VTRS - Why 5%-Yielding Viatris Hasn't Doubled Yet

2023-09-14 06:07:30 ET

Summary

- Viatris is a healthcare corporation formed through a merger, with a diversified global portfolio and a focus on ophthalmology, gastrointestinal, and dermatology therapeutic areas.

- Despite its elevated debt load, Viatris has demonstrated strong financial performance, including revenue growth and high free cash flow, supporting its strategic progress and dividend sustainability.

- Trading at low multiples of EBITDA and free cash flow, Viatris stock presents a long-term investment opportunity, but its valuation improvement may take several years.

Introduction

It's time to discuss a stock that many readers requested me to finally cover. Besides that, after discussing some of its peers, it's time to finally dive into Viatris Inc. ( VTRS ) as well.

FINVIZ

Before writing this article, Viatris has never been on my watchlist, as its stock price has performed poorly since the 2020 merger. I couldn't be bothered to take a closer look, as many of its peers performed better.

Having said that, I changed my mind and believe that Viatris offers significant long-term potential. While it has a slow-growing business, its pipeline is promising, its performance is strong, and its dividend is well-protected.

The problem is that its debt load is elevated, which isn't doing the company any favors in this environment. However, the balance sheet is sustainable, and free cash flow is so high that it supports rapid debt reduction.

While VTRS hasn't been a fun stock to own in recent years, I believe its long-term potential is good.

So, let's dive into the details!

What's Viatris?

Viatris is a very young company.

On November 16, 2020, the company was formed by merging Upjohn and Mylan in a Reverse Morris Trust transaction.

{kind=link}

As a result of this transaction, Mylan emerged as the parent company of the combined Upjohn and Mylan businesses. After the formation of the company, it underwent various strategic initiatives, such as partnering with Biocon Biologics, divesting some non-core assets, and acquiring companies in the ophthalmology sector.

Now, the company is a standalone global healthcare corporation with a mission to improve access to sustainable and high-quality healthcare for people worldwide.

The origin of its name is based on these goals, as Viatris comes from the Latin words Via and Tris , meaning path and three . The path to the three objectives is expanding access to medicines, meeting patient needs through innovation, and earning the trust of the healthcare community.

With a workforce of approximately 37,000 employees, Viatris operates in over 165 countries, offering a portfolio of more than 1,400 approved molecules across various therapeutic areas.

Viatris also has a major foreign footprint. In 2022, the company generated just 24% of its revenues in the United States.

| USD in Million | 2021 | Weight | 2022 | Weight |

|---|---|---|---|---|

| Brands | ||||

| 10,841 | ||||

| 60.6 % | ||||

| 9,890 | ||||

| 60.8 % | ||||

| Generics | ||||

| 5,630 | ||||

| 31.5 % | ||||

| 5,015 | ||||

| 30.8 % | ||||

| Complex GX and Biosimilars | ||||

| 1,342 | ||||

| 7.5 % | ||||

| 1,313 | ||||

| 8.1 % | ||||

| Other | ||||

| 73 | ||||

| 0.4 % | ||||

| 45 | ||||

| 0.3 % |

The company has a well-diversified business and is increasingly emphasizing ophthalmology, gastrointestinal, and dermatology as its core global therapeutic areas, with acquisitions in the ophthalmology sector.

This is an announcement from 2022:

{kind=link}

Essentially, Viatris aims to create a leading global ophthalmology franchise, addressing unmet needs in eye care.

Between Elevated Debt And Shareholder Returns

Viatris hasn't been a great place to be. Since early 2021, shares have lost roughly half of their value. The stock is 21% below its 52-week high and 16% above its 52-week low.

Over the past two years, shares are down 32%, including dividends. The Health Care Select Sector ETF ( XLV ) and S&P 500 have returned more than 10%.

The reason I added Organon ( OGN ) to the chart is because, like Viatris, it is a spin-off with an elevated debt load that seems to struggle despite having a strong portfolio of products. I discussed OGN in this article .

