LMT - Why I'm So Very Bullish On Lockheed Martin

Summary

- Lockheed Martin is my single-biggest investment as a result of the qualities this company brings to the table.

- Not only is LMT a high-quality dividend growth stock, but it also benefits from rising defense spending and its ability to grow margins and revenues in the years ahead.

- While a lot has been priced in, I remain bullish, giving the stock a $700 fair value price target for the next four years.

Introduction

In this article, I will make the case that Lockheed Martin ( LMT ) could be trading at $700 (currently $490). The bull case continues to unfold as Lockheed Martin benefits from (at least) three major tailwinds.

- Favorable market and economic developments benefiting value stocks.

- Improving global defense spending - that's a long-term benefit.

- Lockheed's ability to deliver the right products and improve its business.

While there's no denying that the defense bull case isn't a well-hidden and undervalued investment idea, there's enough potential left for dividend growth investors and everyone looking to diversify into high-quality stocks.

On Dec. 5, 2021, I wrote an article discussing my decision to put 8% of my portfolio in Lockheed Martin. Since then, the stock price has surged 44%, protecting investors against market mayhem and generating a lot of wealth.

Between then and now, I have covered the war in Ukraine, slowly fading supply chain problems, and the company's dividend growth characteristics.

In light of all of this, we'll focus on the company's three main tailwinds as well as the risk/reward after a stellar performance since the pandemic lows.

So, let's get to it!

Buying Value Favors Lockheed Martin

When I bought Lockheed Martin before the war in Ukraine, my goal was not to benefit from any future wars. The decision to go overweight defense stocks was based on their ability to deliver sustainable dividend growth, behave anti-cyclical in recessions, and the fact that most are high-tech companies. Innovation is the best way to avoid a war in the first place.

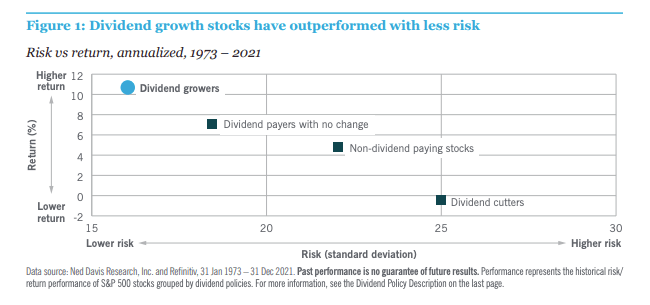

With that said, in one of my most recent dividend articles , I highlighted the ability of high-quality dividend growth stocks to outperform the market based on subdued volatility, protection during bear markets, and satisfying returns during bull markets.

{kind=link}

Nuveen

This certainly applies to Lockheed Martin. Since 1986, the stock has returned 12.9% per year, beating the S&P 500 by roughly 250 basis points per year. Moreover, this outperformance has lasted as the company has generated alpha on a three, five, and 10-year basis as well. Moreover, volatility was subdued.

