MSFT - What Is VMware Worth If The Broadcom Deal Fails?

2023-05-02 10:00:00 ET

Summary

- Broadcom intends to acquire VMware for $142.5 per share in cash or 0.2520 AVGO shares.

- With the Microsoft/Activision Blizzard deal getting blocked, it's a relevant question to ask what would happen in this case.

- What should VMware be worth if the deal fails?

- The shares currently have a 12% discount to the deal offered by Broadcom.

It has been almost one year since Broadcom (AVGO) announced its intended Blockbuster acquisition of VMware (VMW) for $69 billion enterprise value ($61 billion for the equity and assuming $8 billion of VMware net debt). The stock right now trades at a 12% discount to the buyout offer. In light of the recent block from the UK for the Microsoft (MSFT), Activision Blizzard (ATVI) deal, it makes sense to entertain a scenario where the deal doesn't go through and what that would mean for both companies.

MSFT ATVI deal

The MSFT ATVI deal has been a fiercely fought battle over the last year with regulators worldwide. Now the UK has blocked the offer and another round of legal actions are ahead as Microsoft intends to fight this deal. If the agreement fails, ATVI will receive around $3 billion in termination fees from Microsoft. Although the deal has seen much more scrutiny than the AVGO VMW deal, it is still worth considering what would happen if it falls through. The market now assigns a less negligible risk to the deal breaking (12% discount for VMW versus 20% discount for ATVI). If it falls through, VMW will receive $1.5 billion in termination fees from AVGO.

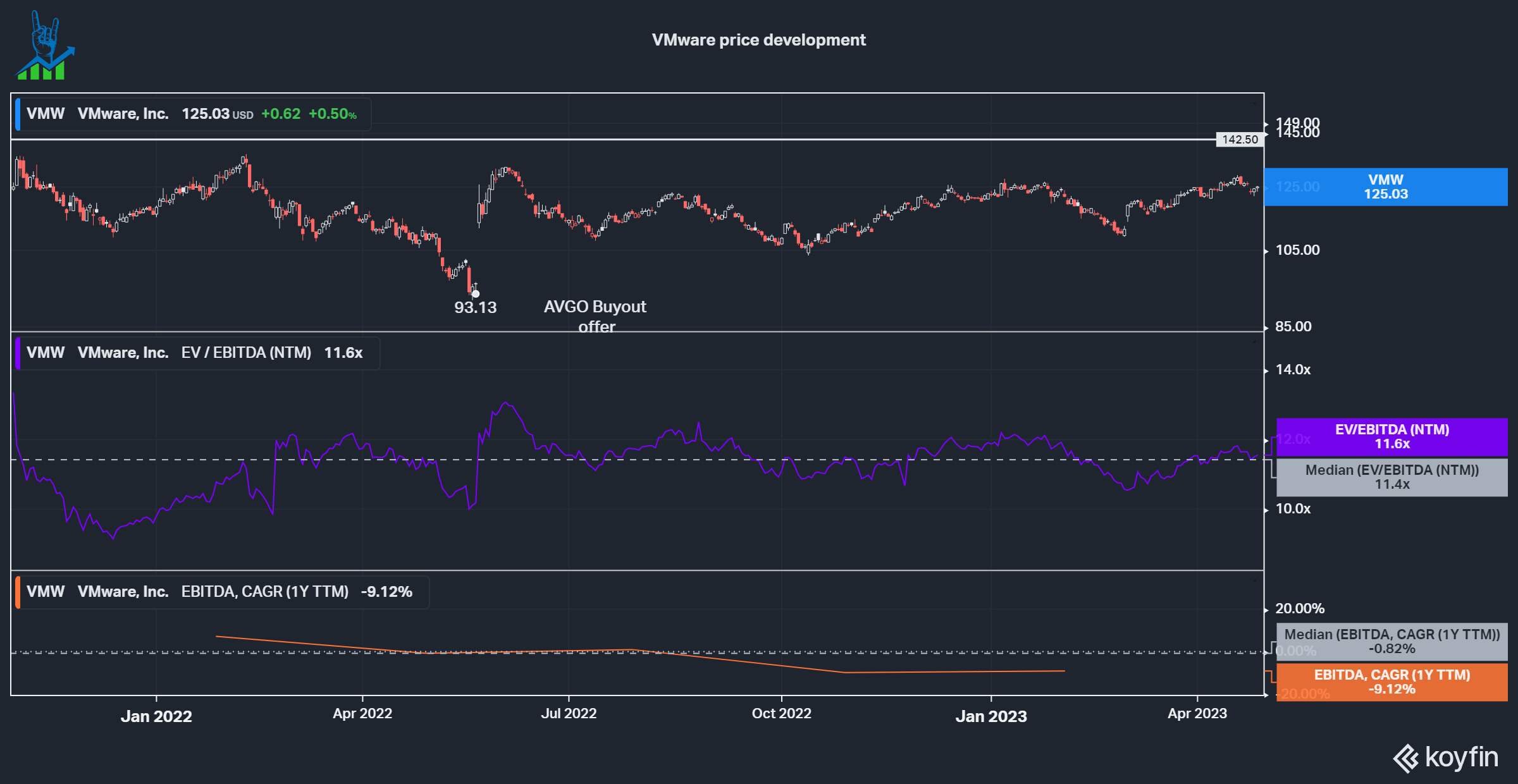

VMware before the deal

In the picture below, we can see the historical price, valuation and growth of VMware. The stock recently got spun out of Dell Technologies (DELL) in late 2021, so the acquisition of Broadcom comes very early in the public life of the company. We can see that Broadcom made its bid when the stock was trading at an all-time low of $93, offering a huge premium of over 40% for the stock ($142.5 per share). For shareholders of VMware, this is a lucrative offer and it is understandable why the deal got approved by shareholders of both companies.

