CA - Why Nutrien Is Still A Strong Buy

2023-06-07 15:48:47 ET

Summary

- Nutrien's stock price has declined, but the fundamentals of the fertilizer industry remain strong due to geopolitical developments, increased affordability, and the need for higher crop output.

- Despite poor first quarter results, Nutrien's outlook is positive, with a subdued supply growth situation and strong demand for crop inputs.

- With a potential mid-term price target of $90, Nutrien offers an attractive risk/reward profile for investors willing to weather the volatility.

Introduction

It's time to talk about fertilizers. On May 8, I wrote an article titled Nutrien: Undervalued And Oversold Going Into Earnings. In that article, I explained that potash fertilizer fundamentals were strong, using earnings and guidance from its largest peer, Florida-based Mosaic Company (MOS).

While I stand behind everything I wrote in that article, the Nutrien Ltd. (NTR) earnings report didn't make me look so good, as management cut guidance.

Right now, NTR shares are down roughly 13% since my prior article.

While that hurt my newly-established NTR position, it's far from unfavorable, as I remain bullish and have continued to add to my favorite agriculture holdings. Thanks to its decline, I decided to keep adding to NTR.

In this article, I will explain why I'm aggressively buying NTR shares, using its earnings, comments, and my view on the agriculture industry.

So, let's get to it!

A Quick Look Back

In my prior article, I wrote a number of things that are important to keep in mind before we dive into new developments and comments.

- Despite the stock price performance, the fertilizer fundamentals remain strong, and the longer-term risk/reward has become more attractive.

- The global supply of fertilizers faces challenges due to factors such as the war in Ukraine, weather phenomena like El Nino, and China's focus on food security.

{kind=link}

- Nutrien plans to increase its production capacity in Saskatchewan, although the timeline may be adjusted based on market conditions.

- Potash, an essential fertilizer, has a positive outlook due to geopolitical developments, increased affordability, and pressure to increase crop output.

- The biggest risk to the potash industry is the return of Eastern-European supply to the market.

- Despite the current decline in stock price, Nutrien is expected to perform well in the long run based on positive potash developments and its strong position in the industry.

So, what happened?

Nutrien Took A Beating, Yet It Remains On Track For Success

What Happened In 1Q23?

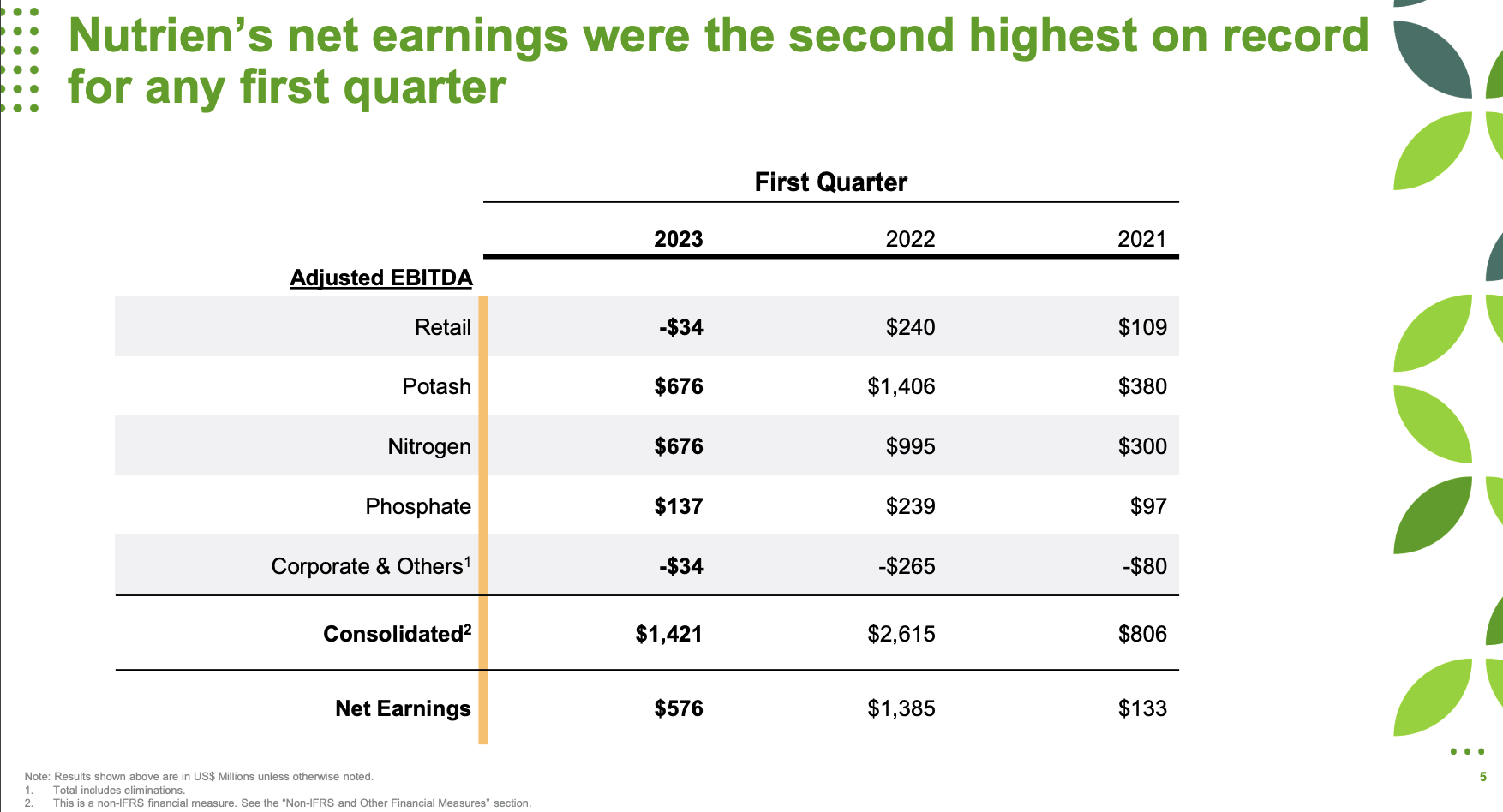

Nutrien's results were worse than expected. The company reported $6.1 billion in revenue. This is 20.2% lower compared to the first quarter of 2021 and $210 million lower than expected.

