CVNA - Why Root's Management Doesn't Want To Sell For $19.34

2023-07-06 07:36:13 ET

Summary

- On June 21, 2023, per the WSJ, it was reported James Hall made a $19.34 cash bid for Root, Inc.

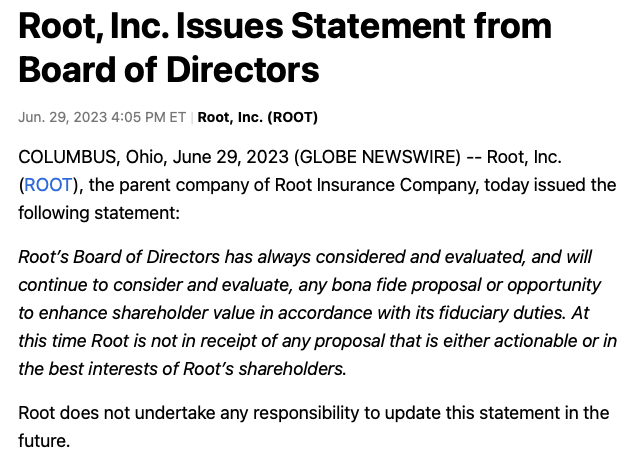

- On June 29, 2023, after the bell, Root's Board of Directors wrote a strangely worded statement, to dispel the legitimacy of the Hall bid.

- Although I think the James Hall bid is highly credible, at least logically and based on the evidence, I write to share the fundamental long case.

On June 21, 2023, per the WSJ, it was reported that James Hall , Founder & Executive Chairman, of Embedded Insurance submitted a formal cash bid, to the Board of Directors, to buyout Root, Inc. ( ROOT ) for $19.34 per share. The WSJ article exclusive was published at 3:24pm, over just less than forty minutes before the end of the trading day. Shares of ROOT were halted and quickly reopened just before the market closed, that day. The next day, June 22, 2023, on super elevated volume, with 9.75 million shares changing hand, ROOT share briefly traded up to $14.80, before retreating.

On June 29, 2023, after the bell, the Board of Directors, at Root, made this statement:

{kind=link}

In after-hours, on June 29th, ROOT shares briefly trade down into the $7s before rebounding to $9. Since then, the stock has been very volatile and trading within a range of $8.42 to $10.60.

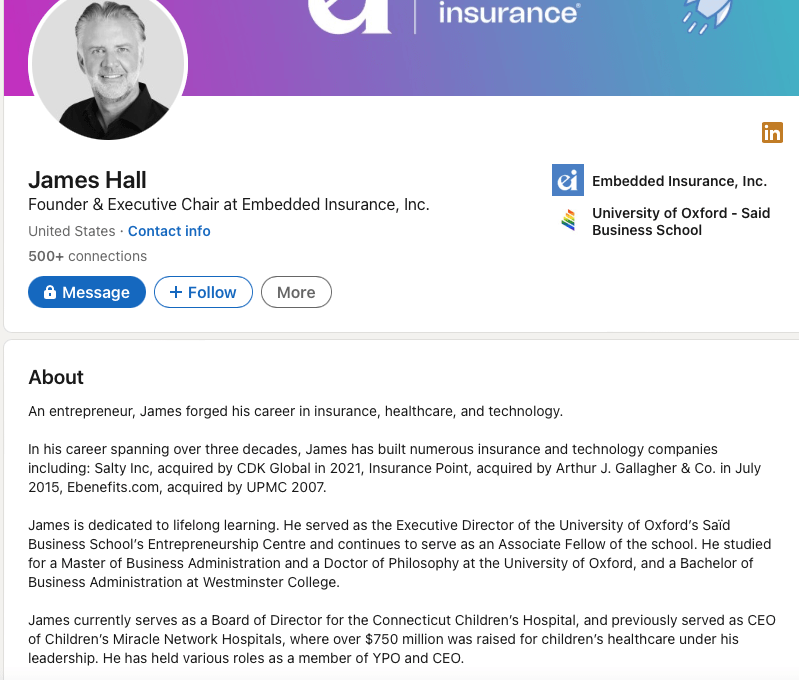

To be crystal clear, at face value, and according to his LinkedIn profile, I would argue it is highly probable that James Hall is very credible and has formally bid Root to buy the business. Legal semantics notwithstanding, if readers take five minutes to synthesize Mr. Hall's background, they quickly see he has bought and sold more than one business. Secondly, he is currently working in the same industry and is focused on the embedded side of the insurance industry.

