WEYS - Weyco Group Stock: 4% Dividend Yield May Not Be Good Enough

2023-11-14 09:21:39 ET

Summary

- The article discusses the Q3 earnings of Weyco Group, Inc.

- High levels of wholesale inventory alongside softer footwear industry trends are pressuring sales.

- Weyco Group benefits from a strong balance sheet, but we expect shares to remain volatile against a poor growth outlook.

Weyco Group Inc. (WEYS) reported its Q3 results marked by a decline in sales and weaker earnings compared to a record period in 2022. The company recognized for its portfolio of footwear brands including "BOGS," "Stacy Adams," and "Florsheim" has faced macro headwinds alongside the broader industry with management also citing high levels of wholesale inventory as limiting demand.

The good news is that the company remains profitable with strong cash flows, and a solid balance sheet considering zero financial debt. The stock yields 4% through a quarterly dividend that we believe remains well-supported.

At the same time, the challenge here is the poor growth outlook without a clear catalyst for a rebound. WEYS is currently trading at an 8-month low, and we expect shares to remain under pressure until there is some evidence of a stabilizing operating environment.

Weyco Group Q3 Earnings Recap

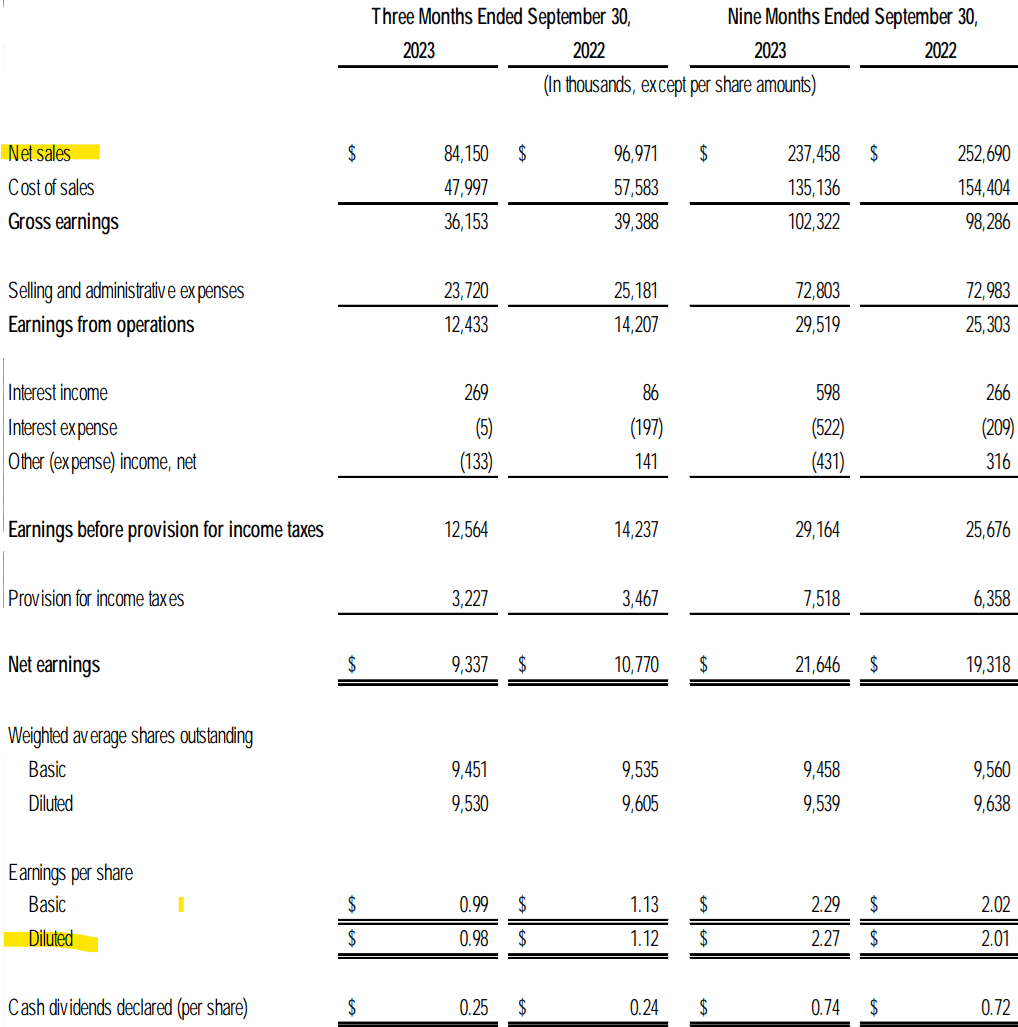

WEYS reported Q3 EPS of $0.98 , down from $1.12 in the period last year. Net sales of $84.2 million, was down by 13% compared to $97.0 million in Q3 2022.

Within that amount, the wholesale segment generating $70 million of revenue was weaker, down 15% y/y, balanced by a 6% increase from the smaller direct-to-consumer retail group.

The BOGS brand performed poorly, with sales at wholesale down -42% y/y. Management believes this was related to the style assortment as well as the timing of sales and unseasonably warm weather against a late-quarter rollout of winter fashions.

The dynamic of a shifting sales mix along with easing cost pressures helped the gross margin climb to 43% compared to 40.6% last year. Similarly, a decline in selling and administrative expenses at least helped limit the earnings decline.

Keep in mind that EPS of $2.27 through the first nine months is still up compared to $2.01 over the period last year, with supply chain constraints being the story in 2022.

{kind=link}

We mentioned the strong balance sheet. Weyco ended the quarter with $41 million in cash and cash equivalents, against zero debt, paying down an outstanding $31 million line of credit during the quarter.