Earnings per share came in at $1.11, which missed estimates by $0.37.

The worst part was its guidance (emphasis added):

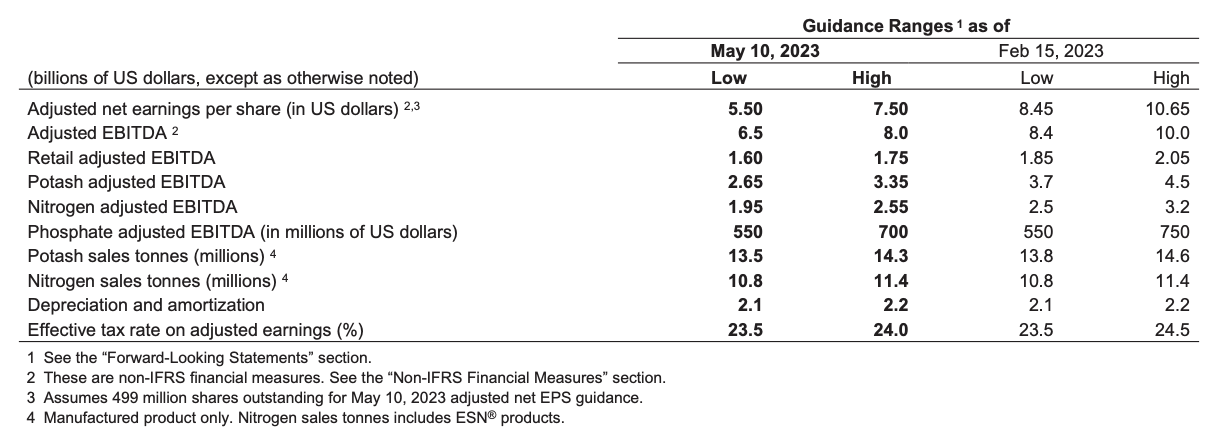

Based on market factors detailed above, we are revising full-year 2023 adjusted EBITDA guidance to $6.5 to $8.0 billion and full year 2023 adjusted net earnings guidance to $5.50 to $7.50 per share . We now project cash from operations of $5.0 to $5.8 billion, which is expected to be relatively stable due to an anticipated release in working capital.

Looking at the table below, we see how significant these adjustments are.

{kind=link}

As explained in the company's 1Q23 earnings call , Nutrien Ag Solutions faced challenges due to delayed grower purchases and lower margins compared to the exceptional performance in 2022.

Retail fertilizer prices declined during the quarter, although at a slower rate than wholesale benchmark prices. Margins were below normal levels due to higher-cost inventory. US fertilizer inventory decreased by 10% year-over-year, leaving a significant amount of spring fertilizer volume to be procured in the second quarter.

{kind=link}

Nutrien's potash, nitrogen, and phosphate businesses experienced various market conditions. Potash sales volumes were lower than the previous year as customers purchased on a just-in-time basis, despite good initial uptake for the potash pre-fill program in North America.

Canpotex achieved record volumes to Brazil, driven by strong demand for the spring planting season and reduced imports from Eastern European producers.

Potash shipments to spot markets in Asia declined as customers reduced inventory, and contract settlements with India and China faced delays.

Global potash prices were stable initially but declined later in the quarter due to inconsistent market engagement.

