WDC - Western Digital: Cyclical Value With Huge Merger Potential

2023-06-15 08:15:00 ET

Summary

- Western Digital has a 37% share in the hard drive market, and a possible merger of its Flash business with Kioxia could unlock shareholder value.

- The company's revenue has declined due to a cyclical pullback in industry demand, but it has beaten expectations for the top and bottom line.

- Activist firm Elliot management estimates following a merger or spin-off its equivalent share price could rise to over $100 per share, representing an ~150% upside.

Western Digital ( WDC ) is one of the big two suppliers of hard disk drives [HDDs] with approximately a 37% market share, along with Seagate, according to data from Statista . The company is facing a tough time as its revenue has declined substantially due to a cyclical pullback in industry demand. A positive is that despite this decline the company has beaten its expectations for the top and bottom line. In addition, there are talks of a merger with JV partner Kioxia and a spin-off of its hard drive business which could unlock greater shareholder value. In fact, activist investor Elliot Management believes Western Digital could reach over $100 per share within a 12 to 18-month period, following a merger or spin-off. Given Western Digital trades at ~$40 per share, this represents a strong upside potential of ~150%. In this post I'm going to break down the details of a potential merger, before diving into the financials and revealing my standalone valuation/forecasts for the stock; let's dive in.

Merger Potential

In my previous post on Western Digital, I discussed its business model which includes its basic hard-dive business as well as its flash (NAND) memory cards, under the SanDisk brand (acquired for $19 billion in 2016), which are used in mobile phones and professional-grade cameras.

On March 30th 2023, Western Digital announced the "world's fastest" NAND (flash memory) in a joint venture with Kioxia. The business is currently in the process of productizing this technology which offers huge potential for growth.

This product partnership could also expand much deeper as there are talks of a merger between the two businesses, according to Reuters.

This potential deal has been a long time coming after activist investment firm Elliot management took a stake in May 2022 and urged a spin-off of its flash business.

