CA - WELL Health Technologies: Exceptional Growth But Price Has Soared

2023-10-09 16:58:58 ET

Summary

- Canadian healthcare services provider WELL Health Technologies has seen a 700% rise in its stock price over the past five years, far surpassing the sector.

- The company has pursued a fast-paced acquisition strategy for growth, which has increased its revenues multi-fold and it's also profitable on an operating basis now.

- Its non-GAAP market multiples however, don't compare favourably with peers, indicating that it's best to Hold the stock for now.

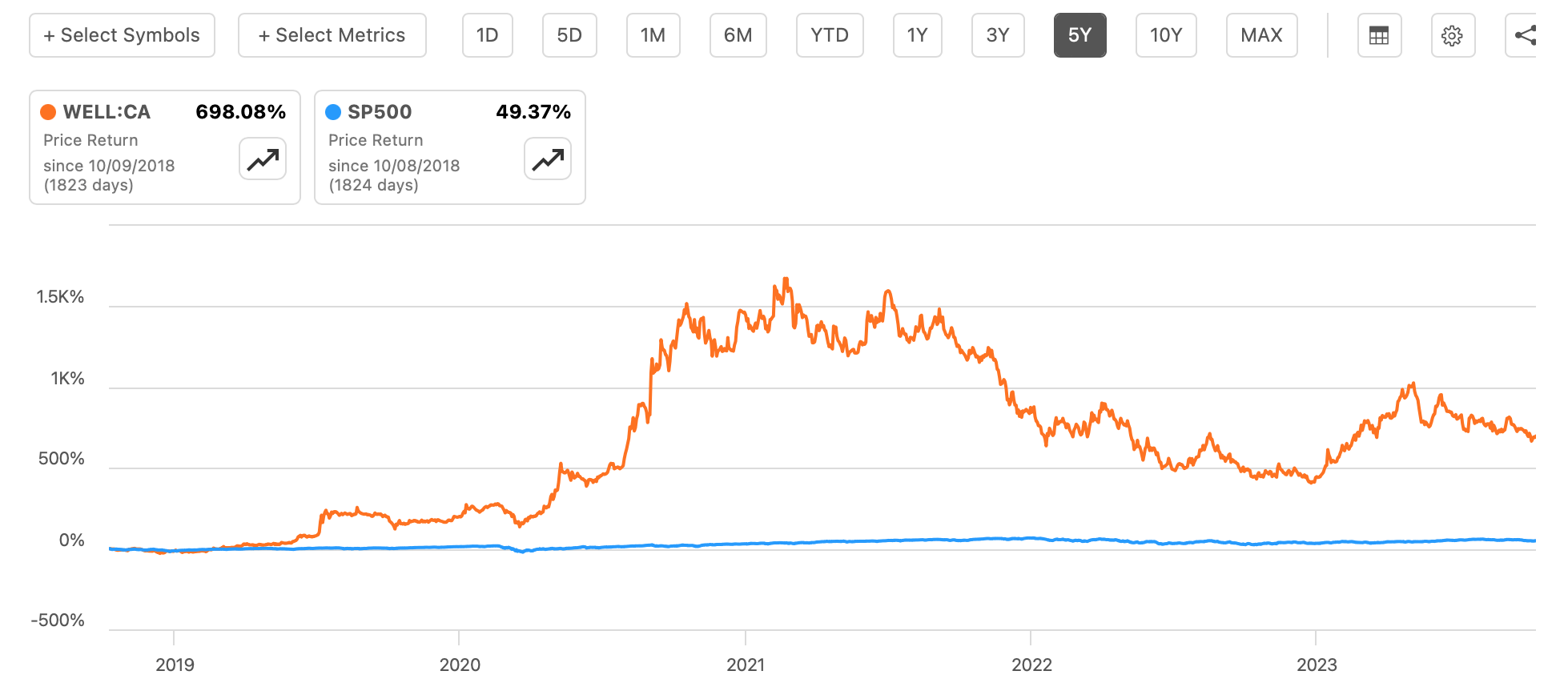

Over the past five years, the Canadian healthcare services provider WELL Health Technologies ( WELL:CA ) has risen by nearly 700%. By comparison, the S&P 500 ( SP500 ) has risen by a far smaller 50% over this time. WELL’s performance shines even more when compared with the S&P 500 Health Care Index, which has risen by just 7% in the last five years.

As encouraging as this is, here I explore the company in some detail as to whether there's more steam in the stock.

