PBR - Why I Sold Altria To Buy Petrobras And Ecopetrol

2023-03-07 08:00:00 ET

Summary

- Altria is still cheap, but their interest in another vape acquisition had me considering alternatives last week.

- South American energy companies Petrobras and Ecopetrol have been on my radar for a couple weeks, but the light bulb went off for me this weekend.

- Petrobras declared a $1.06 dividend for Q4, which puts the yield into the double digits for PBR.A shares. I explain why investors should look at PBR.A over PBR.

- Ecopetrol announced an annual dividend of $2.47, and shares are dirt cheap today.

- Investors looking to diversify outside of the US might want to take a look at these two companies. The rewards far outweigh the risks in my opinion.

I have owned Altria ( MO ) for a little over a year, and the share price performance was a lot better than the overall market. I am a patient investor, but I also have more ideas than I do money right now. I know I made Altria one of my picks for 2023 , and I certainly had no plans on selling a couple months ago. There were several things that started the small voice in the back of my head, but the trade became more obvious as I kept digging. I find the tobacco industry pretty attractive for several reasons, but Altria was my primary holding for its large dividend and brand power of Marlboro.

If I could create the ideal tobacco company from scratch today, the business mix would be approximately a third cigars, a third cigarettes, and the last third would be a competitor for Zyn pouches. You might notice that products like vapes are absent, but I am skeptical on the long-term future of people switching to vapes and other similar products. When I heard that Altria is dumping another couple billion into NJOY , my first thought was all the money that management lit on fire with Juul, another vape company. I wasn’t thinking about selling until last week, but the NJOY acquisition speculation (which has now been confirmed) was kind of the catalyst that caused me to start looking elsewhere.

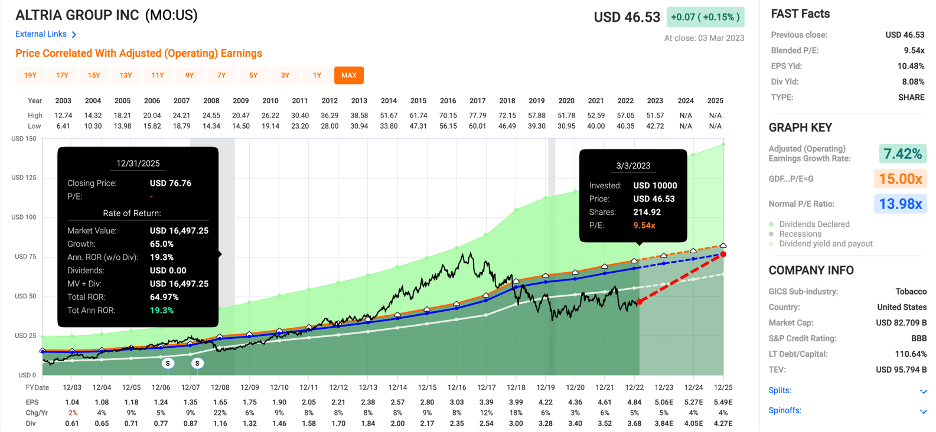

Like many investors, I bought Altria for the cheap valuation and the large dividend. Altria still has a single digit P/E ratio and a yield over 8%. I don’t think a recession proof business with margins like Altria should be this cheap, but that is what ESG will do. I still think Altria is an attractive risk/reward proposition below $50, but I’m willing to take my small gains and reinvest elsewhere because I find the alternatives to be better opportunities.

Price/Earnings (fastgraphs.com)

{kind=link}

I said in my last article that all it would take for Altria to head past $60 was multiple expansion to 12x. That still holds true, and there aren’t many stocks out there where you can collect an 8% dividend while waiting for a likely price appreciation kicker. For me, it all comes down to opportunity cost. Do I think Altria is still cheap? No doubt. Do I think Altria will likely outperform the market? Yes. Do I think shares are as attractive as Petrobras ( PBR ) ( PBR.A ) or Ecopetrol ( EC )? Not even close.

