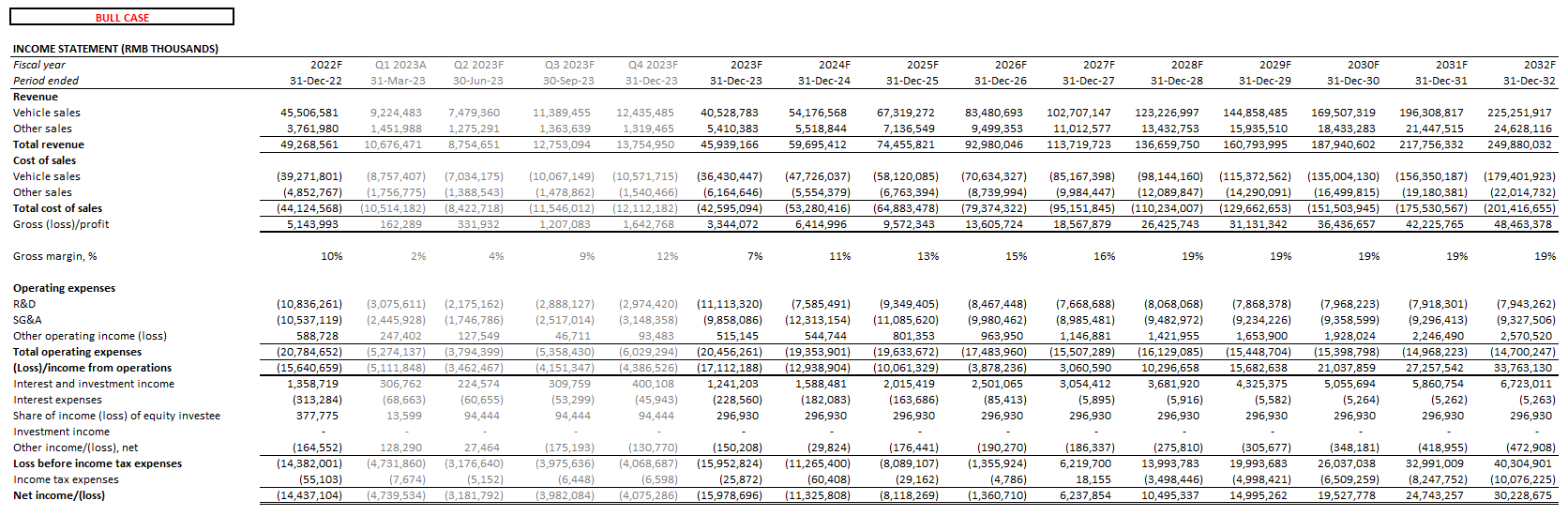

Taking into consideration NIO's actual second quarter deliveries, as well as recent data on the Chinese EV industry as well as the broader Chinese economy, our base case forecast expects revenue to decline on an annualized basis this year for the first time since early 2020 at the onset of the pandemic. While we expect delivery volumes to recover at a faster pace in the second half of the year compared to the tepid second quarter results, buoyed primarily by the introduction of new competitively priced vehicle models, take-rates are likely to remain in decline given limited clarity on China's near-term macroeconomic outlook as well as a relatively tough PY compare.

{kind=link}

And over the longer term, considering the launch of the mass market ALPS sub-brand in 2H24, we expect NIO's consolidated delivery volumes to expand at a 10-year CAGR of 16%. The growth assumption considers both NIO's production capacity as well as the estimated rate of EV penetration in the Chinese auto market from the current 30% range towards more than 50% by mid-decade. While vehicle ASP is expected to normalize as price war headwinds moderate over time, the metric's pace of growth is likely to be offset by the introduction of lower-priced ALPS models from the latter half of 2024 forward. As a result, revenue is expected to expand at a lower average rate of about 15% over the forecast period.

{kind=link}

{kind=link}

On the profitability front, considering the implementation of further price cuts following NIO's first quarter earnings call, the base case forecast expects vehicle gross margins to underperform management's forecast. Recall that management had expected higher prices on the all-new NT 2.0-based ES6 and ES8 SUVs, coupled with production ramp up to scale, as a key driver for margin re-expansion from the single digit percentage range in the first quarter back towards 15% exiting 2023. However, considering the lower starting prices on the all-new SUV models following the June price cuts, our base case forecast expects vehicle gross margins to improve at a relatively modest pace towards the low double-digit range exiting 2023, driven by anticipated scale in new model take-rates as discussed in the foregoing analysis.

