PBR - Why Petrobras Stock Is Set To Keep Soaring

2024-01-12 11:09:20 ET

Summary

- Today I'd like to test the strength of my previous 'Buy' thesis on Petrobras and find out what potential investors and current shareholders should expect from the company.

- Petrobras announced plans to increase its capital spending to $102 billion by the end of 2028. But this move seems to be priced for dividends, as far as I see.

- PRB and PBR.A have an upside potential of 16.35% and 9.88%, respectively, according to Goldman Sachs. My calculations show even more upside potential for Petrobras in 2024.

- So I am willing to reiterate my previous Buy recommendation on the stock because, despite higher capital expenditure in the coming periods.

Introduction

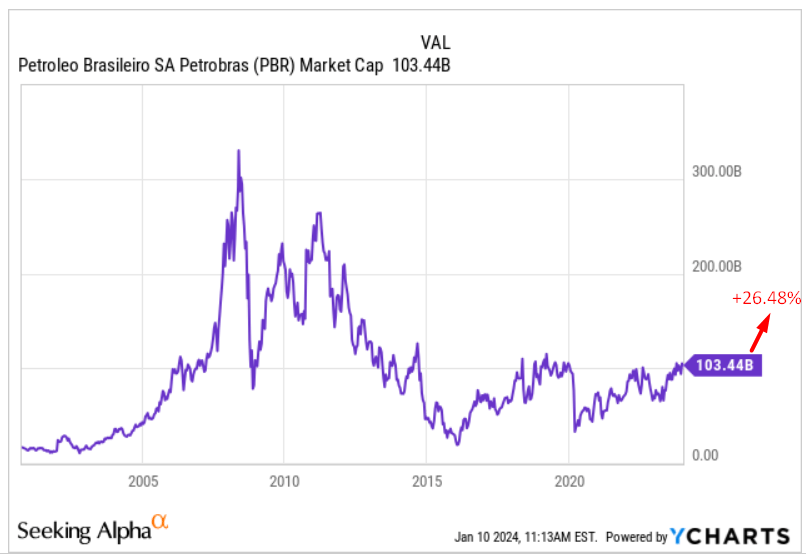

Petrobras, officially known as Petróleo Brasileiro S.A. ( PBR ) ( PBR.A ), is a major Brazilian oil and gas company with a market cap of $103 billion. Operating domestically and internationally, Petrobras is involved in various aspects of the energy industry, including exploration, production, refining, transportation, marketing, and trading crude oil, natural gas, and related products. Additionally, the company is engaged in the production of biodiesel, ethanol, and other energy-related activities. Petrobras is a significant player in the global oil market, ranking among the top 10 oil producers and top 5 exporters of crude oil. In Brazil, it holds a dominant position, contributing to over 90% of the country's oil and gas production . The company is structured into 3 main segments: Exploration and Production, Refining, Transportation and Marketing, and Gas and Power.

I last wrote about Petrobras in October 2023 , when 1 share was trading at $14.72. Today, the Petrobras stock is trading at $16.04. The total return since the inception of my buy recommendation has been about 12%, slightly outperforming the return of the S&P 500 Index ( SPX ) ( SPY ) over the same period.

{kind=link}

In October, I wrote that the company’s high dividend, high operating efficiency, and some projects in promising regions put PBR in line with other western O&G majors; in many ways, PBR looked even better. Today, after 1 quarter, I want to test the strength of my thesis and find out what potential investors and current shareholders should expect from the company.

