CA - Why I Quit Private Equity Real Estate To Buy REITs Instead

Summary

- Private real estate funds claim they can earn you "high returns."

- But they typically underperform REITs despite taking a lot more risks.

- I explain why I quit private equity to become a REIT analyst.

I come from a family of real estate investors.

Pretty much all the money that my parents have ever made, they put it into real estate.

And so, naturally, I felt a clear affinity for it. Growing up, I would regularly visit construction sites and discuss real estate deals with my father.

Eventually, I went to university to study real estate investing and then landed a job in private equity real estate.

My company was a lot smaller than Blackstone ( BX ), Brookfield ( BAM ), or even KKR ( KKR ). We would do mainly smaller deals in the $1-10 million range back then, buying triple net lease properties such as those that Realty Income Corporation ( O ) is targeting.

Realty Income

I loved it. The idea of buying real estate with mainly the bank's money and then having tenants reimburse the mortgage was fascinating to me.

Add to that the cash flow, appreciation, and tax benefits, and you could earn great returns!

But eventually, I learned more about real estate investment trusts, or REITs ( VNQ ). These are publicly listed real estate investments. I quickly came to the conclusion that these were far better investments than private equity real estate in most cases.

This led me to quit private equity and become a REIT analyst in pursuit of superior risk-adjusted returns. Eventually, I created my own REIT investment firm, Leonberg Capital, and that's what also brought me here on Seeking Alpha, where I cover many of my favorite REIT investment opportunities.

In what follows, I will give you five reasons why REITs are better than private equity in most cases. When I say private equity, this includes the big funds managed by the likes of Blackstone, but also the smaller players using crowdfunding like Fundrise, Cardone Capital, etc.

Reason #1: REITs generate higher total returns over time

Private equity players will typically advertise high projected returns when raising capital. A good example is Cardone Capital and its 20%+ targeted IRRs:

{kind=link}

But the reality is that targeted IRRs are rarely achieved. This is marketing for the most part, and since it is "pro-forma," they can use whatever assumptions they want to achieve these projected returns.

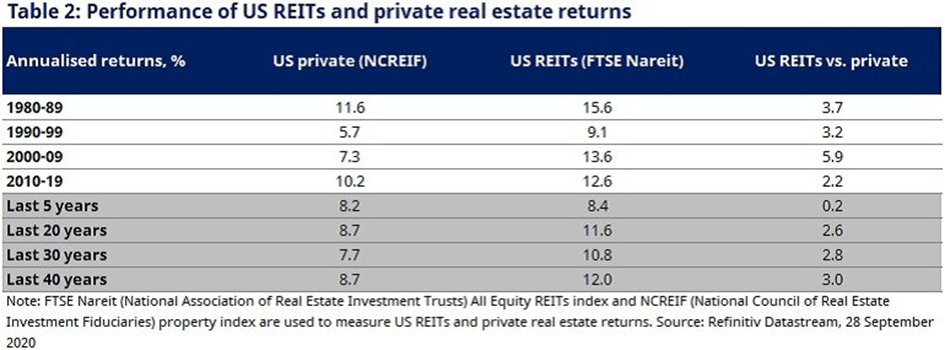

In reality, the average returns of private equity real estate have been a lot lower, at closer to 8-10% per year annually. This is still pretty good, but it is actually quite a bit worse than the returns of REITs.

Many studies have been done on this topic, and the conclusion is that REITs outperform by 2-4% per year on average:

{kind=link}

How is this possible?

This is a surprising result to many people when they first hear about it, but it actually makes sense when you think about it.

REITs are a lot more rewarding because:

1) They enjoy huge economies of scale. REITs will often own 1,000s of properties in a single market, resulting in significant savings on all fronts. The management. The construction/renovation cost. The leasing. Etc. Imagine a REIT doing a deal with a contractor to change 1,000 carpets in a city every year vs. a private fund holding one or a few properties. The pricing will be very different.

2) They have access to cheaper public capital. REITs can raise capital through the public markets. They can access public equity, often at a premium to NAV, preferred equity, convertible debt, public bonds, etc. This diversity and better access allow them to lower their cost of capital, earning better spreads on their investments.

3) They are not limited to organic growth. Private funds are limited to growing the same property NOI. But REITs can also grow externally by making new capital raises. As long as the targeted returns are higher than their cost of capital, there is a positive spread that will boost total returns. That's how REITs like Realty Income manage to grow at >5% per year, despite only having 1% rent hikes in their leases. Private equity cannot compete with that.

4) They can enter other real-estate-related businesses to boost profits. REITs will often use their vast platform to also offer services to other investors and these profits are then shared with the shareholders. As an example, Armada Hoffler Properties ( AHH ) offers construction services, SL Green Realty ( SLG ) offers asset management services, and Farmland Partners ( FPI ) offers brokerage services. Private real estate funds won't share such profits with you because they are managed externally by outside asset management firms, and so they will take these profits for themselves.