Paired with expectations for elevated opex spend within the foreseeable future to support the continued ramp-up of NT 2.0 vehicles alongside SOP preparations for the ALPS sub-brand, we expect NIO's breakeven timeline to be further pushed out into 2027, compared to management's confidence expressed earlier this year in achieving profitability by 2024.

[NIO CFO Steven] Feng said the company is "confident" about breaking even at the group level next year. "Strong revenue growth together with tightened spending are the key to improved profitability," he said.

Source: Bloomberg News .

{kind=link}

NIO_-_Forecasted_Financial_Information.pdf

Valuation Analysis

{kind=link}

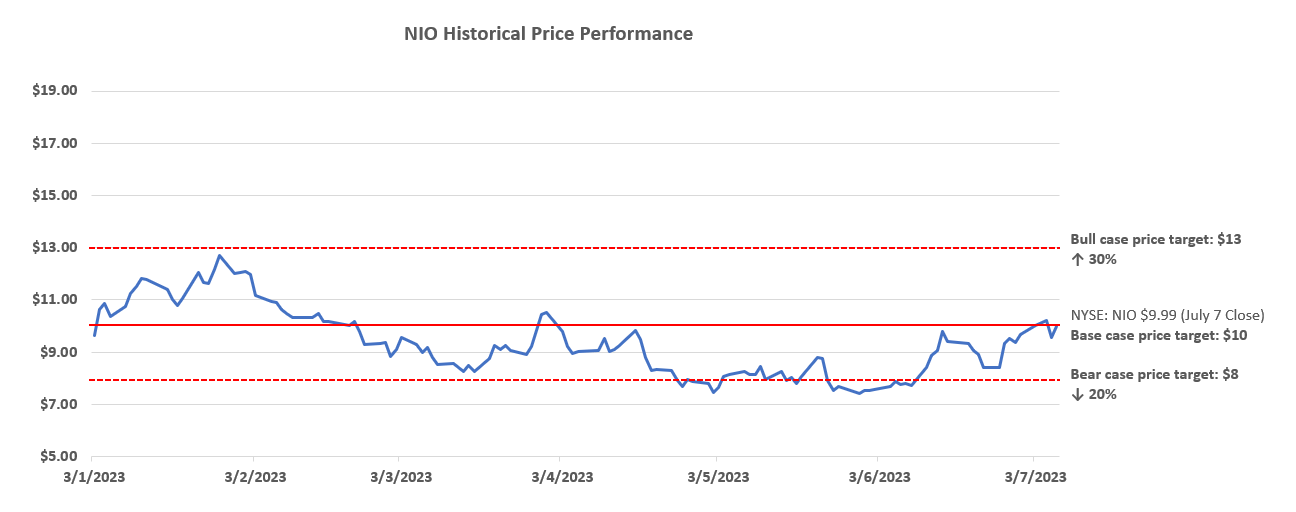

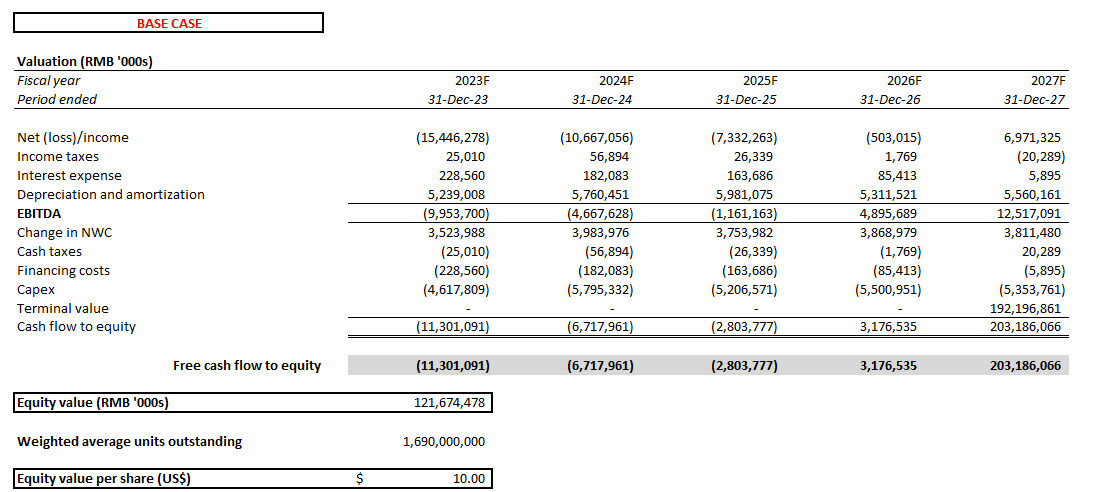

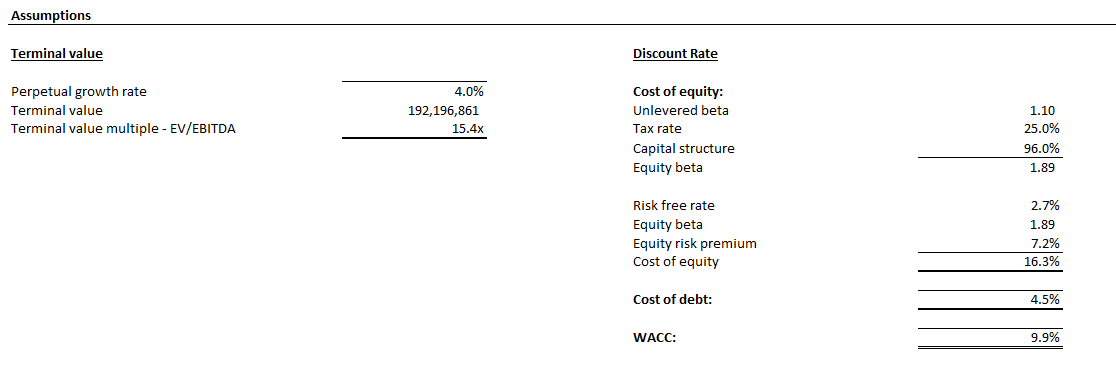

Drawing on projected cash flows taken in conjunction with our base case fundamental forecast for NIO, with the application of a 10% WACC in line with the company's capital structure and risk profile, the stock's current price at about $10 apiece (July 7 close) reflects market's pricing of an implied perpetual growth rate of 4% under the discounted cash flow analysis valuation method.

{kind=link}

{kind=link}

We believe the stock's latest rally has resulted in a better reflection of NIO's growth prospects, especially with anticipation for better penetration into emerging opportunities in the lower-tier cities after the impending start of productions on the ALPS sub-brand next year, despite near-term headwinds on profitability. Recall from our previous analysis that the stock is estimated to have been trading at a projected implied perpetual growth rate in the 1% range prior to the latest rally. We believe the shares' recent gains have resulted in a balanced risk profile between NIO's valuation and fundamental prospects at current levels. And looking ahead, incremental upsides will likely depend on further clarity from management on NIO's growth roadmap - particularly regarding ALPS' go-to-market strategy for optimizing capitalization on emerging demand in lower-tier cities - to compensate for decelerating penetration in the premium segment amid intensifying competition over the longer term.