{kind=link}

VMware's fundamentals

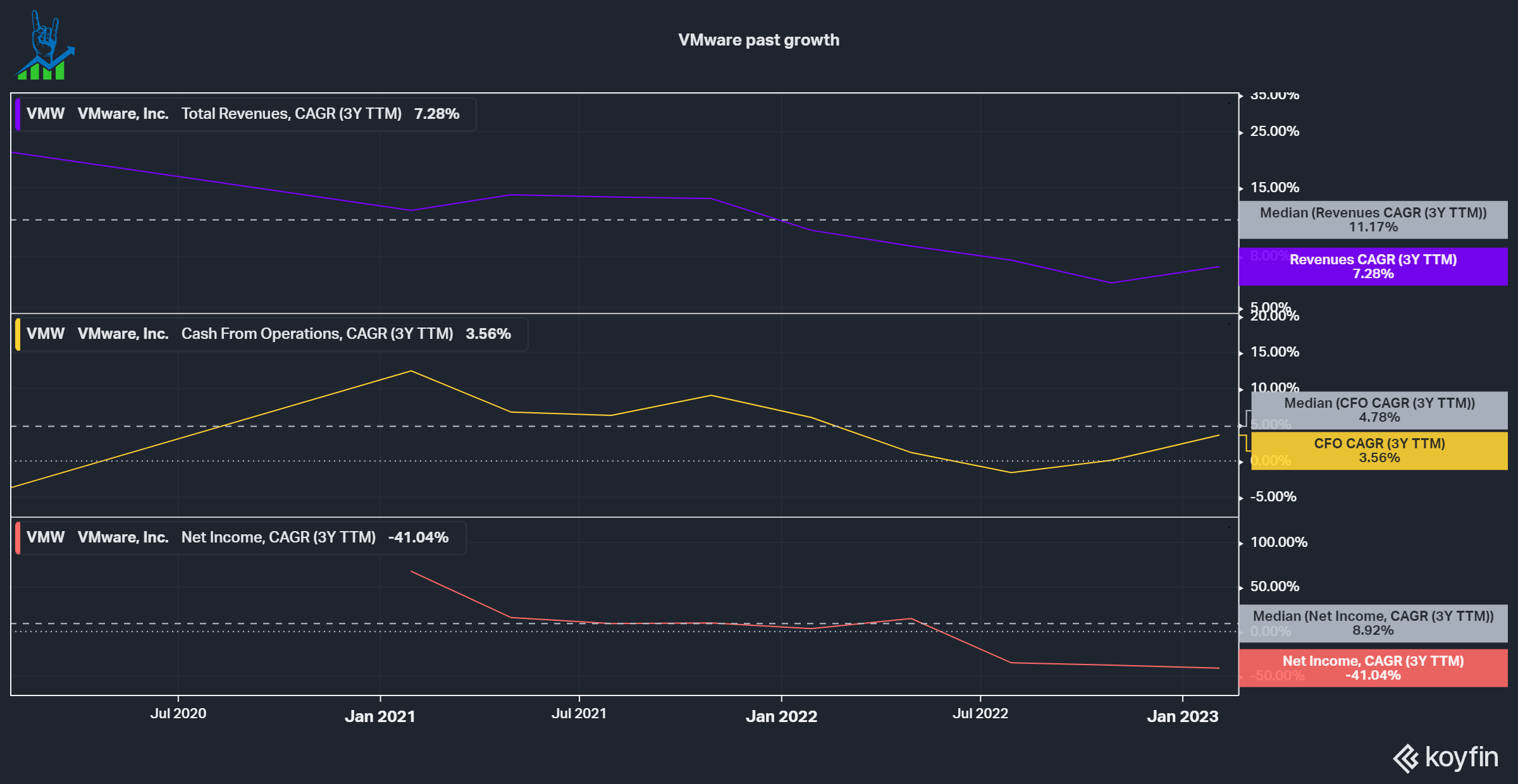

If we look at the past five years for VMware, we can see that the company saw solid growth, with revenues growing 11% on average. Profitability has been lacking behind. With its shift to subscription and SaaS revenue from Licenses, VMW expects to increase its operating margin to 30%. This should help accelerate earnings growth. According to data from Seeking Alpha, the company targets a 10% revenue CAGR, with analysts expecting slightly lower growth.