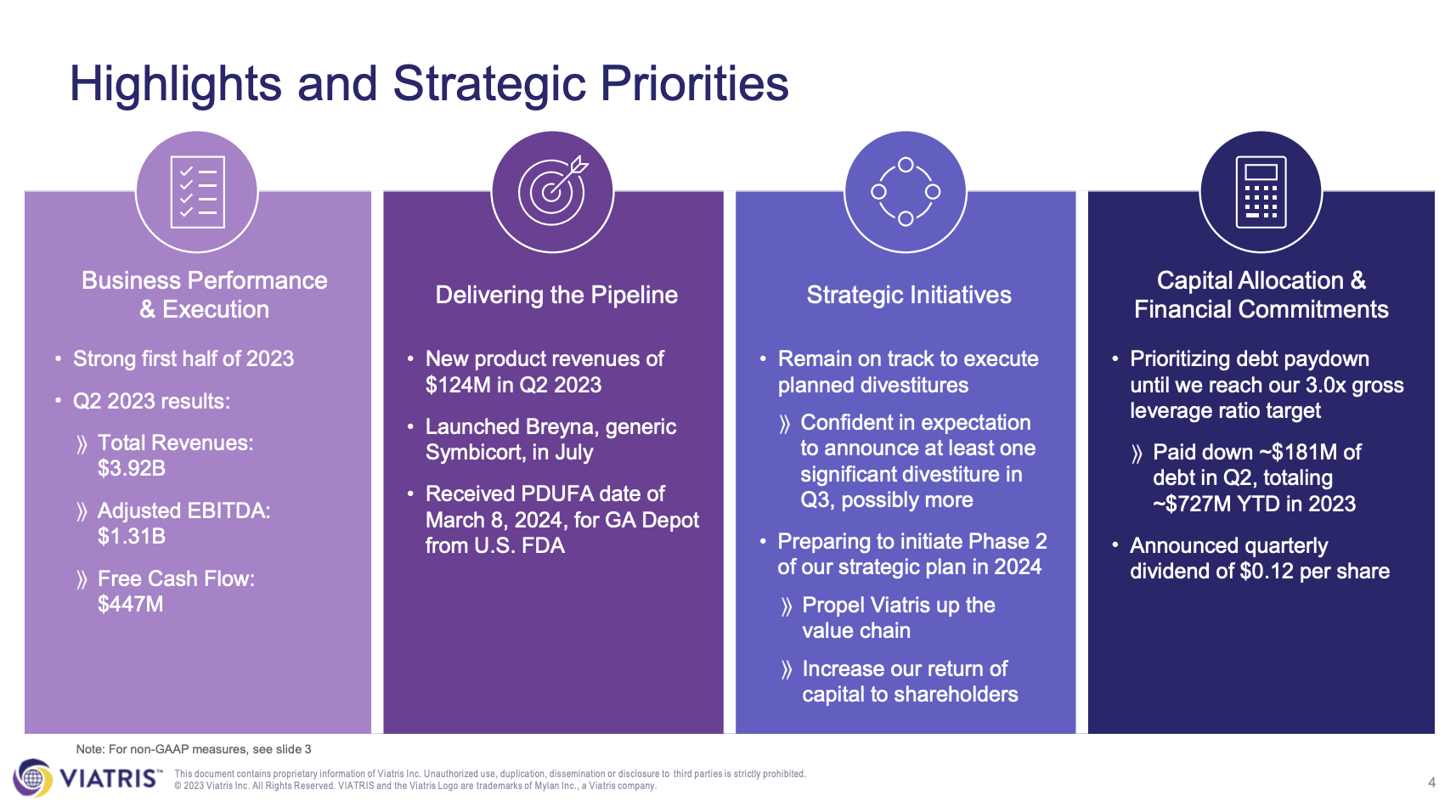

Before we get to the debt part, the company is doing very well when it comes to its strategic progress.

