WDC - Western Digital Struggles With Short-Term Headwinds

2023-09-07 03:01:57 ET

Summary

- Western Digital Corporation is an under-covered data storage device manufacturer that benefits from long-term trends in data storage technology.

- Despite the strong long-term trends, the company has some short-term headwinds, including low demand in all of its three end markets.

- Combined with known unknowns such as the Kioxia merger, this is a name to stay away from. Therefore, WDC stock gets a "Hold" rating.

Investment Thesis

At a time when we need increasingly more data, we don't talk enough about data storage device manufacturers. One of the most under-covered ones is Western Digital Corporation ( WDC ).

The company has customers everywhere in the world. Whether they are manufacturing computers, smartphones, or data centers, companies need the data storage technology Western Digital produces. The business benefits from long-term trends such as an increasing number of intelligent devices, and big technology themes such as smart applications, artificial intelligence, 5G, and increasing usage of clouds.

However, I think there are too many known unknowns for the next five years of the company, making it very difficult to make a bet. Short-term headwinds are obvious as the demand falls, and it is going to take some time to recover. Therefore, I rate Western Digital a "Stay-Away" or "Hold".

Introduction

We see new advancements in technology nearly every month these days. An application like ChatGPT would not have been imaginable five years ago. Now we are talking about cloud computing, 5G, connected mobile devices, autonomous vehicles, smart home applications, and many more.

It's impossible to know where exactly we are going to be in our technological ventures. We do know one thing though: all these advancements use more and more data, and we don't have enough capacity to store them.

This is where data storage devices and their manufacturers come in. There are lots of big players out there such as Micron Technology ( MU ), Seagate Technology Holdings ( STX ), and Samsung Electronics ( SSNLF ).

There is another player that is not as much covered as these examples: Western Digital Corporation. It benefits from the same long-term drivers of revenue and is expected to see more demand as the data storage industry expands.

Company Description

Western Digital is a developer, manufacturer, and provider of data storage devices and solutions based on both Flash and Hard Disc Drive (HDD) technologies, which are the two operating segments.

Companies that build the internet infrastructure need these products to build data centers with higher capacities. These products also exist in most of your technological products including your computer and mobile phone.

These products are sold to three sets of customers.

The first one is the cloud customers. Storage devices sold to them are used for public or private cloud environments and end customers. As people need more data and the cloud emerges as the leading solution, data centers will require more and more storage devices. That is why Western Digital has big expectations from this end market.

The second set of customers are called clients. These are original equipment manufacturers (OEMs) and channel customers with a broad array of high-performance data products across personal computers, mobile gaming, automotive, virtual reality ((VR)) headsets, at-home entertainment, and industrial spaces.

The last one is called the consumer. As it can be understood from the name, these are mostly retailers that buy these storage devices and sell them directly to the end consumer.