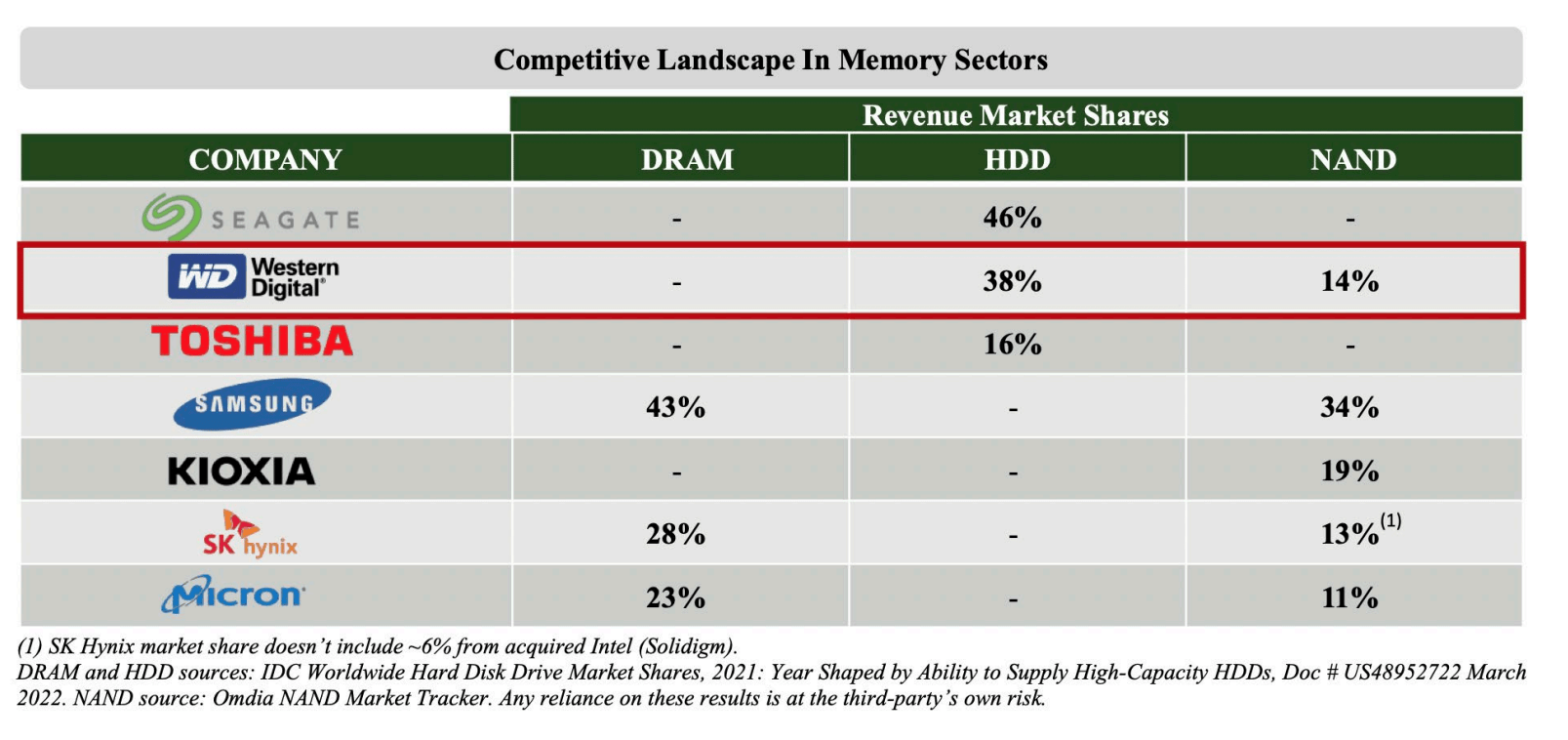

This makes sense as it would effectively result in a combination of the number two player in Flash (Kioxia, formerly Toshiba memory) (19-20% market share ) and the number three player (Western Digital, 14% share). Enabling them to compete effectively against the number one player Samsung (~34% market share).

Competitive Landscape (Omdia and Elliot Management data)

{kind=link}

From the table above you can clearly see a specialization in the storage industry. Western Digital's primary competitor Seagate ( STX ) has specialized in Hard Disk Drives [HDDs] and become the number one player with ~46% market share. Samsung is the number-one player in NAND and sold its hard drive business to Seagate in 2011. While Micron ( MU ) and SK Hynix have both specialized in the DRAM and NAND industries.

Elliot management even previously proposed an investment of over $1 billion in equity capital, into a pure flash business, which can be used to scale up modern manufacturing facilities. I believe this is a positive sign as the activist firm is showing "skin in the game".

The proposed merger is expected to consist of a new entity which is 43% owned by Kioxia and 37% owned by Western Digital. Of course, this is not certain yet as antitrust concerns could block the deal. However, if it did occur I believe greater shareholder value would be unlocked, I will discuss further details in my "Valuation and Forecasts" section.

Cyclical Financials

Western Digital reported $2.8 billion in revenue for the third quarter of the fiscal year 2023. This metric beat analyst forecasts by $115 million despite declining by an eye-watering 36% year over year.

A positive was this decline in revenue was mainly driven by a macro pullback in the storage market, which I believe is cyclical and thus short-term by nature. In my post on competitor Seagate ( STX ), I discovered a similar dynamic that confirmed my thesis.