{kind=link}

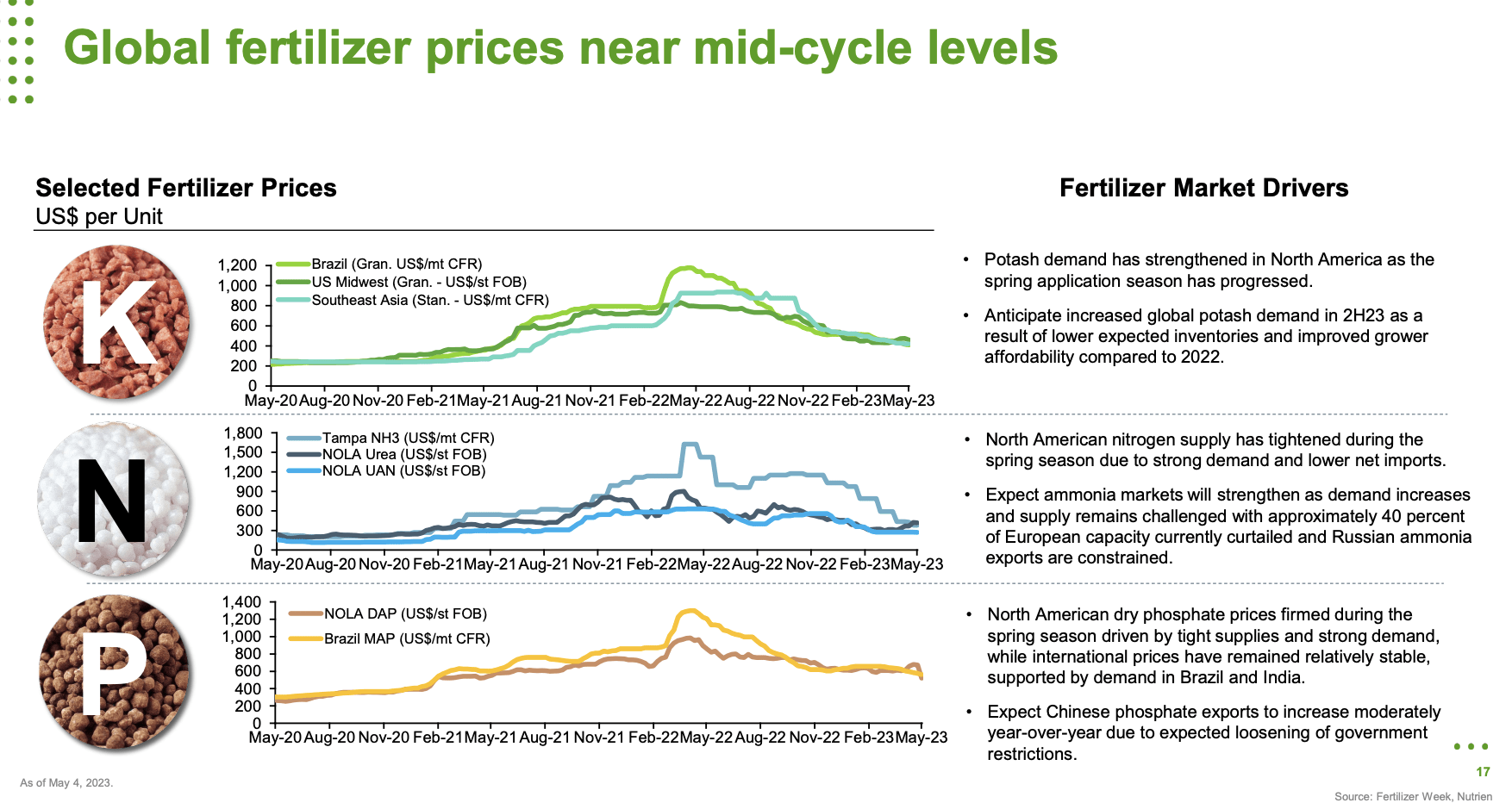

Furthermore, as seen in the charts above, nitrogen benchmark prices were highly volatile due to factors such as European gas prices, lower Indian urea imports, and weaker industrial demand.

Phosphate business results were supported by stable feed and industrial product lines, although lower sales volumes and fertilizer prices offset some gains.

With that said, none of these numbers were groundbreaking. Lower prices were somewhat obvious. The only thing that analysts couldn't predict is the timing of certain sales and some geopolitical developments.

What matters more is the outlook. Thankfully, Nutrien spent a lot of time discussing its outlook, which is also highly beneficial for people who don't invest in NTR and are just interested in the bigger agriculture picture.

Nutrien's Outlook

The bad news - for consumers - is that Nutrien confirmed that we're still in a situation of subdued supply growth.