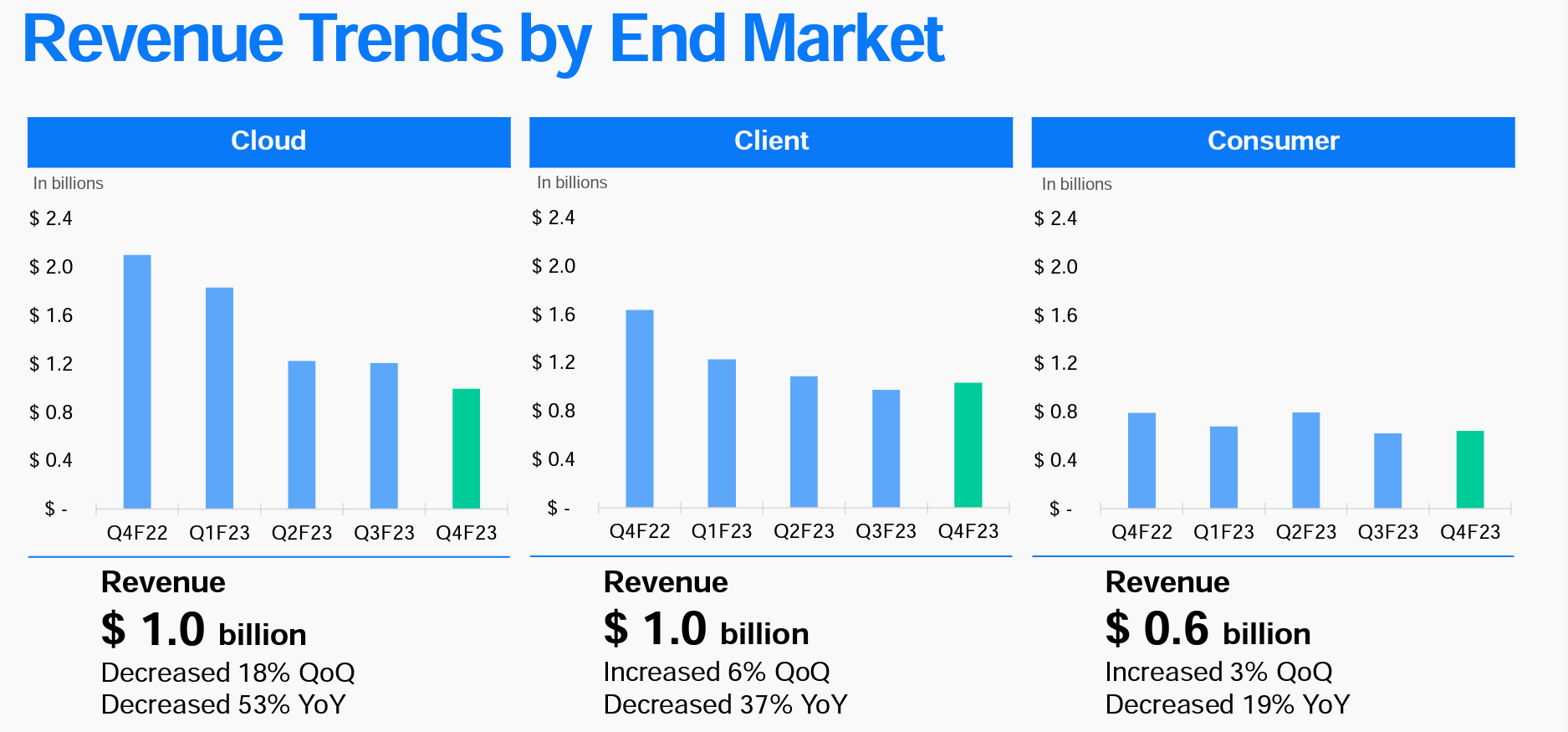

Based on the last earnings call of the company, Q4 2023, cloud, client, and consumer end markets accounted for 38%, 38%, and 24% of the company's total revenue, respectively.

{kind=link}

These clients are literally everywhere in the world. In 2023, the company had sales to the United States, China, Hong Kong, Europe, the Middle East, and Africa. The management showed this geographical breakdown at the investor day the company had in May 2022.

