UP - Wheels Up: I Hope You Avoided This One

2023-04-29 15:56:31 ET

Summary

- I wrote about Wheels up a few months back based on a request from a subscriber. Fortunately, she reached the decision not to invest in the business with her capital.

- While the company may have theoretical appeal, Wheels up has declined over 50% since my last article, where i cautioned on this company.

- I continue, even after a 50% decline, to be careful here, and i say that there isn't a big enough upside here. Here is my update on Wheels Up.

Dear readers/subscribers,

Wheels Up ( UP ) is a problematic business and one I reviewed back in mid-February in my article back then . Since that time, and since I cautioned on buying or even considering buying this company, the share price has declined nearly 60%. That is a massive crash in a very short time.

UP Article RoR (Seeking Alpha)

Of course, there are reasons for the movement - and reasons for why I'm overall pretty "negative" about this company overall. I would say this investment is suitable, at this point, for almost no one. The reason is that even if you have a high-risk tolerance, there are plenty of options out there for you that have better potential upside, along with a good yield with far better fundamentals.

And if you don't have a high-risk tolerance, to begin with, I see no reason beyond simple curiosity to even look at a business like Wheels Up.

Let's review and see what we have here.

Wheels Up - A quick review

This company had, for what it offered, a surprising amount of bullish articles associated with the stock. All of those bullish articles have seen a post-article RoR of more than negative 82%. While there is always a risk, and well-disclosed, of investing in microcaps, it's my view that the risk with this company was extremely elevated, to begin with.

In order to be bullish on a company like Wheels Up, you have to assume that there regardless of the macroeconomic situation, will be a segment of the population that is prepared to pay for the private jet experience/sharing experience, rather than paying an already-expensive amount for what is given/offered if you fly first class commercially. I personally have a very hard time gauging at what point in a financial life/net worth, a private jet or a solution like Wheels Up would become preferable to the risk/reward of simply always picking first class. The costs associated either with jet ownership or the costs associated with this sort of service are simply massive.

Early bullish stances on this company when it was higher, focused on things like brand recognition and that once you start flying private, it's difficult to stop that habit.

I view this stance and the reason for the stance as somewhat flawed. Flying private is such a cost-prohibitive habit that once the economy changes, and your personal financial circumstances change, it becomes something you can't even "elect" to break, because the cost is as much as your mortgage, or your entire fleet of cars. It becomes less a question about "wanting" to break the habit and more about simply not being financially able to afford it

Positivity aside from this was usually related to arguments the company made itself - such as TAM numbers and potential wide appeal. I personally have a very hard time understanding how even during the frothy period during the tech bubble, people were willing to put their hard-earned capital to work in a business like this - but then, this was my stance when it came to many of these companies, and some people made money on them nonetheless.

UP IR (UP IR)

I believe any business that you invest your money in, should be able to back up its marketing and arguments with a working business model. By working business model, I mean that on one end revenue comes in, and on the other end, a positive GAAP/net profit comes out. Or if not that, a clear pathway to positive earnings.

Wheels Up has never had this, and it still doesn't to this day. As before, there are far too many "buzzwords" for my taste, and nothing takes away from the fact that we're talking about an unprofitable business with no real prospect of becoming profitable at any time in the near future. In a business that's in the prospect of turning around, you can usually see signs in the form of improving margins, cash flows, and other key indicators - but none of that is visible here. Instead, what we see, are worsening margins, increasing debt, and more problematic macro that challenges the company even further.

Like with other companies debuting during the zero-percent interest rate period, the company is trying to right its operations during a time where money is getting increasingly expensive. More than that, recent data confirms that customers and households across most income sizes are cutting spending. GDP growth is down, inflation is up more than expected in the US during 1Q. All of this is indicative, and a company that lives on hiring out private jets to customers who typically have not had the capital to afford them, well they're going to face some challenging times.

The company cannot scale its business easily. Anyone who argues economies of scale or an upcoming upward trend in the near future, the indicators I talk about above, is easily disproven by reported financials. Even gross margins are now down to less than 6% - that's gross margins , operating margins are significantly negative into the double digits, and so is every single net indicator in the company that would matter to me as a valuation investor.

The reason I'm driving these points home is to try and educate readers so that they not only avoid UP but avoid investing in companies that have flawed financials, to begin with. Far too many investors go for these companies based on pure hope or assumptions. I do not this as a good approach.

I myself am no stranger to calculated risks - but the key word here is "calculated". What remains if the company cuts the dividend? How are the fundamentals? Would I mind holding this business for 2-4 years while it recovers? All of these questions should be asked prior to any investment made, and too few people ask them early enough prior to going in.

