MSFT - What Is Apple Really Worth? 15% Lower Is My Buy Zone

Summary

- Apple is still slightly overvalued vs. what I am willing to pay, namely $120 in price.

- I would prefer to purchase a stake with a positive inflation-adjusted, free cash flow yield in place. It remains a negative number today.

- A 15% to 20% price decline would also push the valuation vs. sales back toward long-term norms.

- I remain at a Hold rating, waiting patiently for a smarter entry point.

I was not very optimistic on the Apple Inc. ( AAPL ) price outlook in 2020-22, as the stock was selling at steep premiums to what I figured the underlying business was really worth. However, trading weakness over the final months of 2022 has pulled its valuation back into a range that makes more sense. I even wrote a story in November here , explaining why both Apple and Microsoft ( MSFT ) were moving into Hold ratings, a function of improving valuations on flattening growth trends.

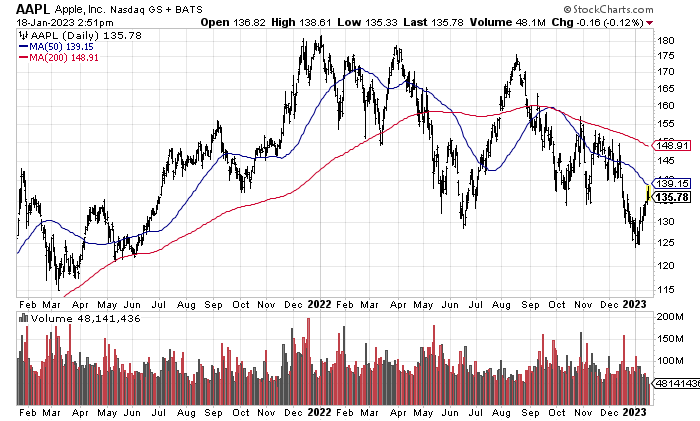

Several of my friends and a few readers have asked me in January, at what price should investors get serious about buying Apple? My view is $120 per share (for a round number), about 15% lower than this week's trading high and under the December 52-week low. Will such price become reality soon? I don't know for sure, but another wave of selling in the stock market generally as recession hits could create an opportunity.

StockCharts.com - Apple, 2 Years of Daily Price & Volume Changes

{kind=link}

Why $120 Is My Fair Value

For starters, analysts and Apple bulls rave about the strong cash position, free cash flow yield, dividend yield and stock repurchase story. I don't completely buy into the enthusiasm. It is a true statement that Apple used to be a cash machine vs. its equity worth five years ago, but such is no longer the case.

For example, price to tangible book value and total market capitalization to cash held on the balance sheet highlight very little underlying value using liquid assets as a measuring stick. While the company was backed by more than 11% cash in 2019 (at a 9:1 market value to cash ratio on the chart below), this number is down to 2.4% currently (hard asset backing ratios above 40:1).

YCharts - Apple, Price to Tangible Book Value, Market Worth vs. Cash Holdings, 10 Years

Free cash flow yield of nearly 5% sounds great, and it is the best Apple showing since 2019, but represents only an average number compared to leading computer manufacturing and online software peers. You can check out this idea in the presented graph. Putting Apple in a basket with Dell ( DELL ), HP Inc. ( HPQ ), Microsoft ( MSFT ), Alphabet/Google ( GOOG ) ( GOOGL ), Hewlett Packard Enterprise ( HPE ), International Business Machines ( IBM ), Canon ( CAJ ) and Sony ( SONY ), free cash flow yield is far from a bargain.

YCharts - Major Integrated Computer and Software Manufacturers, Trailing Free Cash Flow Yield, Past Year

What about basic cash flow valuations? When we review the apples-to-apples enterprise value to EBITDA calculation, Apple is nowhere near the cheap side of its peer group.

YCharts - Major Integrated Computer and Software Manufacturers, EV to Trailing EBITDA, Past Year

The dividend yield + net share buyback proposition of 4.8% annually isn't much to write home about either. Below is a graph of net payout yield vs. competitors, which is the ratio of dividends, plus share repurchases, minus share issuance over the past year divided by total market capitalization. Consequently, the total return of shareholder capital argument has limited weight today.

YCharts - Major Integrated Computer and Software Manufacturers, Net Shareholder Payout Yields, Past Year

Bottom Line

Absolutely, there are many characteristics to like about Apple. It has one of the largest global consumer bases, with incredible user loyalty. Let's not forget the winning corporate formula of designing product in America, manufacturing it in lower labor-cost Asia, and marketing items to rich consumers all over the world is an enviable setup to own as a shareholder. Net profit margins, after taxes, on sales are some of the highest of any high-volume sales business in the world.

YCharts - Major Integrated Computer and Software Manufacturers, Final Income Margins, Past Year

For sure, if a recession hits the U.S. and Apple can still hit its minimal growth forecast by Wall Street analysts this year and next, the "quality" of EPS results would be a nice positive to put your hat on (and capital into).

Seeking Alpha Table - Apple, Analyst Consensus Estimates for 2023-25, Made January 18th, 2023

Yet, with limited growth expected in 2023-25 from the operating business, I am looking for a "real" rate of return from earnings and free cash generation ABOVE the inflation rate. With CPI inflation still running at 6% or greater, owning a company delivering 5% is still failing to meet a college economics class, investment logic hurdle. I talked about this investment research angle and valuation math as an excuse to avoid Big Tech names in 2021-22 over and over again in my articles.

Below is a graph of this negative number for real yield from Apple, which is hugely different than the +10% number of 2015 (with monster company growth coming down the pike). In others, instead of losing wealth to inflation like 2021-22, buyers in 2015 covered the inflation rate while pocketing an extra 10% after taxes for the year (and years thereafter were even greater positive outcomes on rapid business growth)!

YCharts - Apple, Free Cash Flow Yield vs. CPI Inflation, 10 Years

I do expect a recession this year to cut the inflation rate. So, if EPS and free cash flow just stay stagnate in 2023, a crossover to positive real yield returns could happen with a minor drop in Apple's quote to $120 per share. I am guesstimating $120 by April will again provide a positive inflation-adjusted return on "trailing" free cash generation. This would still not be roaring buy territory. But, an argument in favor of slight business growth from the largest market value company in the world ($2.1 trillion today), churning out high margins, with only minor relative liabilities could at least be considered a buy again.

Lastly, the enterprise value to trailing sales average (over 15 years) close to 4x makes logical sense as a buy entry point. A 15% to 20% price decline would get us there.

YCharts - Apple, EV to Revenues, 15 Years

Final Thoughts

Remember, $120 for price may not be the low for this year if a deep recession is next. And, you have to weigh the odds of a China/Taiwan military clash ruining Apple's supply chain. Apple is far from a risk-free investment.

I would comment that I now rate sub-$100 prices, if they happen on a sizable stock market tank, as Strong Buy territory. Modeling total returns of 10% or greater over the next 3-5 years gets easier the lower price sinks in early 2023.

Could prices remain above $120 all year? Sure, I believe the company deserves some sort of premium, especially after inventing and marketing revolutionary personal computers and smart phones for mankind decades apart. Maybe the self-driving Apple EV car will be the next big thing in a couple of years.

That's why my official Apple rating continues to be a Hold. If you own shares and plan on keeping them for years or decades, trying to scalp 15% or 20% is not without risk (especially if you are required to pay capital gains taxes on your liquidation). Assuming price begins to move higher again, you will regret missing the boat selling in January 2023.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

What Is Apple Really Worth? 15% Lower Is My Buy Zone