{kind=link}

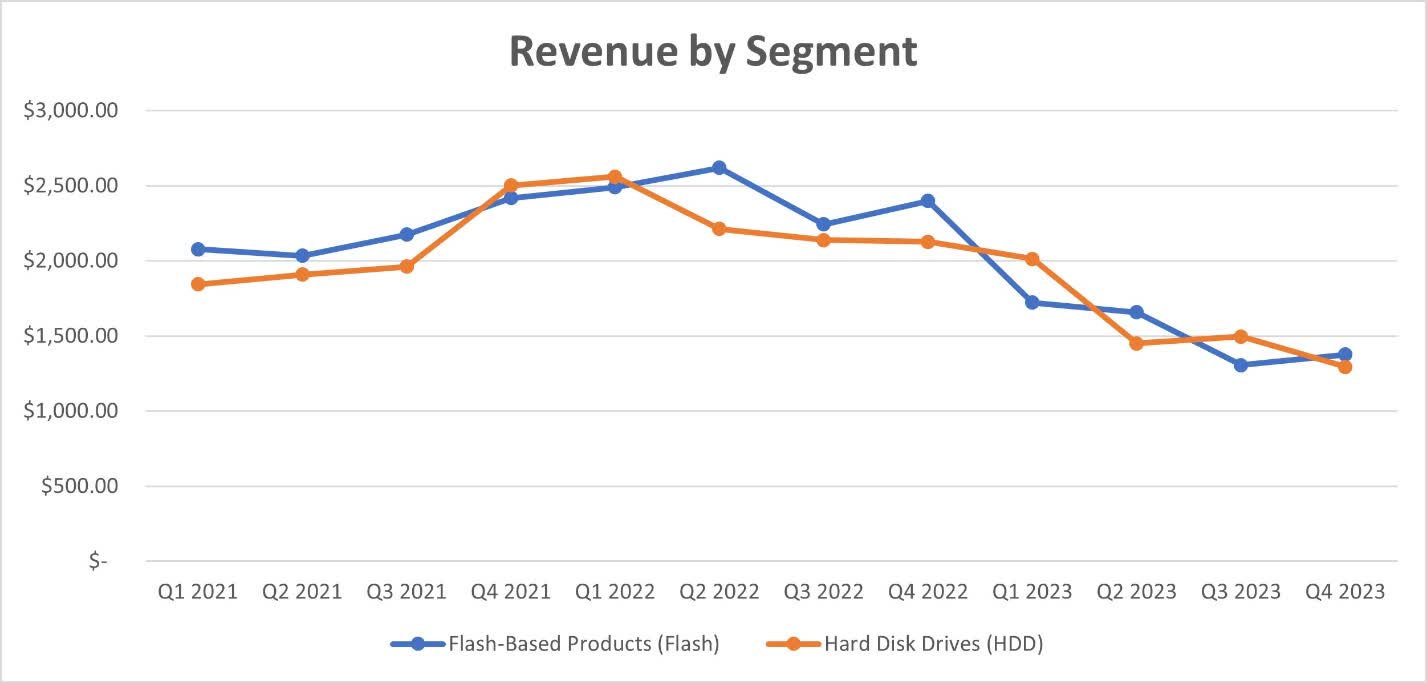

Since the company started to break down its revenue by its operating segments (flash and HDD), revenues from both have been moving mostly together, without the significant dominance of one.

