MCD - Wendy's: Try Its Pub Burger But Hold The Stock

2023-07-21 06:35:30 ET

Summary

- Wendy's, a quick-service restaurant franchise, is gaining reputation for its food quality but lacks widespread reputation.

- The company has some opportunities internationally and to grow its dayparts.

- Despite potential growth opportunities, the stock is a bit overvalued.

While I've become a fan of Wendy's (WEN) food, I'd prefer to be a buyer of the stock when it's on the value menu.

Company Profile

WEN owns and franchises in namesake quick-service restaurants both in the U.S. and abroad. The QSR operator specializes in hamburgers, while also offering other fast-food staples such as chicken nuggets, chicken sandwiches, French fries, and salads, as well as a variety of breakfast items in North America.

At the start of the year, the company had nearly 6,000 locations in the U.S., of which just over 400 were company owned. It has an additional 1,100 locations outside the U.S., of which 12 were operated by the company in the U.K.

For its U.S. franchises, WEN receives a 4.0% monthly royalty, as well as a $50,000 technical assistance fee for each new restaurant location opened. Agreements generally last 20 years. In markets outside the U.S. and Canada, WEN grants franchise or license agreements for a period of 10-20 years. WEN generally gets an initial technical assistance fee as well as monthly fees based on a percentage of gross monthly sales of each restaurant.

Opportunity and Risks

In my 40+ some years of existence, I had never tried WEN until this year. Why would I get a burger from the #3 burger fast food burger place, when there was McDonald's (MCD), and then later more upscale QSR establishments like Shake Shack (SHAK) or Five Guys. Then one of my daughter's softball coaches told me to try WEN, so I did.

I grabbed one of their pub burgers, and it was phenomenal, the best QSR burger I've ever had. I'm a sucker for a pretzel bun, but the burger was much better than anything I've had from Shake Shack, Five Guys, or any other fancier burger place. And therein lies both some of the opportunity and risk associated with WEN. One opportunity is that the food is pretty darn good, but the issue is that the brand doesn't necessarily have that widespread reputation.

WEN actually took over the #2 burger spot from Burger King about a decade ago, as the company shifted to be a little more higher end offerings. So, the company has been gaining share and its reputation is growing, but it's never had the buzz of SHAK or In-N-Out Burger or the marketing muscle of MCD.

WEN has done a nice job with product innovation. In addition to my favorite, the pub burger, it also solid offerings like its Summer Strawberry Salad and Ghost Pepper Ranch Chicken Sandwich. Now it's just a question of getting the word out there and gaining buzz.

Discussing its marking on its Q1 earnings call, CEO Todd Penegor said:

" As our strong programs drive more customers to our restaurants, we are committed to delivering an experience that brings them back more often. Our first quarter customer satisfaction scores and speed of service improved markedly versus the prior year and prior quarter as restaurants were better staffed, turnover improved and our systems focused on operational excellence sharpened even further. As we turn to the second quarter, we will promote products across a variety of price points and occasions with dedicated messaging behind our ownable Biggie Bag platform, the return of the fan favorite Strawberry Frosty and bringing the heat like only Wendy's can with the addition of the Ghost Pepper Ranch Chicken Sandwich to our Made to Crave lineup. We also have plans in place to accelerate our momentum at the bookends of the day, breakfast and late night. We have plans for increased activity to drive the breakfast business in the U.S. and Canada for the remainder of the year and will lean into our playbook of building awareness around our craveable products, launching exciting menu innovation and promoting targeted trial-driving offers."

