VZ - Why I'm Buying 30% Undervalued And 7% Yielding Verizon Heading Into 2024

2023-12-17 03:24:54 ET

Summary

- In 2023, the dominant investment strategies revolved around the Magnificent 7, driven by the AI narrative and investors opting for money markets for their yields.

- In this market climate, Verizon Communications Inc. has notably underperformed, but it remains a fundamentally strong business offering nearly a 7% dividend yield.

- Verizon posted strong Q3 results, and while substantial growth might not be expected ahead, as bond yields decline, investors chasing yield are likely to return.

- Today, Verizon stock is trading around 30% undervalued to its fair value and presents potentially 14%+ returns as a reversion to the mean play.

As we approach the end of 2023, it's clear this year has been quite a rollercoaster. It surprised many, myself included, with how the market performed and the expectations it set. While the SPY showed a 22.7% return, FED's 11 consecutive rate hikes, concerns about a "hard landing", and a pullback in consumer spending meant the more cyclical companies have been punished and equal weight index ( RSP ) only delivered a 10.7% return. It even dipped into the negative briefly a few weeks ago before the November and December stock rally picked up.

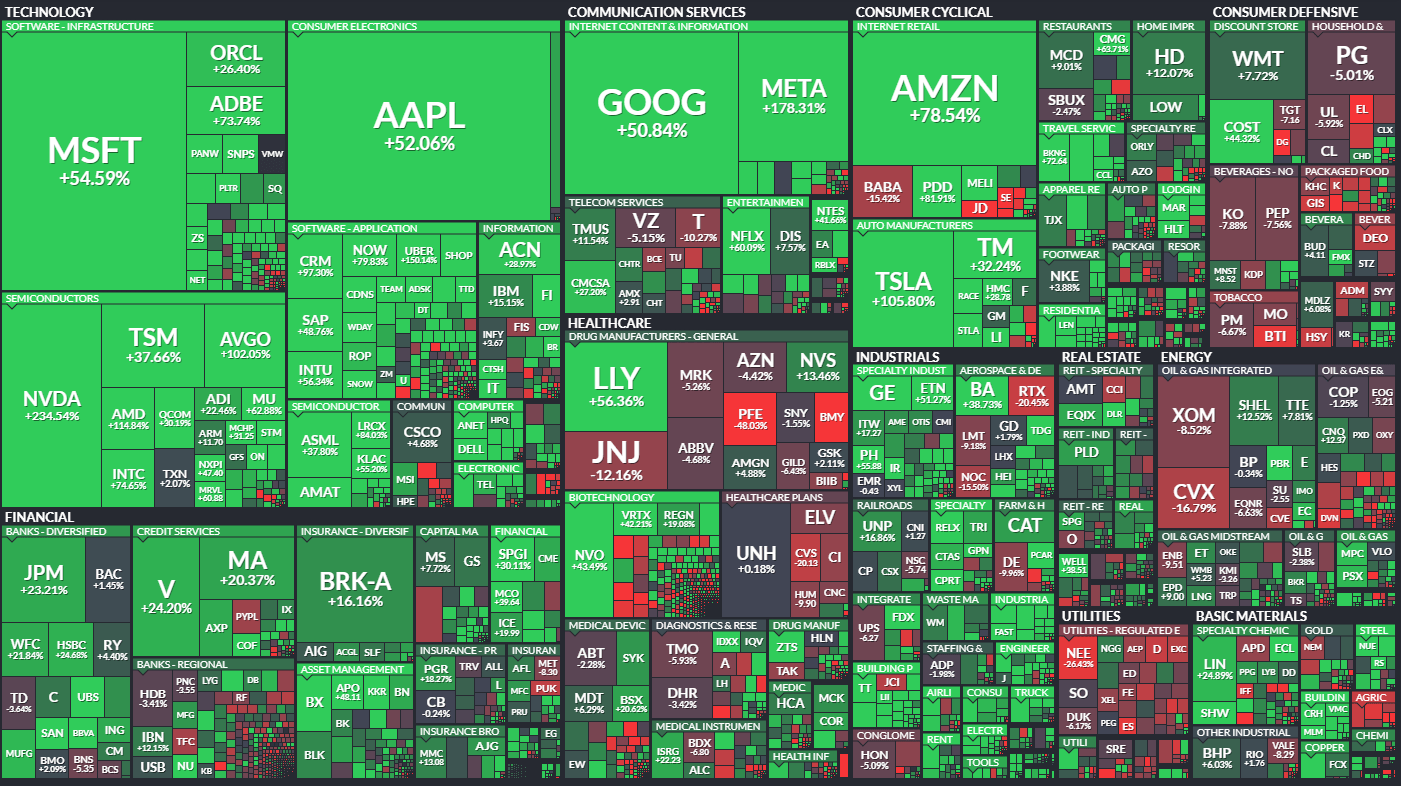

One standout of the year has been the AI narrative, giving a significant boost to the "Magnificent 7" companies: Microsoft ( MSFT ), Apple ( AAPL ), Nvidia ( NVDA ), Google ( GOOGL ), Amazon ( AMZN ), Meta ( META ), and Tesla ( TSLA ). Take a peek at the sea of green among these Magnificent 7 and a few other companies in the chart below. You'll see for yourself the unequal returns this year.

{kind=link}

It got me thinking that while it's not unusual for a handful of top-notch businesses to lead the returns of indices, I'm personally not counting on the Magnificent 7 to pull off the same stellar performance next year.

