WDC - Western Digital: The Unfolding M&A Narrative You Can't Afford To Ignore

2023-09-05 03:15:01 ET

Summary

- Western Digital shows strong indicators of potential M&A activity, including discussing separating its Flash and HDD business units.

- WDC's diverse portfolio and financial flexibility make it an attractive target for strategic M&A deals in the data storage industry.

- WDC's undervaluation, particularly in its EV/Sales ratio, highlights a significant room for upward revaluation.

- The company's talk of "strategic alternatives" and potential business unit separation signals imminent transformative actions.

- Analyst endorsements and a rumored merger with Kioxia validate WDC's M&A potential and could act as stock catalysts.

Companies often race against time to adapt, evolve, and capitalize on market trends in tech. In my view, there’s overwhelming evidence that Western Digital ( WDC ), a leading developer and manufacturer of data storage devices, is at such a pivotal juncture. With a diverse portfolio, strong financials, and a series of strategic moves, WDC is shaping into an intriguing M&A play in the future. This article aims to connect the dots to present a compelling case for WDC's M&A potential and why investors can profit from it.

The M&A indicators

When a company like WDC starts discussing " strategic alternatives ," it's not merely corporate jargon; it's a clear signal that something significant is on the horizon. Typically, this language often precedes transformative M&A transactions. In WDC's case, the company has explicitly mentioned the possibility of separating its Flash and HDD business units. This is a substantial move, considering each unit could stand as a strong, independent entity. The Flash unit, for instance, could attract interest from companies looking to bolster their cloud storage capabilities, while the HDD unit could be a lucrative target for firms focusing on more traditional, yet still essential, data storage solutions.

{kind=link}

In my view, moves like CAPEX reductions or amending loan agreements for additional financing capabilities could be preparatory steps for significant strategic M&A. This financial leeway is crucial, as it provides the liquidity needed to make cash offers or the financial stability to take on debt for larger purchases. Even for mergers, it's important as financing transactions can sometimes be tricky. Generally speaking, WDC can act swiftly when opportunities arise without being hamstrung by financial constraints.

Also, the current macroeconomic environment is fraught with challenges, including supply-demand imbalances and inflationary pressures. However, these challenges can also serve as catalysts for M&A deals. Companies often use M&A to gain immediate market advantages that would be time-consuming and costly to develop organically. For WDC, acquiring a smaller firm with innovative technology could provide a quick edge in the market. Alternatively, a merger with a complementary business could offer synergies that enhance profitability and market reach. In either case, M&A serves as a fast track to adapt to challenging market conditions, turning potential weaknesses into strengths.

{kind=link}

Concretely, WDC's extensive Flash and HDD technologies portfolio holds enormous potential in all these scenarios. First, it provides the company diverse revenue streams, making it resilient against market downturns in any technology. Second, it makes the company an attractive strategic M&A target or partner for various businesses. Companies looking to diversify their product offerings could see WDC as a one-stop shop for a broad range of data storage solutions. Third, this portfolio diversification also gives WDC a unique bargaining chip in M&A negotiations. It can choose to sell off non-core business units to focus on its primary technologies or use its diverse offerings as leverage in partnership discussions.

Why M&A is likely not accurately priced in

In financial markets, uncertainty is often synonymous with risk, and risk tends to depress stock prices. WDC has only hinted at "strategic alternatives" without explicitly confirming an impending M&A. This lack of clarity creates an "uncertainty discount" in the stock price. Investors, especially risk-averse investors, are naturally hesitant to fully price in WDC's M&A potential upside until there is a formal announcement. However, this also presents an opportunity for those willing to bet on the company's strategic direction. Once an M&A is confirmed, the stock is likely to adjust rapidly, rewarding those who invested during the period of uncertainty.

WDC's latest 10K report. Its underperformance could be an opportunity.

{kind=link}

Additionally, the current economic landscape is fraught with challenges, from inflation fears to concerns about a potential recession. These macroeconomic factors obscure the intrinsic value of WDC. Investors may be overly concerned with broader economic indicators and overlook the strategic moves WDC is making toward a significant M&A transaction.

Lastly, during their last earnings call , WDC’s management seemed focused on operational changes, including scaling back on CAPEX. I believe these actions are likely preparatory steps for an M&A transaction, but the market may interpret them as isolated, cost-cutting measures. This misinterpretation may also be contributing to WDC’s glaring valuation gap.

Analyst notes and their implications

Furthermore, analysts across the board find the M&A potential credible. For instance, Wedbush Securities recently elevated WDC to its "Best Ideas List," a move that should not be taken lightly. They see a "strong possibility" that WDC might separate its hard-disk drive and flash businesses, a strategy to unlock shareholder value. This external validation is significant for several reasons. First, it aligns perfectly with WDC's discussions about exploring "strategic alternatives," essentially serving as a third-party endorsement of the company's strategic direction. Second, the "Best Ideas List" inclusion could attract a new cohort of investors interested in M&A opportunities, thereby increasing the support for an M&A transaction and potentially acting as an upside catalyst for the stock.

Likewise, Morgan Stanley set a $52 price target for WDC. They acknowledged near-term pricing pressures but emphasized the robust demand for NAND storage technology. Given the cyclical and capital-intensive nature of the NAND flash market, this point is crucial because these factors make the robust demand for NAND storage even more significant. Strong demand signals that WDC's NAND business is likely undervalued.