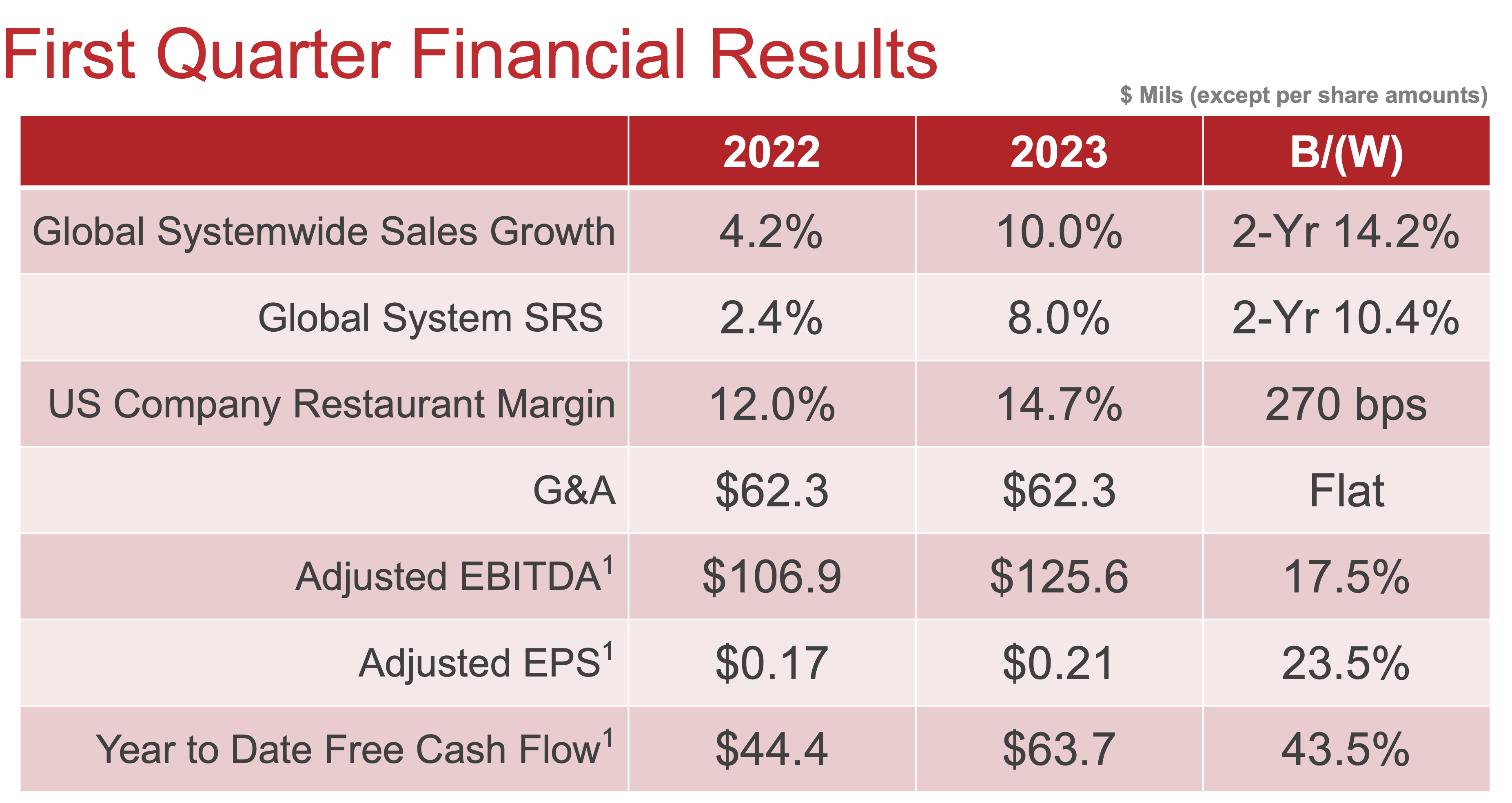

WEN's food offerings and marketing appear to have bee resonating with customers. In Q1, the company saw its same-store sales rise a robust 7.2% in the U.S. It was even stronger in international markets, with same-restaurant sales of 13.9%.

{kind=link}

Now international is another potential growth driver for WEN. With only over 1,100 locations outside the U.S., the company still has a nice runway for international growth. The company plans to grow its number of unit opening to 2-3% in 2023-24, accelerating the pace to 3-4% in 2005.

Expanding daypart is another potential driver for WEN. Outside of North America, the chain doesn't offer breakfast. Meanwhile, the company is looking to lean into night late and breakfast in the U.S. and Canada.

Technology, digital, and delivery continue to be a focus for WEN, as it does for much of the QSR space. The company is looking to use voice AI and digital menu boards to help improve the customer experience. The voice AI, which is in partnership with Google (GOOGL), will look to help speed up the drive-thru order station.

When looking at risks, the economy remains a big one for the restaurant industry. So far, the QSR industry hasn't seen any issues, as price increases have more than made up for any traffic declines. For WEN's Q1 U.S. SSS, nearly 7% of the 7.2% increase came from price, with traffic up less than 1%. When inflation slows and price increases wane, growing SSS for WEN and the industry should become more difficult.

Meanwhile, the burger QSR space obviously comes with a lot of competition. WEN sits right in the middle with pricing and perception. Right now the company said it is doing well with households making over $75,000 and under that amount, but the over $75,000 is growing faster.