{kind=link}

Portfolio Visualizer

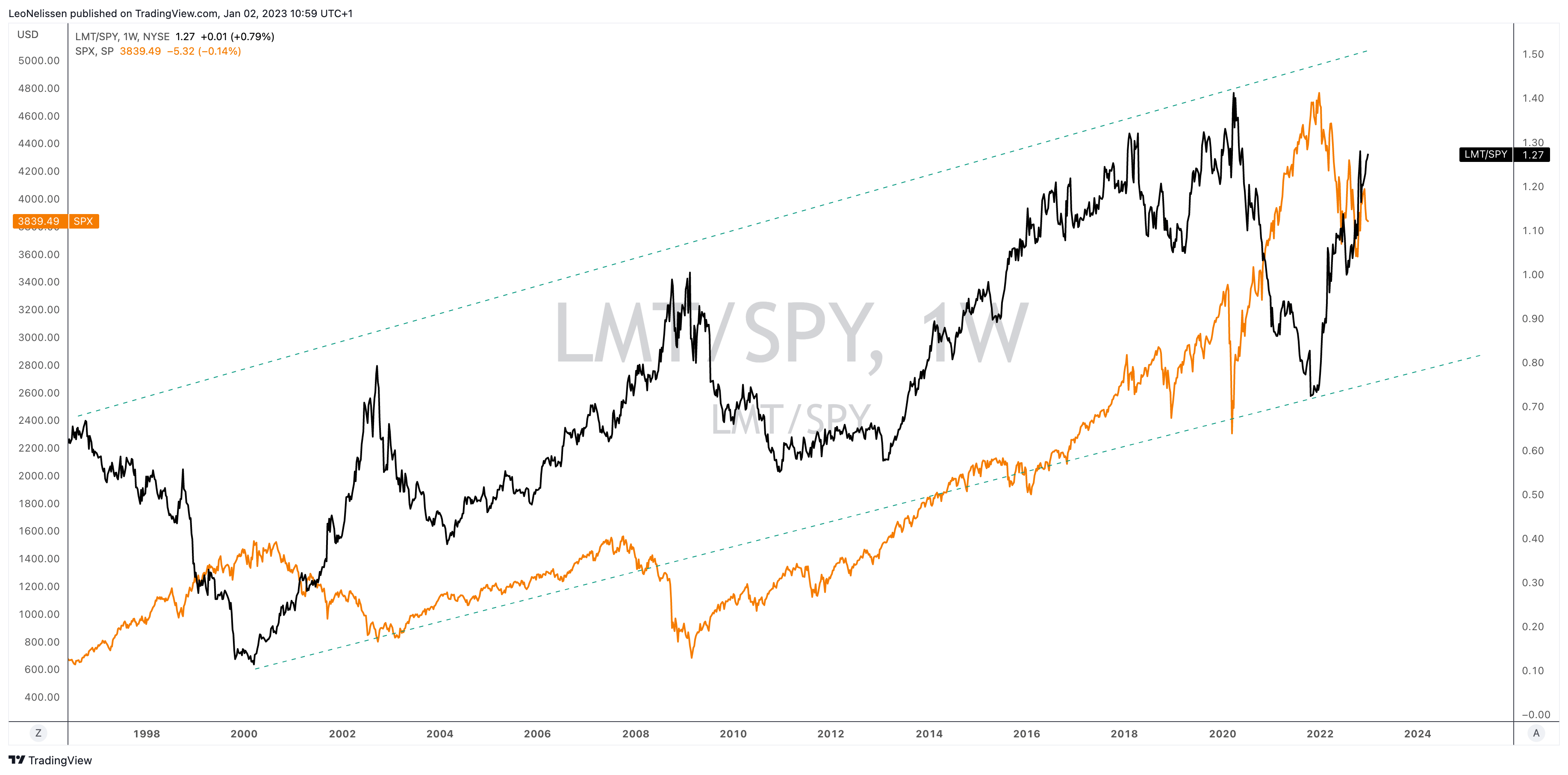

If we compare the ratio between the LMT stock price and the S&P 500 (the black line) to the S&P 500 (orange), we see that LMT shares have outperformed during every single major downturn. The only outlier was that the 2020 pandemic sell-off was rather short and followed by underperformance caused by supply chain issues and a bull market in high-growth stocks.

{kind=link}

TradingView (LMT/SPX, SPX)

Going forward, one can make the case that outperformance (based on quality) remains likely.

Accordin g to JPMorgan :

U.S. equity returns will be driven by earnings against a backdrop characterized by elevated market volatility. In this environment, companies with pricing power and stable cash flows – that are trading at reasonable valuations – are most attractive.

Moreover, last month, I wrote an article covering the high likelihood of a changed investment era. The Fed is unlikely going to become as dovish as it was before 2022. Inflation is stubbornly high, and secular factors like de-globalization and structural labor shortages are set to keep inflation at above-average levels.

This makes a strong case for investments in high-quality stocks with stable cash flows and improving growth.

That's where Lockheed comes in.

Improving Global Defense Spending

By now, everyone is aware of the impact the war in Ukraine has on defense stocks and the need for higher defense spending.

