UP - What To Do With Cash Piling Up At The Bank?

2023-07-21 17:58:01 ET

Summary

- I discuss financial planning strategies for 2023, focusing on optimizing cash in checking/savings accounts and tax management.

- I suggest investing in Certificates of Deposit, corporate bonds, and growth/dividend stock investments to make cash work more effectively.

- I also recommend tax strategies such as Capital Gains Tax Management, Roth IRAs, and Roth 401(k) to optimize tax burdens for high-net-worth investors.

Brian Dress, CFA -- Director of Research, Investment Advisor

More than anything, we value feedback coming from our loyal readers that have supported us from the beginning. We have appreciated the complimentary words we have received since we started sharing our investment thoughts here. However, many have remarked that our investment discussions sometimes require a high level of industry experience to comprehend. Believe me when I say, that is the last thing we want to hear from our readers, as we aim to make financial topics more accessible.

In this month's piece, we are going to take a step back and focus almost primarily on financial planning topics, steps which we think you can take to help you build your wealth that don't require you to read complex financial statements or forecast about earnings per share or any other obscure investment metric. Investments are important to building wealth and, by now, you probably understand that this is a focus for us. But just as important to the way we work with clients is to help them make simple changes that can have a profound difference over time.

For the July piece, we are going to cover two main topics that we think have resonance in 2023 based on conversations we have had with clients and other investors throughout the year: (1) what to do with cash building up in checking/savings accounts and (2) how to optimize taxes, as it relates to investments. While we think working with a financial professional is a good way to implement the strategies we will mention below, some of them are tips you can put in place yourself as part of a sensible financial plan.

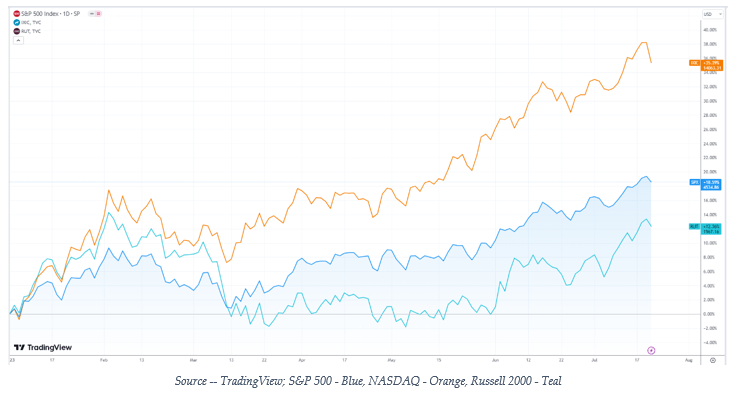

But before we get to those topics, a few words about the current market action. If you have followed us over the last 6 months, you will know that we have been among some of the most bullish market analysts around. We have clearly stated our expectation that both markets and the economy have been well-poised for recovery coming out of last year's bear market. We are pleased to see that to this point in 2023, we have been rewarded for our optimism. As we can see in the graphic below, patient investors that have maintained their positioning in high-quality stocks have been rewarded, thus far in 2023:

{kind=link}

The NASDAQ Composite has shown leadership in 2023, as megacap tech stocks like Nvidia (NVDA), Meta Platforms (META), and Tesla (TSLA), are all up more than 100% in 2023. But in recent weeks, we have seen some broadening on the market rally, with NASDAQ pulling back this week and the small-cap stock-driven Russell 2000 finally starting to show some signs of life. In general, for the overall market to find itself in bull territory sustainably, we will need to see widespread participation from stocks outside the handful of megacap tech companies.

Another data point that I have found to be constructive is the fact that we are seeing strength out of traditionally cyclical sectors like homebuilders and industrials. Despite the fact that interest rates have been on the clear rise in 2023, we have not seen weakness in economically sensitive areas of the market like this. The Industrial Select Sector SPDR Fund (XLI), which contains such heavy manufacturing corporations like Honeywell ( HON ) and Boeing ( BA ), along with transport companies like Union Pacific (UNP) United Parcel Service (UPS), is up more than 12% on the year. At the same time, the SPDR S&P Homebuilders ETF ( XHB ) has gained nearly 40% on the year, despite the fact that 30-year fixed mortgage rates have crept up near 7% . Taken together, we think these data points suggest that the fears of recession over the past year have not come to pass.

With that all being said, let's get into it!

Top 3 Ways to Make Your Cash Work for You!

The most rewarding part of our job as advisors, as well as the most illuminating, is the fact that we get the chance to speak with investors on a daily basis. Doing so gives us an important window into the psychology of what is happening in the economy and in markets.

