CA - Why I Am Selling Medical Properties Trust And Hess Midstream To Buy W. P. Carey

2024-01-08 06:18:48 ET

Summary

- I am adjusting my portfolio to reduce risk and am considering investing in W. P. Carey.

- WPC experienced a stock price rebound after a spinoff and dividend cut, and I believe the company will recover.

- I am cautious about Hess Midstream and Medical Properties Trust due to uncertainties and financial issues.

- W. P. Carey is likely to recover its "SWAN" status and the premium valuation that goes with it.

- Management will likely return the company to the growth pathway. If that happens, the recovery potential of the stock far exceeds any return when the stock was a "SWAN" (recently).

I have always given investors and newsletter subscribers time to get in before I do. I never wanted to already be there without having first given a "heads-up" on where I am heading with my own money. Similarly, I had given a warning on higher risk for Medical Properties Trust ( MPW ) and am not sure about Hess Midstream ( HESM ) with the latest news (the acquisition of Hess ( HES ) by Chevron ( CVX )). Since I am a retiree, I am adjusting my personal risk and moving towards W. P. Carey ( WPC ) a company that is likely to recover back to the good old days. Risk takers may either want all three or remain with both Hess Midstream and Medical Properties Trust.

W. P. Carey Situation

W.P. Carey was a "SWAN or Sleep well at night stock". In my view it still is. But then again, I have a portfolio full of "disappointments" that have come back from the disappointment to return to market favor.

W. P. Carey was long held in very high regard by a lot of income investors. However, every great company sooner or later gets to "the end of the road" because any company can only grow so much or predictably produce an income stream that grows for a certain length of time.

For me, the fact that Carey did this for so long before the disappointment means that management is likely to go back to its winning ways. But if it ever gets priced to perfection in the future, then I will likely shrink my position knowing that at some point there is likely to be another disappointment for investors. Nothing lasts forever.

But in the meantime:

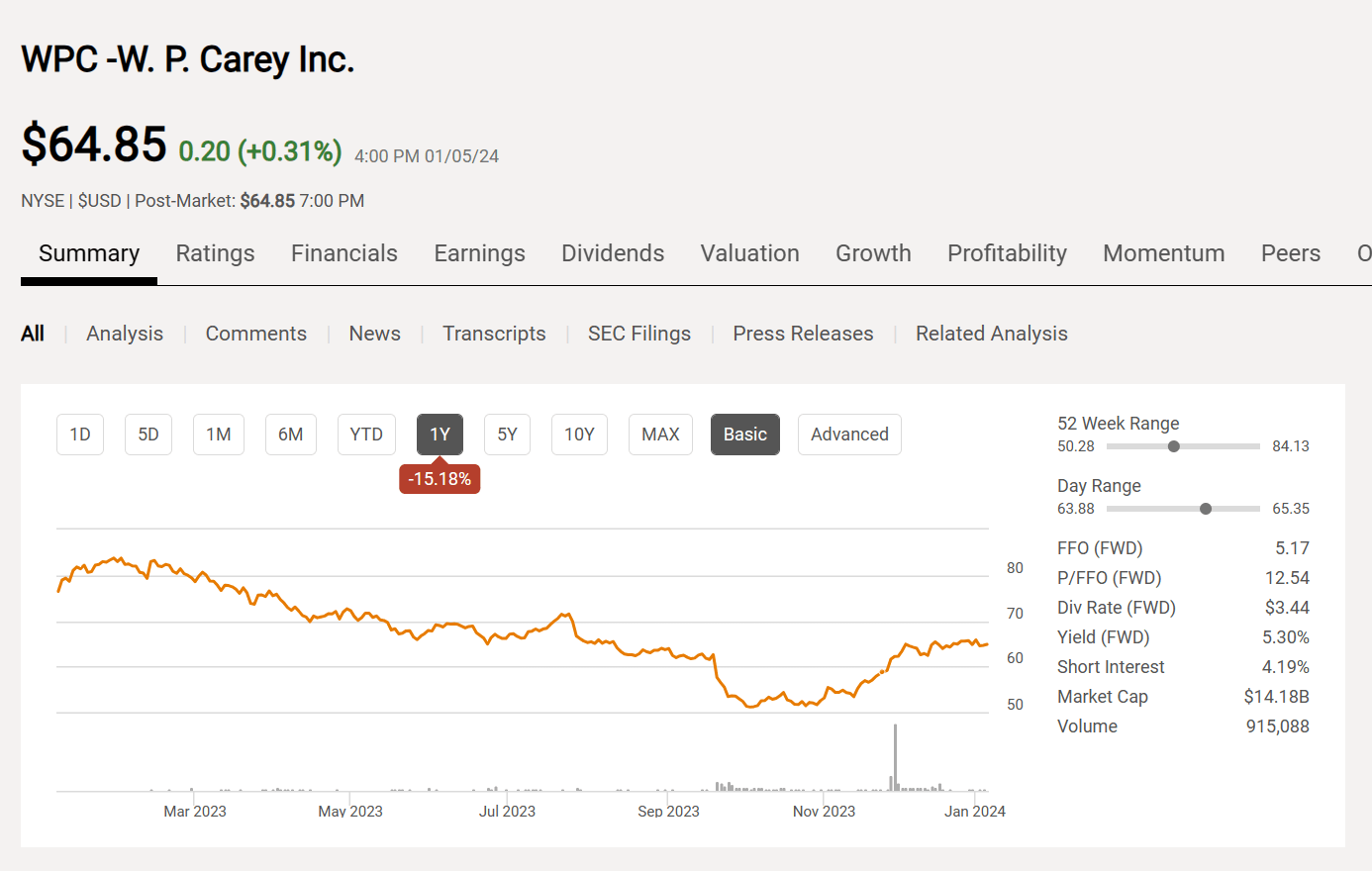

W. P. Carey Common Stock Price History And Key Valuation Measures (Seeking Alpha Website January 7, 2024)

{kind=link}

The stock price has clearly rebounded from the announcement about the spinoff and the dividend cut. In late September 2023, management announced a plan to spin off what would now be considered noncore properties. The key for investors is that at the same time management strongly implied a dividend cut of an unspecified amount was on the way.

Readers can see the market reaction above. The stock was already under pressure from rising interest rates. It then headed lower on the announcement from the $80 range shown on the chart to nearly $50.

But as I noted back then , management is likely to try its best to return to the previous dividend levels. While that may take some time, a stock price in the $50's combined with a future yield based upon that price is a much better proposition than it was with the future yield based on the previous stock price that was far higher. In fact, I may never sell even if there is a hiccup based upon a far higher level in the future.

This management is still committed to growth. The portfolio is still regarded by many as top notch. The only thing that happened was the spinoff followed by a lower dividend. Note that the lower dividend and the lower stock price combine for a 5% yield. This is a better yield than was the case in recent history before all the interest rate rises by the Federal Reserve.

