SFL - We Put To Rest Our Concern About SFL's Large Container Fleet

Summary

- Earlier concerns about SFL Corporation's high concentration of container vessels needs a closer look now that market is weak.

- The influx of more newbuildings of container vessels will take time for the market to absorb.

- History tells us that this is a multi-year event.

- We stress test SFL's loss in revenue over the next 3 years.

SFL Corporation logo ((SFL))

Investment thesis

In our last article in November last year, we continued our line of 7 consecutive Buy stances on SFL Corporation (SFL). We need to go back to the middle of May 2020 to find our last Hold stance.

At that time we concluded that although the dividend yield at the time was 13%, the risks from their offshore drilling assets and the large concentration in containerships were a concern to us.

At that time, we highlighted one risk to the thesis as the large deterioration in charter rates for container vessels. We wrote:

Many new-building deliveries are expected and if we are going to have a prolonged economic slowdown, liner companies will have to adjust their fleet."

Their offshore drilling assets are no longer a concern to us.

However, we have taken a closer look at SFL's exposure to the container ship market and its potential risk and would like to share this with our readers

The containership market

What a difference a year makes.

A year ago, liner companies were outbidding each other to get hold of any ship that could carry containers.

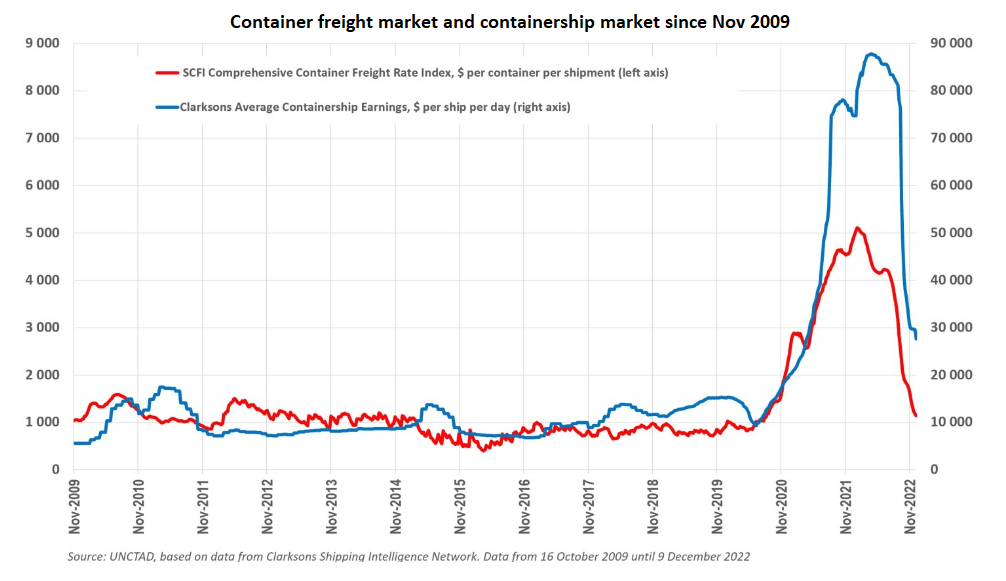

Let us start by looking at the market over a long period of time. That helps to put things into perspective.

Container freight and ship market since November 2009 (Splash 247)

{kind=link}

At the beginning of last year, the average earnings for containerships were nearly USD 90,000.

It did collapse throughout the year.

The best way to determine whether the market can absorb the addition of supply is to look at the order book as a percentage of the present fleet and what is the expected yearly fleet growth.

The order book, as of the end of last year, stood at 29% according to Bimco . The fleet is expected to grow by 7.8% in 2023 and another 8.3% in 2024. The demand growth for container movements is estimated to be 3.5% per year.

The total number of container vessels that went for demolition in the entire 2022 was just 10 vessels, totaling 198,488 deadweights.

But in January this year, so far there have been 13 vessels going for demolition with a total of 278,805 deadweights. In other words, in less than a month, we have already surpassed the entire fleet attrition of last year.

That looks promising.

When we look at the supply up against the demand, Bimco stated that there is a surplus of supply of roughly 1 million TEU in the coming year. It hits the largest ships the most, as 80% of the newbuildings coming are in that category.

That is 50 vessels of 20,000 TEU capacity the market really does not need.

Liner companies have already started with blank sailings and slowing the speed of vessels,

Time charter rates could fall to levels that only cover the operating costs of a vessel. Not servicing the capital costs.

But as of 23 January 2023, rates for some of the smaller vessels are actually not that bad.

Harpex - container vessel rates as of 20 January 2023 (Harper Peterson & Co.)

{kind=link}

The numbers for the SFL liner segment

During Q3 of 2022, which is the latest financial data we have, we learned that their liner segments, which also included revenue from their car carriers, generated a total charter hire of USD $98 million, including USD 10 million in profit share contribution related to fuel savings.

We estimate that the total charter revenue for SFL in FY 2022 will be about USD 688 million, and for the liner division, it should come in at around USD 372 million.