The reason for this being that the upcoming year is expected to be defined by the Fed's pivot , possibly involving up to 3 rate cuts, potentially witnessing a GDP slowdown and a mild recession. These factors might exert a braking effect on growth stocks.

It's no surprise that as bond yields rise and money markets become an appealing alternative for income, offering 5%+ yields with minimal risk, companies like Verizon Communications Inc. ( VZ ) underperform. Their high yields are no longer the exclusive choice for funding retirement or income-oriented goals.

This scenario is precisely what happened with VZ during peak pessimism, resulting in a nearly 25% year-to-date decrease in its stock value. Although the stock has rebounded since then, it's still down by 6.9% for the year, excluding dividends.

It's crucial to remember that the market swings like a pendulum, swinging between buying frenzies and periods of extreme pessimism, often diverging from the actual reality and fundamentals of sound businesses.

So, what happens when bond yields fall again and yields become scarce?

You guessed it.

The income-seeking investors and those on the hunt for yield return to quality high-yielding and dividend growth stocks. With increased demand, stock prices rise—a perfect opportunity to capitalize on investments, provided one avoids getting swayed by market sentiments and instead utilizes peak pessimism to invest in strong businesses.

Verizon is, in my opinion, a robust business with strong fundamentals, albeit highly leveraged, which is common among telecom companies. Despite this, VZ maintains an A- rating from Fitch and currently yields 6.9%, with a safe payout ratio. This makes it an ideal choice for yield-hungry buyers.

Solid Results & Paying Down Debt

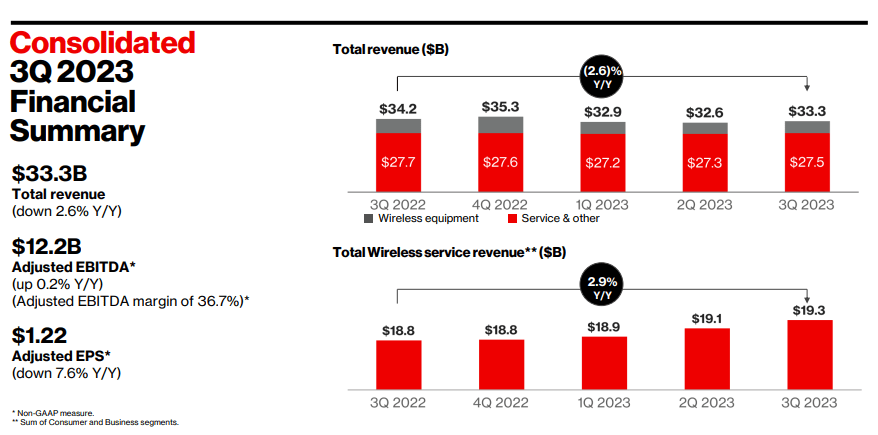

Verizon's Q3 report seems pretty solid, especially given the industry's challenges, particularly the slowdown in equipment revenue due to customers delaying smartphone upgrades in tougher economic times. Despite this, Verizon still managed to report $33.3 billion in revenue, marking a 2.6% YoY decrease but aligning with expectations.