Over the past 12 months, all major defense contractors outperformed the S&P 500. Most of it occurred immediately after the invasion. After that, only several defense stocks continued their uptrends. Among them is Lockheed Martin, which was the second-best performer in the industry.

In this case, it's not just the war in Ukraine but also China's pressure on Taiwan and de-globalization, which causes global defense spending to rise.

Here are some examples:

- Japan is hiking its defense spending by more than a quarter in 2023 as it begins a five-year program to toughen its defense capabilities. This includes new missile capabilities, new jet developments, and ammunition procurement.

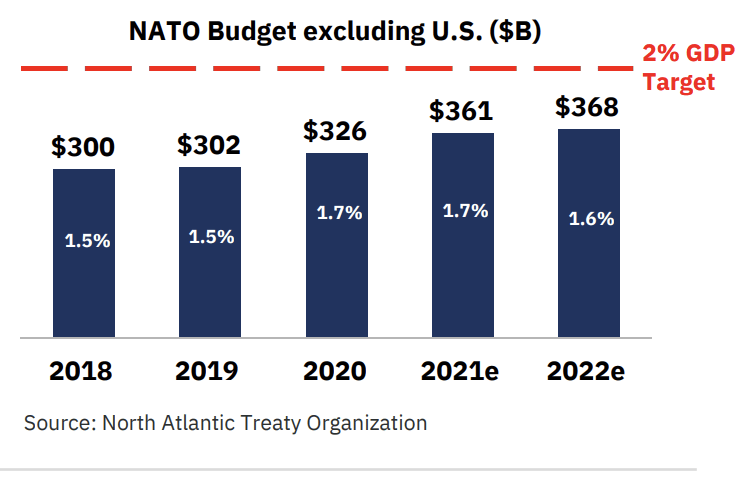

- NATO (ex-US) nations are looking to make the 2% spending target (of GDP) a floor instead of a target. This could mean another $92 billion in annual NATO (ex-US) defense spending, using 2022 numbers as a baseline.

{kind=link}

L3Harris Technologies

- The United States is stepping things up. The new omnibus package includes a 10% defense spending increase to $858 billion. This number is much higher than the 4% increase President Biden originally targeted. Defense contractors are now finally able to move on from the Continuing Resolution. These numbers indicate that the defense budget will have grown at 4.3% per year over the past two years - even after inflation. The average was less than 1% between 2015 and 2021. This is a significant shift in spending.

{kind=link}

DefenseOne

- The government is speeding up weapons contracts. The so-called Undefinitized Contract Action ("UCA") allows for rapid contracting and delivery before all terms and prices are made final. It's based on Operation Warp Speed, which spurred the development of vaccines and related procurement during the pandemic years of 2020 and 2021. The UCA is helping Raytheon Technologies ( RTX ) with advanced surface-to-air missile systems for Ukraine and Lockheed martin with GMLR rockets for its HIMARS system, valued at roughly $520 million. It's also a way to help contractors who struggle with supply shortages:

Suppliers would appreciate if the Pentagon “moved faster issuing contracts,” Jefferies defense analyst Sheila Kahyaoglu said in an interview. The defense industry supply chain “faces parts shortages that’s putting working capital pressure on smaller so-called third- and four-tier suppliers,” she said.

Lockheed's Back On Track

So far, we have mainly talked about the bigger picture. Hence, it's time to dive into Lockheed Martin.