{kind=link}

Thirdly, as a University of Oxford Phd, and although there are always the occasional Elizabeth Holmes of the world, I find it extraordinarily unrealistic, bordering on fantastic, that Mr. Hall was catfishing the WSJ.

James Hall's Education (per LinkedIn)

Now that we covered the brief history and looked at James Hall's background, I write to share my thought process and make a fundamental case as to why Mr. Hall or another companies might want to buy actually Root, Inc., the business.

The Fundamentals

The Business

Root is a technology company that is trying to disrupt the slow and stodgy insurance industry. The company sells short tail products (automobile insurance, renters insurance, and homeowners insurance). The automobile insurance industry is large, with approximately $273 billion of annual premium dollars. The company has aggressively invested in its technology stack, which enables consumers with the ability to shop, get a quote, and ultimately purchase insurance, via their smartphones.

The company operates an embedded insurance model and Carvana ( CVNA ) is the company's first partner. Embedded insurance is arguably the future of insurance and Root is (arguably) way out in front here.

Enclosed below is one technical definition of embedded insurance:

Embedded insurance is a type of bundling and sale of insurance coverage or protection while a consumer is purchasing a product or service, bringing the coverage directly to the consumer at the point of sale .

(Source: Cover Genius)

To picture it, think of buying insurance on your new iPhone or Samsung Galaxy smartphone, at the time of purchase, at the Verizon Wireless, AT&T Wireless, or T-Mobile store. Or think of buying insurance, at the time of purchase, at Home Depot ( HD ) on a basket of home appliances. Additionally, if you buy expensive electronics, at Best Buy ( BBY ), you might consider buying insurance. These are all real world examples of embedded insurance.

Besides the significant investment on technology side of the business, the company's underwriting practices are different in that they want to evaluate insurance risk, at the individual level, as opposed to pricing it on aggregate basis, using the 'law of large numbers'. In others words, the traditional model was that the large players would figure out expected aggregate losses, on a large pool of customers, and then price their coverage similarly, albeit with some modifications and tweaks based on various/ broader risk factors, for each strata of customers.

Moreover, Root uses technology and machine learning to assess risk and behavioral data, notably using proprietary telematics.

The Past Operating Losses And The Opportunity

At face value, a casual observer might quickly glance at ROOT's historical losses and declaratively conclude ROOT will go out of business. ROOT's stock chart is really ugly, and the stock is down 98%, from its all-time highs, accounting for its 1 for 18 reverse split (effective August 12, 2022).

{kind=link}

The chart, on a one year basis, notwithstanding the high volume move, made on June 21st and 22nd, lifting ROOT shares from $6 to $14.80 (the stock actually traded as high as $15.70, in pre-market, on June 22, 2023), is similarly ugly.