At 54% of the revenue, it shows the importance of the health of this business.

We wrote earlier that SFL's share price did not benefit when others did in 2021 when container rates shot up in 2021. That is the nature of having a fleet fixed away on long-term charters. You do not benefit from sudden moves. The flip side to that coin, as we see now, is that it also does not kill you when the market tanks. That is why we like companies that have long-term charter coverage.

Ship by ship

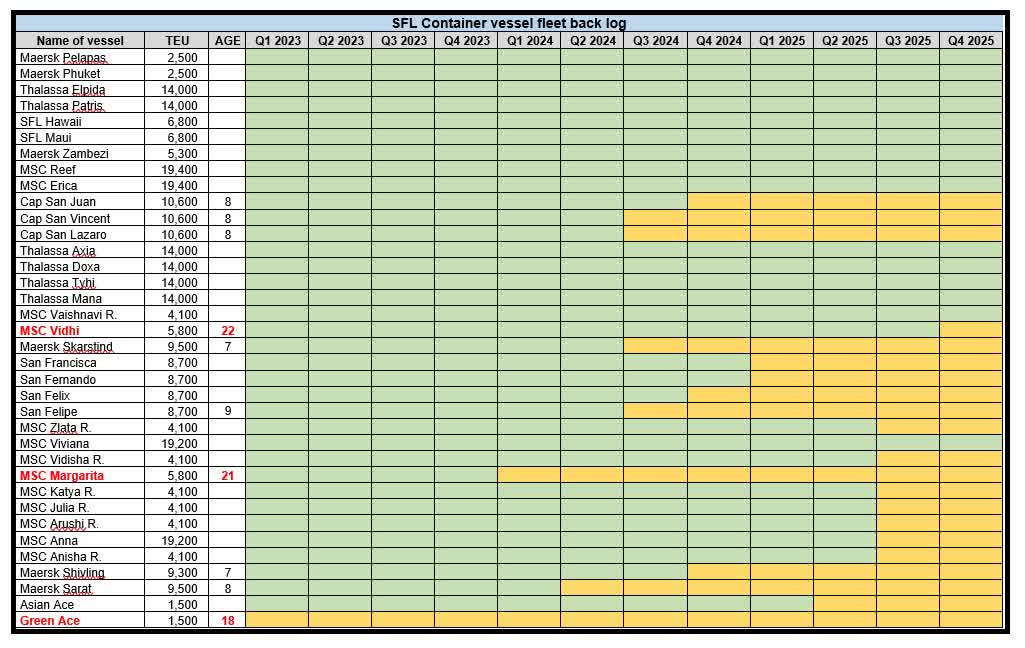

Let us look at the container ship fleet ship by ship as their charters expire over the next 3 years.

SFL - Container fleet backlog ((SFL))

{kind=link}

Presently trading spot market in 2023 is the smallest vessel, the 1,500 TEU vessel "Green Ace".

She is used as a feeder vessel in the Arabian Gulf. We do not know at what rate the vessel is fixed. It could be considerably less than what a 1,700 TEU feeder vessel which ship brokers Harper Petersen & Co stated could now earn approximately USD 14,500 per day since it is of a rather old age and somewhat smaller.

But its break-even rate is probably less than half of that so it should still be contributing to SFL's profit. Therefore, it is not much concern to us if this ship is trading on short-duration charters.

It must also be debt free by now, or very close to it, and have a book value close to what we believe the market value to be, which is about USD 7 million. Should this market deteriorate further and make it loss-making, it would not be a problem to sell the vessel either for further trading or for demolition.

No other ship in 2023 is coming off charter, as can be seen above.

In 2024, there are 8 vessels coming off charters.

- Charter free in Q1

Their oldest containerships are " MSC Vidhi " and the " MSC Margarita ".

In February 2019 SFL agreed with the charterer to extend the charter of these two old vessels up to Q1 of 2024. These vessels are on bareboat charter at about USD 6,500 per day per vessel. The good thing is that charterers have a purchase obligation at the end of this charter, so there are no liabilities related to what to do with these two old ships once the charter comes to an end. MSC has to buy them back at the agreed price.

- Charter free in Q2

A much younger vessel, the 8-year-old "Maersk Sarat" of 9,500 TEU capacity is coming off charter. We estimate that the charter rate presently is about USD 40,000 per day plus profit sharing from the outfitting of a scrubber.

- Charter free in Q3

Also 8 years old are the two 10,600 TEU vessels " Cap San Vincent " and " Cap San Lazaro ".

Somewhat smaller, and one year younger is the " Maersk Skarstind " of 9,500 TEU which is coming off charter. Also on charter to Maersk like the rest of the ships coming off charter in Q3 is the 9-year-old " San Filipe " of 8,700 TEU. These are also on charter at approximately USD 40,000 per day plus profit sharing from the outfitting of a scrubber.