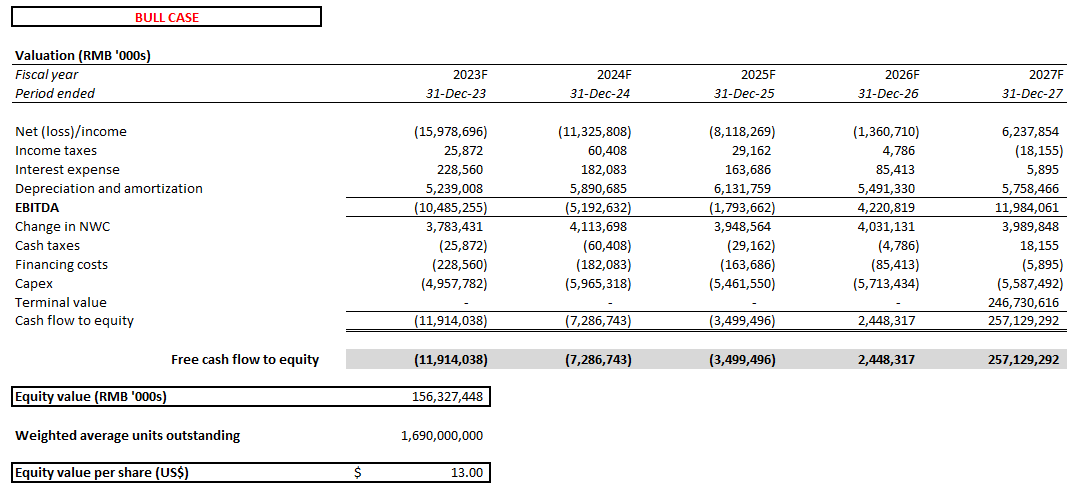

The upside scenario applies projected cash flows taken in conjunction with a bull case fundamental forecast that estimates revenue expansion at a 16% 10-year CAGR, driven by potential for better-than-expected ASP expansion and cost efficiencies realized through scaling production ramp-up on NT 2.0 vehicles and the impending ALPS sub-brand over the longer term.

{kind=link}

{kind=link}

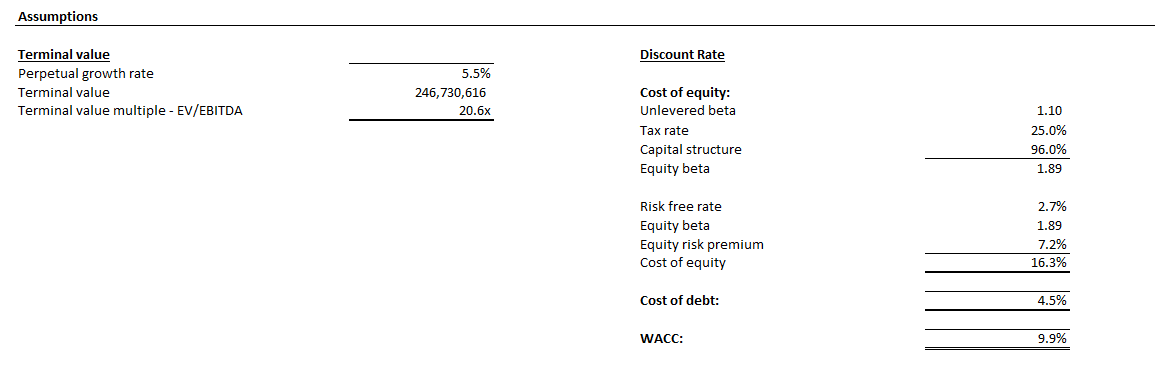

Applying the base case WACC of 10%, alongside an estimated perpetual growth rate of 5.5% in line with China's pace of longer-term economic growth to reflect NIO's potential for better capitalization on EV opportunities ahead in its core domestic market, the bull case valuation reaches $13 apiece. This would represent upside potential of 30% from current levels at about $10 apiece (July 7 close).