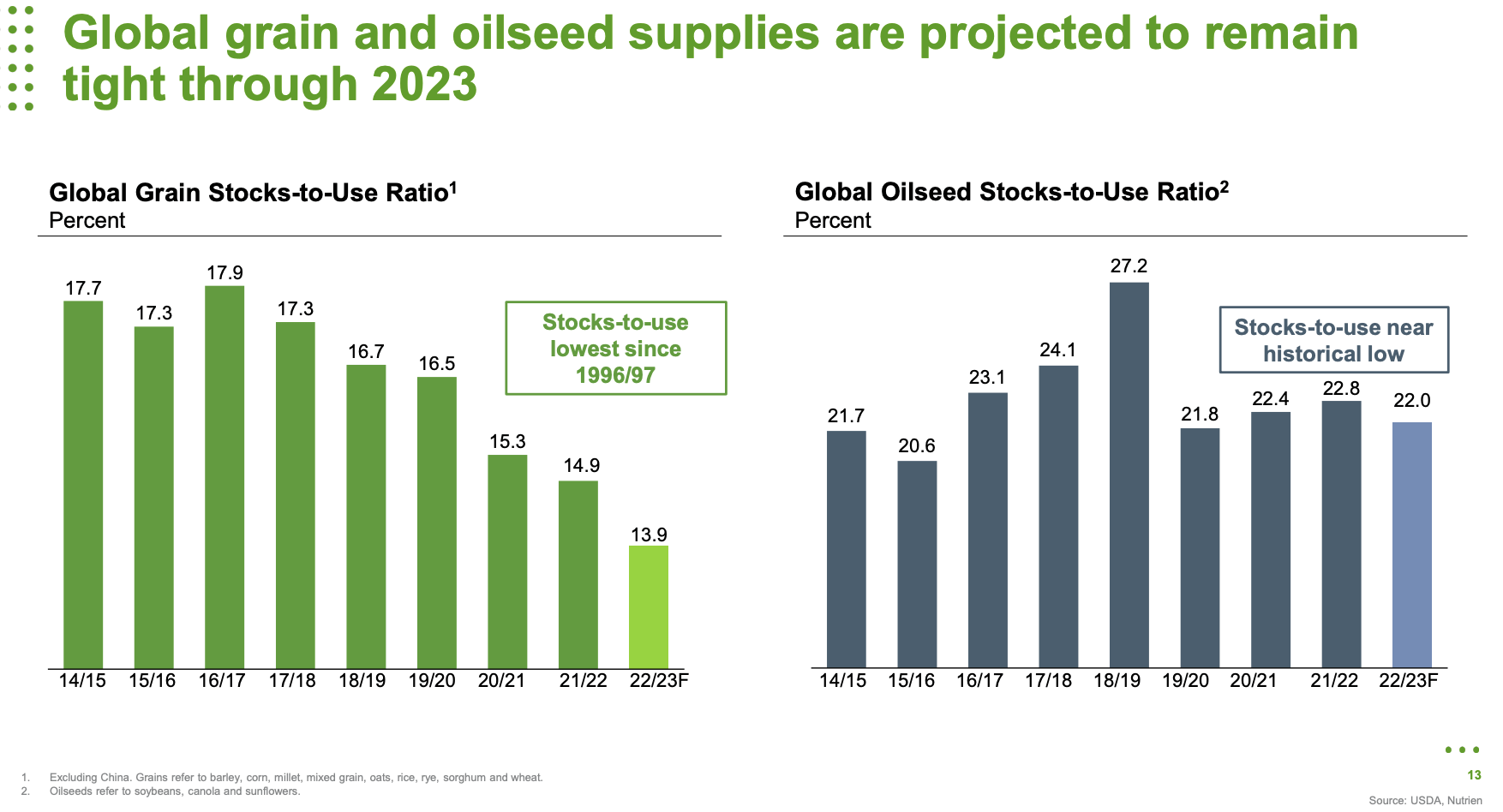

According to the company, geopolitical and weather-related challenges continue to affect global agricultural commodity markets. The global grain stocks-to-use ratio is at its lowest point in over 25 years, and it will likely take multiple cropping cycles to restore stocks to adequate levels.

{kind=link}

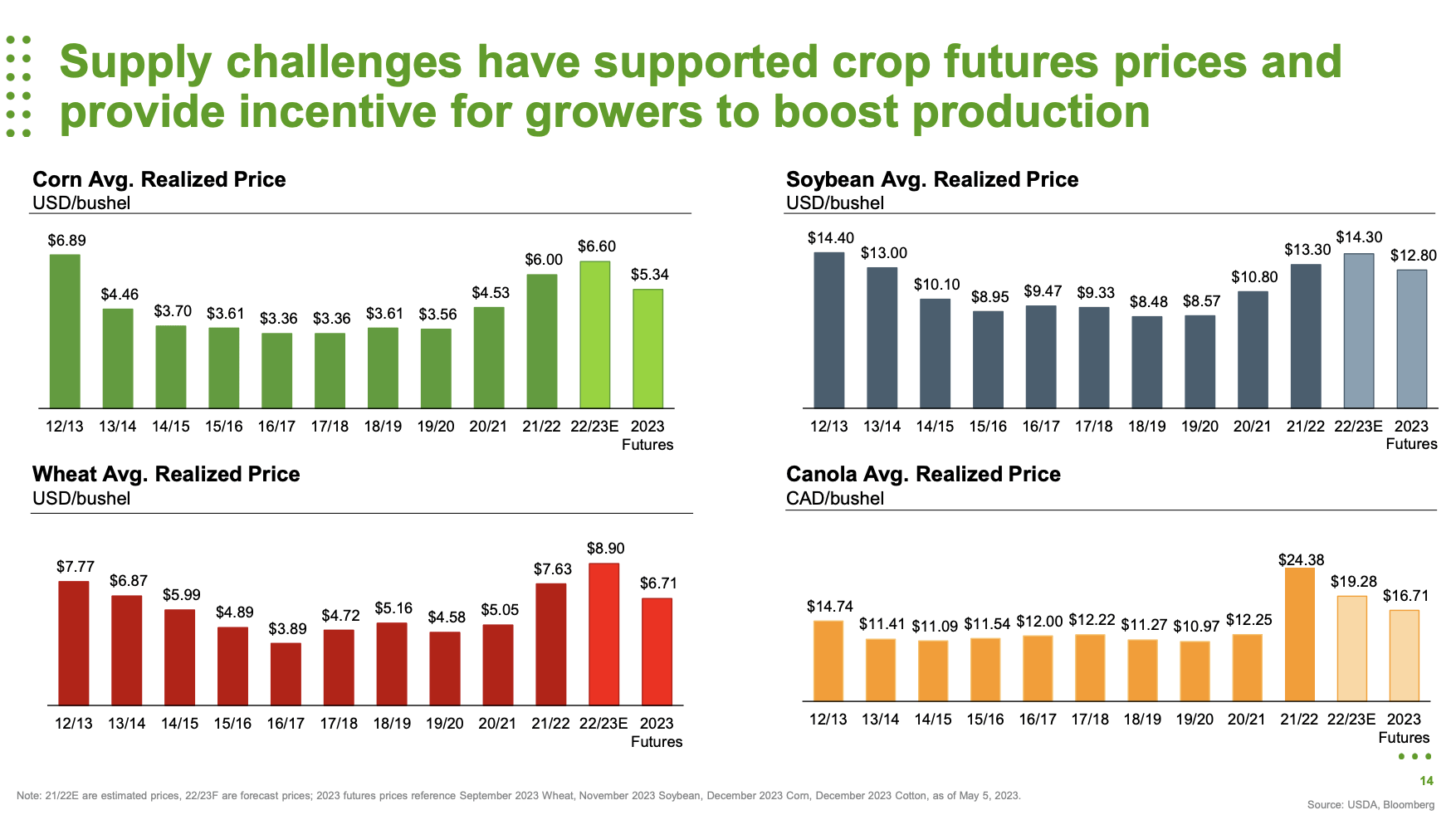

While crop prices have faced near-term pressure due to record Brazilian soybean harvest and favorable planting progress in the US, new crop futures for corn, soybeans, and wheat remain around 15% above the 10-year average. I expect these prices to remain high.

{kind=link}

In light of the poor supply situation, Nutrien saw that farmers were increasing acreage and investing in their crops, driving strong demand for crop inputs during the planting season in the northern hemisphere.

Furthermore, retail fertilizer inventories are projected to end the second quarter significantly lower than last year, highlighting the need for a strong summer refill.