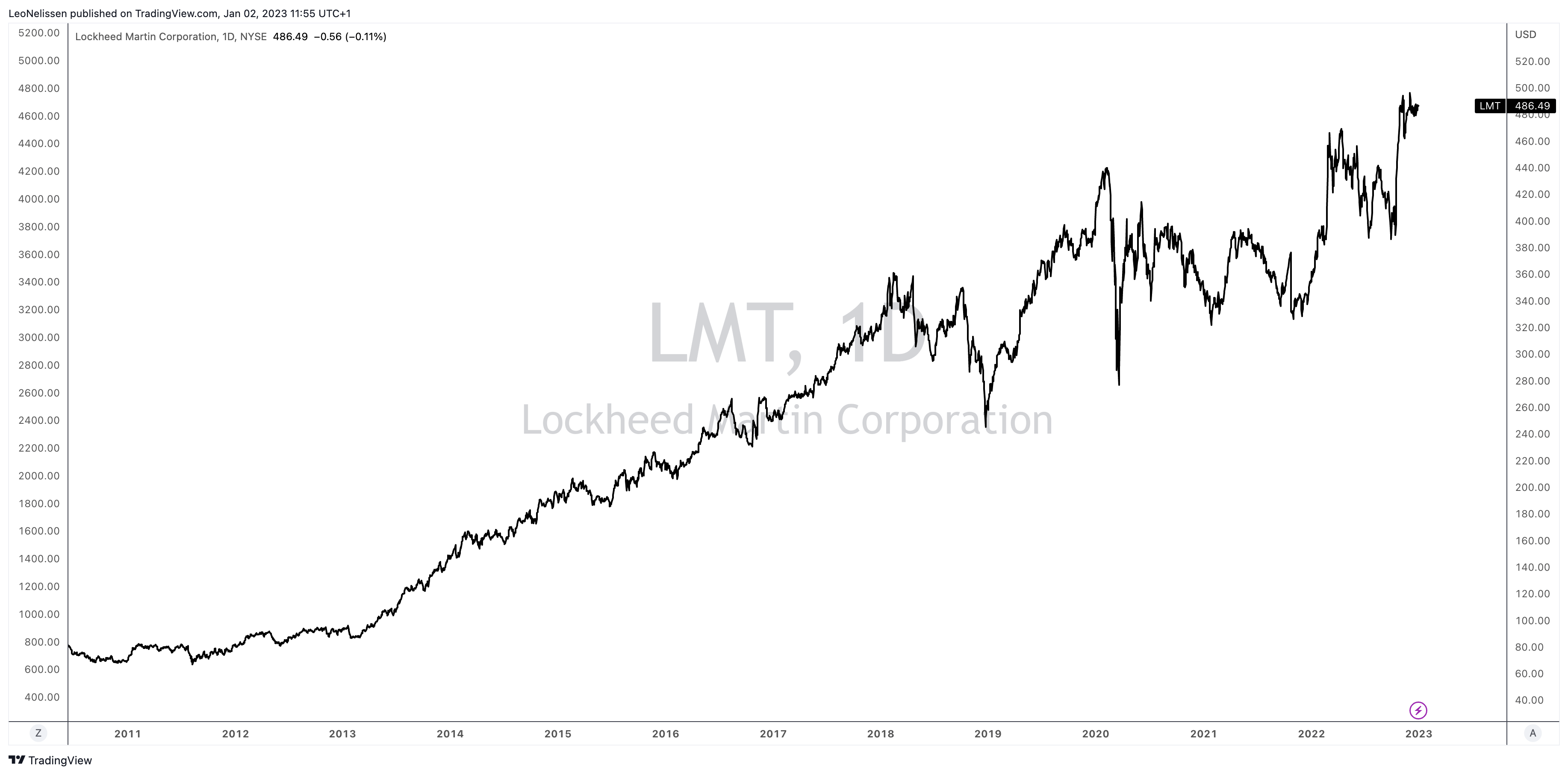

Lockheed Martin's stock price peaked in 2020 when the pandemic hit. While the company does not have commercial exposure, it took until the invasion of Ukraine for the stock to retake its 2020 pre-crisis highs.

{kind=link}

TradingView ((LMT))

The biggest issues non-defense companies had to deal with were supply chain problems hurting margins and the ability to finish orders and the uncertainty regarding government defense spending.

Now, both these issues are fading. Defense spending is ramping up while supply chain problems are easing.