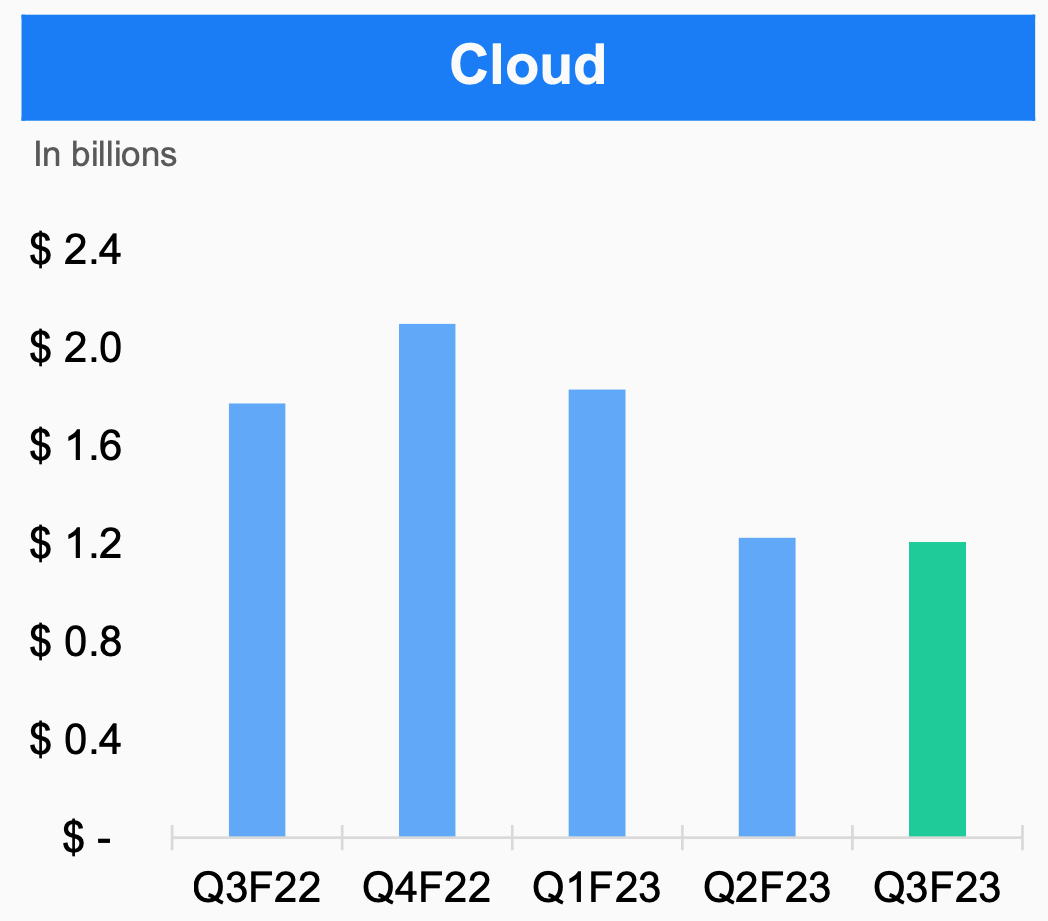

Breaking revenue down by application, its Cloud segment reported $1.2 billion in revenue, which was down 32% year over year. At a high level, this was impacted by cloud providers and enterprises scaling back capital expenditure. Again I believe is a short-term cyclical issue, as the trend towards digital transformation of businesses is still strong. In fact, the cloud computing industry is forecast to grow at a 20% compounded annual growth rate [CAGR], reaching an expected value of $2.4 billion by 2030.

Cloud Revenue (Q3,FY23 results)

{kind=link}

Its second largest application market is Client, which reported $1 billion in revenue down 44% year over year. This was driven by a cyclical pullback in the computing industry. A positive of the demand was aligned with management's expected results across PC, mobile, and gaming. Its Consumer application reported a similar trend with $600 million in revenue, down 29% year over year. This is really a reflection of the average consumer heading into a store to purchase a hard drive or flash drive. I personally believe this application (on the hard drive side) will continue to slow down, as more consumers utilize cloud storage. For example, if you think back 5 or 10 years ago you would have likely purchased an external hard drive to store a backup of your cell phone photos or other information. This was useful at the time, but these days, a simple upgrade on Apple cloud or Google cloud storage is much more seamless and scalable. This also mitigates the risk of losing an external hard drive, which may contain valuable information, or even Bitcoin, which has been stated in past news reports. Either way, my forecast for this application will be offset by continued growth in the cloud.

{kind=link}

Moving onto its product segments, hard disk drive revenue across all applications was $1.5 billion, down 30% year over year, but up 3% sequentially. This recent increase has been driven by stabilization in demand for exabyte shipments (enterprises/cloud), which rose by 50% sequentially and the average price per unit increased by 9% year over year.