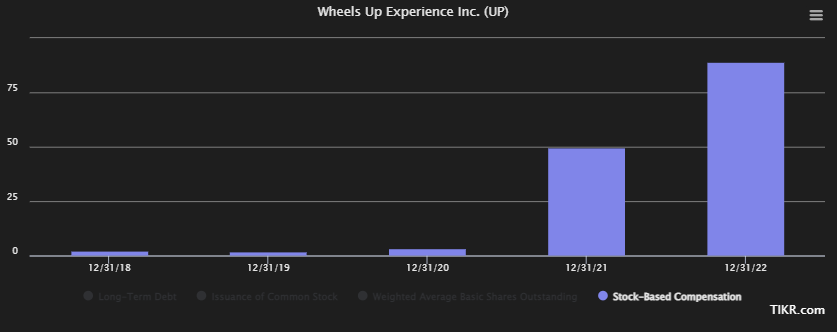

There is also the question of significant shareholder dilution potential. Because the company is, and is likely to remain, strapped for cash, it will need to tap either equity or debt in order to continue operations. It in fact has already done this by increasing its debt to all-time highs in fiscal 2022, currently at over $200M for a company with a market cap of above $100M. Whenever you do need to raise capital, the question becomes at what cost - and as things look today, it seems doubtful that the company can do so at any sort of appealing rate, be it equity or debt. SBC, or stock-based compensation is absolutely through the roof. This company can be used as a cautionary tale, essentially showering SBC during times of only top-line growth.

{kind=link}

There are institutional investors that bought the stock back in December - but those institutions have lost the same 64-94% in value that everyone else investing in UP has. The best thing that can be said is that management has not excessively sold the shares they do own - but the fact is that management has been a very prolific buyer of its own shares - at least up until 2022-09-19. From that point onward, only one "BUY" has been made - the remaining trades have been "SELL".

This does not paint a pleasant picture with regards to the potential dilution that shareholders face if they were to invest more, or for new shareholders, if they do invest here.

Any of the metrics the company presents in its communications are really only of limited value to us, and almost none in terms of actual profitability.

{kind=link}

This brings me to my updated valuation section, and it's not a pleasant read.

Wheels Up - The valuation remains uninteresting

I joked about a $0 valuation in my last article, but this really becomes more than a joke at this point. I have no tolerance for loss-making companies in a segment I believe to have tremendous challenges, because even if the company might survive, the equity holders may not. Estimating what a negative profit business is worth pretty much can come down to the SOTP valuation, the sum of the company's parts, once debt and other considerations are removed. And once you get into SOTP, it usually starts to also consider what happens to the equity holders in such a scenario.

Because once company's start to consider break-up value, that's usually what happens, and C11 or equivalent is on the horizon.

When I last reviewed UP it was trading at the lowest revenue multiple I had ever seen of 0.05x. The company's current revenue multiple is now negative, and it trades at a sales multiple of 0.07x. No serious company at this point that I know of, that has ever recovered, has seen these multiples.

When I last wrote about this company, 7 analysts still gave the company a range starting at $2.4 and going up to $5/share with an average of $3.75. That's what happens when you initiate coverage in 2020 and claim that the company is worth $20/share, which is what some of these analysts did. It becomes somewhat disingenuous if you go from saying "It's worth $20/share" to "Sorry, it's worth $0".

I'm saying this because, despite delisting concerns and reverse splits, analysts are still saying that this company is worth $2.7/share on average, with 2 at a "BUY" and 3 analysts at "outperform".

Meanwhile, if I was employed as someone's financial advisor, I would cut them off mid-sentence and tell them to "SELL" this company. I don't believe it's going anywhere. I don't believe there is saving potential for it.

In my last article, this was the first company in over a year where I declined to give a target share price.

I'm doubling down on this stance at this point, and I'm telling you that my rating for this company is "SELL". After a nearly 60% drop, the company had no convincing plan for achieving profitability, after every single profitability metric in the negative and in the 4-6th percentile in the entire transportation industry (Source: GuruFocus), I do not see a single saving grace for this company in the long run.

Even with current forecasts, the net income margin is expected to stay fully negative beyond 2027E (Source: S&P Global), and this is not excusable for me in any investment at this time.

Oh, and did I mention it has debt? Over $225M long-term debt.

You would literally, as I see it, be better off putting your money in a 2%-yielding savings account.

The following thesis is relevant for UP here.

Thesis

- Wheels Up is a company that targets the private aviation market and seeks to make the concept of flying "private", or "Wheels Up", available to everyone, or at least a wider audience.

- I question whether this customer segment actually exists, and more importantly, whether the customers can provide positive GAAP to the company, which to me is the first requirement for an investable business.

- I am now at a "SELL" - I would say it's dangerous to hold UP here.

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria:

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company fulfills none of my criteria for investment.

For further details see:

Wheels Up: I Hope You Avoided This One