WDC - Western Digital: Storage End Demand And Pricing Turn Positive

2023-11-01 09:00:00 ET

Summary

- We remain buy-rated on Western Digital stock.

- 1Q24 results and outlook for next quarter confirm our belief that storage end demand and pricing will improve sequentially in FY24.

- We expect top-line growth to reaccelerate next year as flash pricing recovers and cloud HDD storage spend recover.

- Additionally, we expect the stock to trade higher on investor confidence in the split of its HDD and Flash businesses into standalone companies, leveraging the end demand rebound in 2024.

- We continue to see a favorable risk-reward profile for the stock at the current level.

We remain buy-rated on Western Digital ( WDC ) stock. We're more optimistic about WDC as we think we're at the turning point for storage end demand and pricing to begin improving in FY24. This quarter, the company reported revenue of $2.75B, down 26.5% Y/Y and up 3% QoQ. Consistent with our expectations , top-line growth is accelerating after the storage and memory correction earlier this year; last quarter , WDC reported revenue down 41.1% Y/Y and 5% QoQ to $2.67B. We see an increasingly favorable risk-reward profile for the stock into 2024 due to two factors at play. The first is the recovery of flash pricing, and the second is the rebound in cloud HDD storage spend.

We think WDC is now better positioned to outperform next year. The stock is up ~16% over the past six months, outperforming the S&P 500 by around 15%. We see top-line growth in 2024, driven by better end demand and pricing in the storage industry after a downturn in 1H23 and the correction that followed, during which Micron ( MU ), SK Hynix, and Samsung as well as WDC cut production to move along the inventory correction cycle. We also expect the stock to continue to trade higher on investor confidence in management's announcement of its intentions to split its HDD and Flash businesses into standalone companies to maximize shareholders' return after Kioxia merger talks stalled. We recommend investors explore entry points at current levels as we think the macro headwinds have been priced in, and new catalysts exist in 2024.

The following graph outlines WDC stock performance against the S&P 500 and Seagate ( STX ) over the past six months.