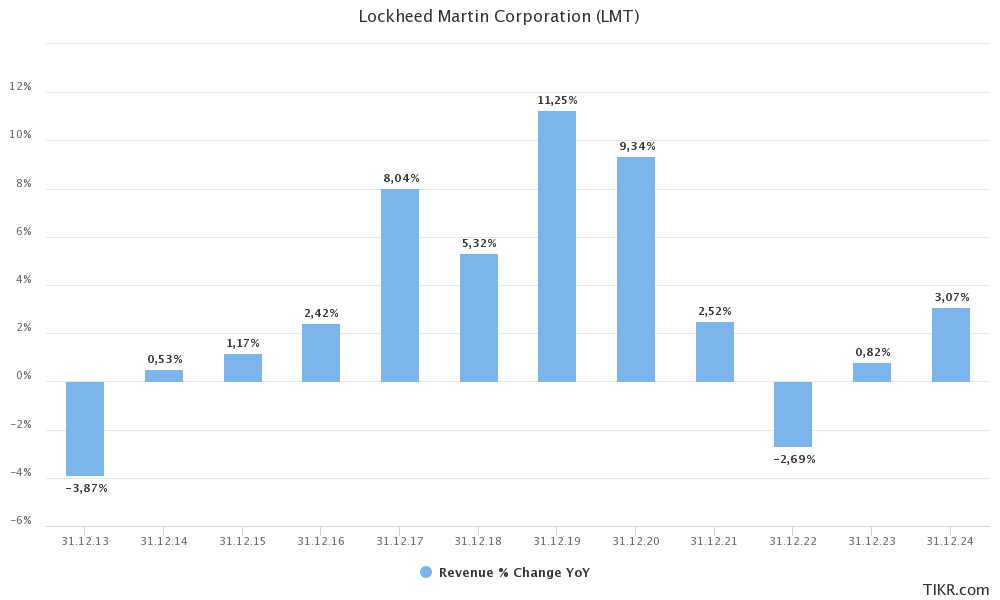

According to Lockheed , this impact will be visible in 2024 with 2023 being roughly in line with 2022.

We continue to anticipate growth over the long term, but with the residual pandemic impacts and supply chain challenges continuing, we now expect a return to growth in 2024 with 2023 sales being approximately equal to our 2022 outlook. We are confident in our four pillars to drive growth in 2024 and beyond. Importantly, we expect to deliver solid growth and free cash flow per share in 2023 and thereafter through a combination of cost reductions throughout the business, improved working capital management, and an expanded share of purchase program.

In 2023, sales growth is expected to be just 0.8%, after a 2.7% contraction in 2022. These two years are some of the weakest in recent history. In 2024, sales growth is expected to pick up, with higher growth expected after that.