Petrobras – The Brazilian Oil Giant

I started looking closer at Petrobras and Ecopetrol over the last couple months. I was surprised to see how deep the selloffs got, but selloffs due to misplaced political fear have created very interesting opportunities. While I typically get most of my new ideas from Seeking Alpha, some of my recent ideas (like Transocean ( RIG ) and Peabody Energy ( BTU )) ended up in my research pile from accounts I follow on Twitter. While some investors might not be comfortable getting investment ideas off of Twitter, a lot of the accounts I follow provide a ton of good information for free.

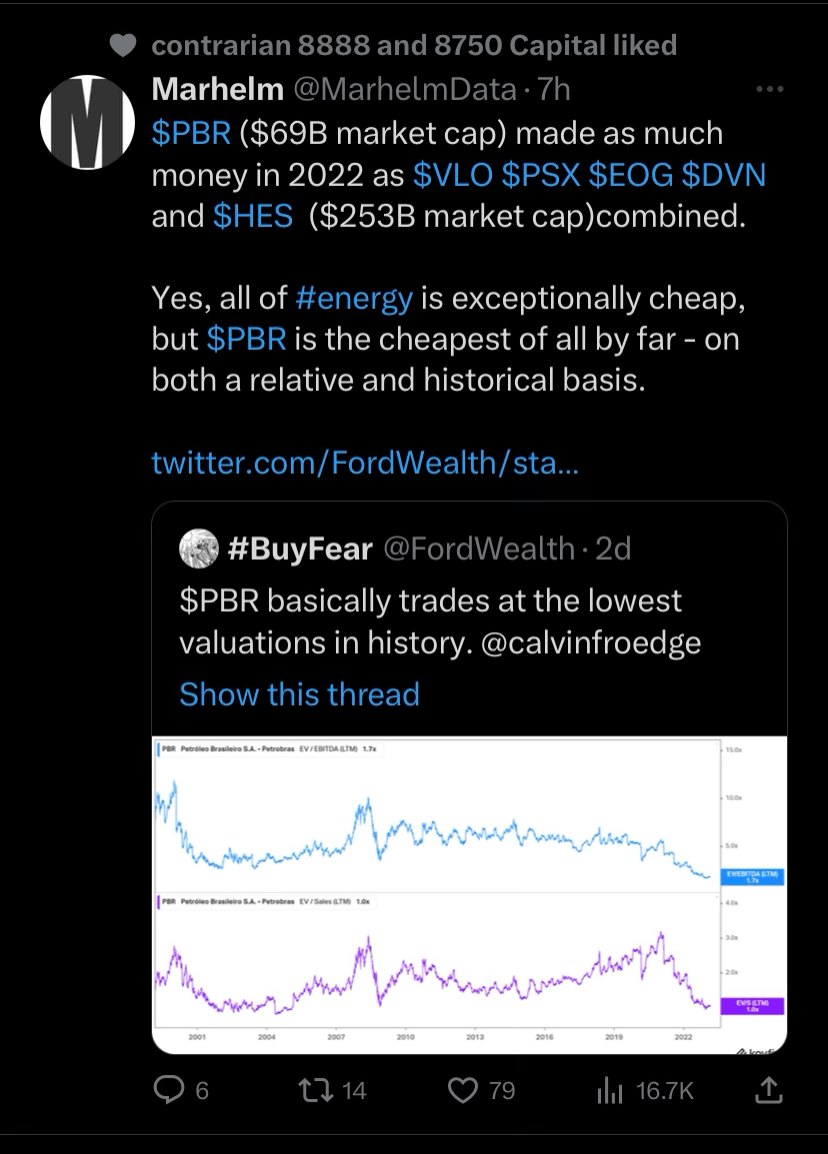

One in particular, @calvinfroedge , has been pounding the table on Petrobras and Ecopetrol for some time. For those with Twitter accounts, I would recommend following him. I can also recommend going into the app and searching or .A, which will bring up top tweets on the company. It’s pretty obvious that Petrobras is very cheap, but one of the tweets I saw this weekend stood out.

Petrobras is CHEAP (twitter.com)

{kind=link}

Petrobras had a monster 2022 like many companies in the energy sector. While I think the American companies will perform fairly well over the next couple years, the valuation on Petrobras looks absurdly cheap. The fact that the company made as much money in 2022 as Valero ( VLO ), Phillips 66 ( PSX ), EOG Resources ( EOG ), Devon Energy ( DVN ), and Hess Corporation ( HES ) combined is an impressive feat. Now consider that Petrobras' market cap is less than one third of the American companies above. I hadn’t looked that closely at Petrobras until the last couple weeks, but the lightbulb finally went off for me. Better late than never, I guess.

