UP - Wheels Up Experience: Targeting Non-Existent Customers

2023-07-12 07:21:04 ET

Summary

- I have been tracking Wheels Up and noted a near-70% decline in the company's value in a short time.

- Investors who held their shares since the last bullish article on Wheels Up have lost 94.17% of their original investment.

- I emphasize the importance of focusing on profit, valuation, and basic fundamentals, not just top-line revenues, and consider this company to be a zero.

Dear readers/followers,

I've been following Wheels Up ( UP ) for some time, going from a neutral "HOLD", to a negative "SELL", and now I'm going to do my final article on this company before I abandon it in my coverage spectrum. Since my last article , this company has realized the lack of potential that I forecasted for it. Since my last piece, this is the RoR we've been seeing. I don't short stocks, but this could obviously have been profitable to do in this case.

Seeking Alpha UP RoR (Seeking Alpha)

So, a near-70% decline in the company is quite amazing in such short a time. The last bullish article on UP here on Seeking Alpha was around a year ago now, and since that particular piece, investors have (if they held their shares) lost a solid total of 94.17% of their original investment. The bullish thesis at this point was a "strong earnings release" (though without GAAP/net profit), and recent company initiatives, as well as quoting Active members, active users, and live flight leg numbers as well as some top-line growth.

This highlights the importance of focusing on profit, not top-line revenues, as well as valuation, as well as basic fundamentals.

Let's look at what we have here.

Wheels up experience - it's going to $0

The latest results for UP we do have is the 1Q23. In those results, the company does call for a "Path to positive adjusted EBITDA in 2024". Now, given that we're talking positive adjusted EBITDA, this could almost mean anything, given the "adjusted" portion of that statement.

Other than that, the company provided Program Changes, Leadership changes, and business changes - pretty much everything in the company is changing - which is a positive to me, because things obviously were not working previously.

The company was able to report increasing membership fees, by 5%, but slipping Flight income, down 2%. The gold star goes to "other", which saw 327% top-line growth - though this is a small segment, the by far smallest of the company.

The lauded plan to reach positive Adjusted EBITDA is as follows.

