WDC - Western Digital: Going South

2023-03-16 09:00:00 ET

Summary

- We continue to be sell-rated on Western Digital Corp.

- We expect WDC to continue to experience gross margin pressure in its flash business as we see weaker demand from PC client and smartphone end-markets.

- Additionally, we don’t expect its HDD business to recover in 1H23 as IT budgets tighten, causing softer cloud and enterprise spending, amid an uncertain macro environment.

- WDC stock is down 23% over the past year, creeping closer to its 52-week-low of $29.73.

- In spite of the cheap valuation, we recommend investors remain on the sidelines as we expect further possible downside to the stock ahead.

We remain sell-rated on Western Digital Corp ( WDC ). We expect WDC stock to see more downside as near-term macroeconomic headwinds persist in taking a bite of revenues. WDC’s 2Q23 earning results reported a revenue drop of 35.6% Y/Y at $3.11B and an EPS miss of $0.29. We believe WDC’s hands are tied on flash and HDD fronts due to weaker end-market demand in PC client and smartphone markets as well as softer cloud spending. We don’t see any way out for the company in the near term despite its efforts to reduce CapEx and shrink supply. The stock is down 23% over the past year, creeping closer to its 52-week-low of $29.73. We see an attractive exit point at current levels as we expect the stock to dip further toward 2H23.