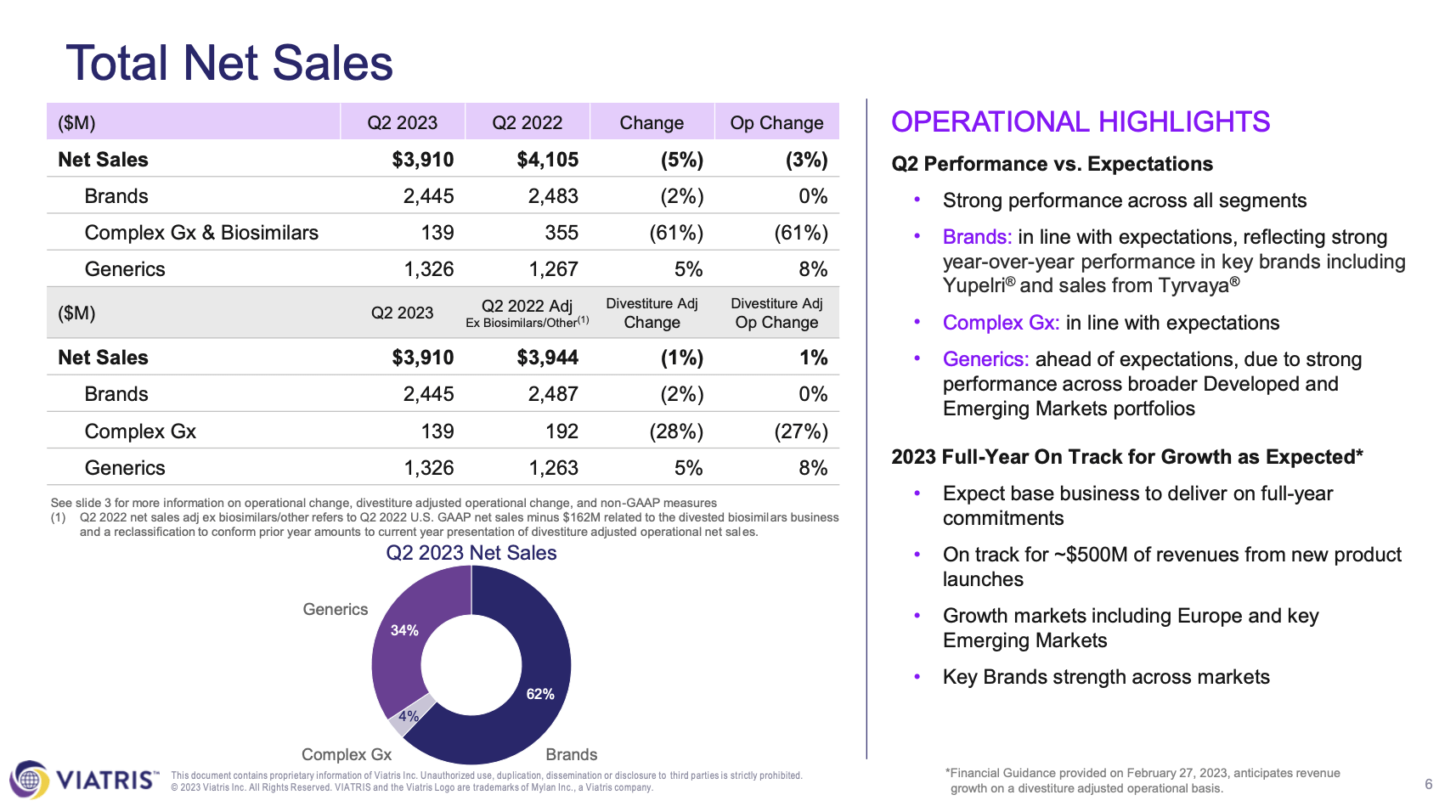

In the second quarter, the company achieved total revenues of $3.9 billion, which translates to a 2% year-over-year growth rate on an operational adjusted basis.