{kind=link}

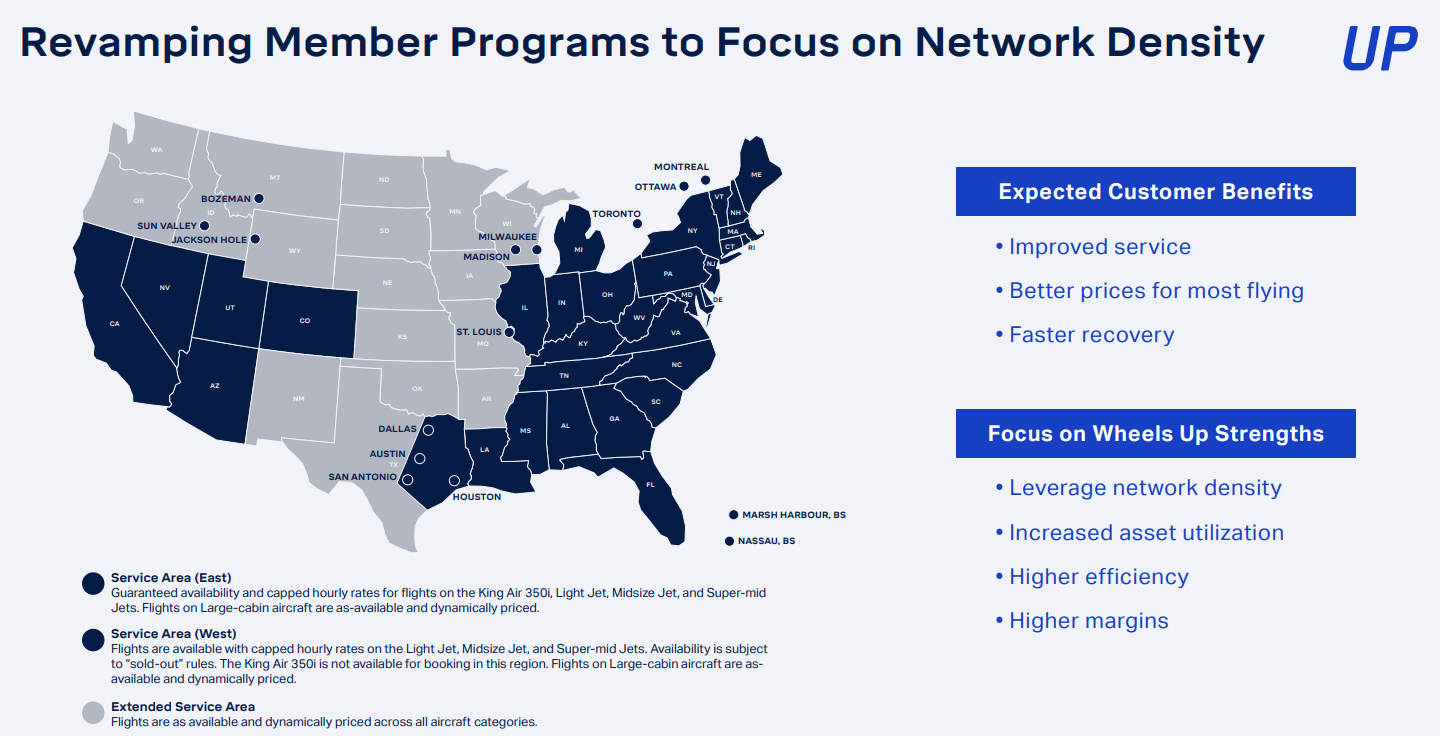

And that's it. Call me pessimistic, but this is not exactly a groundbreaking plan. Almost every organization can try to address SG&A, overhead, and other streamlining. The company does of course need to change its programs, as well as try to find efficiencies in its aircraft management. However, one of the challenges of owning aircraft, as UP has no doubt noticed, is the sheer amount of required maintenance and related costs. Moreover, the company is refocusing its membership areas to focus on where customers actually are. In layman's terms, it's further "asterisks" to the whole "Wheels up experience".

{kind=link}

What's the company doing today , and what has it already done? Well, they're reducing headcounts, and "evaluating" further reductions in fixed costs and cost reductions, without really going into what these are. They're trying to leverage and improve margins with better fleet management, and consolidate certification, but the company is already talking about carving parts of the business off by "divesting non-core assets" - to which my response would be, what exactly would they be divesting? As of yet, details or concrete plans on this are extremely sparse.

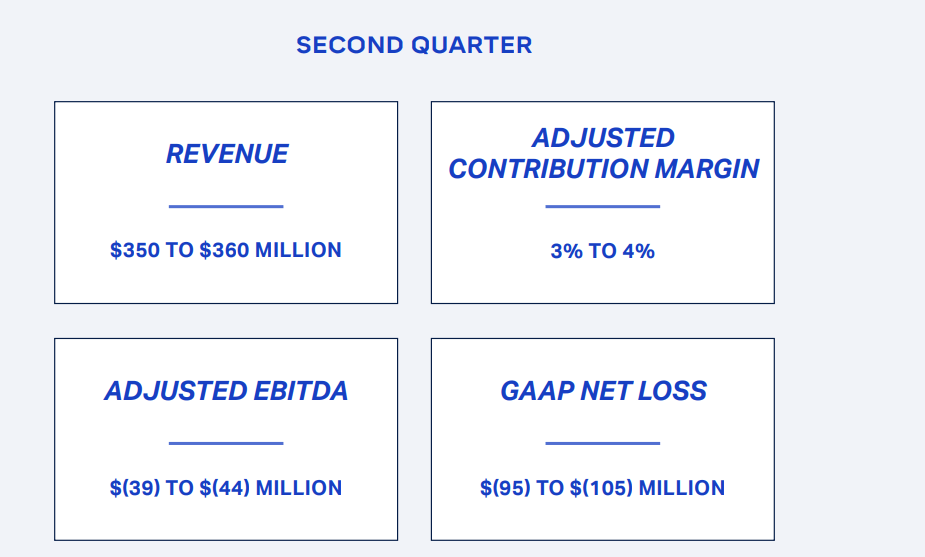

The company does what it can to present the case positively - see the following in terms of guidance.