{kind=link}

TIKR.com

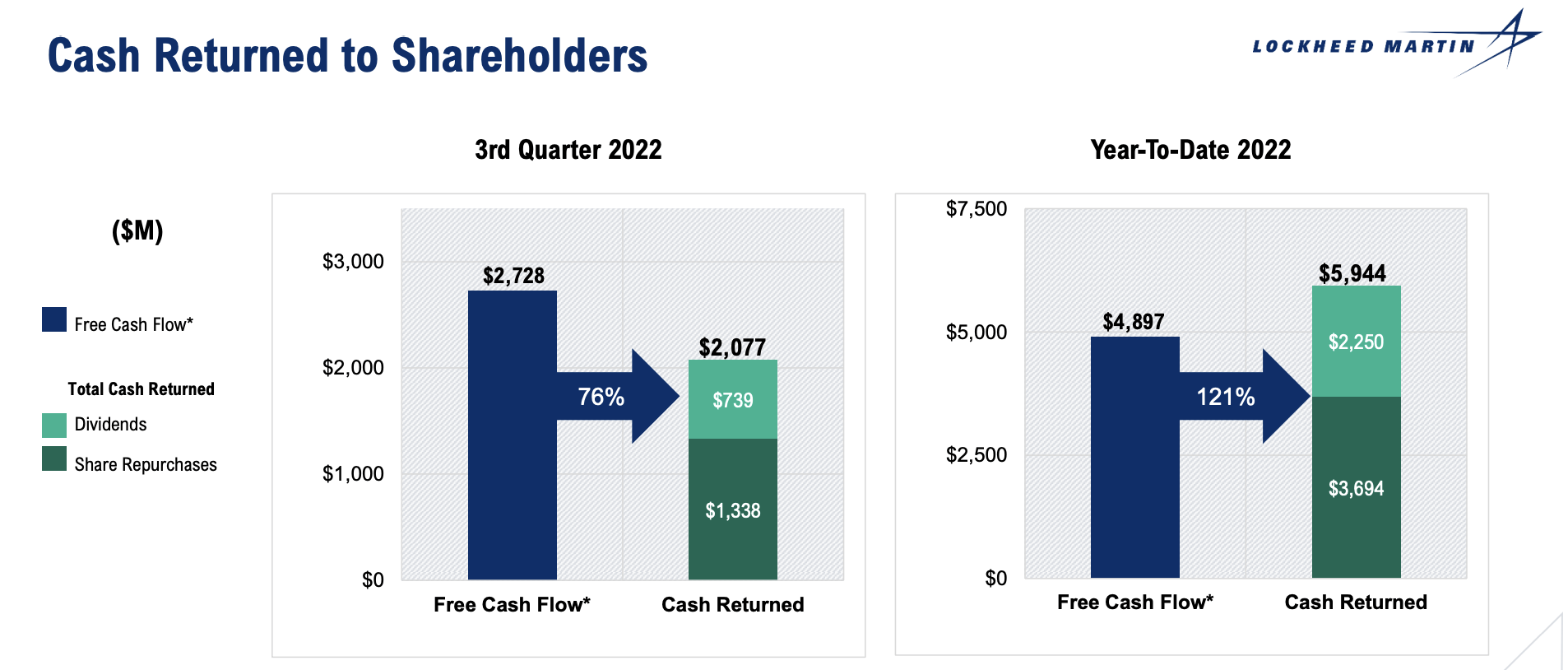

In anticipation of these developments (and to put some weight behind its comments), Lockheed increased its buyback program to $14 billion. In 2022, the company is expected to repurchase shares worth $8 billion.

{kind=link}

Lockheed Martin

Moreover, the company hiked its dividend by 7%. LMT shares now pay a $3.00 per quarter per share dividend. This translates to a 2.5% dividend yield.