Additionally, Viatris reported adjusted EBITDA of $1.3 billion and free cash flow of $447 million, both of which exceeded expectations.

{kind=link}

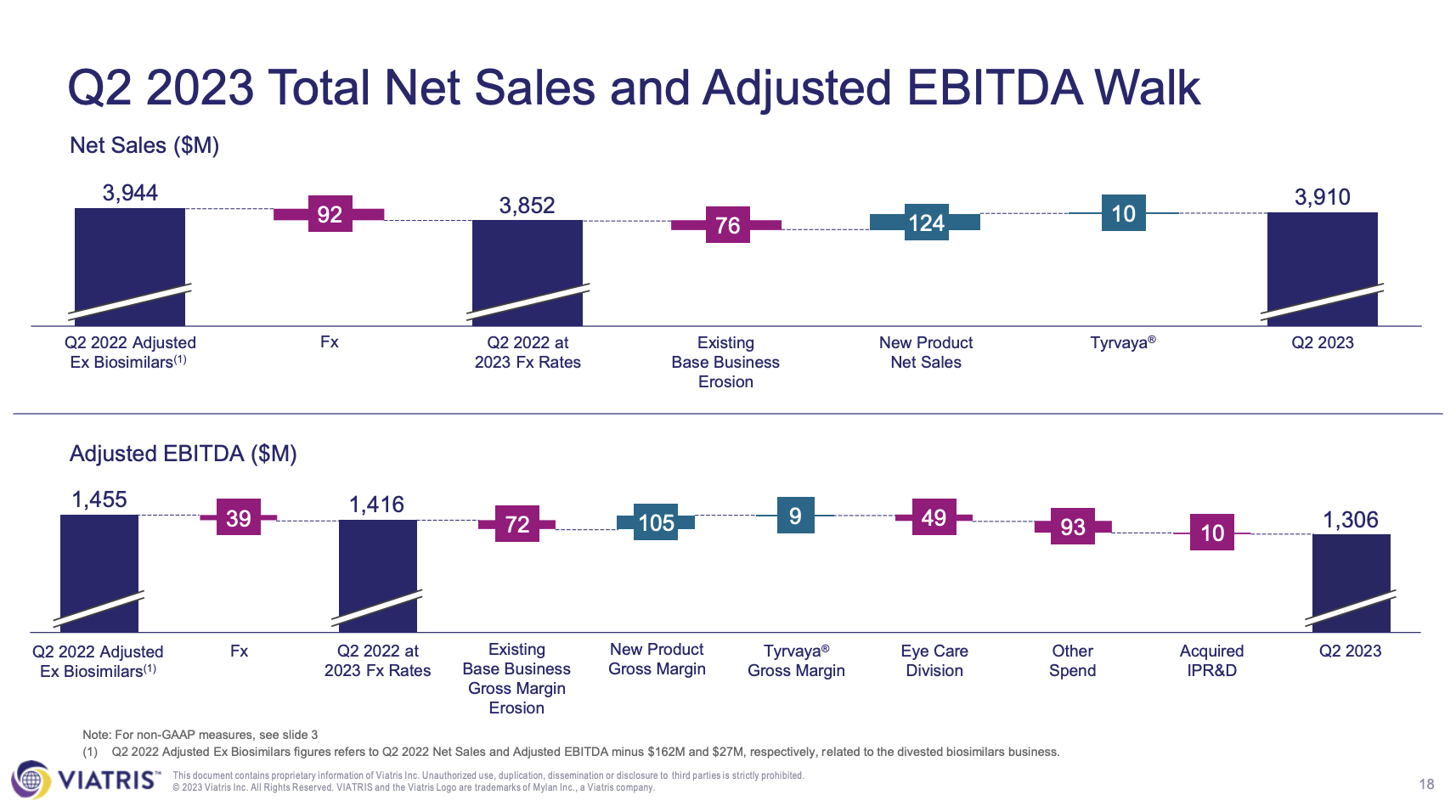

Foreign exchange rates had a 2% impact on net sales, with a diverse portfolio of growth drivers contributing to this performance, including brand performance in emerging markets, Europe, and Greater China.