The standout highlight from the earnings was the 2.9% year-over-year growth in wireless service revenue, attributed to the company's efforts in expanding and strengthening customer relationships. This revenue boost significantly contributed to an adjusted EBITDA of $12.2 billion for the quarter, surpassing both last year's Q3 and the sequential quarter.

Consequently, this led to an EPS of $1.22, reflecting a 7.6% YoY decrease but surpassing analysts' expectations by $0.04.

{kind=link}

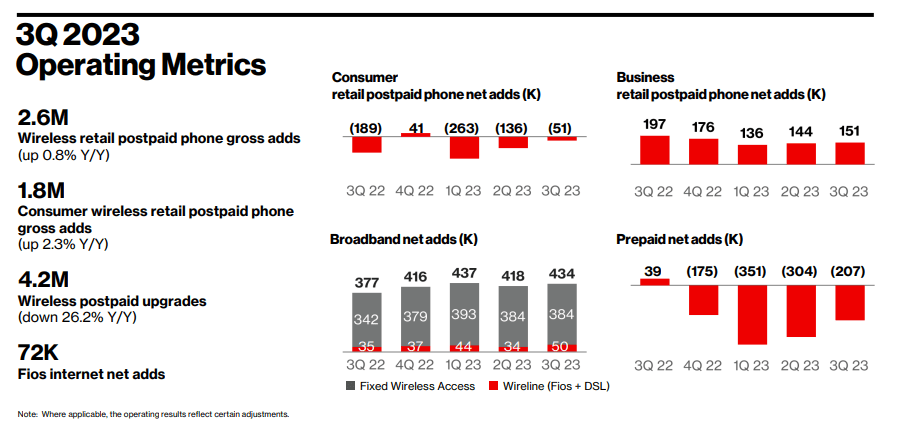

During the quarter, Verizon excelled in its crucial growth sectors: mobility, broadband, and private networks, leveraging its network superiority, scale, and technological advancements.

In Consumer mobility, Verizon saw improvements in postpaid phone net adds both sequentially and year-over-year. Instead of aggressive promotional tactics, Verizon prioritizes offering consumers flexibility in choosing how they utilize their products and services. This approach—focused on segmentation and financial prudence—is yielding positive results, evident in the growth of postpaid phone gross adds and reduced promotional costs.

Within Business Mobility, Verizon achieved 151,000 phone net adds, marking the ninth consecutive quarter surpassing 125,000. Businesses and governments increasingly prioritize Verizon's reliable connectivity. Notably, across mobility, postpaid phone net adds reached 100,000, a significant increase from the 8,000 last year.

The Broadband sector continued its strong performance, securing over 400,000 new subscribers for the fourth consecutive quarter. Q3 concluded with 10.3 million broadband subscribers, showcasing a substantial increase of 1.7 million subscribers—a 21% surge—compared to a year ago. Fixed wireless access remains crucial to bolstering this pivotal area.

Regarding the private network, Verizon earned J.D. Power Awards across all 6 U.S. regions, securing the Most Award for Wireless Network Quality for the 31st consecutive time this quarter.