This year, we have spoken to a substantial number of investors that have significant amounts of cash building up in their checking and/or savings accounts. There are a few reasons for this. First, many investors are understandably shaken after seeing both the stock and bond markets fall considerably in 2022.

Sometimes high-earners are just laser-focused on the things they do well and simply don't have the time to seek out the best opportunities to have their money work for them. We wanted to take a look at some of those uses for cash in today's letter and speak to those of you directly that have cash building up in your low-interest-bearing accounts (a good problem to have, I know). Once you have enough money for a 6-month emergency fund to cover expenses, we think you should consider better uses of your cash on hand.

Bankrate.com, Yahoo! Finance, NerdWallet.com

In researching for this month's piece, we came across some truly disturbing statistics about the amount of return that investors (aren't) receiving in their interest-bearing checking and savings accounts. According to the FDIC , the national average yield on a savings account in a US bank stands currently at just 0.42%, while the picture is even more dire when we look at checking accounts, which are yielding just 0.07%! Not only are banks in the US taking advantage of this cheap source of funding to make money for themselves, but also these paltry rates of return are directly impacting your purchasing power in a time of above-average inflation!

There are many ways to improve your return on cash, but we are going to focus on three in today's letter:

Certificates of Deposit (CDs)

One way in which investors can improve their fixed rates of return is by purchasing Certificates of Deposit (CDs). CDs offer investors a way to lock in a fixed rate of return on a lump sum of money for a specified amount of time. As you can see in the chart above, CDs offer an average 5% return for a 1-year term in today's market. This is a simple and straightforward way to improve your return on cash without taking on any market risk. The downside to CDs is the lack of liquidity, so you will want only to place money in CDs that you will not need to access for the length of the term, whether it be 90-days, 6-months, or 1, 3, or 5 years. For funds that you need ready access to, one alternative to CDs are high-interest money market funds or high-yield savings accounts, which generally have slightly lower yields to CDs.

For CDs, you are not limited to your own bank. You can pursue CDs at any bank throughout the country and you should be looking for the best rate you can find. Many investors might not be aware that their financial advisor can help them find the best CD rate through a brokerage account.

Corporate Bonds

At Left Brain, building portfolios of corporate bonds is one of our favorite ways to put cash to work for clients, without them having to take on direct stock market risk. We know that bonds can be a tricky subject, so in order to make the concept a bit simpler, we want you to think of bonds as a parallel to a loan. When a corporation needs to borrow money, they engage an investment bank to do bond issuance. The bank then sells portions of that loan to individual and institutional investors, the portions of that loan are called "bonds". Where CDs are a way to lend money to a bank for a return, corporate bonds are a means to lend money to any corporation for a return.

As we look again at the chart above, we can see that rates of return on "safer" bonds like US Treasuries, tax-free municipal bonds, and investment grade corporate bonds remain quite low, on average. But again, that is "on average". We are seeing corporate bonds from high quality issuers (either investment grade or just below investment grade) trading with yields in excess of 7, 8, and 9% in some cases. There are a number of key reasons we prefer individual bonds over bond funds: (1) maturity date and cash flows to the investor are predictable, (2) by selecting individual bonds, we have the opportunity to build a portfolio that can deliver greater returns over time and (3) we have control over when/if we realize capital gains and there are a number of tax-efficient strategies that we can pursue to improve your after-tax return.