The overview below shows the various drivers of net sales and EBITDA between 2Q22 and 2Q23.

{kind=link}

The company expected these trends to continue into the second half, supported by product seasonality and the continued launch of new products.

Viatris also believes that this performance is a reaffirmation of its full-year financial guidance for 2023, setting the stage for future success as it progresses through its strategic plan.

{kind=link}

Viatris is dedicated to delivering its pipeline and is excited about its upcoming product launches.

The company has divided its strategic plan into two phases. Phase 1 is expected to be completed successfully, with Phase 2 commencing in 2024.

As part of its plans, Viatris is actively pursuing planned divestitures, and they are on track to announce these transactions throughout 2023.

In light of its elevated debt load, these divestitures are seen as a strategic choice rather than a necessity, and the company is currently in advanced discussions with potential buyers.

The announcement of significant divestitures is expected in the third quarter.

Going back to its guidance and outlook, the company's emphasis is on paying down debt, having already paid down $6.1 billion since the beginning of 2021, with plans to pay down another $500 million in 4Q. They also returned approximately $144 million to shareholders through dividends in the second quarter.

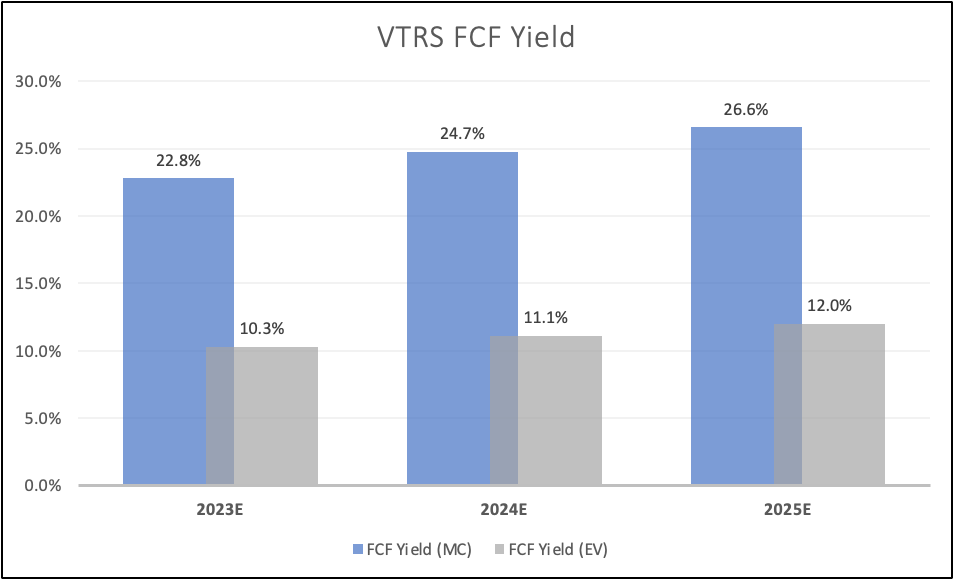

The chart below shows the impact of net debt. Analysts expect the company to end this year with $16.6 billion in net debt. This is more than its $11.8 billion market cap. So, while expected free cash flow is so high that it translates to a free cash flow yield of more than 22% (up to 27% by 2025), that number drops to the low-double-digits when using the enterprise value instead of the market cap (enterprise value is market cap plus net debt). In this case, I also added $500 million in pension-related liabilities.

Leo Nelissen (Based on analyst estimates)

{kind=link}

Having said that, the company is not divesting assets out of necessity. Its financial position isn't that bad.

