CA - Why Canadian National Railway Is The Only Railroad Able To Increase Buybacks

2023-11-26 21:02:09 ET

Summary

- Canadian National Railway Company's Q3 revenues decreased by 12% YoY, but the company expects flat to slightly negative growth going forward.

- The decrease in revenues was mainly due to lower fuel surcharge revenues resulting from lower fuel prices.

- Canadian National has the healthiest balance sheet in the industry and has been able to increase its share buyback program.

Introduction

In Q3, I bought more shares of Canadian National Railway Company ( CNI ). Canadian National, in fact, keeps on being the best available railroad if scrutinized with the criteria Warren Buffett uses to assess and invest in railroads (if you still haven't, please read the article " Learning From Buffett About Investing In Railroads: The BNSF Case Study").

During the past quarter and, more in general, throughout this whole year, railroads have not been an investors' favorite, having AI plays caught most of the attention. On one side, railroad weekly traffic has lagged 2022 all this year until September, when traffic started picking up speed once

again and increased YoY. On the other side, those who know the industry also knew we would have seen unfavorable fuel lag with an impact on fuel surcharges and, as a direct consequence, on revenues.

In the meantime, fears of a slowing economy coupled with deceleration in manufacturing activity have caused weakness in railroad stocks. Moreover, most railroads have found themselves at risk of over-leveraging their balance sheet in case of massive buybacks and thus had to cut on this type of shareholder return.

Why I own Canadian National

On Seeking Alpha, I have shared several articles where I shared my research and what led me to choose Canadian National as my largest railroad by far. As a disclaimer, I also recently started a small position in Canadian Pacific ( CP ) and I also have a very tiny bit of Union Pacific ( UNP ).

Before we dive into the numbers, please keep in mind all financial data are reported as CAD, unless otherwise stated.

Once the company released its Q3 earnings report, there were several weak numbers to be found.

- revenues of $4billion decreased 12% YoY. At the same time, the 9M comparison is down only 2%.

- operating income of $1.5 billion decreased even more: -21% YoY. For the first 9 months, the decrease is only 3%.

- operating ratio, of course, increased 4.8 percentage points to 62%, something Canadian National is not accustomed to. YtD, operating ratio is reported to be at 61.3%, still not good enough (we need it to be below 60%).

- diluted EPS decreased 21% YoY.

- free cash flow decreased by $775 million to only $581 million (-57% YoY). YtD, free cash flow is down 22%.

- operating performance deteriorated in every metric (injury frequency rate, accident rate, through dwell, through network train speed) apart from fuel efficiency, which came in at 0.832 (US gallons of locomotive fuel consumed per 1,000 gross ton miles), improving 1% YoY. YTD, however, fuel efficiency has seen an overall deterioration of 2%.

- revenue ton miles were 55,640 million, down 5% YoY.

However, as we have said, Q3 will probably turn out to be the worst quarter of this fiscal year, as Canadian National's management said during the last earnings call . Since September, weekly rail traffic has increased once again and it has been above 2022 levels. This is why Canadian National's outlook expects flat to slightly negative growth instead of expecting a -4/5% one. If this holiday season goes better than expected, intermodal may lead the way and drive revenues a little above what was previously anticipated.

But let's dig a bit deeper inside the report.

First of all: why did revenues decrease so much? The decrease of $526 million was mainly due to lower fuel surcharge revenues resulting from lower fuel prices. In fact, fuel surcharge revenues decreased by $373 million just in Q3. YtD, the decrease is less meaningful and it is $254 million. So the real decrease linked to freight was $153 million.

If we look at Canadian National's revenue breakdown, we see that only two categories performed well: grain and fertilizers up 16% YoY to $880 million and automotive up 14% to $237 million. Intermodal was down big: from $1,340 million to only $880 (-34%), as a result of a two-week port strike on the West Coast. We then have to distinguish domestic intermodal from international intermodal. The former picked up speed during the quarter thanks to the Falcon service between Canada, Detroit, and Mexico. The latter kept on being weak.

Forest products were down 15% because of a decrease in new home construction and petroleum and chemicals were down 11% because of tough comparables.

Considering many were expecting the economy to slow down completely as a result of high interest rates, I see results showing far more resilience even in an industry that feels directly and immediately the impact of economic slowdowns. Moreover, plastic & chemicals, which is usually an indicator of industrial production, sequentially strengthened in the quarter.

Now, let's look at what I have grown accustomed to calling the "Buffett-metrics". First and foremost, since railroads are capital-intensive businesses, Mr. Buffett focuses on earning power. That is, how well interest expense is covered by pre-tax earnings. Now, YtD interest expense has been $523 million. Pre-tax earnings amount to $4.62 billion. This is a pre-tax earnings/interest expense ratio of 8.8 which is quite good.

As far as efficiency goes, we have already spoken about a deterioration of the operating ratio, but an improvement in fuel efficiency.

Let's look at how the company used its capital.

First of all, YtD, the company has spent on capex $2.25 billion. This is necessary to keep on renewing the company's fleets as well as its tracks.

Most importantly, we have to look at the company's ROIC (return on invested capital). For the quarter ended September 30th, Canadian National's ROIC was 10% . The company has performed better in the past, with a ROIC of 15-16%. But we will have to wait for FY results to assess this metric better. In any case, a 10% is not exceptional, but it is acceptable and it is well above the current yield of bonds, which sets the risk-free rate of returns investors can expect.