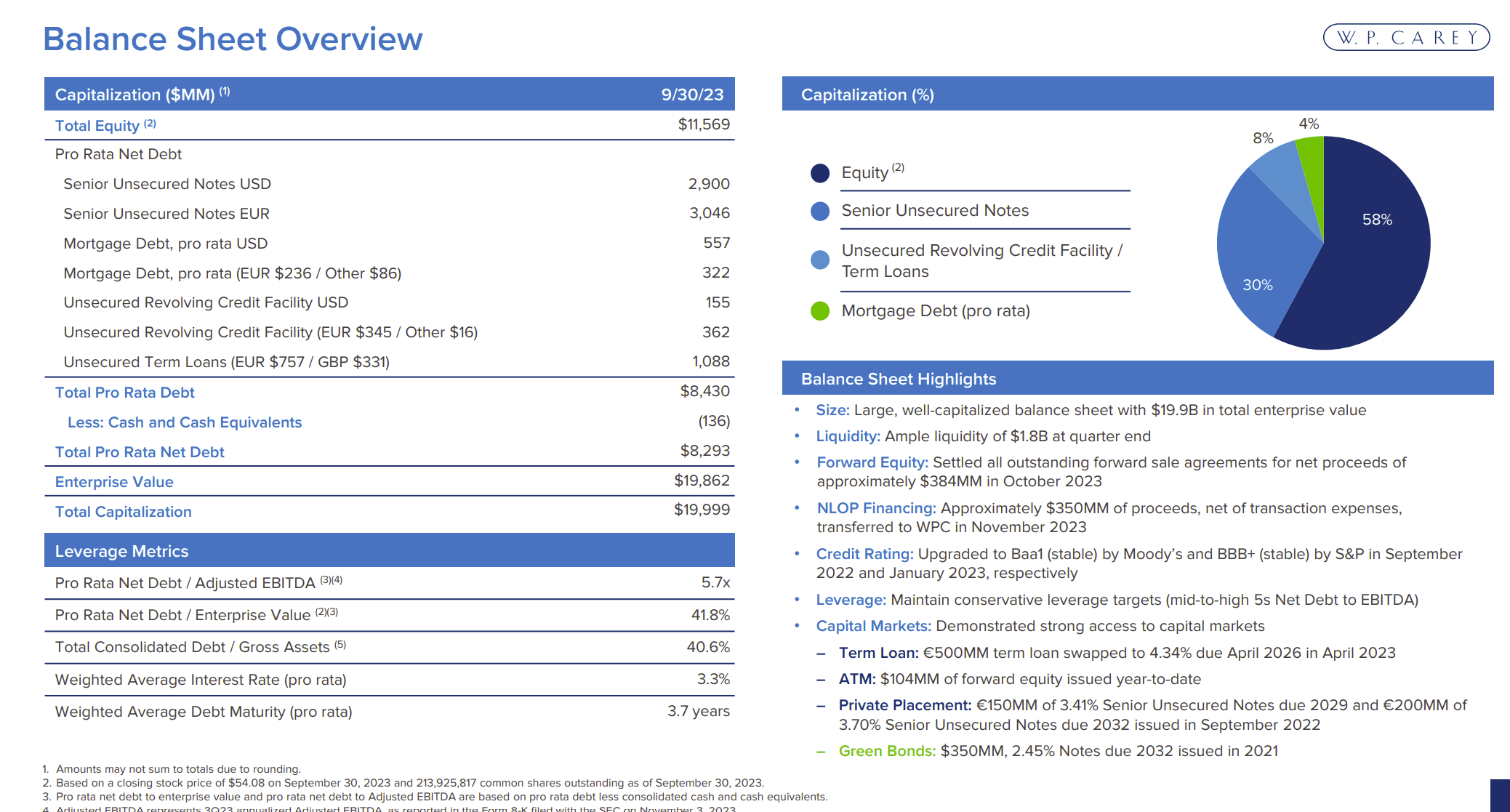

W.P. Carey Summary Business Statistics (W. P. Carey Investor Presentation Third Quarter 2023)

{kind=link}

W. P. Carey is still investment grade. Management has shown that they can handle a larger portfolio as the spinoff shrunk the core holdings. There is every chance that management will build the business back to where it was and probably go for a larger more profitable business in the future.

Mr. Market was worried that interest rates would never come down until the Federal Reserve announced the inevitable. As I noted in the past, inflation was under control. Any resurgence would be appropriately met. But there is no sign of inflation problems (resurgence) on the horizon. Hence the announcement about possible rate cuts has led to an industry-wide stock price recovery.

This company has long been regarded as having some of the better measures as well as a portfolio in the business. It does have a debt to refinance. But any business including this one, will deal with inflation. Management does not just "sit there and take it". The recovery ride could be bumpy. But a recovery with a management of this quality is likely.

Therefore, I think that the dividend will be headed higher sooner rather than later.