{kind=link}

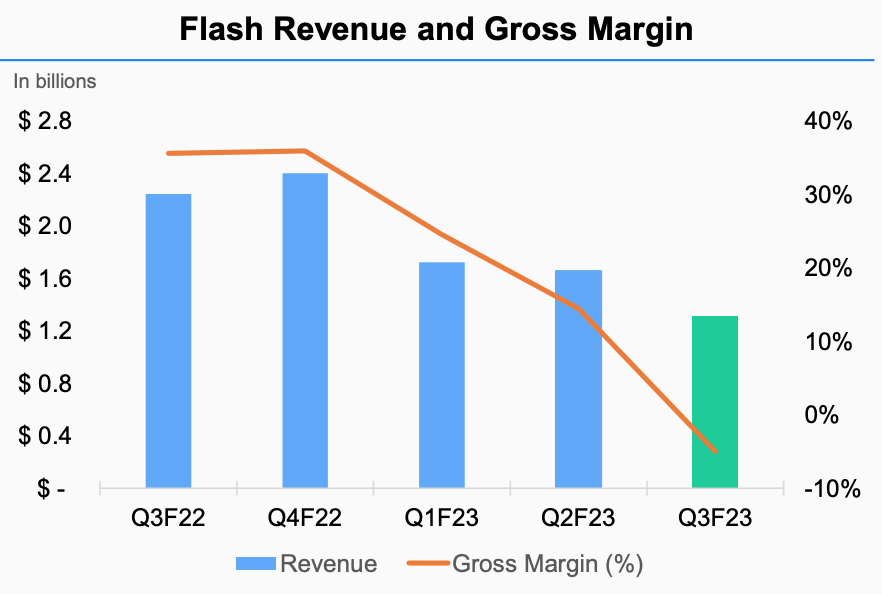

Its Flash revenue was $1.3 billion, which was down 42% year over year. A positive was the company has a diverse range of premium brands such as WD Black (gaming SSD) and its SanDisk memory cards. Given both the gaming and videography industry is forecast to continue to grow, I believe this segment has many tailwinds. In the Q3,FY23 earnings call, management cited "improved demand" in China, with gaming remaining strong.

{kind=link}

Margins and Balance Sheet

Western Digital's gross margin was squeezed by 21.1% year over year as the company absorbed $275 million in charges related to the underutilization of its manufacturing facilities and price adjustments on its inventory. A positive is as production is expected to ramp up (post-recession), the company should benefit from economies of scale which should boost margins. Also as supply/demand dynamics rebalance, prices should stabilize which will increase the value of any inventory.

Another positive is the business has reduced its overall operating expenses to $602 million in Q3,FY23, down $138 million year over year. This wasn't enough to mitigate the huge Non-GAAP loss of $304 million. But its earnings per share did surprisingly beat analyst forecasts by $0.06 (at $1.82 loss per share). The company also has $5.3 billion in total liquidity which consists of $2.2 billion in cash and cash equivalents. In addition, to an unused revolver capacity of $2.25 billion and a loan facility of $875 million. The company does have fairly high gross debt of $7.1 billion, but this could be spread across entities should a merger with Kioxia occur.