{kind=link}

{kind=link}

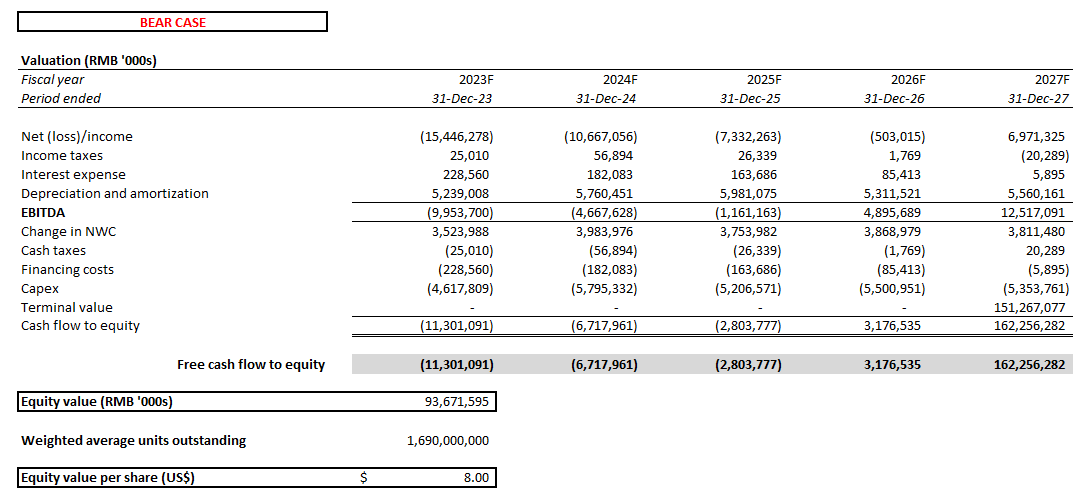

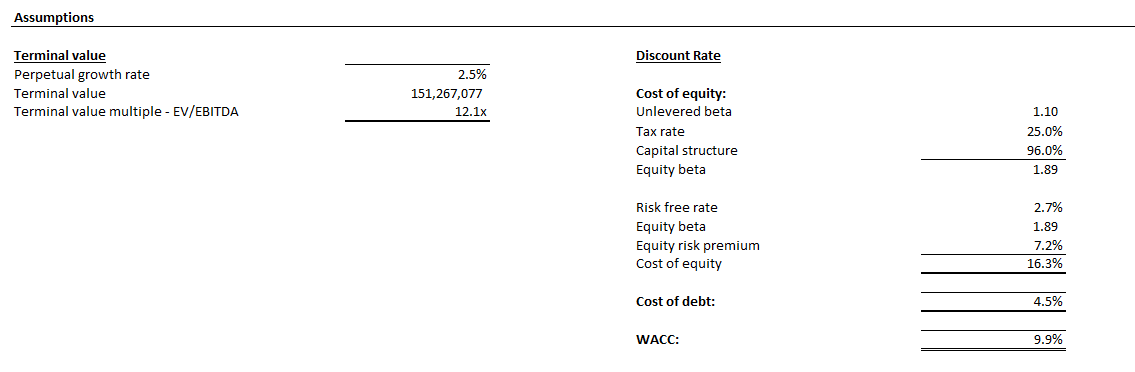

The downside scenario assumes the same base case fundamental estimates but at a lower estimated perpetual growth rate of 2.5% to reflect macroeconomic risks facing China's near-term growth prospects. Our downside valuation prices the stock at $8.

{kind=link}

{kind=link}

The downside scenario keeps the underlying cash flow projections unchanged from the base case as growth assumptions applied already take into consideration the near-term challenges to NIO's operations due to transient macroeconomic uncertainties, which have already been conservatively reduced from management's guidance. The reduced terminal growth assumption applied is in line with recent data that shows a further weakening of consumption and a growing " threat of deflation " in the Chinese economy, which could be an incremental multiple compression risk on the stock's near-term valuation prospects.

The Bottom Line

NIO is likely to bear the brunt of the ongoing EV price war that is expected to last within the foreseeable future, especially as the demand environment weakens amid a slowing post-pandemic economic recovery in China. This is consistent with limited effectiveness from recent government policy support aimed at shoring up EV demand in recent months. Consumers' sensitivity to prices is also reflected in resilient demand for lower-priced, relatively better value-for-money products offered by mainstream segment rivals like BYD and Li Auto, underscoring prioritization of affordability and performance amongst prospected buyers, especially amid the uncertain macroeconomic climate.

While we remain optimistic about NIO's longer-term growth prospects given its proven brand awareness in the Chinese EV market and upcoming launch of a lower-priced sub-brand to improve capitalization of budding opportunities across lower-tier Chinese cities, there is limited respite in the near term to rein in impacts ensuing from the ongoing price war. Paired with persistent macro-driven multiple compression risks, NIO Inc. stock's near-term upside potential from current levels will likely be limited.

In the meantime, we expect improvements on the take-rate of recently introduced NT 2.0-based models to be a driver of scale within internal operations that can partially cushion the impact of the challenging pricing environment on NIO's bottom-line - this leaves NIO's monthly delivery reports going forward as key focus areas for investors through the remainder of the year. Data supportive of resilient take-rates on the newly introduced NT 2.0 models will help to maintain durability in the stock's valuation at current levels, which prices in consistent progress in NIO's margin expansion efforts ahead despite transient cyclical headwinds on the underlying business' fundamentals.

For further details see:

We Like NIO, But Here's Why The Rally Likely Won't Sustain