MSFT - Why I'm Not That Concerned About The Broadcom VMware Deal Breaking

Summary

- Chip maker Broadcom Inc. is buying server software provider VMware, Inc.

- Tech deals are getting scrutinized intensely all over the globe.

- This deal won't be an exception to that rule, and it likely takes many more months to close or fail.

- Yet, the spread is very rich and the downside seems mitigated.

VMware, Inc. ( VMW ) is being acquired by Broadcom Inc. ( AVGO ) for $142.50 per share in cash or 0.252 shares of Broadcom. Broadcom is trading at ~$600 per share, which translates into a theoretical $152 per share. VMware is trading at $117 per share. As I write this, there's roughly 24% upside to the deal closing and the cash consideration. In share consideration, there is ~29% of upside. Most likely, investors will receive a mix, as everyone will choose one or the other, and everyone gets prorated.

Either way, the spread is very wide on a merger arb deal announced back in May 26, 2022. The target is a $50 billion market cap company. Admittedly, this is a big deal, and these can take a long time. They also (rightfully) attract a lot of regulatory scrutiny). Various regulators are taking a close look, and the latest news came yesterday :

Antitrust regulators in the U.S., Europe, UK and China are analyzing whether Broadcom's ((AVGO)) chips could potentially block hardware competitors from interoperating with VMware's visualization software, according to a Dealreporter item on Tuesday, which cited sources familiar.

The parties have had significant engagements with authorities around the world, though there are no current discussions about potential concessions. The companies don't believe that any remedies are needed for deal approval.

What I really like here is that: 1) there's significant upside to the deal closing; and 2) the downside may not be all that bad.

Deals quite a bit underway were generally struck after a significant market downturn, while we've recently seen a recovery. A dreaded recession has not materialized as soon as many expected it.

The market seems to be assigning quite a high probability to the deal failing. However, that's not that obvious to me. I'd think authorities need to get quite creative to stop this deal. The EC outlined what concerns them about the deal (emphasis has been added by the EC):

The Commission's preliminary investigation indicates that the transaction may allow Broadcom to restrict competition in the market for the supply of NICs, FC HBAs and storage adapters by:

- degrading interoperability between VMware's server virtualisation software and competitors' hardware to the benefit of its own hardware, and/or

- foreclosing competitors' hardware by preventing them from using VMware's server virtualisation software or degrading their access to it.

This, in turn, could lead to higher prices, lower quality and less innovation for business customers, and ultimately consumers.

I think there are some analogs between this line of reasoning and the concerns around Microsoft Corporation ( MSFT ), I recently wrote about that deal on The Special Situations Report , restricting key games to its own hardware platforms after potentially acquiring Activision ( ATVI ). Theoretically, they could do that, but it seems that would destroy a lot of the value in the business they have just acquired. While at the same time, it seems really doubtful that increased hardware sales would make up for that. I think it is reasonable to scrutinize these deals and extract behavioral remedies or even divestments in these deals, but I'm skeptical that this type of argument can stop these deals.

The European Commission has a few secondary concerns:

Broadcom may hinder the development of SmartNICs by other providers . In 2020, VMware launched Project Monterey with three SmartNICs sellers (NVIDIA, Intel and AMD Pensando). Broadcom may decrease VMware's involvement in Project Monterey to protect its own NICs revenues. This could hamper innovation to the detriment of customers.

Broadcom may start bundling VMware's virtualisation software with its own software (namely mainframe and security software) and no longer offer VMware's virtualisation software as a stand-alone product reducing choice and potentially foreclosing rival software providers.

Broadcom exclusively bundling its software doesn't make much sense to me. I'd think that would destroy a lot of value of the acquired company. Broadcom may be buying VMware to delay budding competing efforts. I can see regulators being concerned about that, and I think it is good they are looking carefully. It also seems like an issue that can be fixed by behavioral remedies (promising to continue to fund that effort or selling or spinning out that joint venture).