{kind=link}

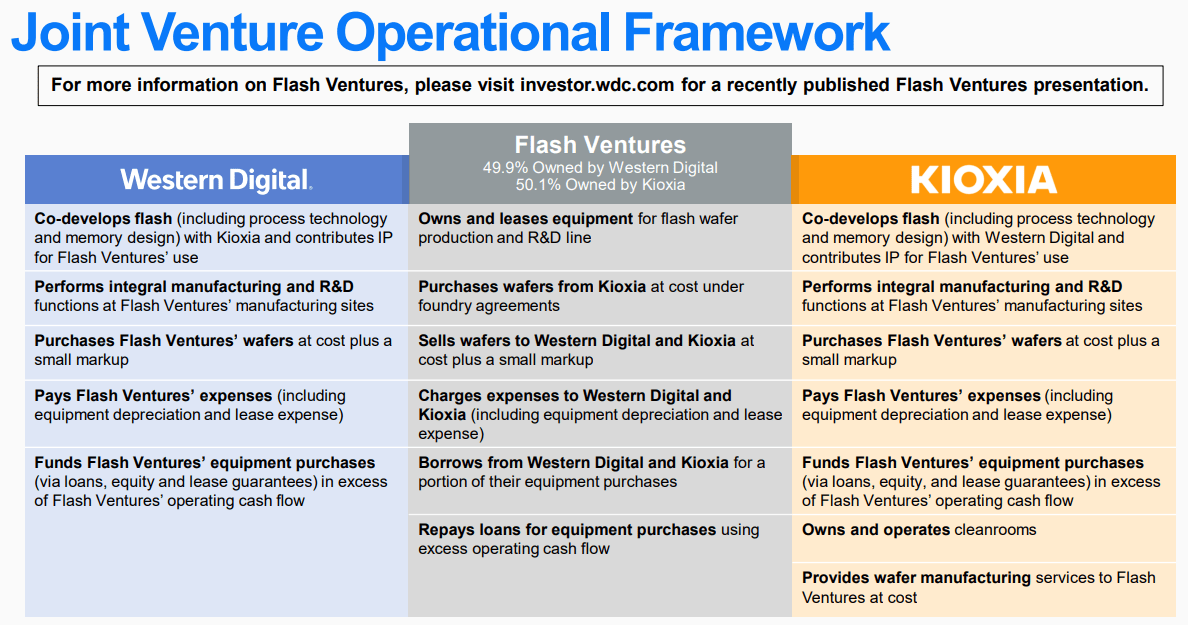

Building on this analysis, the rumored merger with Kioxia further underscores WDC's market potential. The combined entity would capture nearly one-third of the global NAND flash market. Moreover, these merger rumors between WDC and Kioxia highlight their strategic positioning and prospects. Allegedly, the companies contemplated a tax-free spinoff of WDC's flash business, which would merge with Kioxia. And even though it hasn’t materialized so far, this potential remains and sets a precedent for future M&A transactions. In particular, the tax-free nature of the deal underscores the potential value that can be unlocked via M&A.

In the Kioxia deal, WDC shareholders would have owned just over half of the merged entity. Together, their market share would be significant enough to surpass even industry leaders like Samsung. Furthermore, the deal would have broader implications, notably for Toshiba, which holds a substantial stake in Kioxia. A successful merger could positively influence Toshiba's valuation as well. Hence, the potential merger would have industry-wide ramifications.

Connecting the dots and closing thoughts

In the context of M&A, WDC's strategic actions serve as key indicators for future value creation. I believe WDC's recent financial focus on liquidity, CAPEX reductions, and amendments to loan agreements should be considered risk mitigation and capital structure optimization to facilitate accretive M&A transactions. Its diversified technology portfolio is both a revenue stabilizer and a value proposition for potential acquirers or partners, enhancing its attractiveness in a fragmented market. The endorsements from sell-side analysts validate the firm's intrinsic value and signal untapped upside in the context of strategic consolidation. The seemingly ongoing negotiations with Kioxia should be interpreted as a proof-of-concept for WDC's M&A potential, setting a precedent for future value-unlocking transactions. These strategic elements form a compelling investment thesis, underscoring WDC as a high-potential candidate in the M&A landscape.

Seeking Alpha plus Author's elaboration.

Consequently, WDC’s relative undervaluation is compelling, particularly when examining its EV/Sales ratio. The company's TTM EV/Sales stands at 1.70, significantly below the sector median of 2.89. If WDC were valued at this sector median, its Enterprise Value would surge from $20.94B to approximately $35.60B, representing a nearly 70% upside. However, after factoring in the company’s cash and debt, WDC’s equity market value would increase by almost 94%. Even though this isn’t necessarily a realistic price target, I’d argue that this valuation gap highlights the substantial room for upward revaluation.

Also, while WDC’s M&A prospects offer a robust investment thesis, downside risks warrant scrutiny for a nuanced fair price estimate. The absence of M&A could depress the stock, particularly if such expectations are baked into the current price. Pre-M&A financial maneuvers, such as CAPEX curtailment and loan restructuring, could constrain the firm's operational flexibility. Concurrently, macroeconomic headwinds like supply-demand imbalances and inflation pose additional financial risks. Despite these concerns, WDC's current valuation suggests a limited downside. After all, the stock trades at a modest 1.36 PB ratio and isn’t substantially levered, so taking a dip below (or even close to) a 1 PB ratio is highly improbable.

In total, this makes WDC an attractive investment, especially considering its M&A positioning. Thus, I think that for investors seeking long-term rewards amid short-term noise, WDC is strategically poised for transformative growth. And this is a narrative too compelling to ignore.

For further details see:

Western Digital: The Unfolding M&A Narrative You Can't Afford To Ignore