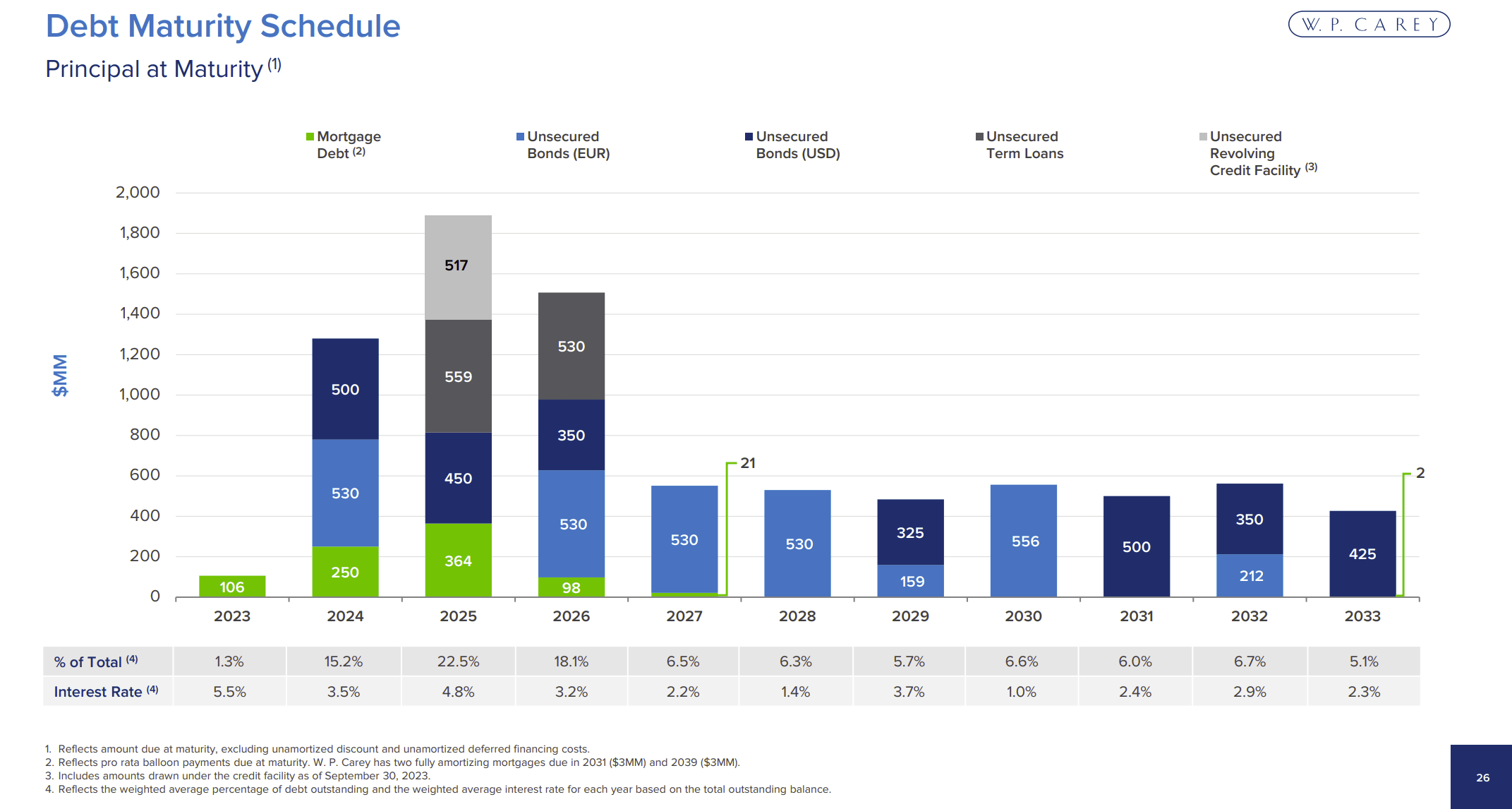

W. P. Carey Debt Due Schedule (W. P. Carey Corporate Presentation Third Quarter 2023)

{kind=link}

All of a sudden, the Federal Reserve announcement has made the debt due ((soon)) schedule a lot less concerning than it was. Now this could hold back the stock price recovery somewhat depending on how this goes. Then again, management was going to have roughly $1 billion in cash knowing that all that debt was coming due.

Any deals that management does will likely be done with interest rates at the current levels along with inflation coverage. Managements like this one were not "born yesterday". Therefore, they cover as many reasonable contingencies as they can before those issues happen.

Furthermore, there is some expected turnover (lease renewals), some sales, and some purchases. All that combines to take the sting out of any refinances.

To summarize, the continuing stock price recovery (even if bumpy), far exceeds the return when this stock was regarded as a "SWAN" stock.

Hess Midstream

Hess Midstream has long been one of those companies that really was not undervalued. But the investment did well anyway. Hess is investment grade and the midstream worked well with the parent company to produce above-average returns.

But now, Hess will be acquired by Chevron. The Bakken, where the midstream operates is unlikely to be the priority it was for Hess. Hess used the Bakken cash flow to fund the Guyana Partnership with Exxon Mobil ( XOM ).

This uncertainty leads me to want to watch what happens from the sidelines. Personally, I want to see how well the new parent company treats the midstream before I commit to a long-term investment in the future. I have had more than a few less-than-stellar experiences to want to be cautious about the coming merger.

Medical Properties Trust

The issue here is that management has issued an update on the Steward situation. This is a material change in Steward's rickety financial condition to the point that now I am willing to " call it a day" and move on. I still suspect that the company will recover from the current situation. However, I now suspect that the recovery will take much longer than I originally anticipated.

I still think that the company will survive the current announcement. Management has a good record with "customers" that run into trouble. However, Steward is a significant enough customer to affect results for at least another year or two.

If Steward needs to be replaced, that would be a big job. The stock price in the current environment would probably not go anywhere for at least a couple of years.

Like Hess Midstream, the risk for me, as someone now retired, has reached past my level of comfort. Therefore, I am adjusting my portfolio to suit my risk level. Since I like the chances of a company recovering from current price levels, risk-taking investors may well decide to either invest or hold their shares while following the company closely.

Summary

I am adjusting my investments to suit my retired status and my risk comfort levels at the current time. W. P. Carey's management appeals to me as a very capable management that has had a bad year. This generally happens to any management sooner or later. But good managements have a lot less bad years (and those bad years turn out to be less significant as well) than mediocre or poor management.

I think that management will again acquire that SWAN label and the premium pricing that goes with it. I also think that management will get back on the growth track.

On the other hand, it is time for me to leave Hess Midstream and Medical Properties Trust for something I am much more comfortable with. I would not fault those who can tolerate the risk for holding on as both companies have done decently for shareholders in the past and they may yet deliver a better future than I anticipate right now.

For further details see:

Why I Am Selling Medical Properties Trust And Hess Midstream To Buy W. P. Carey