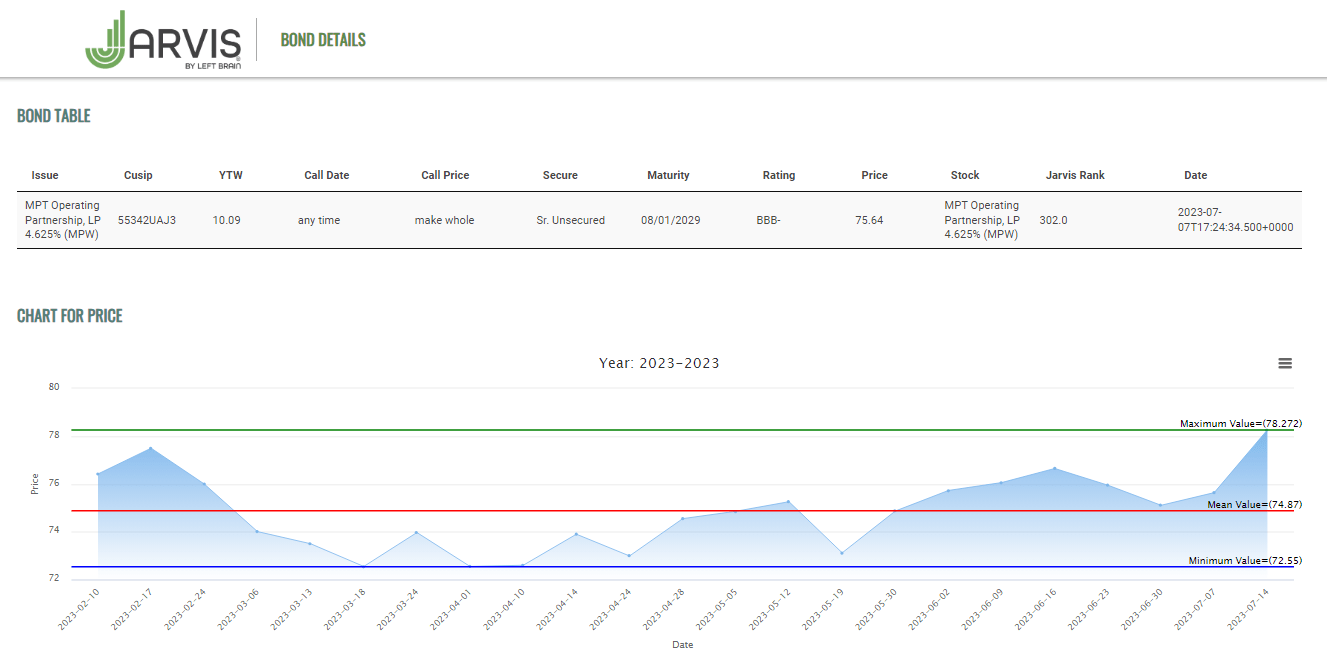

We know this all sounds interesting in theory, but examples better drive the point home, in our view. One of our favorite bonds in the market today is one from Medical Properties Trust, Inc. ( MPW ), a real estate investment trust in the healthcare industry that owns real estate in hospitals and long-term care facilities. Their 2029 bond is BB+ rated (one notch below investment grade) and yields just over 9% annually. You can see more details in the screenshot below from our in-house database of bonds:

{kind=link}

This is just one bond of many that we follow that offer excellent opportunities for high rates of return from investments that are lower on the risk scale than conventional stocks.

Growth/Dividend Stock Investments

We think that most investors have a place in their portfolio for growth investments. Whether you should be in dividend stocks (generally lower risk/return) or in growth stocks (higher risk/return) is a function of your risk tolerance. But over time, stocks have proven to deliver the highest rates of return when compared to other financial instruments.

Selecting which stock investments to choose can be tricky and often it does benefit an investor with a constraint on their time to work with an advisor that devotes his/her time to security selection. Given that most investors could benefit over time from an allocation to growth instruments like stocks, we think if you have considerable cash building up in checking/savings that you should consider getting started with stocks.

Top 3 Tax Strategies for High Net Worth Investors

We know tax time is in the rear-view mirror for most of us, but we think there is never an inopportune time to discuss taxes. With more than 5 months remaining in 2023, now is the time to put strategies in place to optimize your tax burden for this year and beyond. Below are 3 of our favorite tax strategies for high-net-worth investors:

Capital Gains Tax Management

Investors have a leg up on taxes relative to those earning wage income. First, tax rates for long-term capital gains (on assets held for more than 1-year) are significantly lower than corresponding tax rates for W-2 wages:

IRS

But the second advantage is that we can decide when we want to pay capital gains tax. You only pay capital gains tax on an appreciated investment when you sell and realize a profit. Therefore, you have the option of holding an investment ad infinitum and never paying tax.

When you do realize capital gains, there is still a way to mitigate your tax burden: capital gains tax management. If your account shows a gain in a given year, you have the option of selling some losing investments in your account to offset that gain in a strategy known as capital gains loss harvesting. After harvesting a loss, you are able to re-purchase the security for which you harvested the loss in 30 days to avoid what is known as the " wash-sale rule ". There are certainly additional nuances to a capital gains tax management strategy, which you should discuss with a financial professional.

Roth IRAs

Roth IRAs are one of our favorite tax strategies and one of the last bastions of tax relief available to investors. Roth Individual Retirement Accounts (IRAs) allow you to contribute after-tax money, so there is no tax deduction upon funding. However, all growth in the Roth IRA is tax-free forever, so you are able to compound your returns completely tax free for life. Especially for younger investors, we think it is imperative to find a way to fund Roth accounts. Roth IRAs have the additional benefit of no costly Required Minimum Distributions (RMDs), which often balloon household income for tax purposes for retirees. The downside is that there is a relatively low income threshold for eligibility for Roth and the contribution limit is $6,500 per year in 2023 ($7,500 for over age 50).