Price Return Comparison With S&P 500 (Source: Seeking Alpha)

{kind=link}

The company

Founded in 2010, the company provides a range of services like a network of clinics. It also provides a range of patient services as well as saleable technology solutions for both clinics and medical practitioners.

The USP

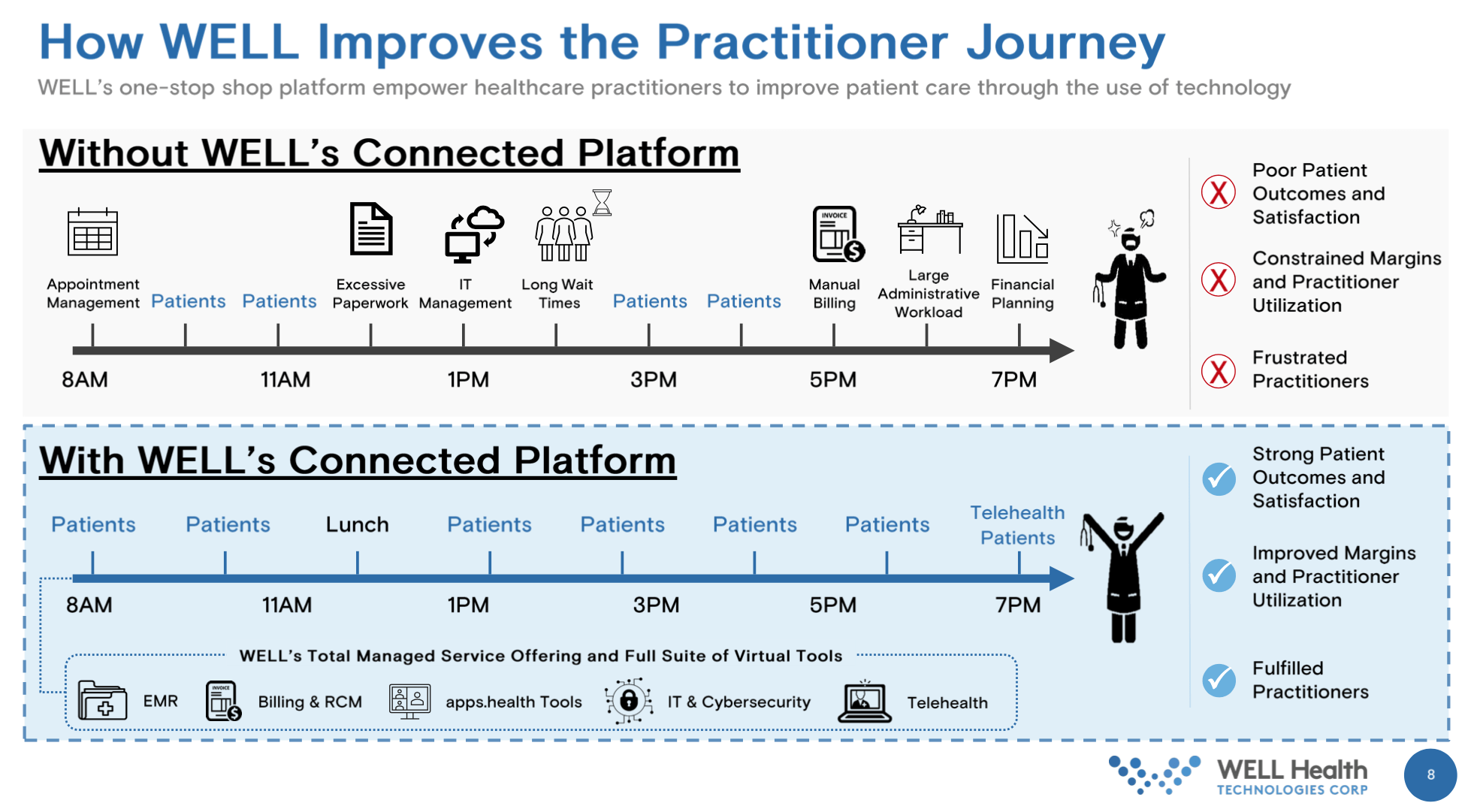

WELL’s unique selling point is enabling productivity improvements for medical practitioners considering that 50% of medical professionals’ time is estimated to be spent on administrative tasks, while only 30% is devoted to patients. Its support services free up this time by managing administrative tasks like appointment management, billing and other paperwork.