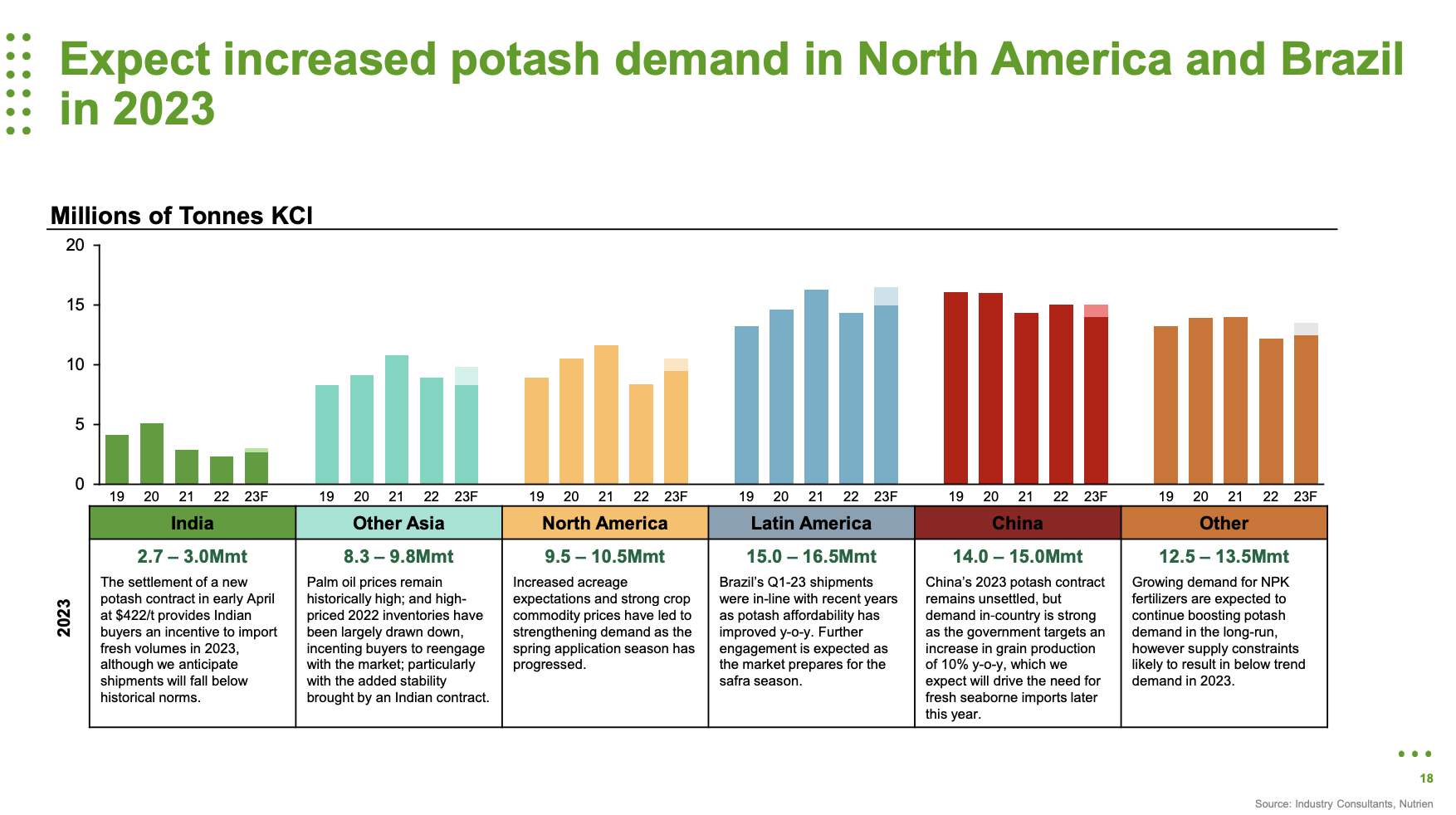

Global potash demand is expected to increase significantly in the second half of 2023, driven by Brazil and North America. Although the timing of a new China contract remains uncertain, Nutrien does not consider it a significant impediment to the recovery and global demand.