Valuation

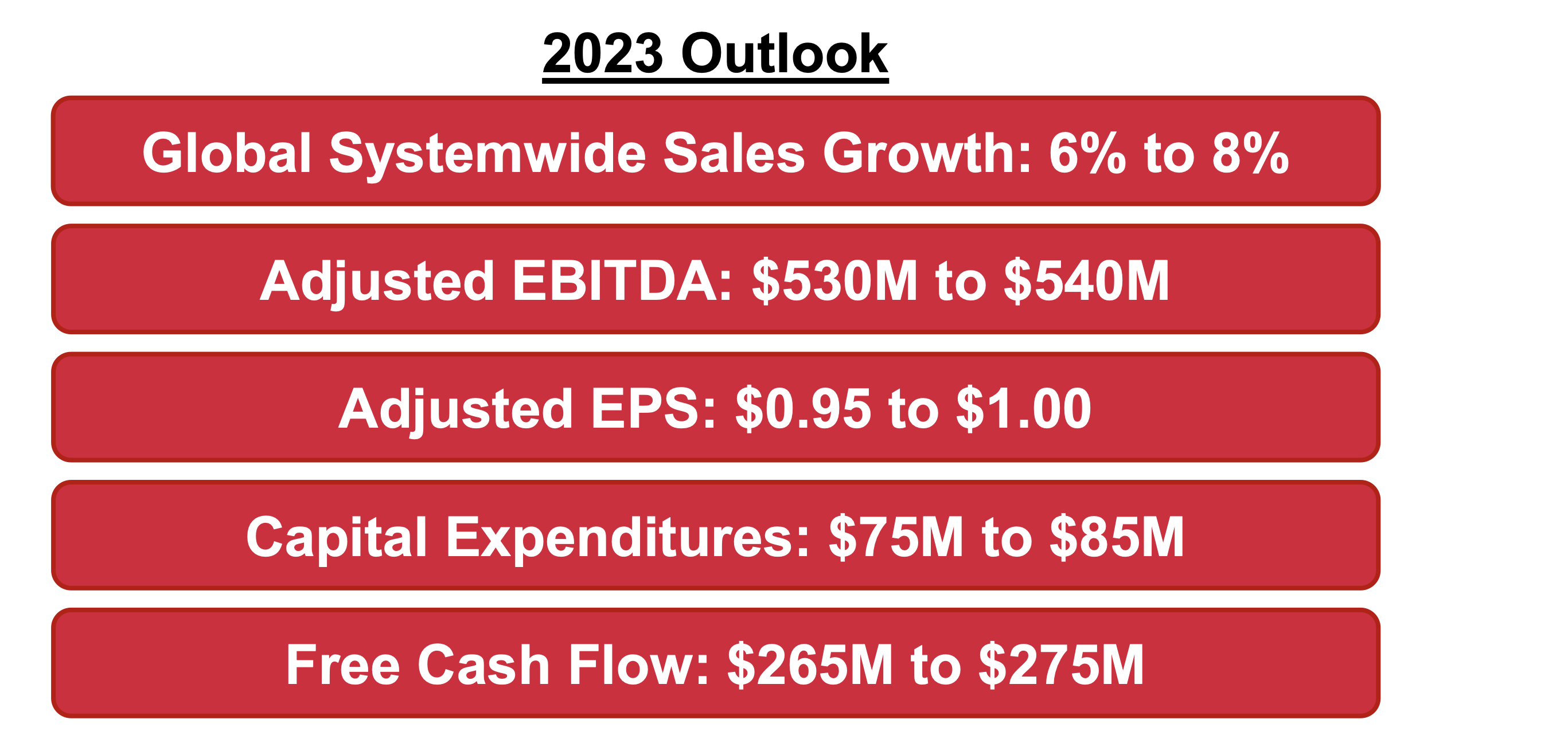

WEN stock currently trades at 15x the 2023 consensus EBITDA of $538 million and 14x the 2024 consensus of $574.6 million.

The company trades at 22x the 2023 EPS census of 98 cents, and 19x the 2024 consensus of $1.12.

Revenue growth is expected to grow 5.6% this year, and 4% next year.