Recent Financials and Business Developments

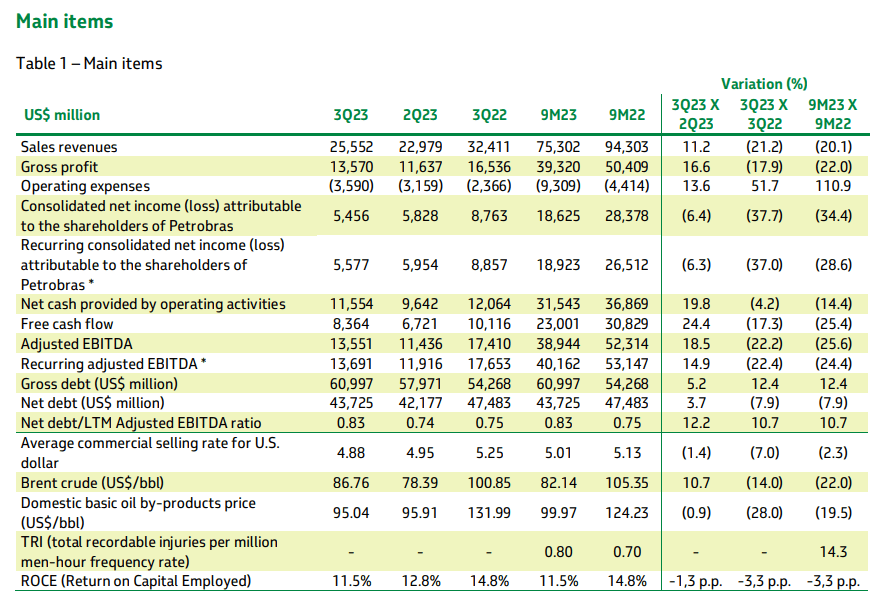

The company released its Q3 FY2023 results on November 10, 2023 . It was a tough quarter for oil and gas producers in general as market players experienced a 14% decrease in Brent, a 16% reduction in the crack spread of diesel, and a 7% decline in fields. But Petrobras demonstrated resilience with a 15% growth in adjusted EBITDA QoQ (but -22.2% YoY), strong operational cash flow generation (4th highest ever), and free cash flow aligned with growth at $8.4 billion.

{kind=link}

PBR reached some operational milestones, including record-breaking production of 22.25 boed from gas, utilization of the refining park at 96%, and significant achievements in pre-salt natural gas processing.

The firm maintained a net debt-to-EBITDA ratio of less than 1 with a well-structured debt of $61 billion, of which $29 billion constituted financial debts with an average term of 11.5 years. Cash on the balance sheet kept recovering, amounting to $13.41 billion (~13.7% of the whole market cap).

Petrobras also initiated a share buyback program, acquiring 35% of the approved 157 million preferred shares. That move is going to simplify the corporate structure and bring value to common shareholders, in my view.

On November 27 , Petrobras announced plans to increase its spending to $102 billion by the end of 2028, surpassing the previous five-year plan's estimate of $78 billion for the 2023-27 period. The majority of this spending, 72% of the total, is allocated for oil and gas exploration and production, to raise average output from 2.8 million boe/day to 3.2 million by FY2028. Notably, investments in low-carbon and decarbonization projects are set to double to $11.5 billion. Petrobras CEO Jean-Paul Prates emphasized the importance of continuing oil production to fund renewable energy initiatives, stating that abruptly halting oil operations would hinder investments in clean energy. The plan also includes the resumption of operations at one fertilizer facility by the end of next year and the completion of construction on a second plant by 2028. The company terminated the planned $34 million sale of its Lubnor refinery due to non-compliance by the buyer, adding complexity to Petrobras' strategic moves.

Investment banks - I mean their equity research teams - reacted differently to PBR's new strategic plan.

JPM's analysis [proprietary source] expresses disappointment in the modest 4.8% increase in oil production for FY2024, contrary to expectations of a more positive revision due to FPSO schedule anticipation. While the forecasted FCF is expected to rise by 6-9%, JPM's report underscores a 30-35% reduction in dividend potential compared to the previous plan , attributing it to increased spending and the absence of asset sale proceeds. The analysis suggests a lower risk to dividends in the shorter term due to significant CAPEX increases post-2024.

On the other hand, Goldman Sachs' analysis [proprietary source] of Petrobras' new strategic plan suggests a generally positive outlook. GS analysts highlight the impact of inflation, new projects, and a focus on pre-salt areas in the Exploration and Production (E&P) segment. The production growth expectations, including the addition of FPSOs to the fleet, are seen as somewhat conservative but are accompanied by a faster ramp-up rate of production. GS analysis underscores Petrobras' wind-generation projects, emphasizing the strategy of acquiring operational assets and partnerships. Goldman believes the strategic plan aligns with market expectations, removing an overhang from the stock .

So who should we believe?