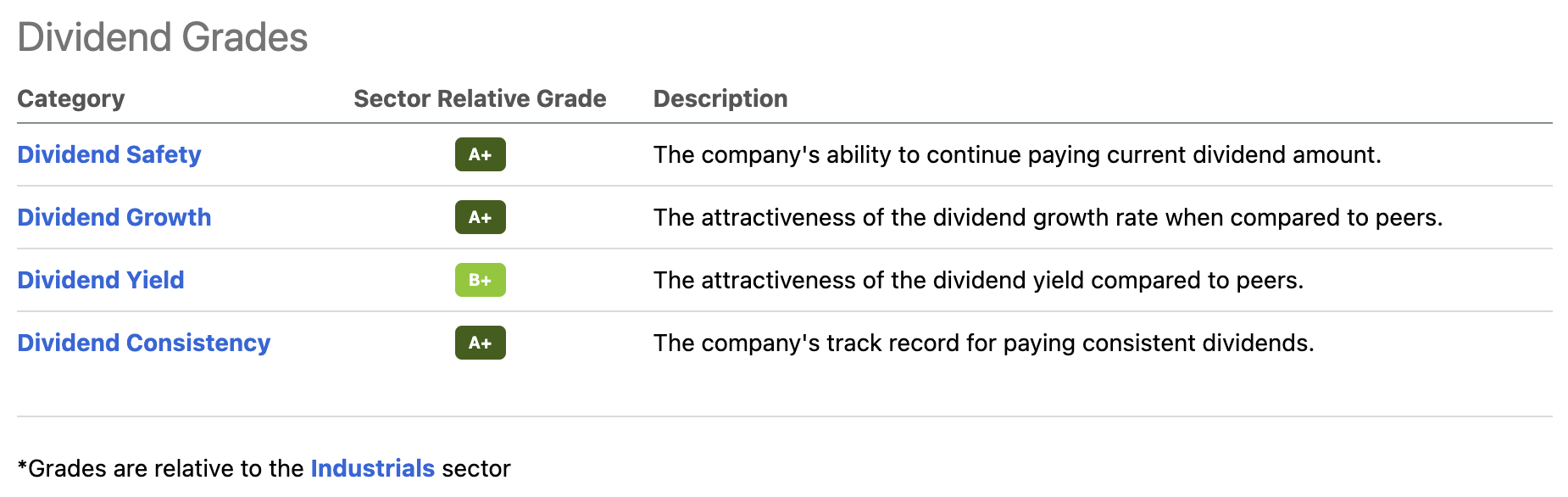

The company has a fantastic Seeking Alpha dividend scorecard, which shows high scores in all categories, including dividend safety, growth, and consistency.

{kind=link}

Seeking Alpha

Over the past ten years, the average annual dividend growth rate was 10.6%. While that number has declined to 8.9% over the past five years, I expect it to remain close to double-digits, especially as the company is improving its business again.

This brings me back to the company's business improvements. One of these things is One LMX, a multi-billion-dollar, seven-year company-wide program to transform its end-to-end business processes and systems. LMX will create a model-based enterprise using digital systems to review areas allowing the company to create synergies between business areas and reduce unnecessary costs.

Moreover, while 2023 sales will be flat-ish as a result of ongoing supply chain issues and the possibility of lower F-35 sales, the company sees higher growth going into 2024 (as I already briefly mentioned). F-35 production will ramp up, and the higher installed base of existing planes is expected to result in a meaningful increase in maintenance and related.

Starting in 2024, the company expects to produce 156 aircraft as it anticipates normalizing supply chains. This would be based on 80 domestic aircraft and 75 coming from international orders.

My opinion is that supply chains might normalize faster than expected. If the US enters a recession this year, a lot of competition for high-tech materials and labor will fade. That benefits defense companies that have anti-cyclical order flows.

Adding to that, Lockheed expects to be in a great position to benefit from changing defense needs - especially when it comes to nuclear deterrents.

On F-35, the U.S. government has got to kind of determine what its budget priorities are at the macro level going forward. One of those has been nuclear deterrents. And so, between the bomber program, the ground-based missile recapitalization and the fleet ballistic missile that I just mentioned, there’s going to be a significant amount of defense budget proportionately spent on the nuclear revitalization. But also the conventional threats have gotten worse instead of better as we look forward into the next 2 or 3, 4 years, and that’s going to be a budget issue for the U.S. government.

Moreover, I have to comment on inflation. 60% of Lockheed's contracts are fixed-price contracts. This is important to mention concerning the company's ability to protect itself and its investors against inflation. 40% of sales are directly protected against inflation based on the variable cost structure. The 60% that are fixed benefit from the fact that contracts with suppliers are also fixed. In other words, the inflation risks are spread out throughout the supply chain. At that point, it becomes a government issue again. It's one of the reasons why boosting defense spending by 10% was so important. A lot of smaller defense players were struggling with inflation.

With that said, I know you have at least one more question.

What About The Valuation?