{kind=link}

Implications for Broadcom

In a previous article on Broadcom , I outlined what I expect the range of earnings potential to be for the company. Besides the M&A risk from the VMware deal, I included the Apple (AAPL) risk: Apple is a large part of Broadcom's revenue (20%) and there are rumors that the company is looking to develop its own chips. While I do not believe it to be a significant threat, I wanted to entertain the thought nonetheless. Depending on the deal and possible (even though unlikely) loss of Apple's business, I came to a range of $15.8-$27.8 billion in EBITDA (around $3 billion at risk from Apple and $3-$8.5 billion from the merger depending on the cost-cutting measures) and used an 85% FCF conversion rate between $13.4-23.6 billion in Free Cash Flow. This leaves a wide array of possible outcomes, but I'll use the reported FCF numbers for the following valuations for both companies.

Both stocks look cheap

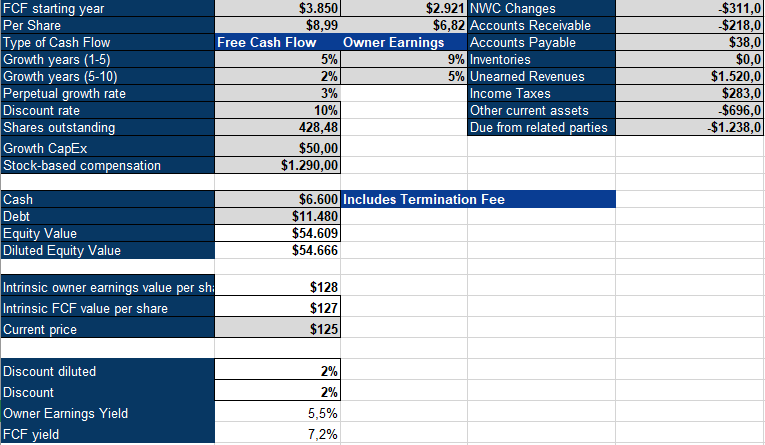

To value both companies, let's look at an inverse DCF model. I calculate it using reported Free Cash Flow and Owner Earnings, which I define as:

FCF + Growth CapEx - SBC +/- Changes in Net Working Capital

We can see that VMware has quite a bit of stock-based compensation compared to its Free cash flows (1/3). Growth CapEx can be largely ignored as both companies aren't heavy spenders on CapEx. Changes in NWC distort FCF somewhat, but not meaningfully. I added $1.5 billion to this valuation model's cash balance from termination fees. With these numbers, VMware needs to grow its Owner Earnings by 9% for the next five years, followed by 5% for the next five years after that. This looks achievable if we consider Analyst expectations of Revenue growth in the high single digits on average and the plan to increase operating margins from the SaaS transition. VMW looks reasonably priced, so I wouldn't expect the stock to drop too significantly even if the deal falls through. At 6% EV FCF yield and 11 times forward EBITDA, the company is priced cheaply on a multiple basis as well.

VMW inverse DCF model (Authors Model)

{kind=link}

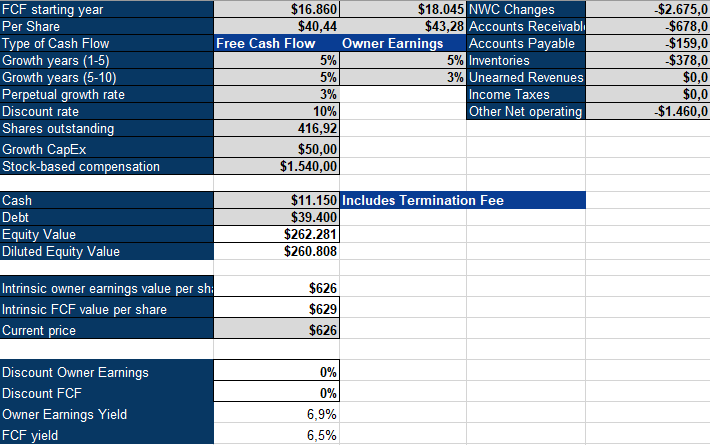

For Broadcom, we can see that SBC is not as much of a problem. Changes in NWC distorted Free cash flow a lot more than for VMware. Growth CapEx is not relevant here; Broadcom outsources most of its manufacturing. I also included the termination fee for this scenario where the deal falls through. This time it is subtracted from the cash balance. Broadcom needs to grow owner earnings at 5% for the next five years, followed by 3% over the next five years after that. This aligns with Analyst revenue growth expectations for the following years and leaves room for the upside from margin optimization.

AVGO Inverse DCF Model (Authors Model)

{kind=link}

Conclusion

Both companies look like a good deal at these levels, even if the deal falls through: VMware should not fall too much, given their fundamentals and fair valuation. They would also receive $1.5 billion (2.5% of the enterprise value) in termination fees. Over the short-term, I'd assume the stock to fall if it is terminated from people selling out of the merger arbitrage positions, but that should rebound given the valuation. Broadcom wouldn't be much impacted by the termination fees and even without the deal, it looks fairly priced, given its valuation and modest growth expectations.

For further details see:

What Is VMware Worth If The Broadcom Deal Fails?