- Despite having an elevated debt load, the company is generating so much EBITDA that its leverage ratio is expected to end this year at 3.2x (EBITDA).

- The company's free cash flow yield is above 20%. 4.9 points (4.9% yield) will go towards sustaining the dividend. The rest can be used for other purposes.

- Because of the high expected excess free cash flow, analysts expect the company to lower net debt to less than $12 billion by 2025 (2.3x EBITDA).

- The company has a BBB- credit rating (investment-grade).

- Viatris is improving its business with a strong pipeline, which means we should not expect EBITDA to weaken anytime soon. Analysts expect no EBITDA growth but consistent results close to $15.3 billion in annual EBITDA. On a longer-term basis, we'll see how well the company is able to transform itself into a faster-growing healthcare company with a focus on some key areas (like ophthalmology).

During its second-quarter earnings call, the company also noted investments in future growth drivers, including DTC investment in Tyrvaya, the Eye Care pipeline, and organic R&D.

The company also provided updates on its pipeline, including GA Depot, for which the FDA accepted an NDA with a PDUFA date of March 8, 2024. The company expects this product to improve patient experience.

The Botox biosimilar program is progressing well, with plans to file the IND by year-end.

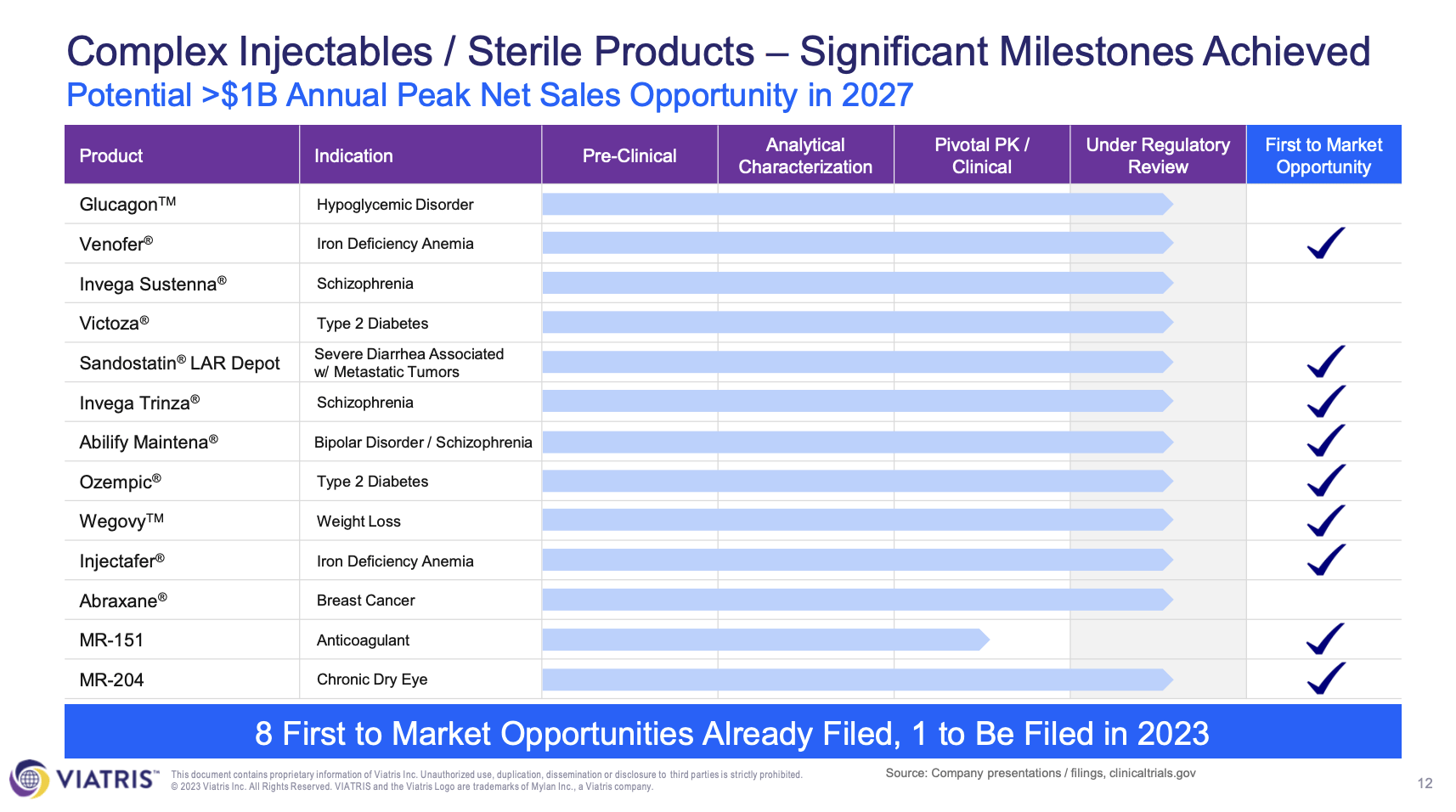

Other programs, such as Xulane Low Dose and Effexor for Generalized Anxiety Disorder, are on track, with expected NDA filings in the coming years. Complex injectable programs are also moving forward as planned.

Here's an overview of some of its pipeline products:

{kind=link}

Furthermore, the company is (indirectly) confirming my expectations that it doesn't fear financial instability by sticking to dividend growth - even before its transformation took shape.

On January 6, 2022, the company hiked its dividend by 9.1%. While I do not expect aggressive dividend growth for the next few years, there's a path to a much higher quarterly dividend in the future (thanks to high free cash flow and consistent debt reduction).