However, Canadian National has been able to distinguish itself from the crowd this year because it can benefit from the healthiest balance sheet in the industry. While all its peers had to cut on buybacks, Canadian National has been able to actually increase its program from the previous budget of $4 billion to $4.5 billion to be spent through January 31st, 2024.

This is doubly accretive: it supports the stock during weakness and it makes the company buy its shares during a low. Other railroads bought heavily during peaks, creating further damage to their balance sheets.

During the conference call, Canadian National's CEO Stacy Robinson also explained a major change in the structure of the company. Ed Harris (the COO) is retiring for the 5th time and he is handing over his job to two people: Derek Taylor, who will be the Chief Field Operating Officer and Pat Whitehead, who will be the Chief Network Operating Officer. Both of them are quite experienced and Miss Robinson plans on having two people instead of Mr. Harris to focus, on one side, on daily execution and, on the other, on longer-term plans.

Valuation and Conclusion

While investors don't flock to railroads, it is the right moment to consider them as a very easy pick for the long term. The current report has not shaken my conviction about Canadian National. Actually, it made me more convinced the company, as long as it trades below $120, is in value territory as I have previously explained. Here is what I am expecting from the company, based on how its management is delivering.

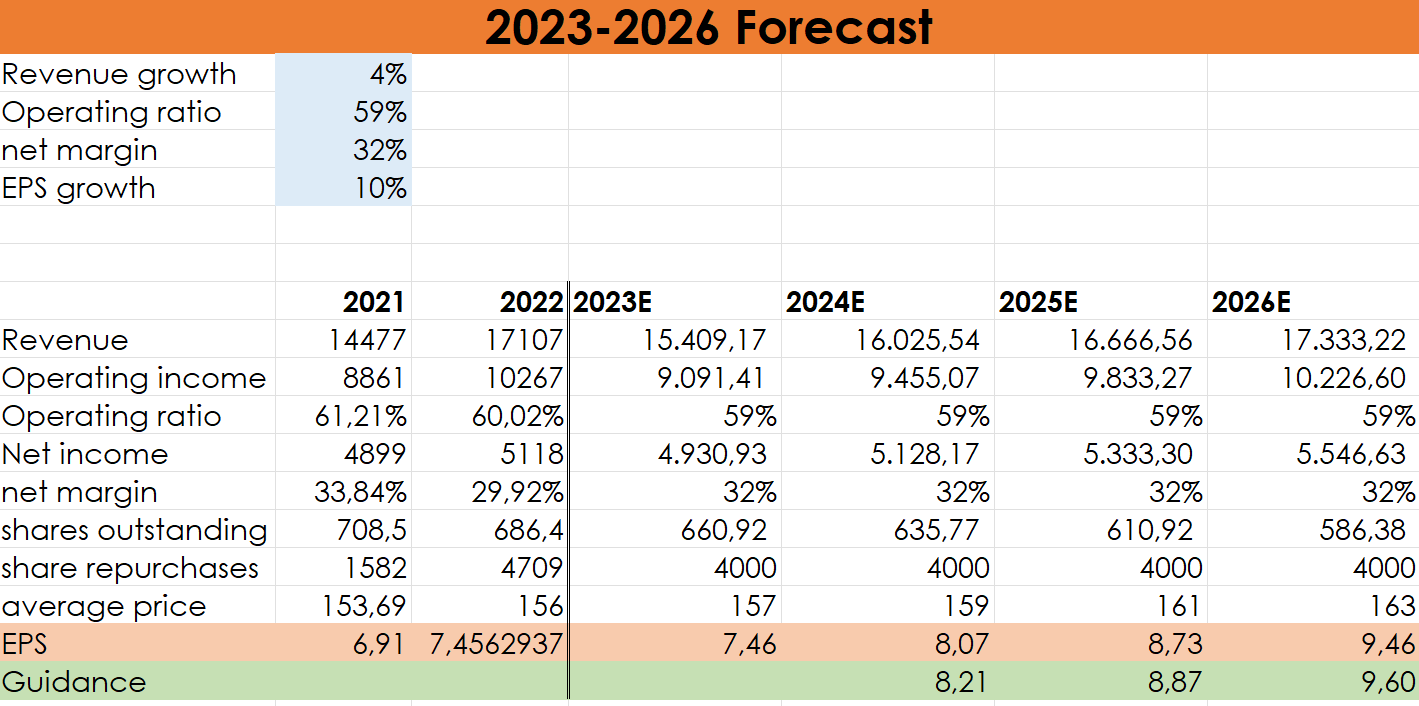

{kind=link}

Please remember all data are in CAD. I expect almost flat EPS growth and then forecast an EPS growth lower than the overall guidance the company has given. Of course, with Canadian National having already increased by $500 million its buybacks, my forecast is now even more conservative than it was a month ago. But this is helpful because, according to this model, Canadian National is trading at its highest at a fwd 2024 PE of 19.5 and a fwd 2026 PE of 16.6. There is however an increased chance these multiples are actually lower. For a company with a business and efficient operating history as Canadian National, these are multiples that don't price the company with a premium compared to the general market, since the S&P500 is trading at an expected fwd 2024 PE of 20.5.

This is why I recently took advantage of the situation and increased my stake in Canadian National, making it 8% of my portfolio.

For further details see:

Why Canadian National Railway Is The Only Railroad Able To Increase Buybacks