{kind=link}

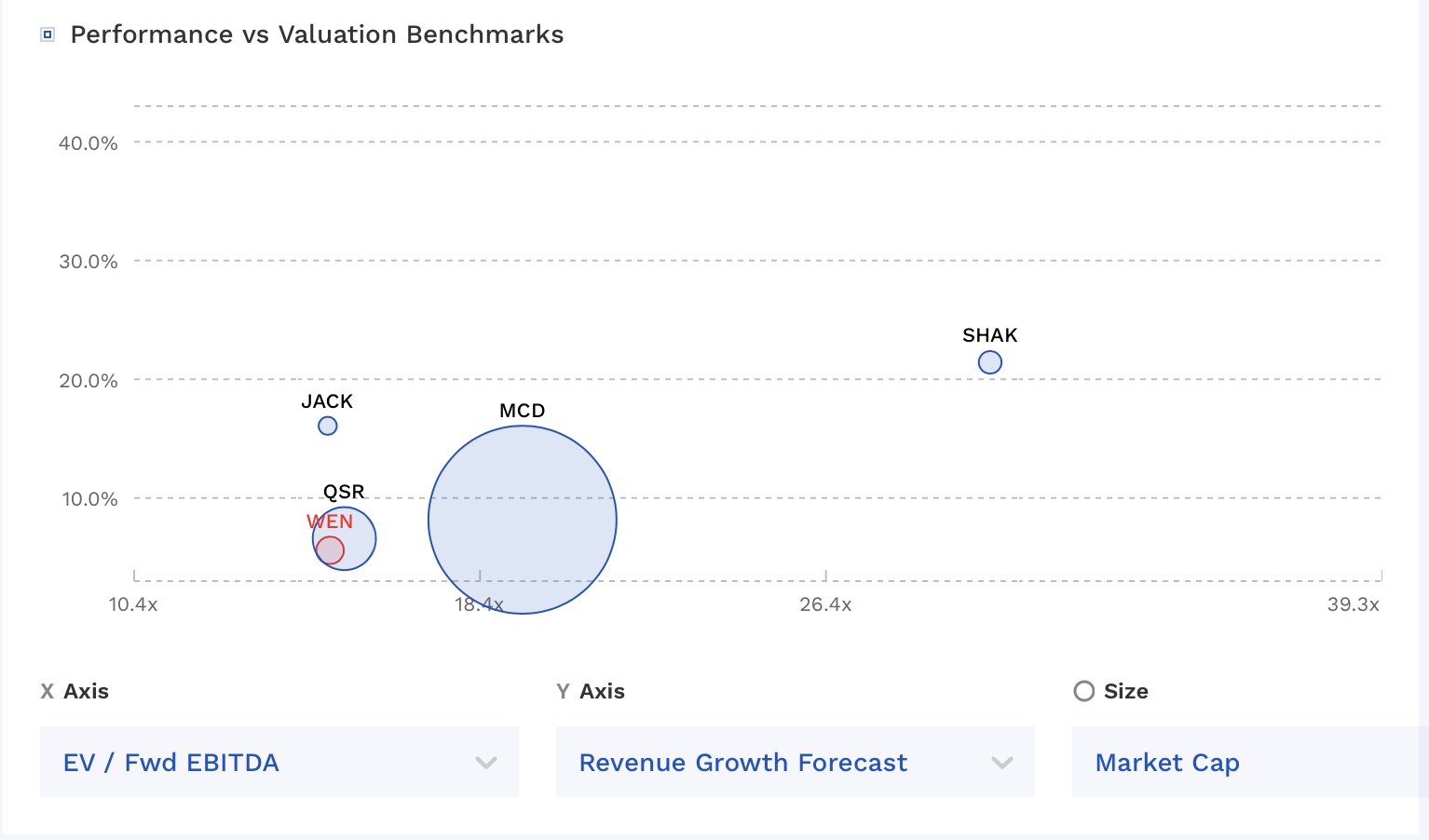

WEN trades in line with most of its burger joint peers, but below leader MCD and the fast-growing SHAK.

{kind=link}

Conclusion

The whole QSR space seems overvalued in my view, and WEN is no exception. The industry has clearly been benefiting from inflation and the ability to raise prices, but that is not going to last forever. The question is where will valuations settle in once this inflation cycle and price increase cycle cools down.

WEN does have some growth opportunities as it expands internationally and it could have more room to run with breakfast and late night. Meanwhile, the stock has a nice 4.6% yield. As such, I'm going to place a "Hold" rating on the stock, and would prefer to be a buy on a dip in the $16-17 range.

For further details see:

Wendy's: Try Its Pub Burger, But Hold The Stock