YCharts

Upside in 2024 for end demand & pricing

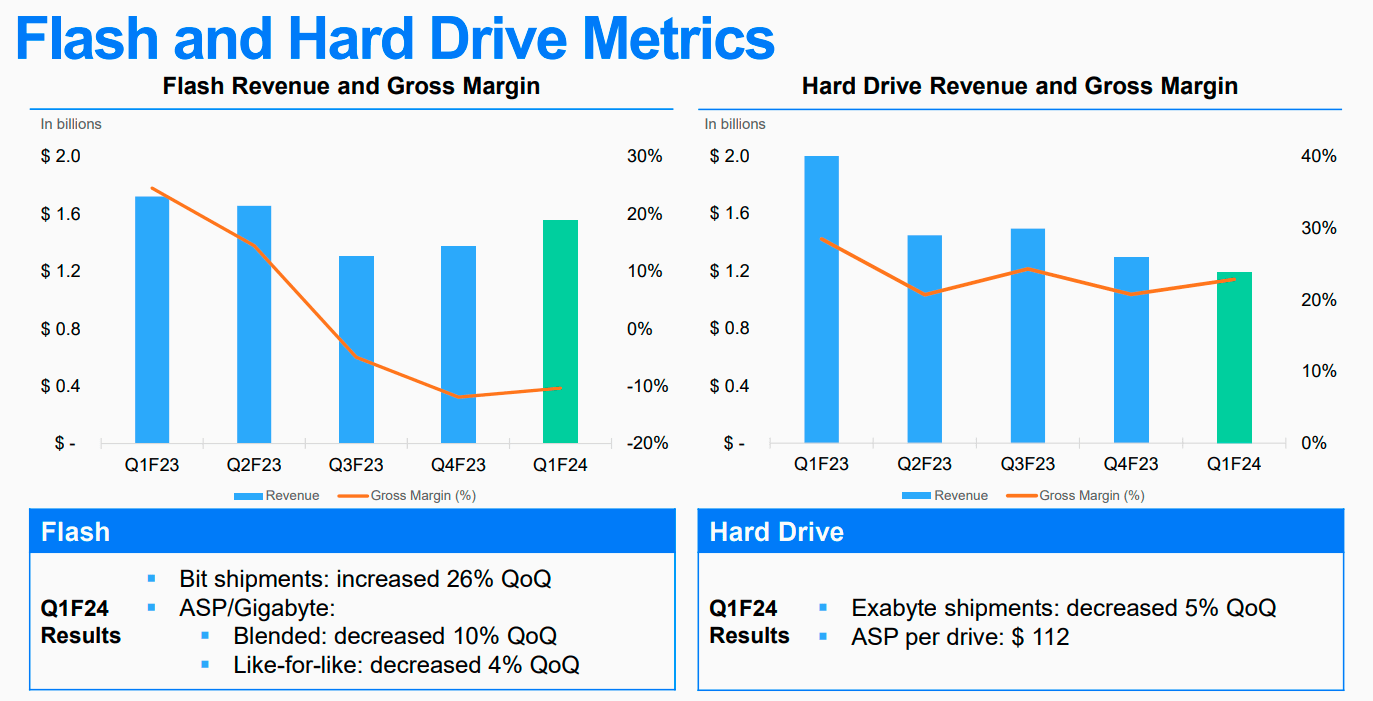

WDC is uniquely positioned due to its exposure to both HDD and Flash markets; our bullish sentiment is based on our belief that the company will experience positives on both fronts in 2024. We think 3Q23 results reflected the end of the inventory correction cycle and the start of the next leg of growth; HDD sales dropped 8% QoQ to $1.19B this quarter versus a 13% QoQ decline last quarter; we see HDD sales improving as cloud capex is revised up in 2024. Flash revenue grew 13% QoQ this quarter to $1.56B versus a 5% QoQ rebound in 4Q23, driven by an increase in bit shipment to both client and consumer end markets. We think Flash revenue growth was offset this quarter by the lower ASP and see this reversing in 2024 as pricing improves.

Additionally, we see a rebound occurring in the client and consumer-related end markets next year; we've already begun to see demand rebound this quarter, with client revenue up 11% QoQ and consumer-related revenue up 14%, respectively. We think WDC has a competitive advantage into next year due to its end-demand exposure and recommend investors take advantage of pullbacks in the near term to add to their position.

The following graph outlines WDC's Flash and HDD revenue in 1Q24.

{kind=link}

Valuation

WDC stock is undervalued, in our opinion. The stock is trading at 1.6x EV/C2023 Sales versus the peer group average of 5.0x. We think WDC is trading well below the peer group average due to the downturn in the storage and memory market this year. We see a more attractive risk-reward after weakness has been priced into the stock price, and we're on the horizon of an upward trend in the storage market.

The following chart outlines the WDC valuation against the peer group.

TSP

Word on Wall Street

Wall Street is bullish on the stock, as are we. Of the 24 analysts covering the stock, 14 are buy-rated, nine are hold-rated, and the remaining are sell-rated. The stock is currently priced at $42. The median sell-side price-target is $50 while the mean is $48 with a potential 14-20%.

The following charts outline Wall Street's sell-side ratings and price-targets.

TSP

What to do with the stock

We remain buy-rated on WDC. We believe we're at the turning point for the storage industry in terms of end demand and pricing after a rough 2023. We expect a PC rebound and expanded cloud spend in 2024. We see WDC growing top-line growth into the higher double-digit range towards 2HFY24. Management now expects next quarter's revenue to be between $2.85-$3.05B, in line with the consensus of $2.92B, representing a 4-11% QoQ growth. We see more upside ahead and recommend investors explore entry points at current levels.

For further details see:

Western Digital: Storage End Demand And Pricing Turn Positive