{kind=link}

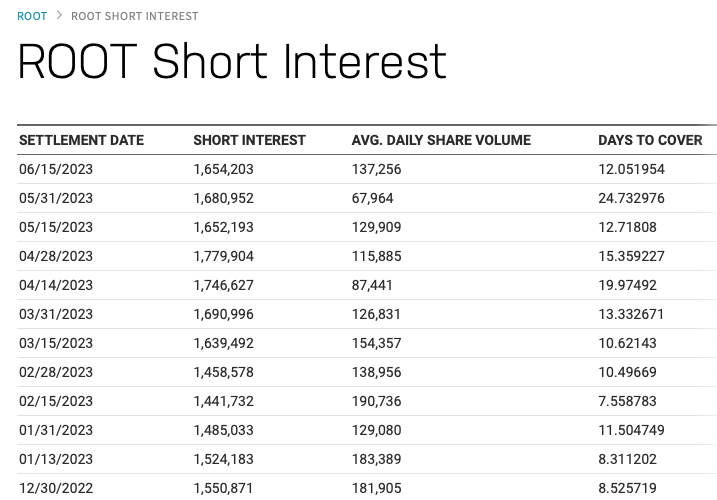

Perhaps, the shorts have been short this stock, for a long time and at a very high prices, and certainly seems like they intent on riding this stock to zero, or so they think.

{kind=link}

As I mentioned earlier, I've saved readers the trouble of digging through ROOT's past conference calls and 10-Ks and present its unencumbered capital and hefty operating losses.

Net Cash Used In Operating Activities (Cash Flow Burn Rate)

- FY 2022: -$210.6 million

- FY 2021: -$403.4 million

- FY 2020: -$287.2 million

As you see, the unencumbered capital base is relatively sizable and the speed of losses is slowing.

Trajectory Of Unencumbered Capital (period ending)

- 3/31/2023: $524 million

- 12/31/2022: $559 million

- 9/30/2022: $629 million

- 6/30/2022: $696 million

- 3/31/2022: $736 million (signed a $300 million term loan with BlackRock)

- 12/31/2021: $450 million

That said, investing, even the higher risk variety, and make no mistake here, if you're long ROOT, you're swimming in the higher risk end of the pool, is about the future.

If you actually do some real works, a clever and forward thing observer might try and work out why James Hall wants to buy this business, for $19.34 per share, in cash, a seemingly astounding 220% premium to its June 20, 2023 closing price.

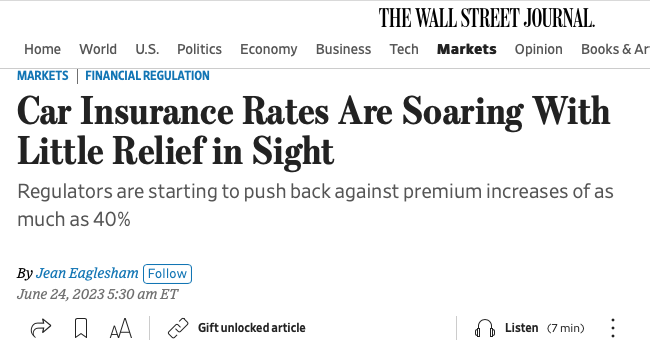

Big rates increases, lower loss ratios, and big SG&A / marketing cuts

1) Big Rates Increases on Tap

If you actually dig in, you learn that 2022 was the worst year, from a profitability standpoint, for the auto insurance industry, in thirty years!

{kind=link}

Check out these two poignant excerpts, from the June 24, 2023 WSJ article, referenced above.

Exhibit A:

Auto insurers say their rate requests are driven by necessity, not greed. The cost of claims has soared since the pandemic, due to more accidents, higher repair costs , bigger medical bills and increased litigation. Car insurers last year lost on average 12 cents for every dollar of premium written, according to S&P Global. State Farm, the country's biggest car insurer by premium volume, lost 28 cents for every dollar written last year, posting a $13 billion underwriting loss for its auto arm.

Exhibit B:

It's probably the worst period for auto insurers it's been in 30 years at least," said Neil Alldredge, chief executive of industry body National Association of Mutual Insurance Companies.

As we already established, the auto insurance business is very large, with approximately $273 billion in annual premium dollar written, as of 2022. Like or hate it, this industry plays an important role in the functioning of society. Therefore, in order for the industry to exist, it has to remain profitable, over the full business life cycle. Because of the record losses, State Insurance Regulators have little choice and have to agree to rate increases, such that we, as in the society, has a functioning automobile insurance industry.

Specifically, if we take the work a step further, and you read ROOT's February 23, 2023 Q4 FY 2022 earnings call transcript, we learn that ROOT already has in motion average rate increase of 37% because of the broader industry's big operating losses, last year.