Source: WELL Health Technologies

{kind=link}

Business units

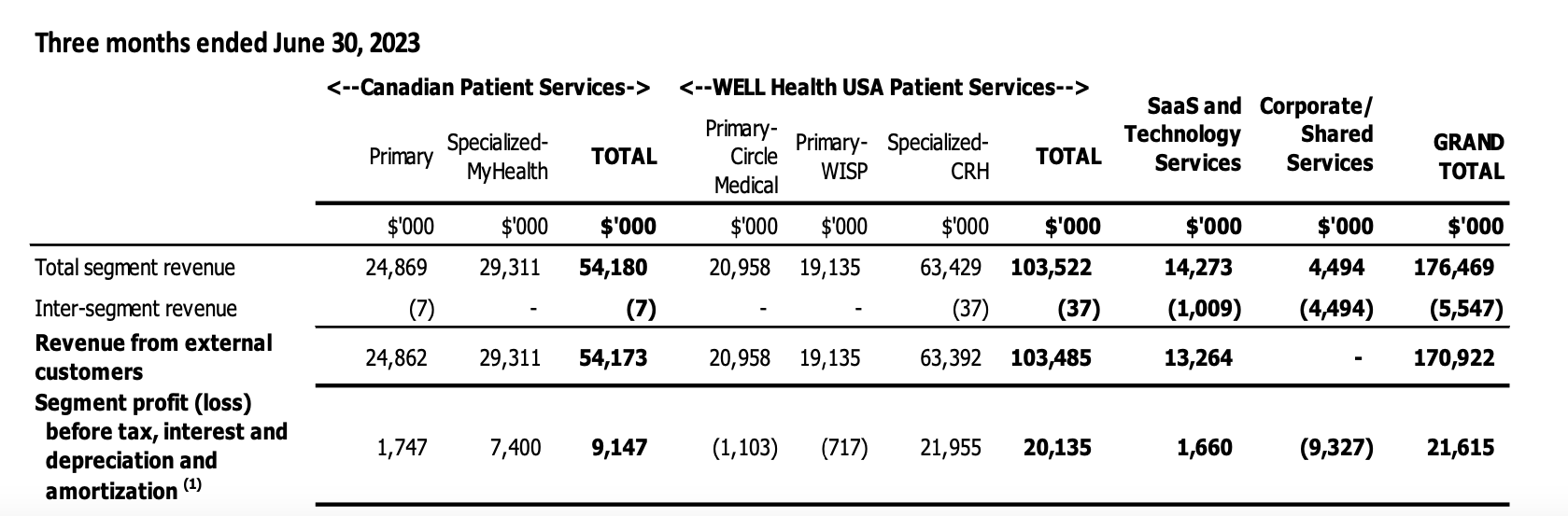

The company has three business units. The biggest is US Patient Services, which brought in 60.5% of the revenues for the three months ending June 2023 . More than half of this unit’s revenues come from the CRH segment, the gastroenterology focused patient services provider. The other segments are Circle Medical, which provides both virtual and in-person mental health care, and Wisp, which provides online women’s health services.

Revenues By Segment (Source: WELL Health Technologies)

{kind=link}

The second business unit is Canadian Patient Services, which accounted for 31.7% of the revenues during the quarter. This unit is divided into clinics in the Ontario province, under the MyHealth segment, and diagnostics services like X-rays and ultrasounds.

SaaS and Technology Services is the third business unit that brought in the remaining 7.8% of the revenue. Through this unit, WELL provides its national leading services in billing, among other support services as well as cybersecurity services for patient data protection.

Impact of acquisitive growth on financials

Almost 78% of WELL’s revenues today are because of its acquisitions made during 2020 and 2021. This includes all three segments in its US operations as well as the Canadian MyHealth. As a result, the company’s revenues have risen by over 17x between 2019 and 2022.

Trends In Key Financials (Source: Seeking Alpha)

{kind=link}

It has also swung into operating profits of CAD 39.2 million for the trailing twelve months [TTM], reporting positive operating income in both 2021 and 2022, from a CAD 7.5 million loss in 2019. On the downside, while it did report a small attributable net profit for the full year 2022, for the TTM it has fallen back into losses for two reasons.

One, its interest expenses have risen in tandem with debt. Before anything else, even with an almost 18x increase in debt between 2019 and 2022, its TTM debt-to-assets ratio at 27%, still looks good. However, at a time of rising interest rates, it has meant higher interest expense, resulting in an 18x increase between 2019 and 2022. This shows up not only in a slightly less-than-ideal TTM interest coverage ratio at 1.3x but also eats into the net income.