{kind=link}

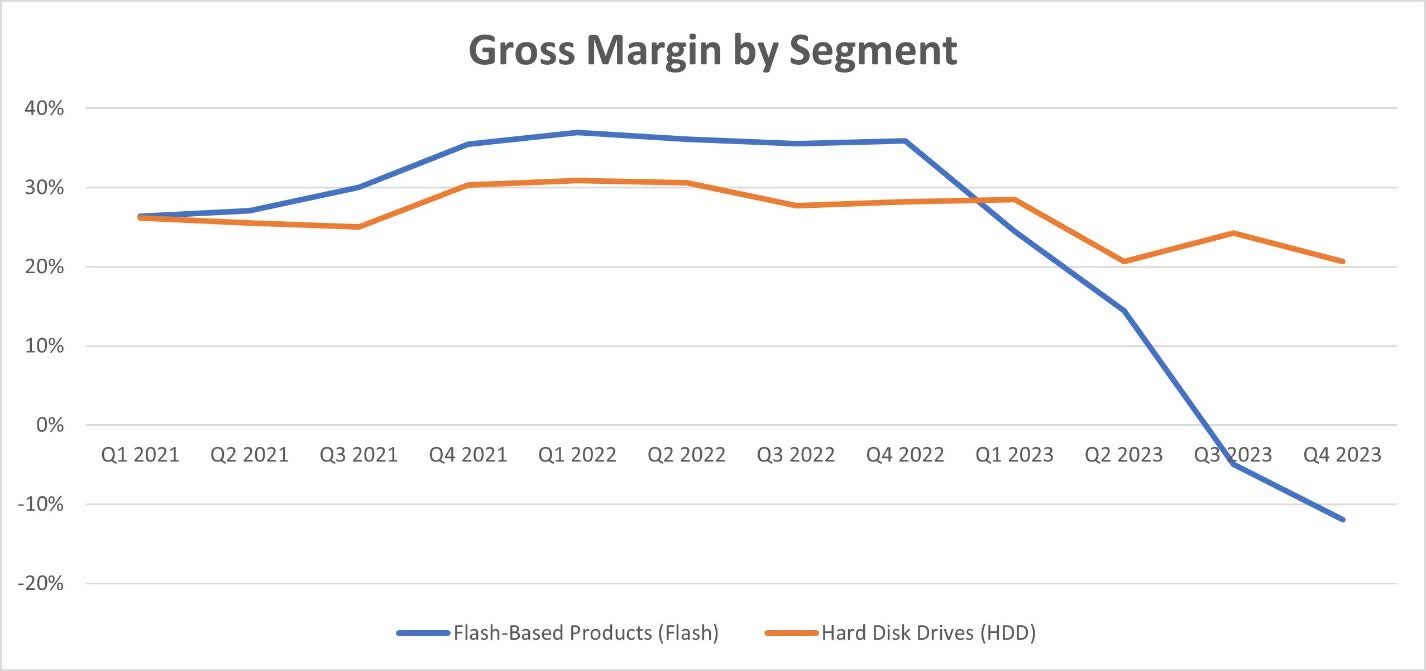

That is not the case for gross margins though… Flash has historically been a slightly more profitable business than HDD, before it started crashing in Q4 2022. We will get to the reasons later.

{kind=link}

Competitive Advantages

Western Digital has some strong competitive advantages and long-term drivers it benefits from in the long term.

First of all, technology brings us to a place where each movement creates a data point, which is later used to maximize your satisfaction and companies' topline. AI, cloud computing, and smart homes mean an ever-increasing number of intelligent devices in our lives. This will boost demand for data and storage in the long term.

Additionally, the U.S. has been trying to increase its infrastructure spending to make new roads, improve the supply chain, and bring services to underserved areas. Western Digital's products would enable these investments, meaning more demand for the company.

One of the biggest competitive advantages it has is that it is vertically integrated. It designs and manufactures both flash- and HDD-based technology. Its competitors usually focus on one of these. Micron and Samsung produce flash technology while Seagate produces HDD. This makes Western Digital a one-stop shop for both. The management says that they are the only company in the world with large-scale capabilities to do that, which doesn't seem wrong.

The Data Storage Giant Has Been Struggling Recently

There is no disagreement about how big this company is. It is one of the biggest players in both of its segments. It has a 37% market share in the HDD market , which makes it one of the two biggest companies in that space with Seagate.

But that also means that they have the biggest exposure to struggling end markets.

Demand for personal computers and mobile phones has been falling since the pandemic highs as a result of high inflation and aggressively raised interest rates. People do not want to invest in big luxury purchases when their earnings have not increased as much as costs and they face the threat of being laid-off.

We see above how the gross margin for the Flash segment started going south at the end of FY2022 and became negative in Q3 2023. As consumer spending remains weak, it could take a while for them to recover.

Additionally, the demand for the HDD segment is not where the management expected. The biggest set of customers for this segment is the cloud customers we discussed above. Now, even though the cloud is a big long-term trend, the company failed to achieve what it thought it would.