In 2022, we implemented 53 rate filings with an average increase of 37% across our total book. We filed revised policyholder contracts in 33 markets to tighten underwriting and refine our fee schedules. We plan to increase rates again in 2023 where needed to offset loss trends from persistently higher than historical severity. The combination of rate increases strengthened underwriting and meaningful segmentation improvements continue to drive decreases in our loss ratios quarter-over-quarter, moving us closer to our long-term target of 65%.

So if you think about it, albeit with a lag, as the rate increases have to take effect, this is a big tailwind for future profitability.

2) Gross Accident Loss Ratios Rapidly Improving

During that same Q4 FY 2023 conference call, and referenced directly above, we also learn ROOT's longer term targeted loss ratio is 65%.

Lo and behold, during Q4 FY 2022 and Q1 FY 2023, we are seeing tangible evidence of that loss ratio is materially declining.

Q4 FY 2022:

The gross accident period loss ratio was 77% for the fourth quarter, a 17 point improvement versus the fourth quarter of 2021 . We have recognized and responded to loss trends early, which has driven this year-over-year improvement.

Q1 FY 2023:

The gross accident period loss ratio was 69% for the first quarter, a 13-point improvement versus the first quarter of 2022 as we recognized and responded to loss trends early. We remain committed to lowering the loss ratio and expenses to improve our financial performance and the fiscal foundation of the company.

3) Management has taken a lot of costs out of the business via SG&A cuts and Marketing Cuts

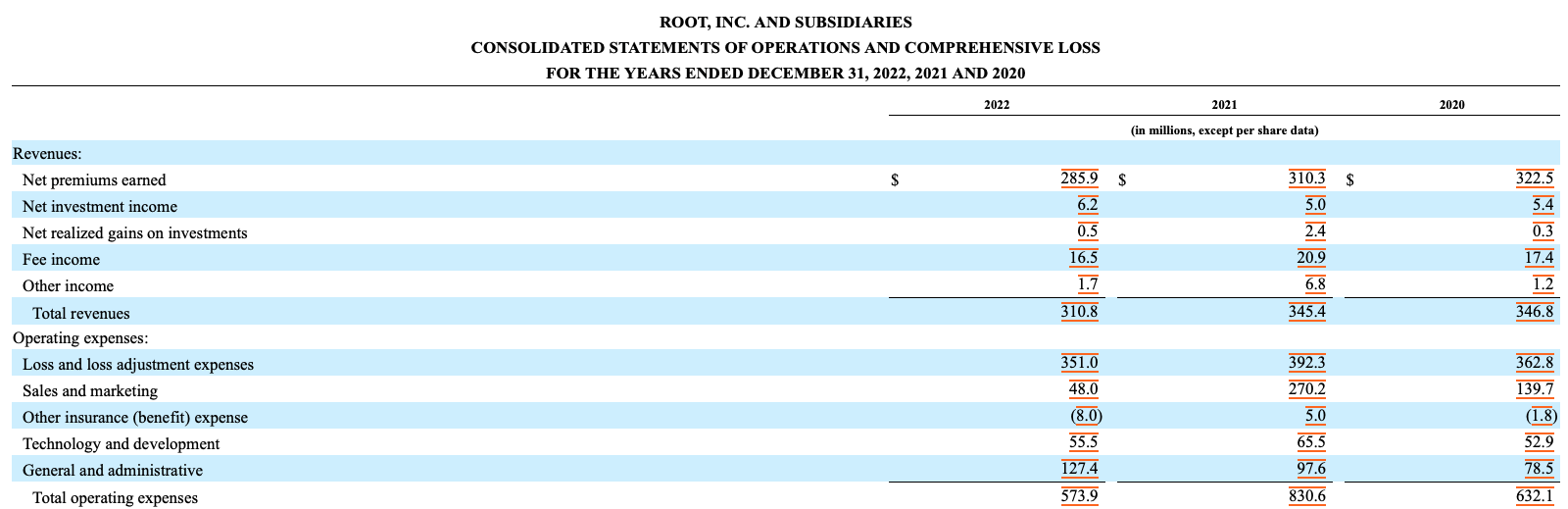

The easiest way to see this is to look at ROOT's FY 2022 10-K and simply review trajectory and declining cost of SG&A and Marketing.