Two, the share of minority interest in the net income is also applicable now, considering that it has a majority stake in its US acquisitions like Circle Medical and Wisp, among more acquisitions made since 2021.

Latest developments and outlook

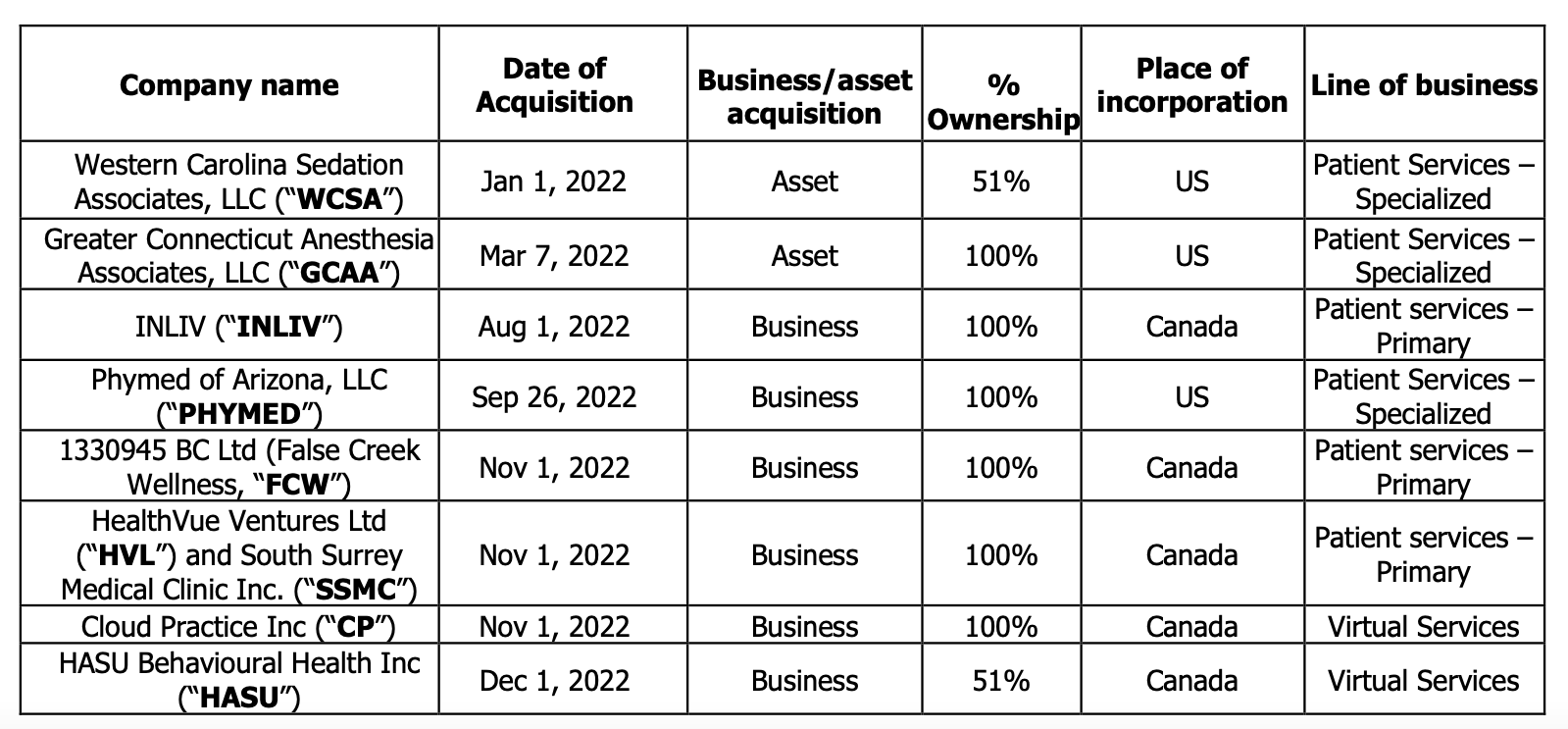

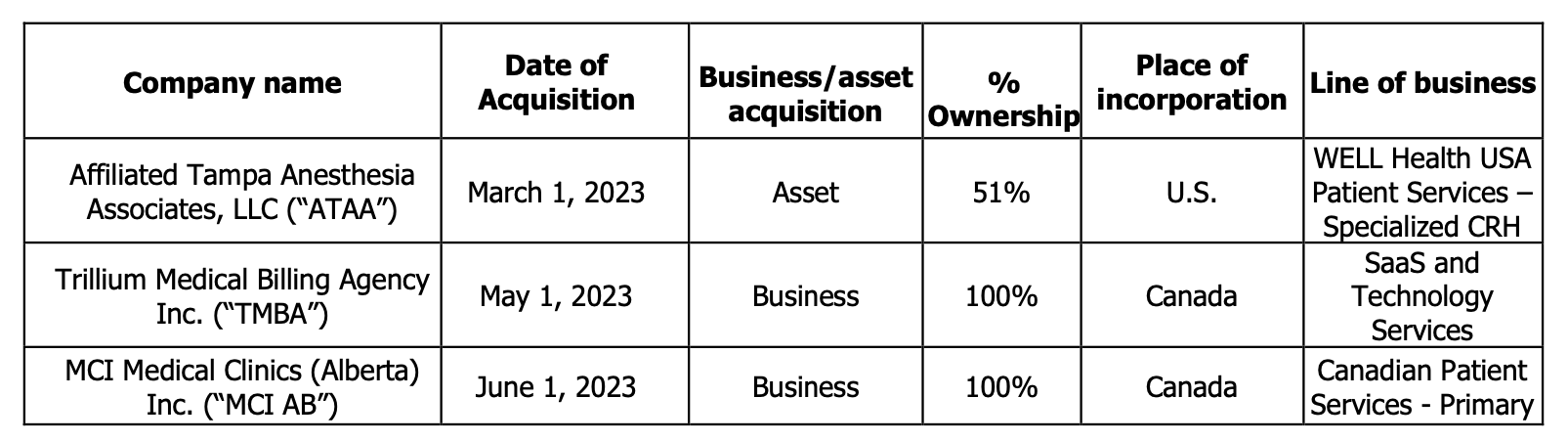

Even though they don’t show up in its financials yet, the company has bought out or bought majority stakes in more companies in 2022 and continuing into 2023 (see tables below).

Acquisitions in 2022 (WELL Health Technologies) Acquisitions in 2023 (Source: WELL Health Technologies)

{kind=link}

{kind=link}

These are naturally expected to add to WELL’s revenues as well. The company projects revenues of CAD 740-760 million in 2023. At the mid-point, this implies an almost 32% year-on-year [YoY] growth.

It also expects a 10% increase in adjusted EBITDA levels from CAD 104.6 million in 2022. If the adjusted net income to adjusted EBITDA ratio stays constant at 51% in 2023, the company’s adjusted EPS rises slightly to CAD 0.245 in 2023 from CAD 0.24 in 2022.

What the market multiples say

This results in a forward price-to-earnings (P/E) ratio for 2023 at 16.7x, which is competitive compared to the median for the Health Care Services sector at 18.8x. Its TTM P/E however, is at 17.3x, which is almost in line with the sector median at 17.6x.

