WDC - Western Digital: Better Pricing And AI-Led Storage Growth Prospects

2023-09-05 11:49:45 ET

Summary

- Western Digital's stock price received a boost after Morgan Stanley maintained their price target of $52 based on better pricing.

- Analysts also warn of hyperscalers spending money on Nvidia's GPUs at the expense of the non-AI data center market.

- Therefore, I value the company based on the above two diverging conditions.

- Since AI workloads have to be trained on immense amounts of data, the company should sell more hard drives, but, uncertainties in the Chinese market persist.

- Based on opportunities and risks, this thesis has a target of $51.

Western Digital Corporation ( WDC ) stock popped by around $2.5 on August 24 after analysts at Morgan Stanley ( MS ) maintained their price target of $52 . This is about 6 dollars above the current stock price as charted below.

The reason for the investment bank reiterating its overweight rating is mainly based on the secular demand for NAND (flash memory) and improved pricing, but analysts at Citigroup ( C ) warn about risks posed to the non-AI data center market, as investors are diverting funds to Nvidia ( NVDA ) which manufactures GPU chips, the key to building the infrastructure for Gen (Generative) AI algorithms.

These are two diverging views, and I will assess both arguments when valuing the stock, with my objective being also to focus on how the company's storage can benefit from increasing data usage resulting from artificial intelligence becoming more mainstream.

First, I provide an overview of the finances and competition.

The Finances, Demand, and Supply

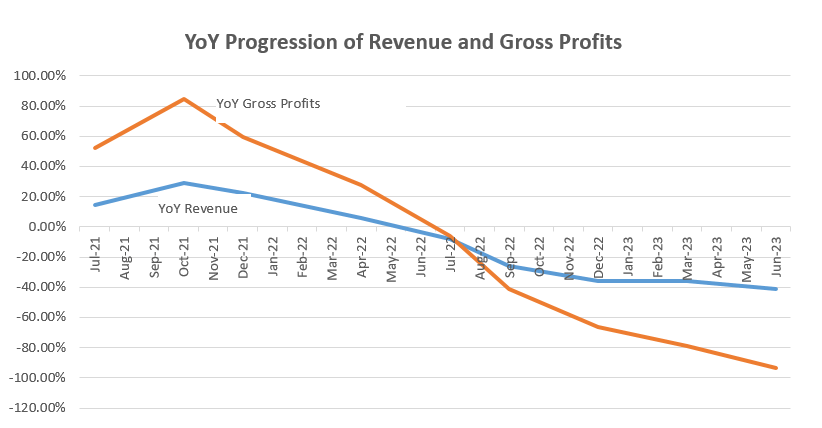

As seen by the quarterly revenue trend in the blue chart below, WDC's YoY growth has been decreasing from the October 2021 quarter when it was at a peak of 29%, with the deceleration persisting in the fourth quarter of 2023 (Q4) to -41% as shown in the blue chart below. However, more worrisome was gross profits falling at an even faster rate as shown in the orange chart.

Now, such topline and profitability regressions are synonymous with both reduction in demand due to weakness in the consumer and enterprise markets as well as dwindling pricing power because of the competition. For this purpose, the company sells storage products consisting of both NAND and HDD (hard drives) to the consumer, enterprise, and OEM markets to be used in everything from PCs and smartphones. Its HDDs are also used in servers by hyperscalers which are the big public cloud providers.

Charts built using Income Statement data from (seekingalpha.com)

{kind=link}

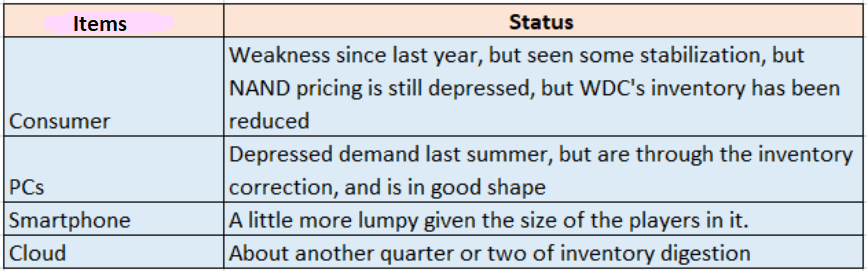

Now, according to David Goeckeler, the CEO talking during a conference on August 31 or exactly one month after the earnings call, the weakness in the consumer market seen in 2022 has somewhat stabilized with demand being more predictable, but NAND prices are still low as tabled below. As for PCs, demand is still weak but recovering as customers may have already consumed existing inventories. Exploring further, the smartphone market is still a difficult one while for the cloud, the management foresees further inventory digestion, for a further three to six months, but at the same time, based on the build-to-order model which basically provides for longer lead time, there are signs of an improvement.

Coming back to NAND pricing, some signs of bottoming have been seen. This could be the result of suppliers scaling back production in order to favor higher prices according to TrendForce , a fact which is confirmed by WDC's inventory decreasing during Q4. Looking deeper, this has been achieved through a realignment of the company's fab utilization and could result in fewer supplies reaching the markets and resulting in higher prices, which could be as early as in the third quarter which lasts from July to September.

Key data from the Deutsche Bank 2023 Technology Conference (seekingalpha.com)

{kind=link}

This also turns out to be WDC's first quarter of 2024 (Q1) whose results could be favorably impacted. Results are expected to be released on November 9, but, in addition, there could also be AI-led benefits.