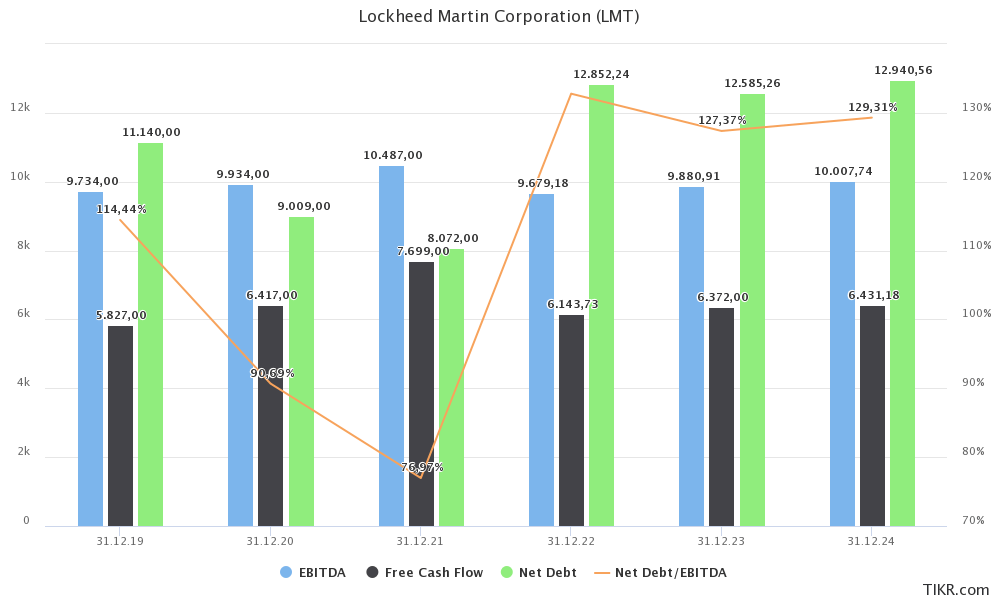

Lockheed's total return of the past 12 months exceeds 40%. In other words, a lot of good news has been priced in. The company is now trading at 14.6x 2023E EBITDA of roughly $10.0 billion. This is based on its $127.5 billion market cap, $12.6 billion in expected net debt, and $5.7 billion in pension-related liabilities.

{kind=link}

TIKR.com

The company has an A- credit rating.

A forward multiple of 14.6x is everything except cheap. It's a fair valuation given the bigger picture. I doubt the market will allow the stock to fall a lot in light of expected business improvements and support from higher orders for many years to come.

While I'm writing this, I have roughly 8.5% exposure in Lockheed Martin, making it my largest position.

Because I aggressively added to defense stocks during weakness in 4Q22, I'm not yet looking to buy more exposure. However, I believe that any 10% to 15% pullback is buyable.

Over the next two to four years, I estimate that LMT's fair value is $700 per share. That is an opinion far from the consensus. However, if we incorporate moderate sales growth, the company should be able to do close to $12 billion in EBITDA over the next two years. I see more upside, allowing the company to breach $700 per share. My first target is $600 over the next two years.

Needless to say, I believe that LMT is a must-own investment. The company has a stellar business model, anti-cyclical behavior, subdued volatility, and the ability to outperform the market on a long-term basis while providing steadily rising income through dividends.

Risks

Putting 8.5% of my portfolio in a single stock means it's a high-conviction investment. However, despite my very bullish view, there are risks that need to be incorporated.

- The company remains dependent on governments. The US government alone accounts for more than 70% of sales. This means that future defense spending slumps could cause the stock to seize any uptrend.

- The success of the F-35 program is important as this fighter accounts for close to 30% of total sales. This includes technical and performance risks that could hurt the demand.

- The government could implement procurement policies that negatively impact the company's ability to use pricing as a way to grow sales.

- Competition risks are high as next-gen technologies are becoming key drivers of growth and profitability.

Needless to say, I believe that none of these risks will materialize. Also, "if" any of these risks do materialize, I do not expect it to impact the company's ability to pay a dividend. The risk/reward remains very attractive.

Takeaway

In this article, we covered the Lockheed Martin bull case. The company's shareholders benefit from three bullish tailwinds. The first one is the favorable position of value stocks in this market environment. High macroeconomic uncertainty is favoring stocks that bring value to the table. That's where LMT comes in.

Second, the company finally benefits from rising defense spending. The US, NATO nations, and other allies are stepping up spending to erase years of below-average spending growth and to be prepared for a changing defense environment.

Third, LMT is improving its own business. While 2023 is expected to be a flat year, we should expect accelerating growth after 2023. Orders are strong, margins are improving, and supply chain issues are rapidly fading.

This should continue to provide high dividend growth and buybacks for investors buying LMT for both capital gains and dividends.

I believe that LMT should be trading at $700 in the 2-4 years ahead. Needless to say, there's no guarantee that this happens. If the stock remains in a sideways trend, investors will still benefit from a decent yield and satisfying dividend growth.

While I have bought considerable defense exposure, I'm a buyer again as soon as the stock drops 10%-15%.

(Dis)agree? Let me know in the comments!

For further details see:

Why I'm So Very Bullish On Lockheed Martin