{kind=link}

Most of it adjusted, and with a GAAP net loss in excess of $100M, potentially, for a single quarter, coming to a run rate of around negative $400M.

The question becomes how long the company can survive this inarguably terrible state of being in a rising interest rate environment where money is becoming more and more expensive in terms of funding its operations. With its share price bottoming, issuing equity should also be out of the question. The company has barely-positive 2.78% gross margins , negative operating margins of 24%, negative net margins of 35.33%, and a negative RoE of over 130%. To call the company, at this juncture, to be "troubled" is a gross understatement.

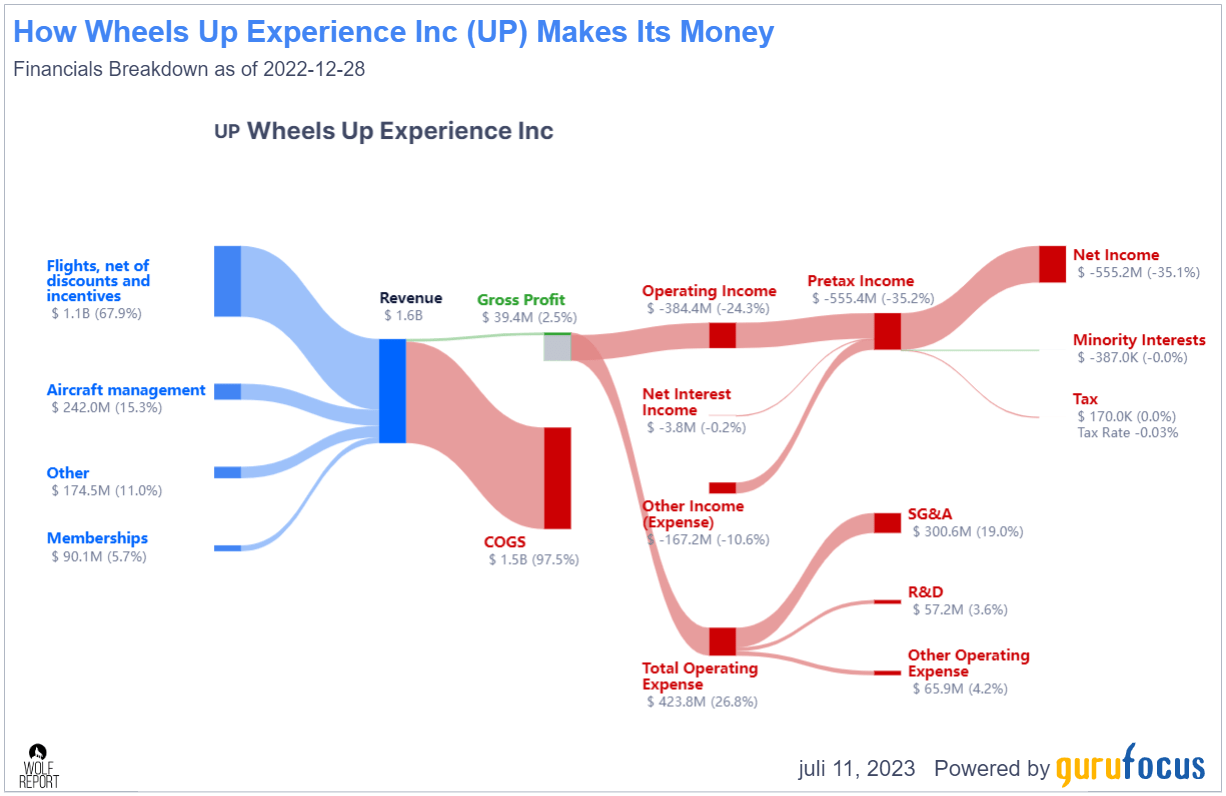

This, as you see below, is the worst revenue/net flow that I've seen in any company I've officially covered in my history as an analyst. It's also the reason why this article represents my final look into UP.