{kind=link}

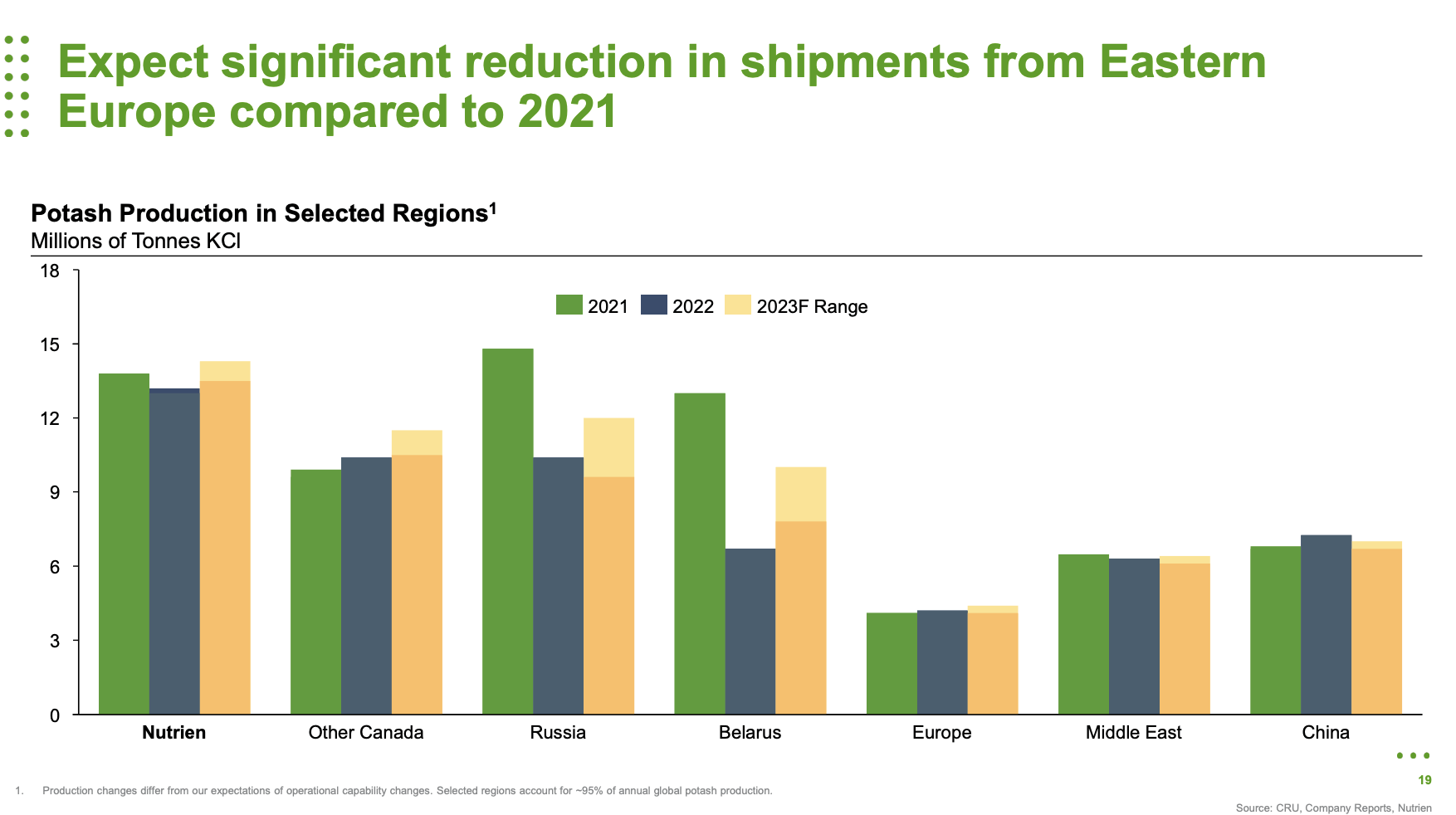

In response to these developments, Nutrien has shifted more volume to higher netback markets, and Eastern European potash shipments are projected to increase by approximately 15% compared to last year.

{kind=link}

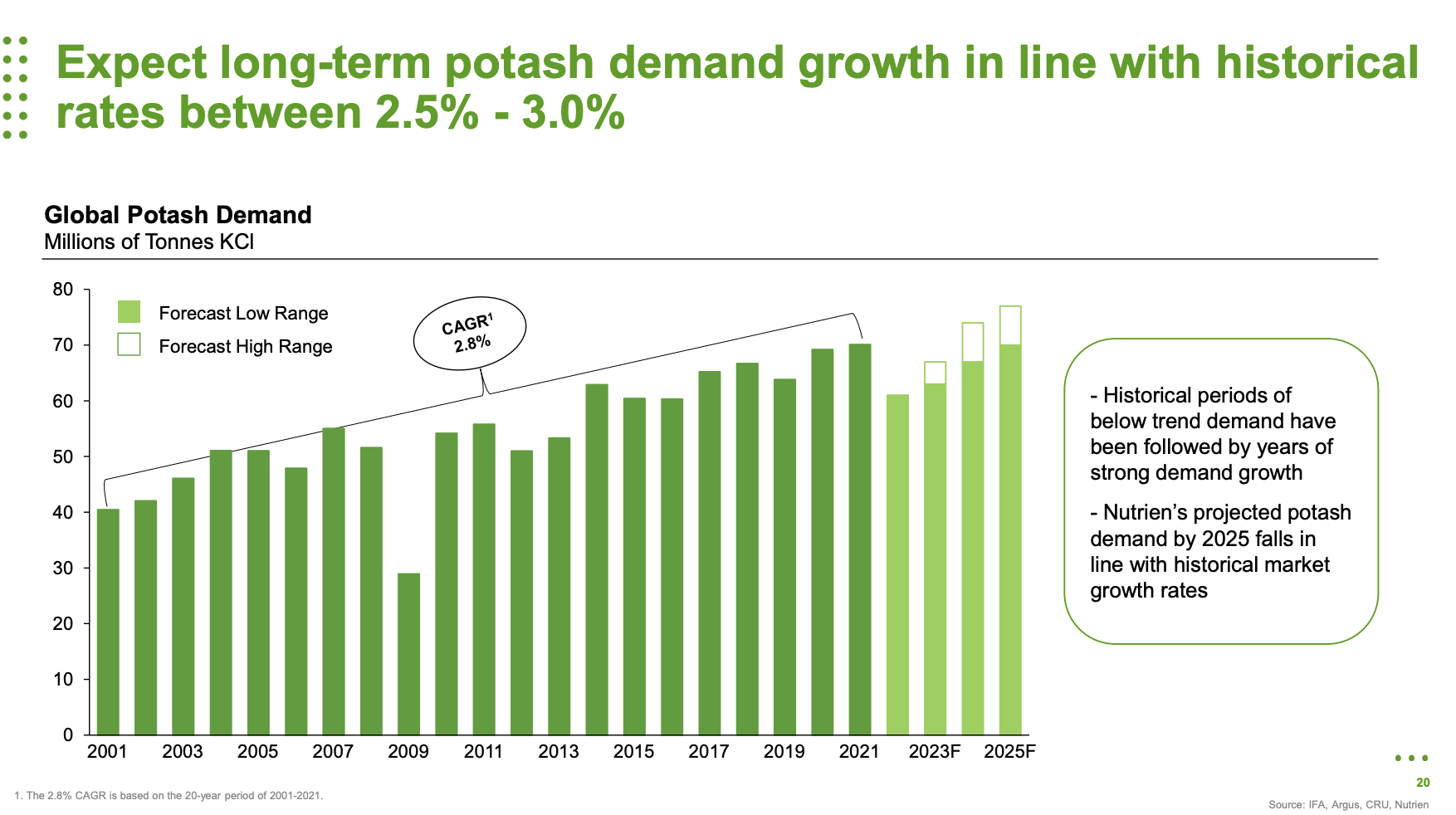

Based on these comments, Nutrien maintains a global potash shipment forecast of 63 million to 67 million tonnes, below the estimated trend demand of over 70 million tonnes, which is bullish.