TAM forecast reduction for 2023 vs. 2022

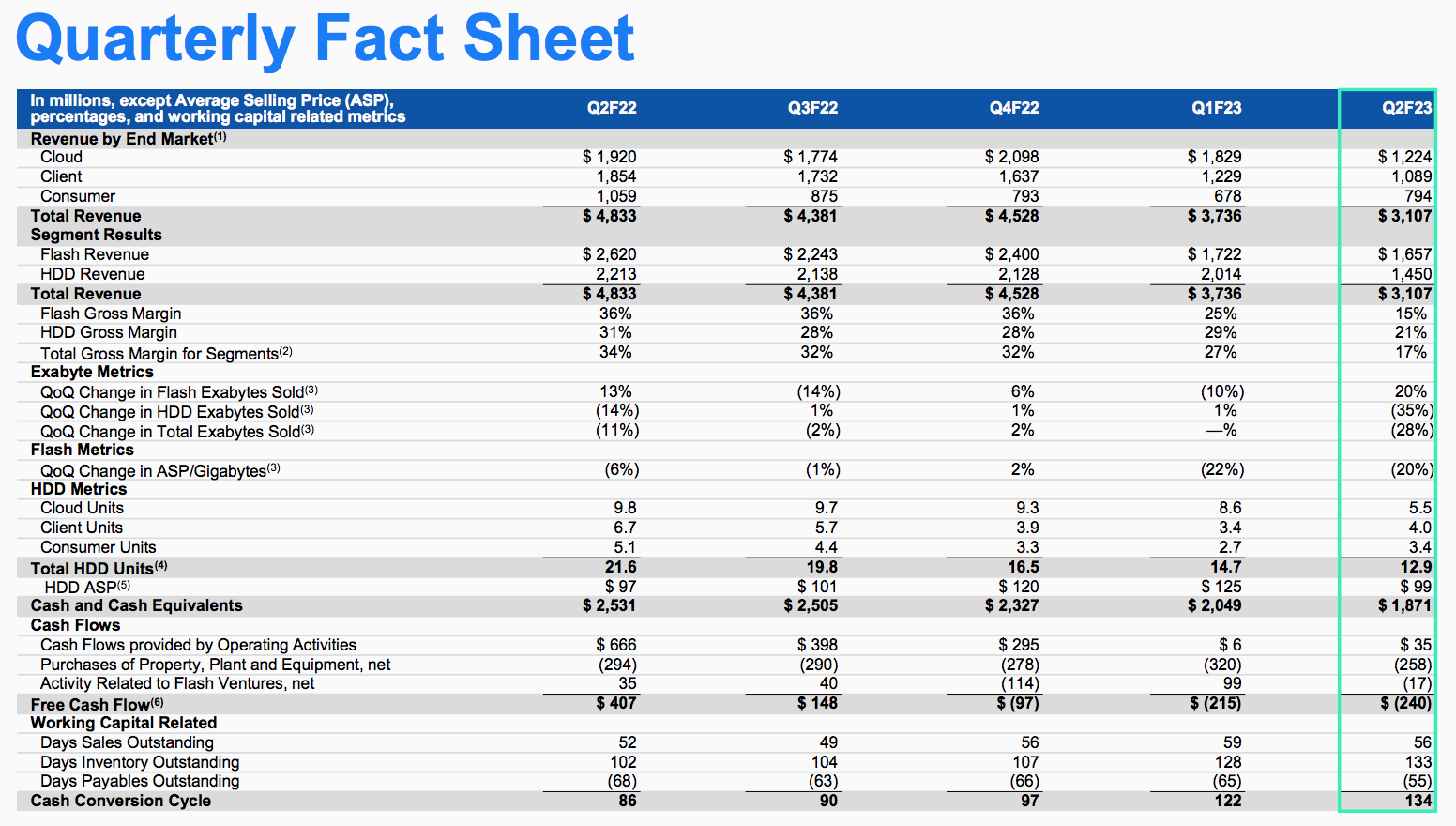

WDC stock dropped nearly 52% during 2022, and we don’t expect things to improve in 1H23 as TAM forecasts for 2023 reduce in comparison to 2022. WDC operates in two core storage businesses: NAND flash and HDDs. Our bearish sentiment on the stock is based on our expectation that demand will weaken in both segments in the near term. We previously wrote on WDC expecting the stock to face demand headwinds, and we’re now seeing the demand headwinds spill into 2023. In 2Q23, WDC experienced Y/Y and sequential declines in its flash and HDD revenues; flash revenue was $1,675M, down almost 37% Y/Y, and HDD revenue was $1,450M, down nearly 35%. The following graph outlines WDC’s quarterly results as of 2Q23.

{kind=link}

WDC’s March quarter guidance also fell short of Wall Street’s expectations, with revenue for 3Q23 expected to be within the $2.60B to $2.80B range. The following outlines our expectations for WDC’s flash and HDD businesses based on the reduced TAM forecast for 2023 vs. 2022.

1. Flash business

The NAND flash market mainly services PC client and smartphone end-markets, which crashed in the post-pandemic environment last year and have yet to recover. According to Gartner, the PC client market saw its largest decline ever, with PC shipments decreasing 28.5% Y/Y in 4Q22 due to weaker consumer spending. The smartphone market isn’t doing much better, with smartphone shipments suffering the largest-ever decline of 18.3% Y/Y in 4Q22, according to IDC. We expect muted consumer demand for PCs and smartphones to persist during the first half of the year, further denting WDC’s flash revenue. WDC’s flash gross margin is down from 36% in 2Q22 to 15% in 2Q23. Our bearish sentiment is also driven by TAM forecast reduction for the smartphone market from 1.21B in 2022 to 1.18B in 2023, accounting for a 2.5% decline. We expect OEM and retail channel inventory correction cycles to continue to adjust supply-demand dynamics, but don’t see consumer demand recovering before the end of the year.

2. HDD business

HDD revenue is also not a safe haven for the stock. We expect IT budgets to tighten amid market uncertainty harming cloud demand. The global cloud infrastructure services spend is expected to increase by 23% in 2023 compared to 29% in 2022, according to Canalys. WDC’s earnings reflect the weaker cloud demand, with a total of 5.5M units shipped in 2Q23 compared to 8.6M a quarter earlier and 9.8M a year ago. WDC’s ASP for HDD units is also down significantly to $99 from $125 a quarter earlier. We expect weaker HDD demand and lower ASP to cause HDD revenues to decline further next quarter.