Valuation

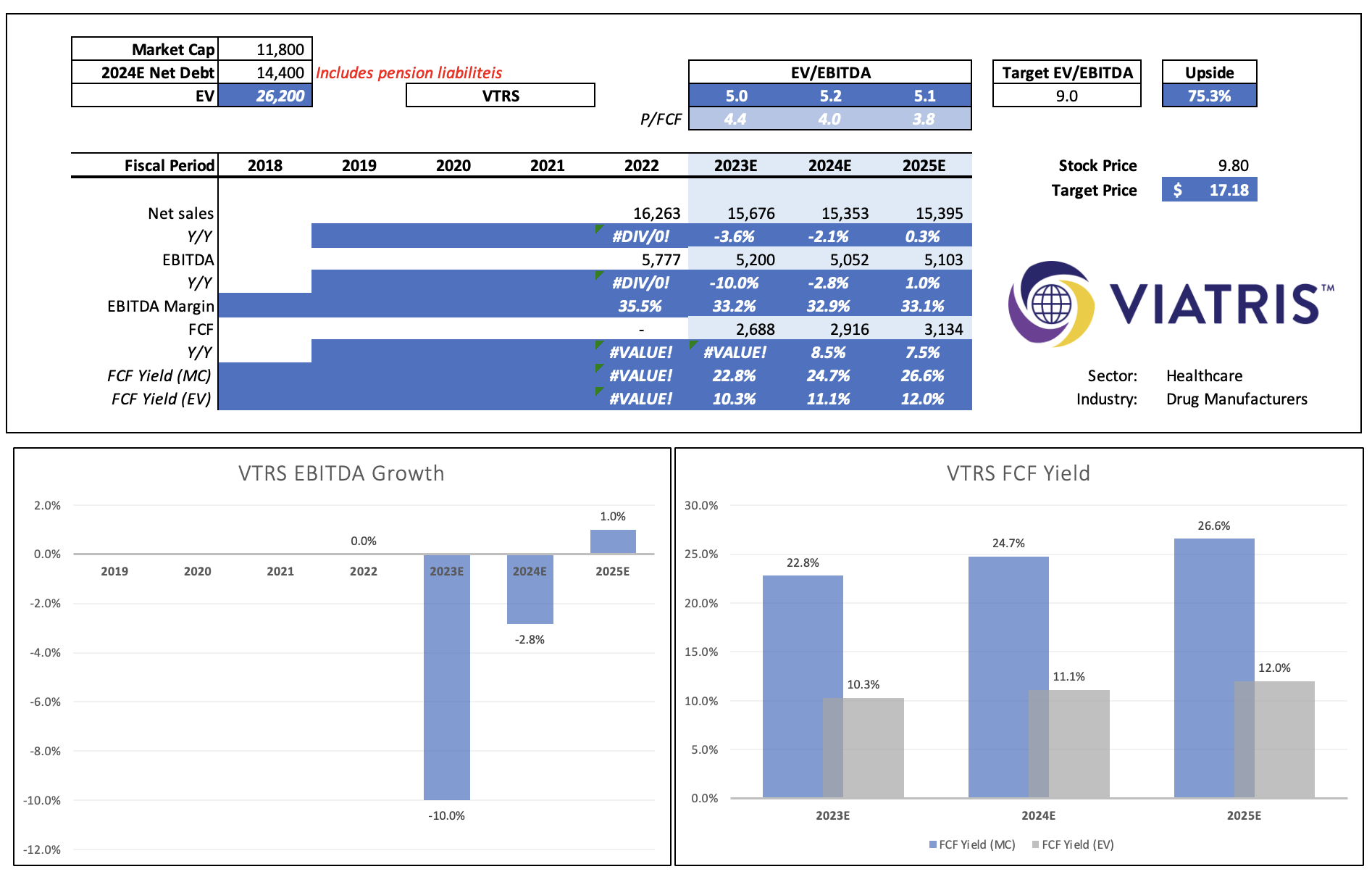

This is the tricky part. Essentially, VTRS is trading at just 5.0x 2023E EBITDA.

That number is expected to be fairly consistent due to the absence of expected EBITDA growth.

The company is trading at less than 4x 2025E free cash flow, which is one of the lowest multiples I've seen in a very long time. Not even coal companies are trading this low.

Leo Nelissen (Based on analyst estimates)

{kind=link}

Just like Organon, investors aren't willing to give a company dealing with debt reduction and a business restructuring. After all, who knows how successful Viatris is at reshaping its business over the next 5, 10, or 15 years?

What if growth turns into contraction and the company daily to deleverage its business?

However, as we discussed in this article, Viatris is not in bad shape. Its debt load is well-covered by free cash flow. Its juicy dividend is well-protected and there's plenty of room for debt reduction.

Nonetheless, the company paid close to $600 million in interest expenses last year on $2.8 billion in operating income (21%). Markets don't like that right now.

Over time, I believe that VTRS will trade close to 9x EBITDA, which would imply between 70% and 80% in potential capital gains. When adding dividends, I believe that VTRS has the potential to double.

However, this isn't a call to get people to pile into this company. It may take a while until this company gets the valuation it deserves. Lowering debt is a multi-year task. So is its restructuring process.

While I believe that this company will be successful, we're likely looking at 4-5 years until the company gets the valuation it deserves.

Takeaway

Viatris may not have been the most exciting stock in recent years, but it's certainly worth a closer look. Despite an elevated debt load, the company is making strategic progress, reporting strong revenues and impressive free cash flow.

Viatris is actively working on divestitures to reduce debt, and its strong pipeline indicates a promising future.

Trading at a low valuation compared to its EBITDA and free cash flow, Viatris has the potential for significant capital gains and offers a juicy dividend that seems well-protected.

While it may take some time for the market to fully recognize its value, patient investors could see substantial returns in the long run.

In summary, Viatris presents an opportunity for those willing to wait for its transformation and debt reduction efforts to pay off.

For further details see:

Why 5%-Yielding Viatris Hasn't Doubled Yet