RTX - Why Buy L3Harris As Shares Dip Lower

2023-05-12 07:00:00 ET

Summary

- Strong revenue growth contradicts the bearish L3Harris stock chart that started late last year.

- Aerojet Rocketdyne acquisition to add meaningfully to results down the road.

- This defence contractor is an attractive stock to hold at lower prices.

After peaking last Oct. 2022, aerospace and defence contractor L3Harris Technologies ( LHX ) continued its downtrend late last month. The company posted modest revenue growth. Its earnings failed to lift LHX stock out of the D+ valuation grade . Still rated a 'hold' from the quant ratings , at what price is L3Harris a buy?

L3Harris' Revenue Growth in the First Quarter of 2023

In Q1/2023, L3Harris posted revenue growing by 9% Y/Y to $4.47 billion . It earned $2.86 a share, annualizing the forward price-to-earnings of LHX stock to 16.36 times. This is fractionally higher than that of Lockheed Martin ( LMT ) and Raytheon ( RTX ), whose prospects appear stronger. Lockheed, for example, announced several billion-dollar contracts in recent days . Raytheon announced several nine- figure contract wins in April .

For its upcoming dividend, Raytheon raised its dividend by 7% to 59 cents a share . The yield of 2.45% is comparable to that of LHX stock, which yields 2.41%.

L3Harris expects its free cash flow improvement, which was $300 million, to strengthen. It already front-loaded its share repurchase commitment for the year. The downtrend in LHX stock suggests that markets lack the conviction to start a position at current valuations.

Speculating broadly, the ongoing Ukraine and Russia war may capitulate in the coming weeks. Should Ukraine launch a counter-offensive attack, markets may "sell on the news."

This is a mistake.

L3Harris said that geopolitical tensions remain elevated. It cited near-peer threats such as China as a reason to expect strong order volumes.

Countries worldwide committed to higher military spending over the next few years. The expansion of the L3Harris business through the Aerojet Rocketdyne acquisition may raise its prospects. Expect L3Harris to increase its revenue guidance as it logs more record orders and books higher revenue.

Opportunity

Aerojet Rocketdyne will cost $4.7 billion inclusive of debt. It furthers the company's focus on delivering critical capabilities to warfighters .

The acquisition represents around 10% of L3Harris's enterprise value. It is paying for the acquisition entirely in cash, which will not dilute shareholders. As always, mergers and acquisitions are opportunities to cut costs. L3Harris will shed non-core assets that do not add sufficiently to its business as a government or defense contractor.

Chief Executive Officer Chris Kubasik said that the company should find additional divestitures and M&A deals worth around $1 billion.

In the near term, markets will eventually recognize the company's healthy book-to-bill of 1.31 times , which includes winning over $1.5 billion from new prime space awards. The stock must first overcome the bearish downtrend as shown in this weekly chart . Market sentiment is neutral for defense contractors and bearish for L3Harris for no discernible reason.

Risks

Chief Financial Officer Michelle Turner said on the conference call that the company submitted over $6 billion in space proposals over the first half of Q1. While the business prospects expand from space exposure, investors want to see contract deals announced. Without this, the stock could re-test 2020 lows. That year, the stock traded in the $160 - $180 level. LHX stock closed recently at $187.27.

CFO Turner said to expect lower margins for the first half of the year. It will accelerate in the second half. Higher product deliveries, helped by easing supply chain constraints, will increase profit margins. Secondly, the fixed price backlog will dissipate steadily. However, lumpy aircraft revenue recognition from L3Harris's ISR business (global intelligence, surveillance, and reconnaissance) may add uncertainties to margins.

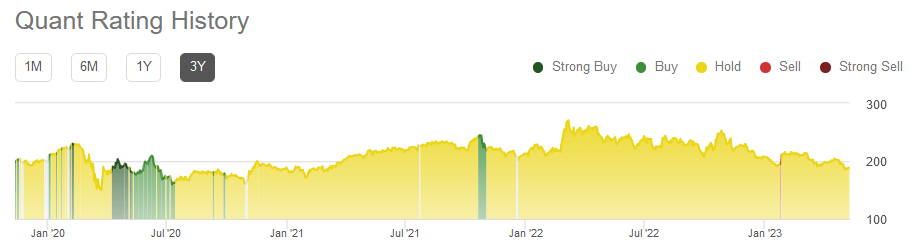

L3Harris does not have a strong quant rating history. It rarely earned a "buy" rating.

LHX Stock Rating History

{kind=link}

L3Harris has a good profitability grade, although it fell by one level from three months ago.

Seeking Alpha Premium

The stock has a weak value and growth score, which suggests the stock is not yet a buy at today's price.

Your Takeaway

Investors view L3Harris as a turnaround story. The firm needs to report a consistent increase in margins. Shareholders will have higher confidence in accumulating shares as the company navigates through the macro headwinds. More recently, supply chain disruptions are easing. This is stabilizing its attrition rates.

With the Aerojet Rocketdyne acquisition in progress, continuous improvements and cost cuts are expected. This is not a catalyst that will reverse the stock's downtrend. When margins expand, working capital improves, and L3Harris is more efficient in delivering the product, the stock will rebound.

L3Harris remains a stock that investors should consider accumulating on the dip.

For further details see:

Why Buy L3Harris As Shares Dip Lower