Its multiples don’t compare favourably with other Canadian healthcare services providers like the specialty hospitals company Medical Facilities Corporation ( DR:CA ), with a non-GAAP TTM and forward P/Es at 10.2x and 8.6x respectively or the US based diagnostics provider Laboratory Corporation of America ( LH ) at 12.5x and 14.7x respectively.

What next?

Based on the market multiples, the case for WELL looks weak right now as its price has risen significantly over the years. This price rise isn’t for no reason, to be sure. The company has actively pursued an acquisition strategy, which includes its entire US operation that brings in more than half its revenues now. It continues to do so, making multiple acquisitions in 2023 so far alone.

The strategy has clearly done well. Not only have its revenues grown multi-fold in the past few years, but it has also started reporting a positive operating income, compared to being loss-making pre-pandemic. While it’s still net loss-making on a reported basis, it is profitable in non-GAAP terms.

Going forward, its revenues are expected to continue growing at a fast clip, and while its debt could continue rising, it's significantly in check. The company also benefits from being a defensive stock at a time when the outlook on the economy is uncertain. The only catch is, that it doesn’t look attractive compared to peers and its TTM P/E is also in line with the sector. I think it’s best to Hold for now and buy only if it dips significantly.

For further details see:

WELL Health Technologies: Exceptional Growth, But Price Has Soared