AI-Led Storage Prospects and Geographical Footprint

In this respect, a report by Data Center Frontier states that there is currently a squeeze on data center capacity (for both space and power) in North America. Now, this shortage is due mostly to hyperscalers leasing collocation space and power to host AI workloads after they have purchased GPUs from Nvidia and HBMs (high bandwidth memory) from SK Hynix. Therefore, as the focus is mainly on building up AI infrastructures, there may be a temporary pause in the demand for non-AI data center markets as companies redeploy capital away from conventional CPUs (computing processing units). Looking closer , those most impacted would probably be Intel ( INTC ) and Advanced Micro Devices ( AMD ), not storage-producing WDC.

Well, the contrary could happen, as, after the initial phase when companies concentrate on optimizing their high-performance computing platforms using GPUs, they will hereafter need data, lots of them to feed to their large language models or LLMs for the learning process. This is where Generative AI is trained on data before it actually generates reports, and, the more the amount of data available, the better ChatGPT's precision.

All these data in turn require massive terabytes of storage space as corporations try to capitalize on and aggregate the knowledge lying idle in their databases.

In this respect, a study by Kearney estimates that Generative AI will contribute 6% to 9% to total memory sales by 2025, driven by complex natural language processing as AI models are trained not only in text but also in images and video. In this respect, WDC has started preparations to sample its ultra-high-capacity 28 TB hard drive making use of energy-assisted perpendicular magnetic recording (ePMR) technology specially designed for hyperscalers. The new HDD also helps it compete with Seagate ( STX ) which will release a 32 TB HDD with heat-assisted magnetic recording technology in 2024.

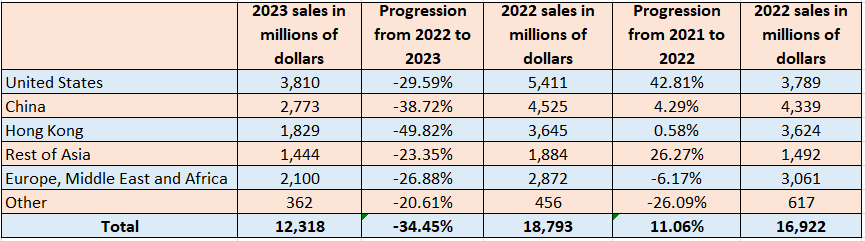

Furthermore, most of this AI-led growth should come from the U.S. at 40% of overall sales, followed by the Asia Pacific region. In this case, according to its SEC filings, the company derived 22% of its revenues from China for the fiscal year 2023 which ended in June. This represents a 38.7% regression from 2022 as shown in the table below.

Table built using SEC filing data from (seekingalpha.com)

{kind=link}

Therefore, while the U.S. still represented a substantial portion of 2023 sales at 31% (3810/12318 as per the above table), China's share is also important and the post-Covid uneven economic recovery in that country has contributed to Western Digital's woes. Now, the authorities in that country are trying to boost the economy through a number of ways, which means that there could be more demand for consumer goods, which can also reverberate positively across WDC's portfolio. In this respect, contrarily, to Nvidia's GPUs which cannot be exported to China following restrictions by the U.S. Department of Commerce, no such constraints apply to the storage company.

Therefore, with potentially improved NAND pricing and higher demand for its hard drives from cloud services providers, the company could beat the sales guidance for Q1 expected at $2.65 billion (mid-point). This figure represents a $22 million decline compared to the previous quarter or Q4 and a $1.086 billion decrease compared to the first quarter of 2023 respectively.

Valuation in View of Opportunities and Risks

Moreover, with a price-to-sales multiple of 1.19x, WDC is undervalued relative to the IT sector by over 56%, signifying that despite its recent upside, it can still potentially rise further. Now, just assuming an 11% upside as was the case in the second quarter results on January 26 when there was a revenue beat , the stock could climb to $51, which is just one dollar short of estimates .

Moreover, with the progress made in achieving greater visibility on demand/supply conditions, adjusting production accordingly in favor of prices, and reducing fixed costs (or underutilization charges), WDC could also see better margins and even produce an earnings beat thereby sending the shares even higher. In the same breath, progress has been made in reducing capex in the last two quarters, resulting in a positive free cash flow of $254.3 million (levered) in Q4 compared to negative figures in the three preceding quarters. Also, total debt has stayed at $7.35 billion to $7.37 billion during the last four quarters and should not increase as Capex is expected to decline significantly in fiscal 2024.

Looking at the competition, in addition to Seagate, WDC competes with major players like Toshiba ( TOSYY ), and Samsung, and a merger with Kioxia would have been beneficial to its market share in the highly competitive NAND space which generated slightly less than 50% of sales in FY-2023. However, getting the go-ahead from Chinese authorities may be problematic in the current geopolitical context, but, the two have a partnership for developing capital-efficient flash memory like the BICS8 for high-density applications.

This partnership with Kioxia also reminds us that in addition to market demand and competition, the company's financial performance is also influenced by technology trends which means risks of stock underperformance in case the deployment of an innovative product is delayed as a result of an hyperscaler shifting priorities or choosing to wait for a competitive product before making a final purchase decision. Therefore, this can have a delaying effect on revenues. In this respect, according to the CEO, "Gen AI may have some disruptions on the business in the near-term, as the compute infrastructure gets built out". However, in the same vein, he is very optimistic that it will be a catalyst for a profound increase in the rate of data creation.

Finally, adopting more of a cautious tone, the $51 price target is slightly lower than what analysts at Morgan Stanley estimate, but constitutes a fair value as it accounts both for price increases for NAND and uptake for HDDs by cloud providers, while also considering the persisting uncertainties in the Chinese economy. At the same time, it is also important to be realistic about AI-driven storage demand as it may simply take more time to materialize.

For further details see:

Western Digital: Better Pricing And AI-Led Storage Growth Prospects