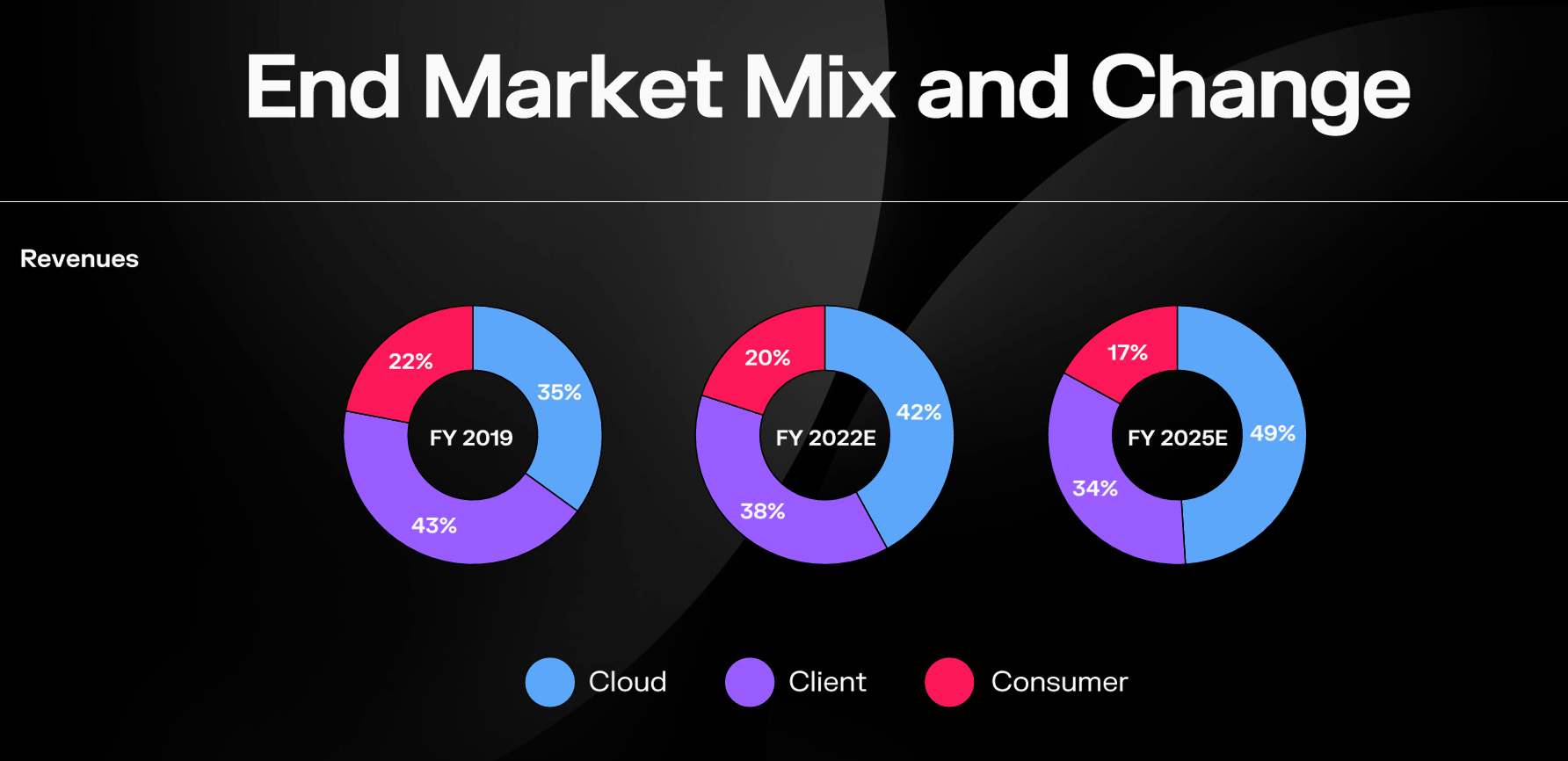

The management showed the below targets during their investor day in 2022. It clearly shows expectations to achieve 42% of revenue to come from cloud customers in 2022 and 49% in 2025. Cloud revenue was 38% of total revenue in 2023. That is going to be tough to realize those 2025 targets.

{kind=link}

The revenue for both of these operational segments has been coming down since Q2 2022. There is not much the management can do to boost the topline without hurting margins at the moment. This will depend on how serious of a recession risk companies and consumers foresee and how they arrange their budgets and purchases.