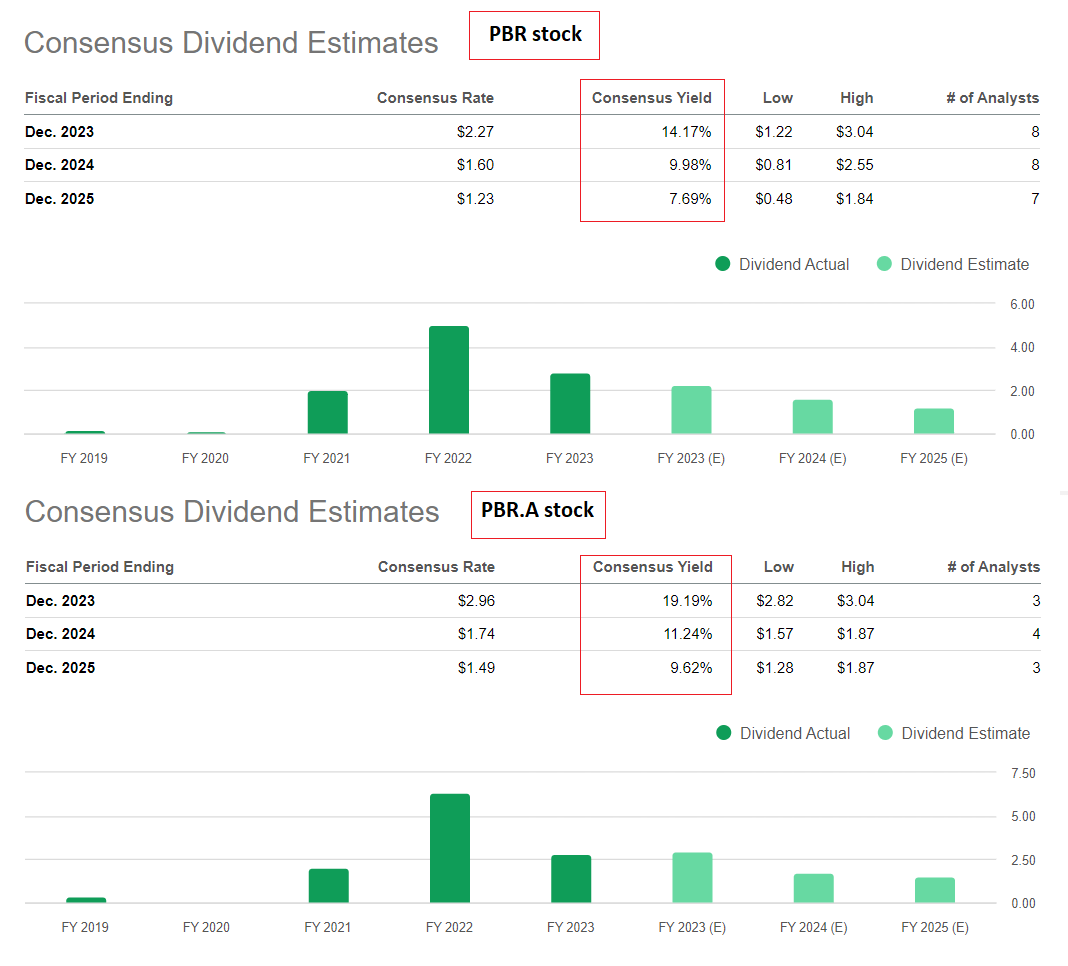

I look at PBR's moves in a more positive light. This strategic plan is necessary for the company to renew itself and become a long-term leader in the industry. What is important today is the question of the sustainability of the company's dividends, because you can talk about a wonderful distant future for as long as you want, but if the dividends fall sharply, it will not make investors happy. The advantage of PBR today is that the market already knows about the dividend payout fall in FY2024 and FY2025 . And even taking that into account, we still see a very attractive yield for the stock.

{kind=link}

The big wild card here will be the momentum of commodities this year. But today we are dealing with a growing likelihood of a relatively rapid reversal of monetary policy, which in theory will drive up the prices of everything that tends to burn (economic activity is increasing due to more accessible credit, and demand for fuel is rising).

I think that Petrobras will continue to expand its operations despite the high volatility of oil and gas prices, which, against the backdrop of continued cost-cutting efforts, will ensure a certain stability of earnings sufficient to maintain the dividend yield in the medium term (2-3 years). To check the relevance of this argument, I would first look at how the margin indicators will behave in the foreseeable future.

The question of whether it still makes sense to hold or even buy PBR stock should be based on the current state of the company's valuation.

Valuation Of Petrobras Stock

The first thing that struck me was the still incredibly high FCF yield that PBR has maintained despite all the difficulties in the industry in recent months.

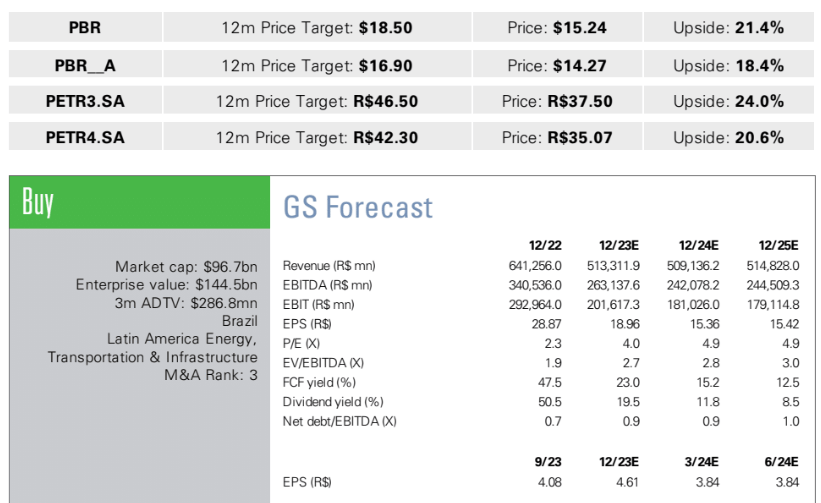

This is the metric that Goldman Sachs analysts use to estimate the fair value of a company. According to their calculations, PRB and PBR.A have an upside potential of 16.35% and 9.88%, respectively, if we convert the outputs of the bank's model to today's market prices.