{kind=link}

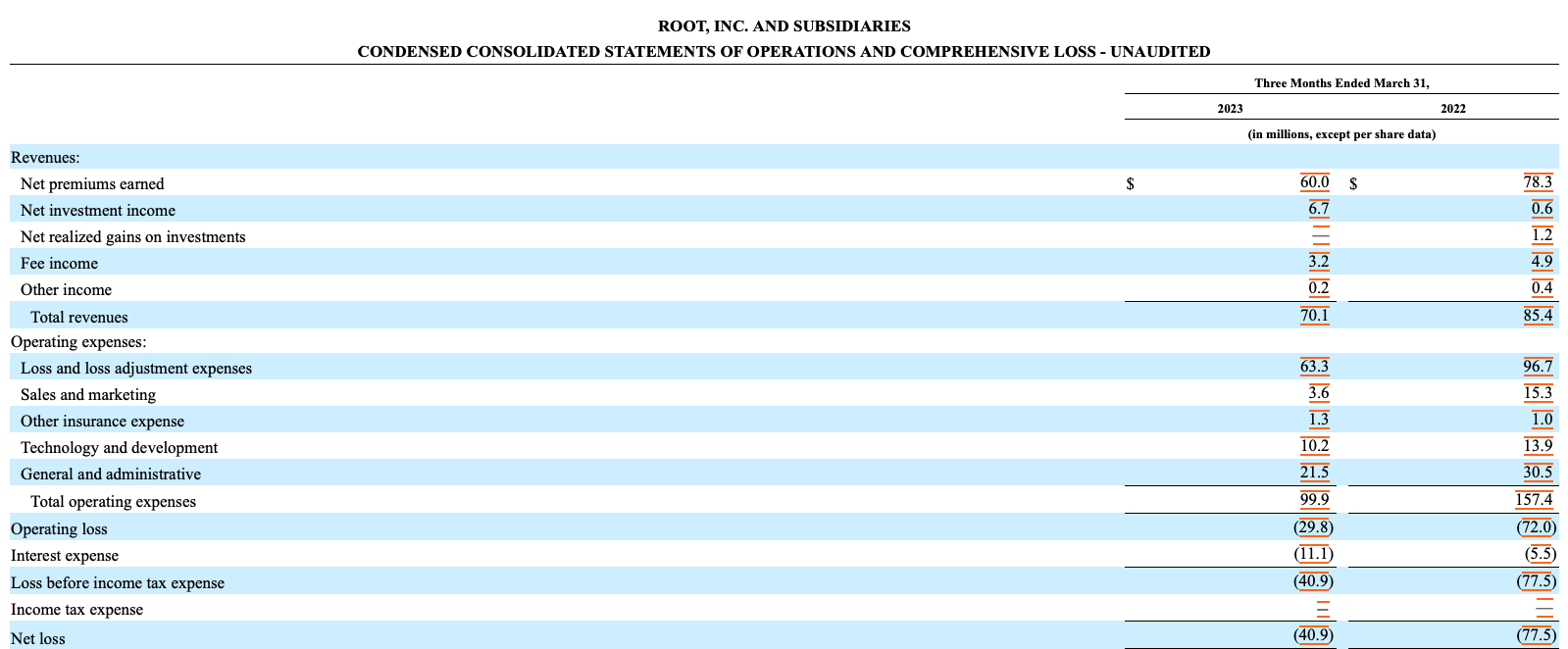

Q1 FY 2023 SG&A is down materially, as is its marketing spend.

SG&A has gone from $30.5 million (Q1 FY 2022) to $21.5 million (Q1 FY 2023) and Sales and Marketing has gone from $96.7 million (Q1 FY 2022) to $63.3 million (Q1 FY 2023)!