If you are married, filing jointly and your household generates more than $218,000 in adjusted gross income ((AGI)), you are not eligible for direct Roth contributions. However, you would be eligible for Roth conversions. If you hold a Traditional IRA, you can elect to convert all or a portion of that account into a Roth IRA by paying the tax you have deferred in the year of conversion. For example, if I have a Traditional IRA with $100,000, I can convert that to a Roth this year and I would add $100,000 to my AGI at tax time. It is a straightforward calculation to determine whether a Roth conversion makes financial sense for you, one which a professional advisor can help you complete.

Roth 401(k)

Roth 401(k) is a relatively new tax advantage available to investors in their workplace retirement plans. Roth 401k accounts work similarly to Roth IRAs, in the sense that investors contribute after tax money (in contrast to pre-tax contributions in Traditional 401(k) accounts). So, Roth 401(k) is a great way to get money into your very valuable Roth bucket. However, contribution limits are far less stringent than in the Roth IRA context and there is no income threshold. In 2023, you can contribute $22,500 in after tax money to your Roth 401(k) (or $30,000 if you are over age 50) and there is no income cut-off. For high-earning professionals, this is the best way to fill your Roth bucket.

Many more retirement plan sponsors are offering a Roth 401(k), so contact your plan administrator to see if Roth 401(k) is an option. Your age and tax bracket will have a direct impact on your decision of whether to contribute to a Roth 401(k) or a Traditional 401(k), so contact a financial professional to help you make that calculation.

Remember, it's not what you make, it's what you keep in the context of after-tax income. The same is true for investing income, so pay particular attention to being tax-efficient in your investing!

Takeaways

Another month is in the books and investment markets continue to show strength, despite what some of the doomsayers have been peddling. With that in mind as well as an inflationary environment, we think it is more important than ever for investors with large cash balances to find better rates of return than the <1% on offer at their bank. We think you should let your money work for you and not for your bank's profits! Some good options in that regard include CDs, corporate bonds, and, of course, the stock market.

We also think now is a great time to think about tax-efficiency in your investment strategy. Three potential strategies to that end are: Capital Gains Tax Management, Roth IRAs, and Roth 401(k).

DISCLAIMER: This report contains views and opinions which, by their very nature, are subject to uncertainty and involve inherent risks. Predictions or forecasts, described or implied, may prove to be wrong and are subject to change without notice. All expressions of opinion included herein are subject to change without notice. Predictions or forecasts described or implied are forward-looking statements based on certain assumptions which may prove to be wrong and/or other events which were not taken into account may occur. Any predictions, forecasts, outlooks, opinions, or assumptions should not be construed to be indicative of the actual events which will occur. Investing involves risk, including the possible loss of principal. The opinions and data in this report have been obtained from sources believed to be reliable; neither Left Brain nor its affiliates warrant the accuracy or completeness of such and accept no liability for any direct or consequential losses arising from its use. In addition, please note that Left Brain, including its principals, employees, agents, affiliates, and advisory clients, may have positions in one or more of the securities discussed in this communication. Please note that Left Brain, including its principals, employees, agents, affiliates, and advisory clients may take positions or effect transactions contrary to the views expressed in this communication based upon individual or firm circumstances. Any decision to effect transactions in the securities discussed within this communication should be balanced against the potential conflict of interest that Left Brain, its principals, employees, agents, affiliates, and advisory clients has by virtue of its investment in one or more of these securities.

Past performance is not indicative of future performance. The price of securities can and will fluctuate, and any individual security may become worthless. A high or favorable rating, rating outlook, gauge, or similar opinion is not indicative of future performance, and no user should rely on any such rating, rating outlook, gauge, or similar opinion to predict performance or potential for return. Future performance may not equal projected or forecasted performance or potential for return. All ratings and related analysis, as well as data, statistics, analysis, and opinions contained herein are solely statements of opinion and are not statements of fact or recommendations to purchase, hold, or sell any security or make any other investment decisions.

This report may contain "forward-looking" information that is not purely historical in nature. Such information may include, among other things, projections, and forecasts. There is no guarantee that any forecasts made will materialize. Reliance upon information herein is at the sole discretion of the reader.

THE REPORT IS PROVIDED ON AN "AS IS" AND "AS AVAILABLE" BASIS WITHOUT REPRESENTATION OR WARRANTY OF ANY KIND. Left Brain Wealth Management DISCLAIMS ALL EXPRESS AND IMPLIED WARRANTIES WITH RESPECT TO THE REPORT, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE.

The Report is current only as of the date set forth herein. Left Brain Wealth Management has no obligation to update the Report, or any material or content set forth herein.

For further details see:

What To Do With Cash Piling Up At The Bank?