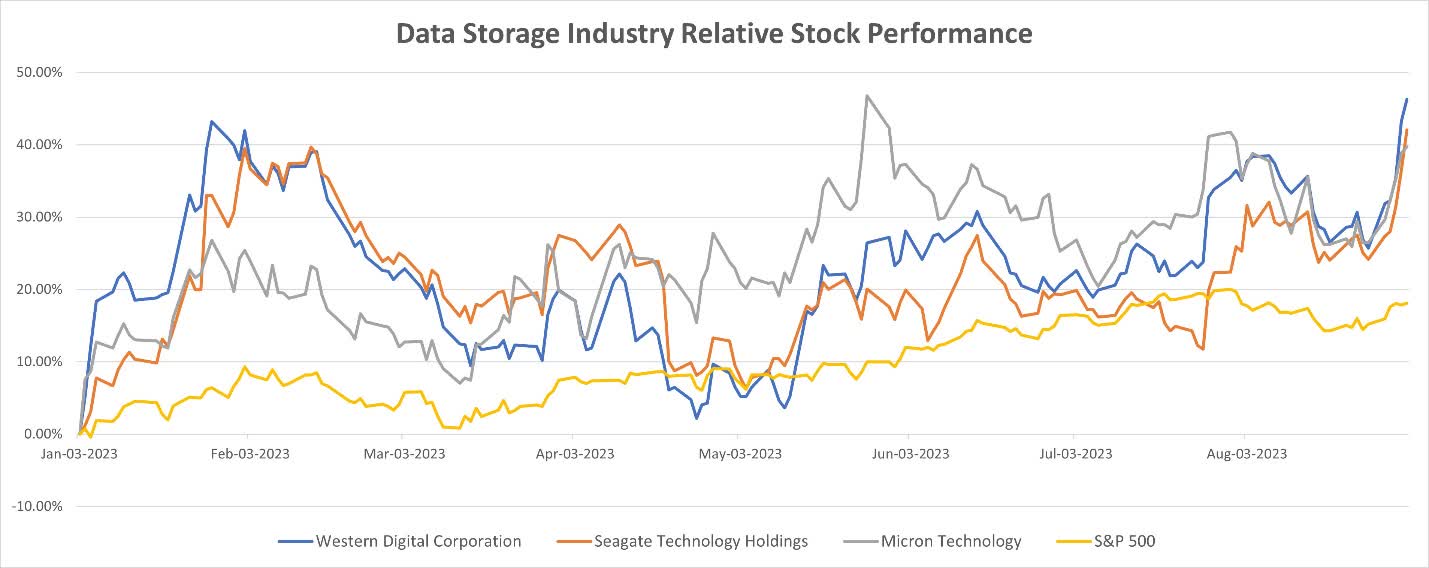

There is one positive in this story. Despite the deteriorating fundamentals, the industry has been doing quite well year-to-date. The stocks of the big three players in the United States, Western Digital, Seagate Technology, and Micron Technology, beat the market by quite a difference this year.

This makes me think all three were part of the AI rally we had this year, led by Nvidia (NVDA).

{kind=link}

Valuation

So far, Western Digital looks like a quality company with big short-term headwinds. Let's look at the valuation to see if there could be an opportunity.

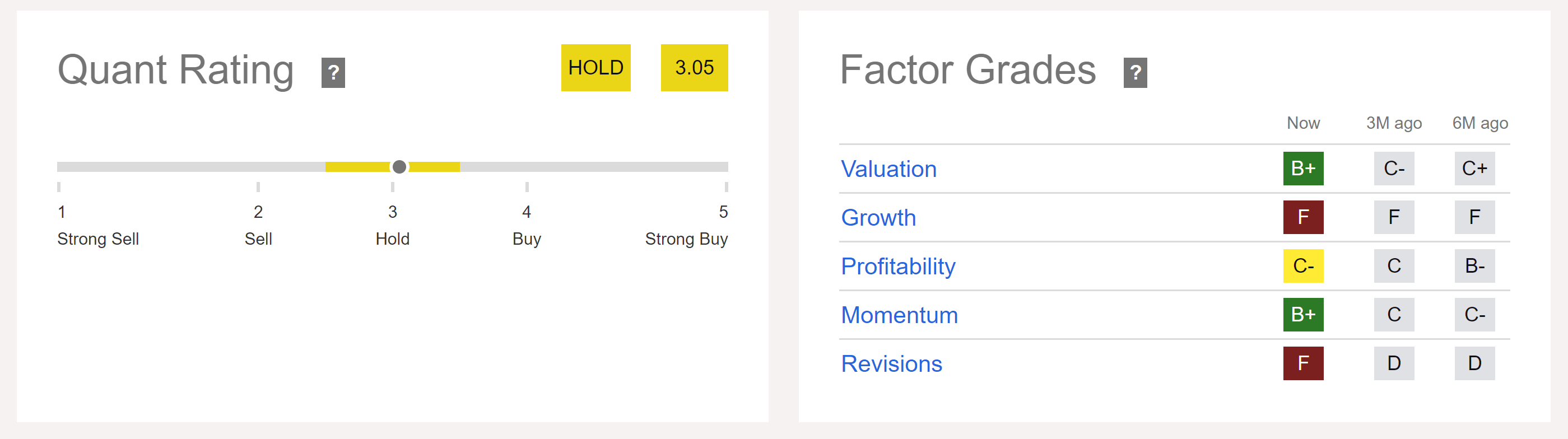

Seeking Alpha gives the company a valuation grade of B+. This rating was C- 3 months ago and C+ 6 months ago. Additionally, the company gets a quant rating of 3.05, which is in the middle of the Hold rating.

{kind=link}

We will use the DCF approach to value the company and understand if the stock trades at a premium, par, or discount.