{kind=link}

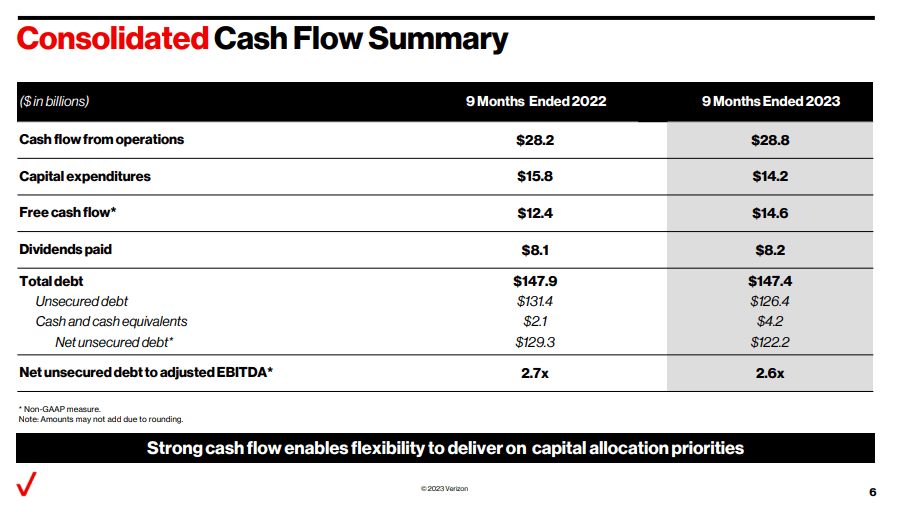

Verizon generated $14.6 billion in free cash flow in the quarter, showcasing robust performance that provides flexibility and supports the company's capital allocation priorities. During Q3, Verizon successfully executed a $2.6 billion debt tender, with a majority of the tendered debt being floating rate.

By the end of the quarter, Verizon's net unsecured debt stood at $122.2 billion, marking a $4.3 billion improvement from the second quarter and a $7.1 billion decrease year-over-year. The company closed the quarter with $4.2 billion in cash reserves. As of the end of the third quarter, the net unsecured debt to consolidated adjusted EBITDA ratio was at 2.6x, exhibiting a 0.1 turn improvement compared to the previous year.

7% Yield with Safe Payout Ratio

The primary argument often cited by investors discussing telecom companies as potential investments for their yield is the concern about high leverage, which could jeopardize the sustainability of their dividends .

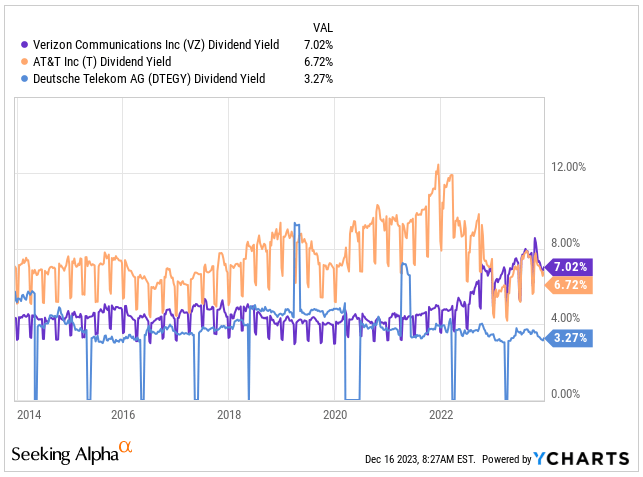

Indeed, Verizon carries $143 billion in net debt on its balance sheet, surpassing AT&T's ( T ) $132 billion and even exceeding Deutsche Telekom ( DTEGY ), the majority owner of T-Mobile ( TMUS ), with $97 billion on their balance sheet. This naturally results in a high interest expense, which hit a record high for Verizon in 2023, reaching $5.03 billion. However, to be candid, this has not proven to be a significant issue for the company, although it does present a slight drag to their EPS.

To present a different perspective, let's delve into the cash flow from operating activities on a year-to-date basis, which stood at $28.8 billion, with a CAPEX of $14.2 billion, resulting in free cash flow of $14.6 billion.

Looking ahead to the full fiscal 2023, the company has revised its free cash flow guidance upward by $1 billion, now expecting it to reach around $18 billion.

Considering the anticipated dividends paid for the year, estimated at around $11 billion, this places us at a very comfortable payout ratio of 61.1% based on the projected 2023 free cash flow.

This indicates that even without growth, Verizon can comfortably continue increasing dividends. Furthermore, if the company were to distribute its entire free cash flow as dividends, investors would enjoy an 11.5% dividend yield without risking the company's operations.

{kind=link}

Verizon currently offers the most appealing dividend compared to AT&T and Deutsche Telekom based on the trailing-twelve-month yield.

I bring up Deutsche Telekom because European investors aren't subjected to withholding tax on their dividends at present. While their 3.27% dividend might not match Verizon's allure, it's still worth considering due to the company's stronger growth prospects, expecting a consistent 10% dividend growth for the next four years.

I've written an article discussing Deutsche Telekom's appeal, which you can read by accessing it here.

Dividend Yield (Seeking Alpha)

{kind=link}

Verizon has been consistently upping its dividend over the last 14 years, marking a total increase of 40% or approximately 2.85% annually. Though not the speediest growth, it's a reliable one for investors. The most recent hike occurred earlier this year, showing a 1.9% increase.