{kind=link}

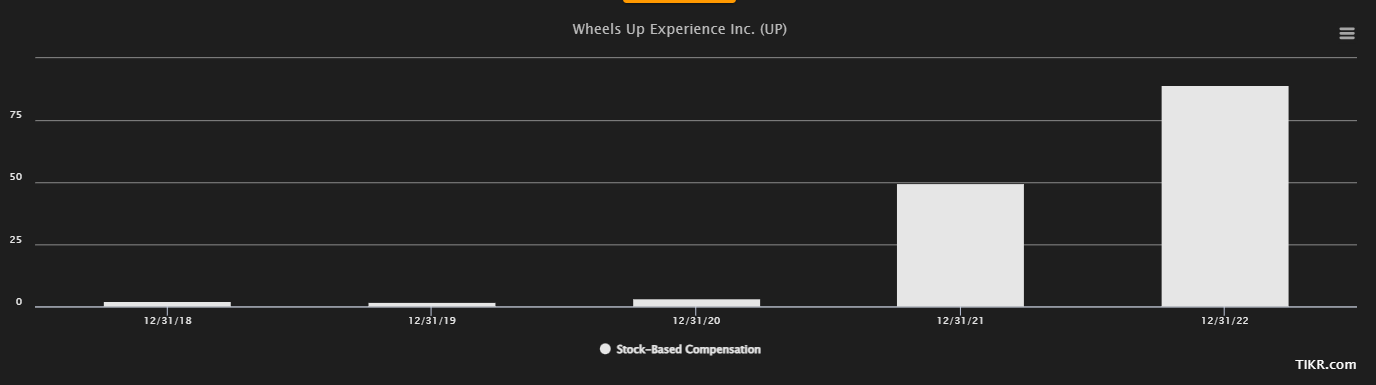

I suppose if the company makes what would be an absolutely miraculous turnaround and turns profitable, I will do the equivalent of "eating crow" and show where I turned out to be wrong here - but I do not believe this to be the case. Take into consideration that as the share price has been plummeting, the company's management has ratcheted up SBC to never-before-seen levels for this company. The 2022 SBC alone was nearly the entire loss for a quarter on a GAAP basis, and that's saying something.

{kind=link}

I've said before that my problem with UP goes very deep, and I'll state it with clarity here in my last article.

UP's business idea is predicated on the assumption that there exists a group of people that over the course of business and economic cycles would prefer to pay for a membership in a company where they can get something between a private jet and flying commercially in first class. They believe this group of people to be large enough to base a business model upon, and they believe that these people will not only be willing to pay for this but also keep paying as the circumstances and specifics of this model change, as we've seen as late as this quarter, rather than pay less money for a ticket in business or first class on a commercial flight, even in the face of a significantly declining economy, upwards inflation and everything that comes with such a downcycle.

I do not believe this group of customers exists in the same way that the company believes it does. I believe it does not exist or is insufficiently "sticky" to a degree that it invalidates the company's business model and profitability - and I believe the recent results are a confirmation of this stance.

What part of it?

Well, the company recently suspended all full-year revenue guidance. The current quarterly guidance calls for a near-20% revenue decline organically. The company, in the latest earnings call can't pinpoint one specific factor that's driving this, instead referring to analysts where they as a company have tried to target growth and profit, they have turned out not to be profitable at all. The company also refers to a general slowdown consistent to the entire industry - again, I could have guided for this before this current environment even began.