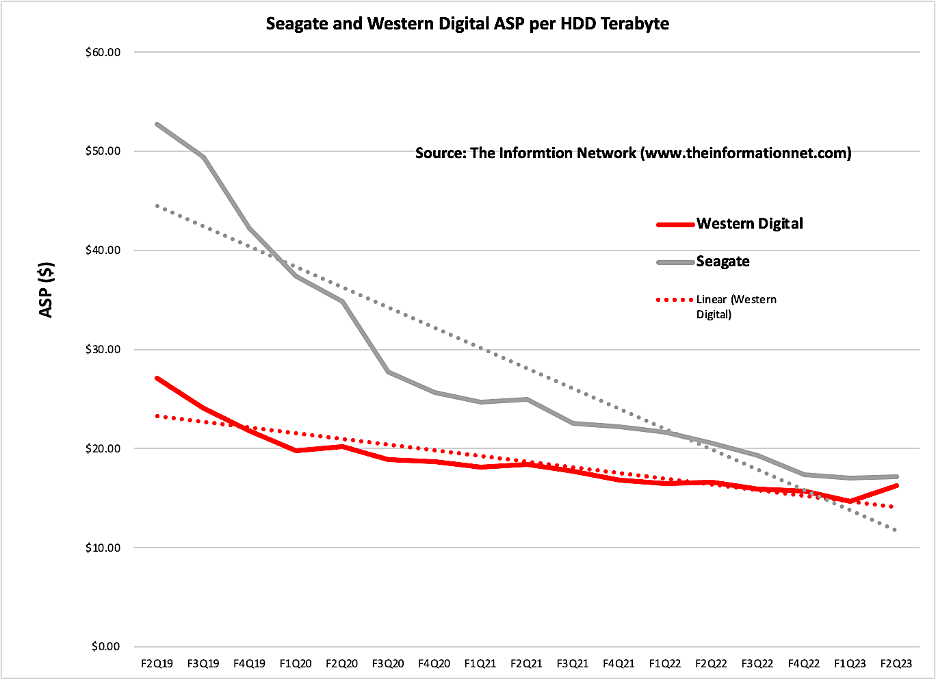

We expect WDC to underperform the peer group in the near term; we’re more constructive on Seagate ( STX ) in the storage space. We upgraded STX to a buy-in early February based on our belief that the company has hit its infliction point after 1Q23. STX is less exposed to flash market headwinds and derives the bulk of its revenues from HDDs. Hence, we believe STX is better positioned to recover in FY2023 than WDC, as we expect HDD demand to rebound faster than flash demand. We also expect STX’s growth to be driven by improved ASP and more customer adoption for higher-capacity HDDs. The following graph outlines STX’s ASP compared to WDC.

{kind=link}

Valuation

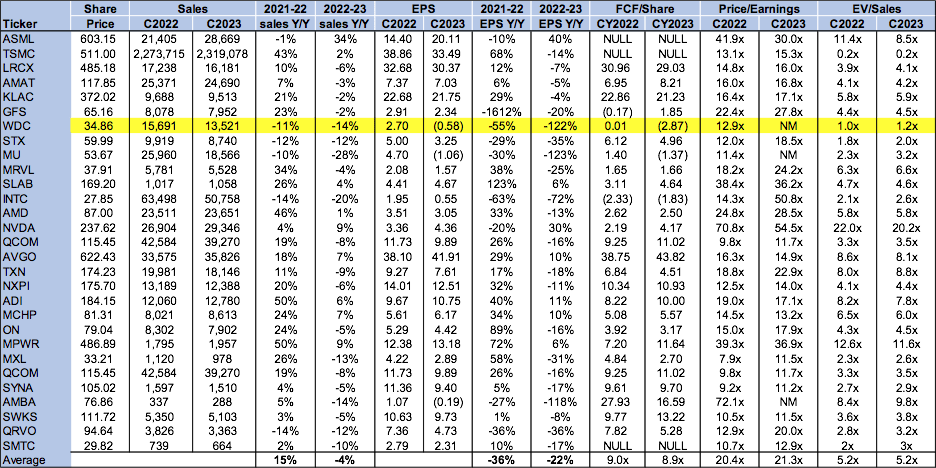

WDC is relatively cheap, but we recommend investors against buying the stock on weakness. The stock is trading at 1.2x EV/C2023 Sales versus the peer group average of 5.2x. We continue to see the stock price sliding in the near term and recommend investors sell their shares at current levels.

The following table outlines the company’s valuation against the semi-peer group.

{kind=link}

Word on Wall Street

Wall Street shares our bearish sentiment on the stock. Of the 28 analysts covering the stock, 13 are buy-rated, 14 are hold-rated, and the remaining are sell-rated. The stock is trading at $35 per share. The median sell-side price target is $48, while the mean is $47, with a potential 35-38% upside.

The following tables outline WDC’s sell-side ratings and price targets.

TechStockPros

What to do with the stock

We’re sell-rated on WDC. We expect weakness in the PC, smartphone, and data center markets to continue to weigh on WDC’s gross margins in the near term. We believe IT budgets will continue to shrink amid market uncertainty and see weaker consumer demand due to inflationary pressures. While WDC’s valuation is tempting, we see WDC’s stock dipping further in 1H23 and recommend investors sell the stock before further downside materializes.

For further details see:

Western Digital: Going South