Goldman Sachs, November 2023 [proprietary source]

{kind=link}

Please note that we are talking about the growth potential of a share in nominal terms and not in full. This means that double-digit dividend yields need to be added to the indicated upside potential figures to get the actual return the bank is projecting for this year.

I would like to add my contribution to the bank’s conclusions and calculate a price target not from FCF but from EBITDA and the corresponding valuation multiple. We see today that PBR's EBITDA margin continues to decline from its all-time high [in 2021], although it is still relatively high to date.

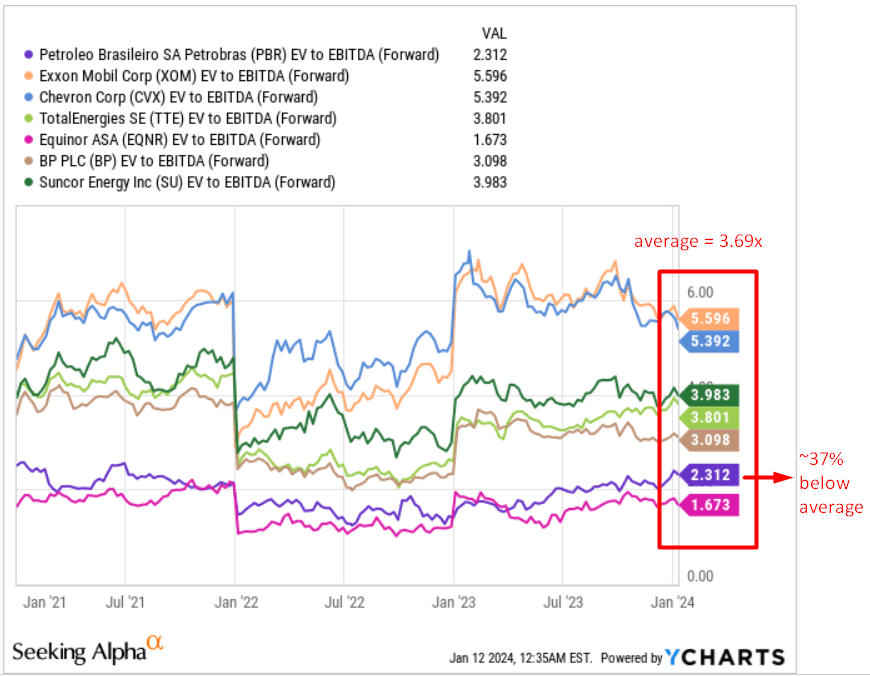

Let's assume that the EBITDA margin falls to 45% in FY2024. With a consensus forecast for revenue of $99.02 billion, this gives an implied EBITDA of $44.56 billion for the year. The EV/EBITDA ratio for next year is slightly higher than the TTM, but the figure of 2.3x is still too low to be sustainable in my opinion. It would be fair to assume that PBR's EV/EBITDA will continue to rise in 2024 and reach 4x. PBR's enterprise value should then be $178.24 billion, which corresponds to an equity value of $ 130.83 billion after adjusting for net debt. That's an upside potential of ~26.48% in a matter of 12 months.

{kind=link}

In my last article, I didn't mention such specific price targets as I do today. At that time, I concentrated mainly on the valuation of comparative multiples. It is worth noting, however, that today PBR's EV/EBITDA multiple is still significantly lower than the average of its Western peers. Despite the existing geographic risks, I believe this discrepancy only reinforces my calculations above.

{kind=link}

The Bottom Line

Of course, my thesis has its share of potential risks that I might be underestimating (but you definitely shouldn't). Various investors express concerns about Petrobras, ranging from overlooked cost management and unclear pricing policies to the possibility of unprofitable investments, especially with recent news hinting at increased drilling activities in the coming years. Additionally, Petrobras is contemplating venturing into offshore wind, a move surrounded by regulatory and financial uncertainties. Critics argue that the company should stick to its core activities. The revised dividend policy may also result in dividend cuts, a factor currently factored into the company's modest valuation levels.

Despite these risks, I am willing to reiterate my previous Buy recommendation on the stock because, despite higher capital expenditure in the coming periods, the company remains one of the cheapest among the majors and also one of the most efficient, given how resilient its financials have been in the recent period of falling commodity prices.

The conclusions of my valuation calculations, which are supported by Goldman Sachs' models, indicate that PBR stock still has tangible growth potential in 2024.

Thanks for reading!

For further details see:

Why Petrobras Stock Is Set To Keep Soaring