What'll happen, I believe are a few things in such an environment.

- The jet owners will for the most part retain their private jets if they can. If they own them in the first place, they're likely to be able to continue to finance them, though some may be forced to sell and step down to commercial flights as the "jaws" close in terms of costs, inflation, and interest rates.

- The commercial flyers will likely try to find cheaper tickets, fly less, or get better deals to offset some of the cost increases.

The problem is that the company targets a customer group between those two. The group that wants that private jet experience, but can't really afford it in the first place. When the jaws close around the economy for these individuals, they will, I believe, be the first to chuck their membership out the door. None of them will go up to jet owners - not in this environment. Instead, they'll likely all (or most) move down to coach. Only very few will in this environment say that "Yes, I want to pay a monthly fee for access to a private plane that I share with others and where I have to pay by distance, instead of flying commercially, even in this environment."

Because the company's customers are no longer as numerous, or maybe by themselves were a product of ZIRP (this is my actual stance), I do not believe this business model to be sustainable.

And this is the reason why I view the company as "done" here, and move on to valuation.

Wheels Up Valuation - Not much to like.

As for this article, I am saying that UP is not worth actual money. By that I mean the common share is not investable, and by that, I mean that if you invest in this company, it's my conviction that your investment even in the case of a SOTP breakup and sell-off, will turn out to be worth $0 after the company's creditors and other senior lienholders/debt holders are satisfied.

I am saying that factually speaking, the company's P/S ratio here is 0.02x, and it trades at a negative EV/Gross profit of 0.09x. The current share price represents a book value of 0.21x and a tangible book value of negative 0.1x. Remember, tangible BV excludes the value of intangible assets. This means that the company's assets that can be liquidated have a negative value. What this means is that the company's liabilities are greater than the company's tangible assets.

This in itself does not make a company, or even this company, uninvestable. That is not what I am saying. The reasons the company is uninvestable are visible all across the board - from a negative ROIC net of WACC of -27% to the company's quarterly results.

One of the clearest signs that influence my view on valuation here is that we're seeing the general customer pull-back I've been waiting for. These are not my statements - the company itself and management noted in the earnings call that prepaid block sales are down significantly. The only positive is that it can be said that 2021-2022 was an ATH for block sales - the problem is, as I said, I believe that "was it" for this company. Its appeal outside of that macro is limited, or can even be said not to exist.

Once the company comes out with more competitive rates and more "competitive" terms, I believe the appeal of the company's business model, which when it dilutes its terms and exclusivity, will drop for its customers as well, and this decline in block sales will continue further. If you were positive about the company, it's these block sales that I would keep an eye on going forward.

As of yet, the company hasn't given any indication of what its asset disposals are (see below).

Yes. I mean just given where we are in the process, I won't give any specifics about exactly what those are, as I'm sure you can understand. I mean, obviously, we're working through that with -- in the appropriate way. But I would say this is really a continuation of some of the things that we've been talking about for now for a few quarters, right?

(Source: Todd Smith, 1Q23)

And frankly, listening to the earnings call, investors might not be certain whether management is adjusting to current reality or is delivering any sort of ideas as to how positive GAAP might at any time in the near future be possible. This is not me calling out or criticizing the team - because as I've said, I do not believe that to be a possible goal.

At this time, I'm officially ceasing my coverage of UP, with the following thesis.

Thesis

- Wheels Up is a company that targets the private aviation market and seeks to make the concept of flying "private", or "Wheels Up", available to everyone, or at least a wider audience.

- I question whether this customer segment actually exists, and more importantly, whether the customers can provide positive GAAP to the company, which to me is the first requirement for an investable business.

- I cease coverage on UP calling the company a "SELL". I do not believe the business idea to be investable in a profitable way for common shareholders.

- I will not give the company a PT, owing to its negative tangible BV.

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria:

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company fulfills none of my criteria for investment.

For further details see:

Wheels Up Experience: Targeting Non-Existent Customers