5) They are better aligned with shareholders. Most REITs are internally managed, which means that the managers are hired as employees of the REIT and they earn salaries that are a function of shareholder value creation. Private funds, on the other hand, are externally managed by outside companies that earn fees that are largely a function of assets under management, creating significant conflicts of interest as they will attempt to grow as big as possible to earn higher fees.

6) They skip real estate transaction costs. REITs are so large that they have their own relationships with other real estate owners and also with tenants. This allows them to skip costly brokerage fees and other transaction costs. Unless you are a huge private equity player, you will end up paying more in transaction costs.

7) They hold more bargaining power with tenants. REITs are big vehicles, they are highly diversified, and this gives them more power as they negotiate with them. Private equity vehicles typically own just 1-10 properties in a single entity and so their tenants often hold the cards. They know that a vacancy would be a huge problem for them.

And there are many other reasons!

Reason #2: REITs are far safer investments

Private equity players will also claim that they are safer than REITs because they aren't as volatile.

But again this is not correct.

Private equity funds are typically concentrated, illiquid, and highly leveraged.

REITs, on the other hand, are typically diversified, liquid, and conservatively leveraged.

How are you going to tell me that REITs are riskier?

It is the opposite. Just because you aren't listed and don't have daily liquidity does not mean that your equity value isn't very volatile. On the contrary, it is far more volatile since you are concentrated, illiquid, and highly leveraged. Not having access to information and closing your eyes on the volatility does not make its value more stable.

I cover this topic in more detail in a recent YouTube video.

{kind=link}

Reason #3: REITs give you liquidity and control

Recently, Blackstone ( BX ) made headlines as many investors attempted to exit one of its non-listed real estate vehicles, but it limited redemptions.

That's illiquidity.

Most private equity vehicles have ~10-year terms, which means that you simply cannot get out unless the general partner allows you to sell your interest to another investor, likely with significant fees and at a big discount.

{kind=link}

With REITs, you have liquidity and you are in control.

You can leave at any time with a few clicks of mouth. It is quick and easy. If a REIT suddenly becomes unattractive because the fundamentals of its properties are starting to deteriorate, you can sell and invest elsewhere.

This greater flexibility allows you to earn higher total returns over time.

With private equity vehicles, you are stuck, whether you want to stay invested or not.

Reason #4: REITs align interests between managers and investor

Show me the incentive... and I will show you the end result...

We already shortly discussed this earlier, but I want to make an addition to really bring this point across.

Private equity vehicles are externally managed and the interests of the manager are to maximize their fees, and they typically achieve this by growing their assets under management. They can achieve this with sleek marketing even if their results are questionable. After all, their funds are illiquid and private so you wouldn't know about their results anyway. They may sell one or a few good-performing assets just to show that they have a great track record, which will then allow them to raise more capital and earn more fees. The manager will also manage many other vehicles at the same time, creating conflicts of interest.

REITs are internally managed and so the incentives are much better aligned. The managers are employees and their salaries/bonuses are a function of the performance of the REIT. Their sole focus is this one REIT that they work for.

This seemingly small change in management structure alone will materially lower risks and increase returns over time.

Just take a look at how private equity real estate players bought more and more real estate leading up to the great financial crisis. They were buying to increase their fees. Meanwhile, REITs were selling to them because interests are better aligned:

{kind=link}

So again: show me the incentive... and I will show you the end result...

Reason #5: REITs can be bought at a steep discount and you save commissions and fees

Finally, and perhaps most importantly, REITs allow you to invest in real estate at a steep discount to fair value.

It is not uncommon for REITs to trade at a 20, 30, 40, or even 50% discount relative to the underlying value of the real estate they own. This essentially means that you get to buy real estate at cents of the dollar.

To give you a few examples:

Vonovia (VNA / VONOY ), the biggest publicly listed apartment landlord in Germany is currently priced at just 40% of its net asset value. This means you get a 60% discount.

Camden Property Trust ( CPT ), one of the biggest apartment owners in rapidly growing sunbelt markets in the US, is currently priced at an estimated 30% discount.

SL Green, the biggest Class A office landlord in NYC, is currently priced at an estimated 50% discount to its net asset value.

Camden Property Trust

You regularly have such opportunities in the REIT sector because of stock market volatility. Most stock investors are short-term oriented and this leads to lots of pricing inefficiencies in the REIT sector.

But if you invest in a private real estate fund, you are going to pay full price. You will get in at the latest net asset value, plus you will likely also pay some commissions and other fees.

Just saving those commissions alone will give you a head start, and then the added discount will also boost returns and provide margin of safety.

Bottom line

I think that most real estate investors will earn much better returns with less risk by investing in REITs than in fancy private equity real estate vehicles.

It is less cool. You don't get the feeling of being part of an "exclusive" group.

But studies clearly show that REITs outperform and they do so with less risk. This is why I ultimately quit private equity and became a REIT investor.

For further details see:

Why I Quit Private Equity Real Estate To Buy REITs Instead