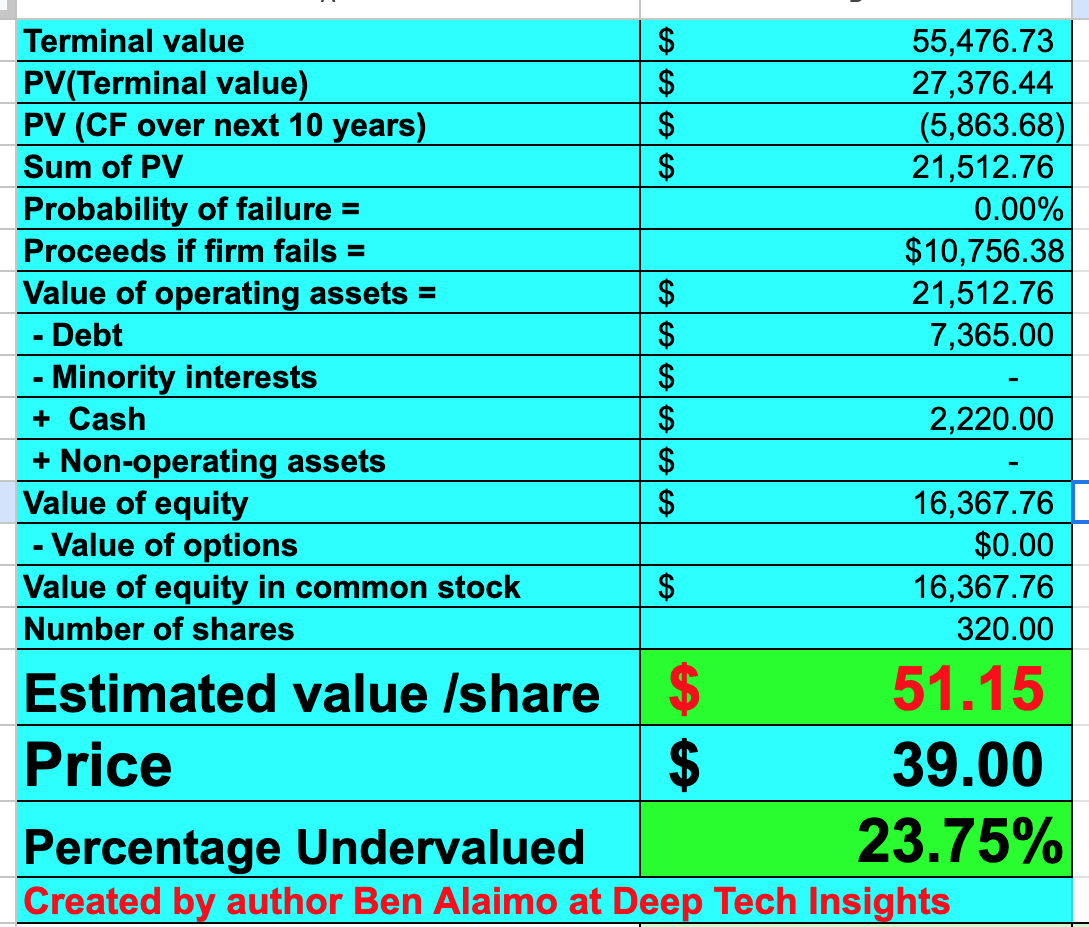

Valuation and Forecasts

In order to value Western Digital, I have plugged its latest financial data into my discounted cash flow model. I have forecast a negative 30% decline in revenue over the next year. This is based on an improvement over the 46.6% YoY decline management has guided for in Q4, FY24, and the 36% YoY decline reported in Q3, FY23. I expect demand to start to stabilize in the latter half of 2023, as inventory sells through and demand in the cloud begins to rebalance. Management has also forecast its Flash Bit shipments to "accelerate" in the first half of the fiscal year 2024, according to its earnings call.

In years 2 to 5, I have revised up my growth rate estimate to 18% per year. This is based upon a better understanding of the cyclical market dynamics and prior quarterly YoY growth rates which have ranged between 6% and 29% in 2021. I also believe the business will benefit from sales of its "world's fastest" NAND, once developed into a product. A merger with Kioxia would also be an added bonus with regards to growth, as a spin-out of its hard drive business could generate more value and the combined flash entity would have a formidable presence in the market.

Western Digital Stock valuation 1 (created by author Ben at Deep Tech Insights)

{kind=link}

Moving onto margins I have forecast a pre-tax operating margin of 17% by year 8. This may seem optimistic but this is just 1% higher than its prior margin generated in 2021. At a base level management has forecast between $580 million and $600 million in operating expenses per quarter throughout FY24, which is lower than the $603 million reported in Q3,FY24. Cash-based Capital expenditures are also ~35% lower than the FY22 levels. This forecast does not include any cost synergies which would likely occur from a merger with Kioxia.

Western Digital stock valuation 2 (created by author Ben at Deep Tech Insights)

{kind=link}

Given these factors I get a fair value of $51 per share, the stock is trading at ~$39 per share at the time of writing and thus is ~24% undervalued.

As an extra data point, Elliot management shared details of its 2023 relative-based valuation in a spin-off scenario. This assumes a $17.8 billion valuation for its hard drive business based on (1.9 times its CY2023 expected revenue). In addition to an $18.1 billion value for its flash business based upon (1.6x its CY23 expected revenue). For reference in 2017, an investment group with Bain Capital paid $18 billion for Toshiba Memory (now Kioxia) at a 1.9x LTM revenue. Therefore these numbers don't seem too crazy.

For Western Digital's whole business, this valuation is assuming $2 billion in free cash flow generated in 2023, up from the $1.446 billion reported in free cash flow in the prior year.

Given Western Digital currently has an enterprise value of ~$17.985 billion, this means its hard drive business alone would be worth 98.8% of its current valuation.

Western Digital also trades at a price-to-sales (P/S) ratio = 0.87, which is 2% cheaper than its 5-year average. Its forward price to sales ratio = 1, which is lower than its primary competitor Seagate ( STX ) which has a P/S ratio = 1.6.

Risks

Competition/cyclical pullback/antitrust

Western Digital's primary competitor is the market leader Seagate in hard disk drives. However, the company also faces competition from Samsung and even NAND memory providers such as Micron ( MU ). Trade issues with China, could also a ban on Western Digital products, as we have recently with Micron , following a review by the cybersecurity regulator. Then of course the cyclical pullback in the industry could take longer to recover than expected, dragging into the calendar year of 2024. With regards to the potential merger with Kioxia, antitrust regulators could block this from occurring. These are all risks that investors should be aware of, which could suppress the stock in the short term.

Final Thoughts

Western Digital is a tremendous business and a leading player in the hard drive market. If the company decides to merge its flash memory with Kioxia that could unlock greater value for the business through cost-saving synergies across its manufacturing setup. Elliot Management makes a strong case for the valuation benefit on a relative basis if such a merger occurs. However, even in my base valuation (assuming no merger), Western Digital looks to be undervalued intrinsically. Of course, this assumes the company can rebound following a recovery in global computing and the cloud.

For further details see:

Western Digital: Cyclical Value With Huge Merger Potential