As of now, the dividend per share stands at $0.665.

{kind=link}

It's essential to note that due to their heavily leveraged business models and substantial interest expenses, telecom companies seldom engage in share buybacks, rather the opposite for M&A.

This remains the case with Verizon, where their outstanding shares have remained virtually unchanged in recent years.

30% Undervalued Heading Into 2024

The stock's underperformance over the past year and the overall decline in Verizon's stock price from its peak at $62.22 back in 2019 have resulted in the company being traded at an incredibly low valuation .

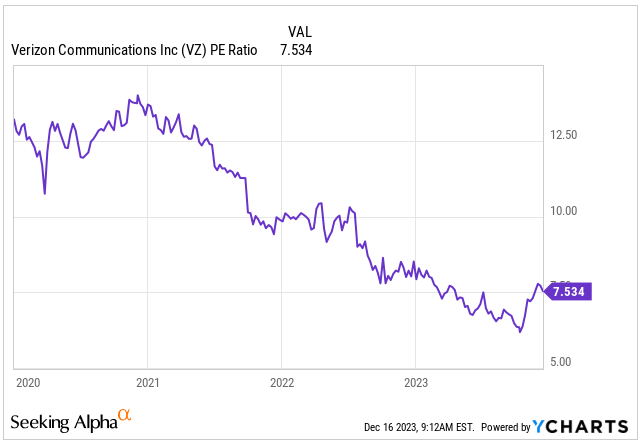

Currently, the stock is trading at a blended PE valuation of 7.53x its expected 2023 earnings of $4.7.

Comparing this to the average of around 10.5x earnings over the past four years, it's evident that the stock's fair value over this period should hover around $49.

{kind=link}

I don't anticipate a swift return to fair value, especially considering Verizon's projected 9.4% EPS decline for fiscal 2023. Any recovery isn't likely before 2025.

Even when recovery begins, the estimated growth is modest, averaging around 2% to 3% annually. However, this investment opportunity isn't solely about growth; it's more about the stock trading at an exceptionally low valuation and its eventual return to the mean.

My projection suggests a return to the 10.5x PE ratio by 2026. This implies annual returns of 7%. Factoring in the 7% dividend, a reasonable expectation points to close to 14% total returns, which, in my view, would outperform the market.

Nonetheless, if the recovery timeline extends beyond expectations, it could continue to weigh on the stock. Yet, holding a strong business yielding 7% is always a wise move.

| Fiscal Year |

| 2023 |

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| Revenue (b) |

| $ 133.5 |

| $ 135.5 |

| $ 137.4 |

| $ 140.4 |

| $ 142.0 |

| Revenue Growth |

| -2.5% |

| 1.5% |

| 1.4% |

| 2.2% |

| 1.1% |

| EPS |

| $ 4.7 |

| $ 4.6 |

| $ 4.7 |

| $ 4.9 |

| $ 5.0 |

| EPS Growth |

| -9.4% |

| -1.7% |

| 1.5% |

| 5.1% |

| 1.8% |

| Forward PE |

| 8.0 |

| 9.0 |

| 10.0 |

| 10.5 |

| 10.5 |

| Stock Price |

| $ 38 |

| $ 41 |

| $ 47 |

| $ 52 |

| $ 53 |

Takeaway

When inflation and interest rates climb, investors usually shy away from heavily leveraged businesses, often opting to stay out of the market while money markets provide decent returns minus the risk to their capital. This cautious approach isn't limited to Verizon alone; it also affects various sectors like REITs and Utility companies, including fundamentally strong companies such as Realty Income ( O ) and NextEra Energy ( NEE ), just to name a few.

However, the landscape is changing. Bond yields are coming down, and it's anticipated that the Fed will cut rates 2024. Once this shift occurs, there's an expectation that demand for high-yield companies will reignite as investors chasing yield will return.

Verizon stands as a robust business, offering a well-covered 7% dividend yield. Additionally, the management is focused on reducing a portion of its unsecured debt to navigate high interest rates.

Being undervalued at least 30%, I believe the current market presents a promising opportunity to invest in what I see as a fundamentally strong business.

For further details see:

Why I'm Buying 30% Undervalued And 7% Yielding Verizon Heading Into 2024