{kind=link}

The company expects increased demand as markets stabilize, supported by global crop production growth, lower channel inventories, and the need to replenish potassium levels in the soil.

With all of this in mind, there are a few more things that need to be mentioned.

- Due to delayed contract settlements and slightly higher export volumes from Eastern Europe, NTR has adjusted its 2023 potash sales volume guidance to 13.5 million to 14.3 million tonnes. In light of these temporary headwinds, the company plans to maintain a flexible approach to potash ramp-up and align capital expenditures with the expected recovery in demand. In other words, we can expect that the company will reduce the speed of the expected longer-term ramp-up in potash production.

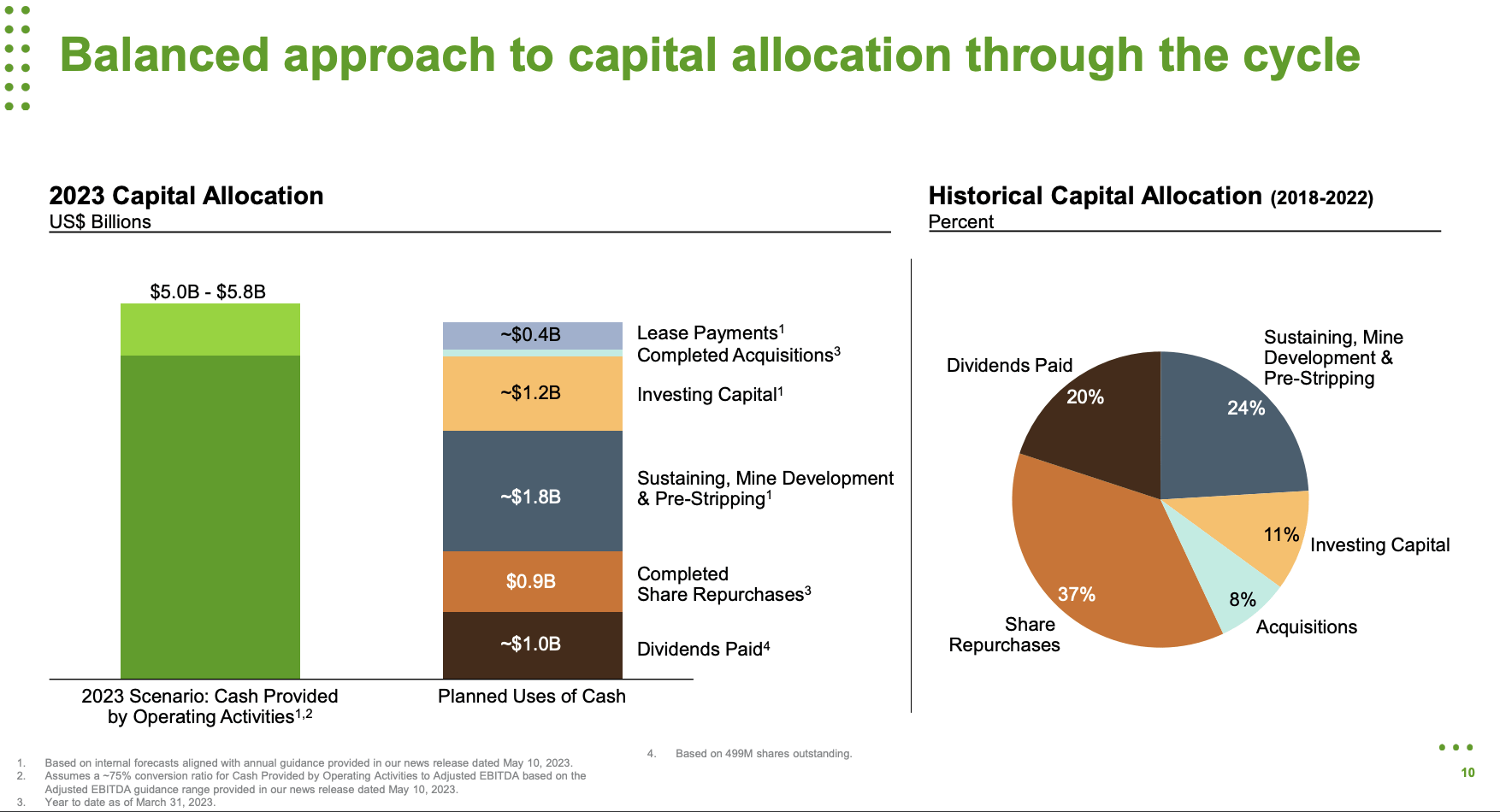

- NTR allocated $900 million to share repurchases in the first quarter and intends to remain opportunistic, taking advantage of existing and future opportunities. Since 2018, roughly 37% of the company's capital has been spent on buybacks.

{kind=link}

- In February, NTR hiked its dividend by 10%. NTR's stock currently yields 3.6%.

- Cash from operating activities is projected to range from $5 billion to $5.8 billion in 2023, representing a relatively small decline compared to previous forecasts.

Valuation

Since my last article roughly four weeks ago, analyst estimates have come down a lot.