It is easy for companies to boost earnings or invest heavily in asset growth if the management wants to do so. These numbers are volatile and provide less insight when looking into the future. The one metric that is structurally difficult to change is the return on assets ((ROA)).

You can see how cyclical the industry is below. The adjusted ROA has had a wide range between 7.5% and 29.2% since 2023. The fundamentals have been improving since the 2019 lows. However, the big drop in demand destroyed the bottom line, and the company became loss-making.

I expect a recovery to 2022 highs, but not suddenly. That makes more sense that it happens slowly in the next five years as the demand slowly recovers. That means adjusted ROA should recover from -7.2% in 2023 to around 15% in 2028.

{kind=link}

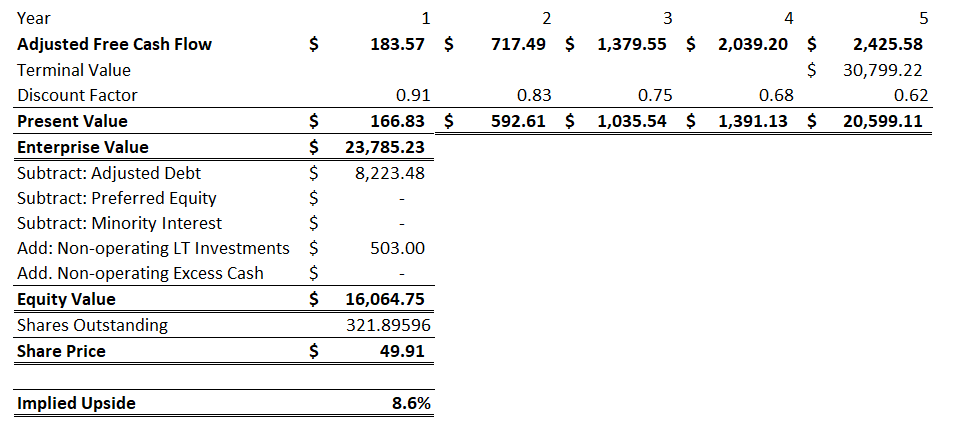

This ROA translates to an adjusted free cash flow of $184 million in 2024 and $2.43 billion in 2028 as demand recovers.

We will use a very conservative terminal growth rate of 2%, in line with long-term inflation targets. The cost of equity is calculated as 11.5% using a long-term risk-free rate of 2%, a market risk premium of 5.7%, and the stock's 5-year equity beta of 1.67. The cost of debt is taken at 7.1%, considering the yield-to-worst ((YTW)) the company's 2029 bonds have.

Using these numbers, we find an equity value of $16.065 billion, which means a target share price of $49.91. This is only an 8.6% upside over the current share price at the time of this article's writing.

{kind=link}

Risks

Investing in Western Digital stock comes with its risks.

The obvious one is the short-term headwinds. Consumer spending is weak and the sales to cloud customers are not as strong as the management imagined they would be. The management may have to wait until the macro environment is better to push sales. Otherwise, margins could compress further.

A known unknown is the company's relations with Kioxia, formerly known as Toshiba Memory Corporation. Earlier this year, two sides have been talking about making a deal that would unite the two technology storage providers. The aim was to create a giant in the industry. They already have a joint venture that produces chips. It is difficult to see how it will affect the shareholder value if the deal goes through. Therefore, I state it as a risk item.

Another topic that is not as discussed as the two above is the company's huge research and development (R&D) spending. Western Digital's long-term performance depends on innovation. They have to come up with new technology to protect their competitive advantage.

And the management knows this… 49% of cash outflow was done for R&D purposes in 2023. Regardless of the demand, the company will have to keep spending, which means margins can fall pretty quickly if the topline isn't there.

Conclusion

Western Digital is an interesting under-covered company in an industry that is historically seen as a growth-focused one. Its products are essential for the continuation of long-term trends and technological advancements. While there are still big growth prospects, things are not so attractive in the short term.

Demand from the consumer side has been falling, the cloud customer end market could not get as big as the management expected, and there are known unknowns about a possible merger with Kioxia, which makes things difficult to assess.

There are bigger, better, and safer opportunities in the market. Therefore, investors should stay away from Western Digital Corporation stock.

For further details see:

Western Digital Struggles With Short-Term Headwinds