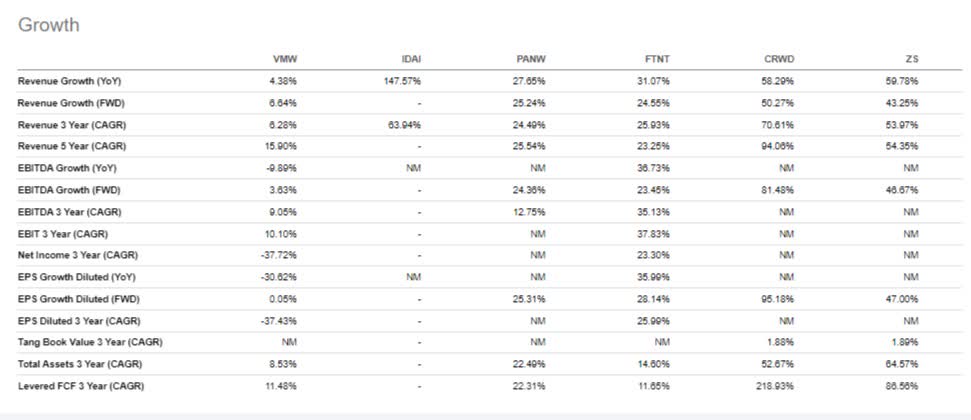

To get a better idea of the downside here, I pulled up growth and valuation data from Seeking Alpha for VMware and what Seeking Alpha designated as peers. I'm not very knowledgeable about tech companies (I have a value investing background, and tech has rarely traded at my kind of cheap). VMware is still showing growth year-over-year, over 3-year and 5-year periods. 3-year EBITDA growth looks quite attractive. Competitors or tech peers are generally growing revenue much, much faster, and as we'll see, their multiples reflect that. I think this picture is consistent with my understanding VMWare provides a lot of the incumbent legacy software and has a fighting chance to stay relevant, but its products aren't the hot new tech.

{kind=link}

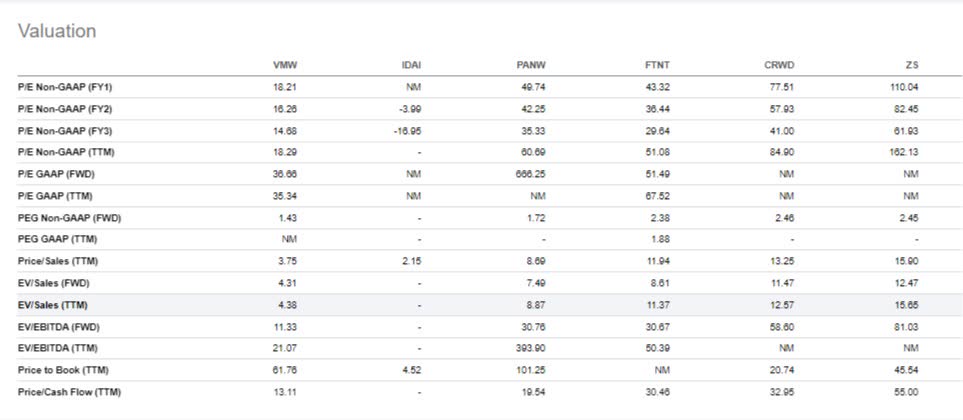

In terms of valuation, the company trades at a reasonable valuation at 13x free cash flow, 11x forward EV/EBITDA, 4x EV/Sales or 18x P/E.

VMware valuation (Seeking Alpha)

{kind=link}

Analyst estimates are for around $8 for the next fiscal year:

After falling throughout the merger period, there's been a recent uptick, which is a good sign.

Broadcom has committed financing from banks, the transaction could complete within several months, but more likely by mid-23'. The outside date is end of February, but this can be extended several times by 9 months total. By end of 23', the deal should be done or busted.

Regulators are rightfully concerned, but it is a vertical merger. The business is growing revenue and cash flow positive while I'm waiting. The valuation seems reasonable and based on pre-deal prices, the downside should be mitigated. Finally, there's also a 1% break fee which isn't much, but it is worth mentioning. I've hedged out about half of my long position by going short Broadcom.

The problem with shorting the acquirer is that you often get burned on both sides if the deal does break. This helps to explain why the deal has so much upside while it appears the target wouldn't fall that much on a deal break. Because the spread is so large here, an alternative tactic could be to go long the target VMware and forget about shorting Broadcom (or only short part of the exposure). Because the spread is very large, I think that's worth considering.

For further details see:

Why I'm Not That Concerned About The Broadcom VMware Deal Breaking