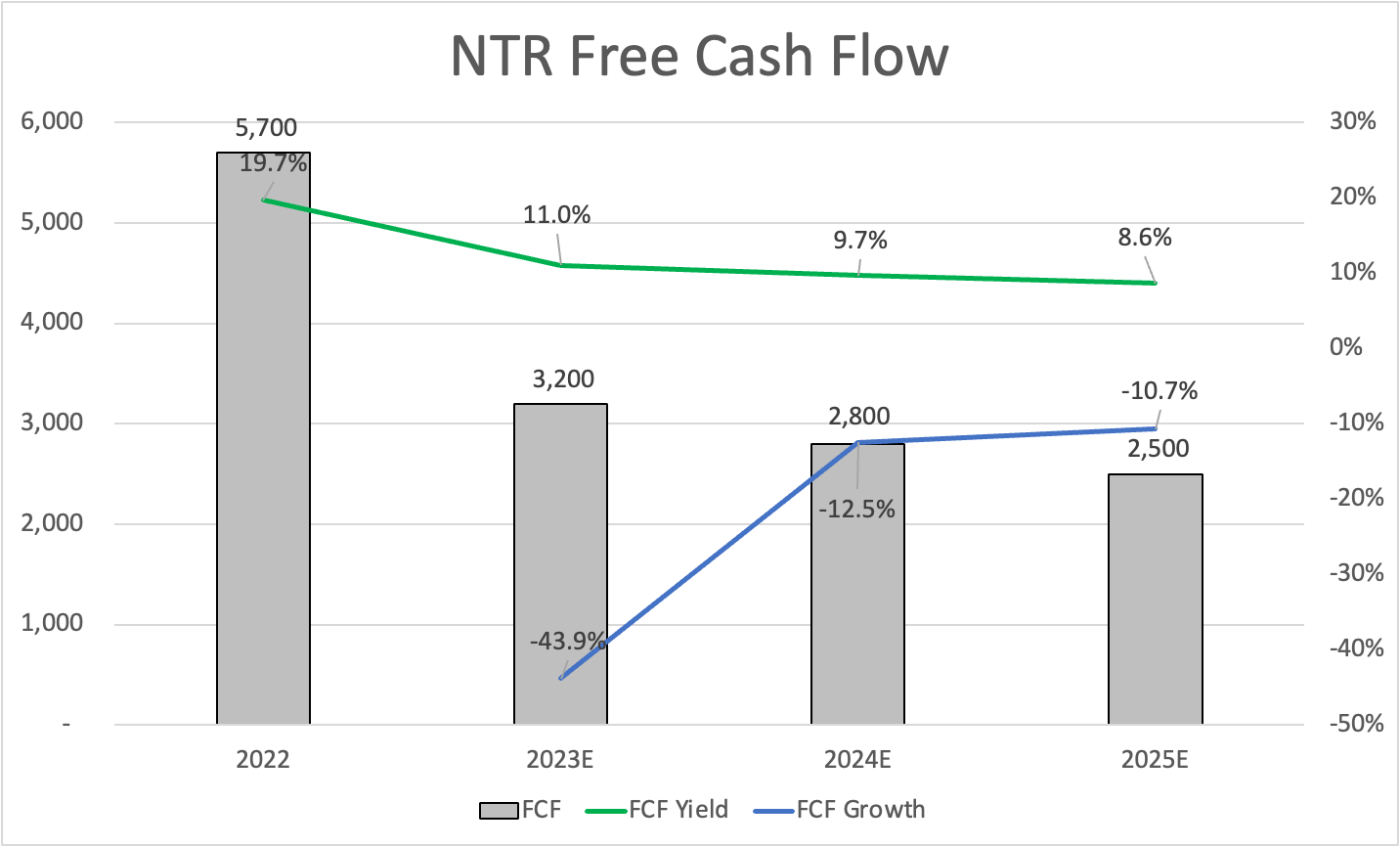

This year, analysts expect the company to generate $3.2 billion in free cash flow. That's down from $4.5 billion. Next year, that number is expected to be $2.8 billion instead of $4.0 billion. In 2025, free cash flow is expected to decline by another 11% to $2.5 billion (versus prior estimates of $3.4 billion).

{kind=link}

Furthermore, NTR is now trading at 5.6x NTM EBITDA, which is up from 5.0x EBITDA - despite the decline in its stock price.

In this case, I believe that the valuation will come down. I think actual numbers in 2024 (and likely even 2023) will be higher than expected. Due to the poor first quarter, analysts have now become too bearish - in my opinion.

I also believe that NTR will generate close to $4 billion in 2024 free cash flow, which leads me to stick to my target price.

While the consensus stock price target has come down from $90 to $78, I will stick to the $90 price target, which implies a 50% upside potential.

On a longer-term basis, I believe that NTR will rise to $120 and beyond, which is mainly based on my outlook for energy and the impact this is likely to have on agriculture.

Needless to say, NTR is highly volatile and needs to be handled with care. While I'm not betting on it, NTR could fall to $40 if we were to enter a full-blown recession.

FINVIZ

Nonetheless, even when incorporating the downside risks, I like the longer-term risk/reward a lot.

Takeaway

Despite the recent setbacks in Nutrien's earnings report, my bullish stance on the company remains intact. While the stock price has taken a hit, it presents a favorable opportunity for investors, and I have continued to add to my position.

The fundamentals of the fertilizer industry, particularly potash, remain strong due to geopolitical developments, increased affordability, and the need for higher crop output.

Nutrien's poor first-quarter results were largely expected, and what matters more is the company's outlook.

With a subdued supply growth situation and strong demand for crop inputs, Nutrien is well-positioned for success in the long run.

Although there are short-term uncertainties, such as delayed contract settlements and geopolitical factors, the company's flexible approach and strategic shifts in market focus indicate a positive outlook.

With a potential mid-term price target of $90, Nutrien offers an attractive risk/reward profile for investors willing to weather the volatility.

For further details see:

Why Nutrien Is Still A Strong Buy