The dividend, which might not be consistent like American companies, has been very rewarding for investors over the last couple years. Shares of Petrobras paid over $6 in dividends in 2022, which is absolutely insane for a stock trading below $10. I bought the PBR.A (I’ll explain why shortly). The next dividend payout will be $1.06, with two equal payments in May and June. I plan to buy 1,000 shares, so I’ll be getting a bit over $1000 and 10% of my money back by the end of June. I don’t think we will see the dividends be as big as last year, but I think investors will get another payout in the second half of the year.

PBR or PBR.A?

One last thing I want to cover on Petrobras is the share structure. If you search Petrobras, you will be able to find two tickers: PBR and PBR.A. PBR is the common stock, which gives you voting rights and more liquidity, but trades at a pretty wide premium ($11.43 as I write this Monday night). PBR.A, on the other hand, is just over $10. It is a preferred share, which means no voting rights and less liquidity, which are both nonissues for me. The PBR.A shares have dividend priority, which is a nice bonus for investors. The company is required by law to distribute at least 25% of net profits for PBR.A, so even if the dividends drop on the common share, PBR.A holders should still receive sizable dividends.

I wouldn’t be surprised to see Petrobras pay more than $2 in dividends to shareholders over the next 12 months. I think that Petrobras will continue to pay sizable dividends for years to come, and with my view on oil prices over the next three to five years, I think it is entirely possible that investors buying today could see their entire initial investment returned to them over the next three to five years. That is another reason I prefer PBR.A, which has legal protections for the dividend.

Unless you plan to move mountains of money in Petrobras, I think the PBR.A shares would be a better fit for most investors. You get the shares at a decent discount, and the voting rights and liquidity aren’t issues for most investors anyway. While Petrobras does have some political risk, I have a hard time seeing how investors could lose money over the next couple years with Petrobras. If shares keep dropping, I’ll gladly add to my position.

Ecopetrol – Petrobras' Colombian Counterpart

Many investors familiar with the energy space have heard of Petrobras, but Ecopetrol flies under the radar by comparison. I’m going to keep this section shorter as Ian Bezek did a great write up on the company last week. Some investors might not like the idea of buying shares of a company where 88% of the stock is owned by the government, but I think the potential rewards justify the risks with Ecopetrol. Ecopetrol will be paying out $2.47 this year, so I will be getting over $2,000 or 20% of my money back by the end of the year.

The payment of dividends to minority shareholders will be made in three equal installments on April 27, September 28 and December 21, 2023.

- Ecopetrol's 2022 Earnings Distribution Proposal | Seeking Alpha

Conclusion

We will see what things look like over the next couple years, but I’m expecting higher oil prices for the most part. While Altria is still undervalued, I don’t think the risk/reward is close to these two companies. That is why I sold my shares of Altria and reinvested in Petrobras and Ecopetrol. For me it was a simple opportunity cost calculation. If you purely want to look at dividend income, the shares of Altria I sold were worth about $20,000, which would have provided a bit more than $1600 in income over the next year. I bought 1,000 shares of PBR.A and 1,000 shares of Ecopetrol on Monday morning. Petrobras will pay over $1000 by June, and another payout in the second half of the year is possible. Ecopetrol will pay over $2,000 over the next 9 months.

I won’t make projections for 2024, but I think the downside risk is limited, and I couldn’t pass up the opportunity to double my dividends for 2023. By swapping out Altria for Petrobras and Ecopetrol, I get the chance to buy dirt cheap assets, with plenty of juice on the upside due to the valuation and potential for a run higher in oil prices, and a massive income stream at the same time. Is there political risk? Sure. Does that mean investors should ignore markets outside of the US? I don’t think so. I think Altria should do fine over the next couple years, but I will simplify things like this: buying shares of Petrobras and Ecopetrol looks to me like spotting a giant pile of money that some investors have thrown away prematurely. I just took the time to figure it out and go over to pick it up.

For further details see:

Why I Sold Altria To Buy Petrobras And Ecopetrol