- Charter free in Q4

In the last quarter of the year, 3 vessels are coming off charter. They are the 8-year-old 10,600 TEU vessel " Cap San Juan ", the 9-year-old 8,700 TEU vessel " San Felix ", and the 7-year-old " Maersk Shivling " which is 9,300 TEU.

In March 2020, the charters on the three 9,300 to 9,500 TEU container vessels " Maersk Sarat" , " M aersk Skarstind" and " Maersk Shivling" were extended by 44 month period at a revised charter hire. We do not know the extended rates, but we calculated the rates for the initial period of 5 years to be about $38,000/day. The extension to the charter was done just before the market took off, so we assume that the rates were only increased to about $40,000/day.

In 2025 , there are only 3 more vessels coming off charters.

- Charter free in Q1

"San Francisca" and "San Fernando". Our estimate is that these are earning about $38,000 per day per vessel.

- Charter free in Q2

The sister vessel to "Green Ace", the 1,500 TEU old feeder vessel "Asian Ace" is coming off charter. We are not concerned about this vessel either. See our explanation above regarding the "Green Ace".

No other vessels are coming off charter in 2025.

We are not saying that the ships that are coming off charter will all be laid up without any employment. That is the worst-case scenario. In all likelihood, they will either be renewed with the same charterers at market rates or with other charterers.

This is especially the case for modern vessels.

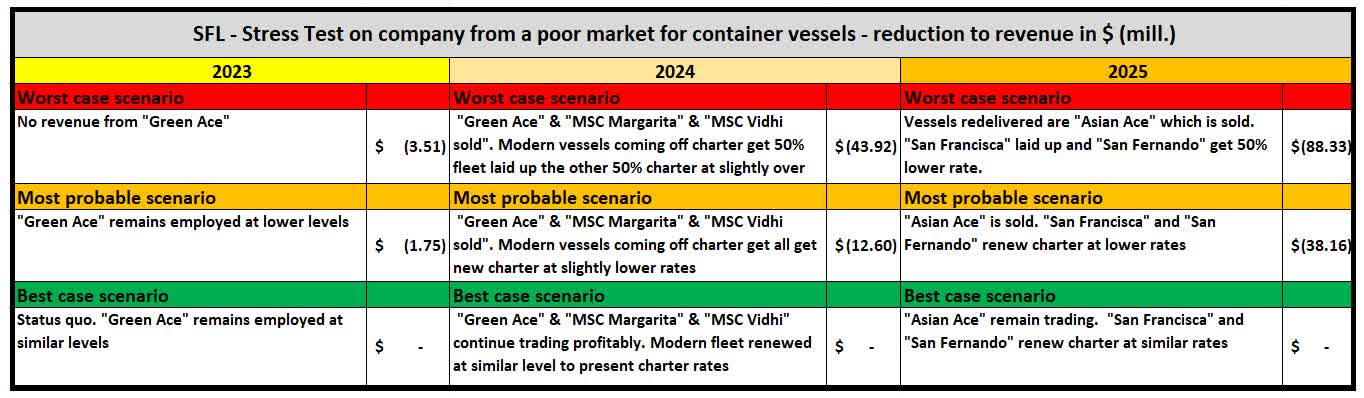

Our stress test on SFL

Just like banks test the potential liabilities of a bank in the event of severe market drawdowns, where regulators use a bank's common equity tier 1 ratio to determine if they can withstand a serious shock to their expected credit losses, we too should be able to look at how SFL's financial position could handle any further deterioration to their business.

We need to set some parameters and some assumptions. None of them are perfect but we try to run different scenarios. They are not based on a prolonged and deep economic recession.

Nevertheless, we have just seen above how long time it can take to absorb a large influx of tonnage capacity. It can take many years.

SFL - stress test on revenues (Data from SFL. Calculation by author)

{kind=link}

For simplicity, we shall look at the reduction in relation to its present estimated FY 2022 charter revenue of about USD 688 million. As we stated earlier, there is no concern for 2023.

However, in our worst-case scenario, a reduction of USD 44 million in 2024 would be 10.5% of their total revenue. This is not insignificant but it is absorbable without too much strain on their finances.

Should the poor market condition continue throughout 2025, this loss grows to USD 88 million loss for that year.

SFL's main customers, the liner companies have made a lot of money over the last couple of years. Therefore, we do not at this point in time see any likelihood that they will face any difficulties from charterers not honoring their agreements.

Conclusion

We believe that the high charter coverage for the liner division will shelter SFL from the current lower charter rates in the container ship market.

The rates that the ships are fixed on were also considerably lower than the elevated rates we saw in 2021. This means that it is less likely that SFL's ships will be the first ships Maersk and MSC would want to cancel.

After our evaluation and stress test, we give SFL a "green light".

It is also a testament to the importance of two things.

First of all diversification. Secondly is the comfort one can take from having longer-term charters as opposed to relying on spot rates.

Our Buy stance remains.

For further details see:

We Put To Rest Our Concern About SFL's Large Container Fleet