The effort was facilitated by generating approximately $63 million in free cash flow over the past year. This level is supportive of the quarterly dividend of $0.25 per share, representing an annual payout of approximately $10 million. Separately, WEYS has also been active with share repurchases, buying back $1.3 million in stock in Q3.

While the company is not providing financial targets, management projected a sense of confidence during the earnings conference call despite recognizing some ongoing macro uncertainties.

There is also a sense that inventory levels at the company have normalized lower, around $80 million compared to $128 million at the end of 2022. This should provide some room to support margins over the near term. The plan is to refocus on the styles on offer targeting opportunities that can perform well.

What's Next For WEYS

Outside the dividend return, WEYS has been nearly flat from levels going back to late 2019, pre-pandemic. The fundamentals are "fine," but the company's current combination of a strong balance sheet against poor growth typically doesn't translate to a good investment thesis in our experience.

The backdrop here of declining sales this last quarter and concerns consumer spending will remain under pressure doesn't help with sentiment.

{kind=link}

Management made an effort to downplay the weakness of the BOGS brand, but it's fair to remain skeptical about whether that group will rebound going forward. Until there is a confirmation that growth is rebounding, and earnings have an upside, our base case is for shares to remain volatile.

As it relates to valuation, WEYS is trading at a 7.5x earnings multiple and 0.7x sales. While these figures represent a discount to the broader stock market, it's important to recognize that this segment of footwear stocks often trades with an even wider discount.

By this measure, stocks like Caleres Inc ( CAL ) or even Designer Brands Inc ( DBI ) closer to 6x multiple offer a bit better value. In many ways, the weakness of Weyco is its relatively concentrated brand portfolio highly dependent on BOGS compared to other players in the segment that have more diversification including through retail channels.

Final Thoughts

We just don't find much of a reason to expect shares of Weyco Group, Inc. to break out higher anytime soon. Officially, we rate the stock as a hold but lean bearish over the near term.

The risk is that results over the upcoming quarters continue to disappoint, opening the door for a deeper selloff. On the upside, we'll want to see some evidence that growth is rebounding while the operating margin and cash flow trends are the key monitoring points.

For further details see:

Weyco Group Stock: 4% Dividend Yield May Not Be Good Enough