{kind=link}

More Green Shoots

If you take the time to understand ROOT's business model, they are marching towards an embedded model.

See here:

Furthermore, we continue to prove our differentiation in the embedded channel and are excited to announce we finalized a third partnership.

I'd like to take this opportunity to discuss the key elements of our differentiation. Having built our company on a flexible technology stack, allowing customers to get a quote without ever touching a keyboard, we are able to create seamless, real-time, quote-to-bind experiences in the moments that are most relevant to consumers. This drives adoption rates, as shown by an over 3x increase in our attach rates since launching our fully-embedded product.

Second, our platform continues to advance through our API developments, allowing us to rapidly scale and add new partnerships while materially reducing the cost and time to deployment for those partners. Putting these three things together, increasing adoption while decreasing costs and increasing speed to market, that's the differentiated value we provide to our partners.

(Source: ROOT's Q1 FY 2023 Conference Call)

And in terms of upcoming big catalysts, for both the business and the stock, ROOT already has two new embedded partners, and behind the scenes, they are working on near-term product launches.

Two New Embedded Partners:

We're also equally, if not more excited, by the two new embedded partners that we have that we think will provide substantial new writings. Now we want to launch those in the coming months. It will take time to get those products into market, but we have all the faith in the world that those are two excellent partners that will provide significant scale for the business.

(Source: Root's Q1 FY 2023 C.C. (May 4, 2023))

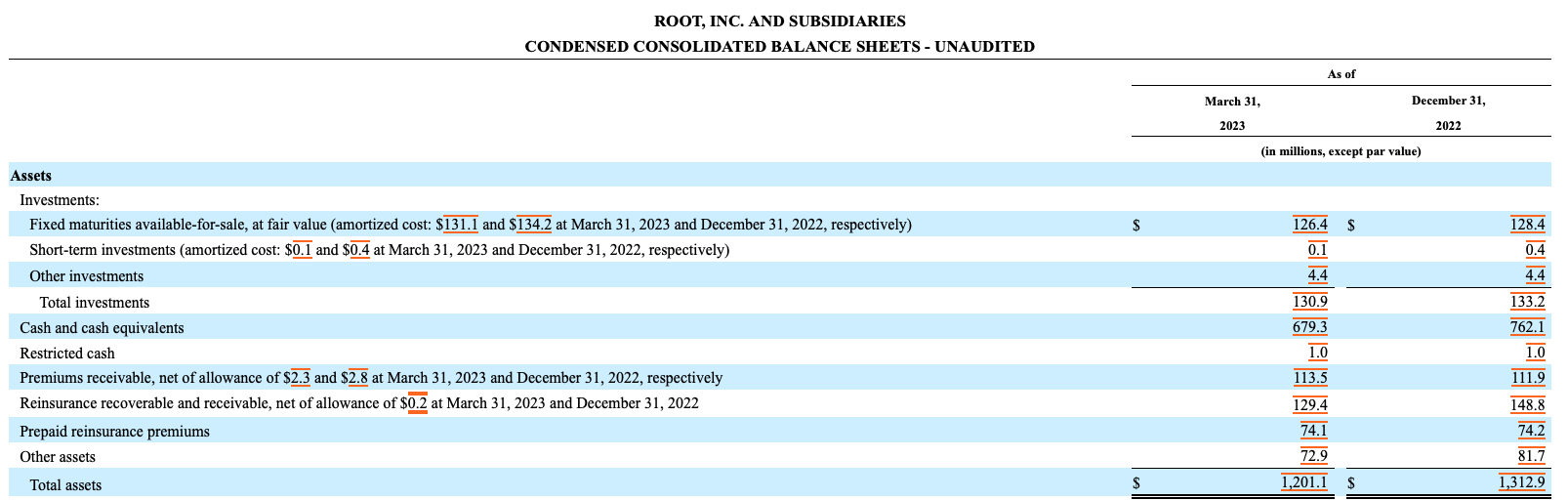

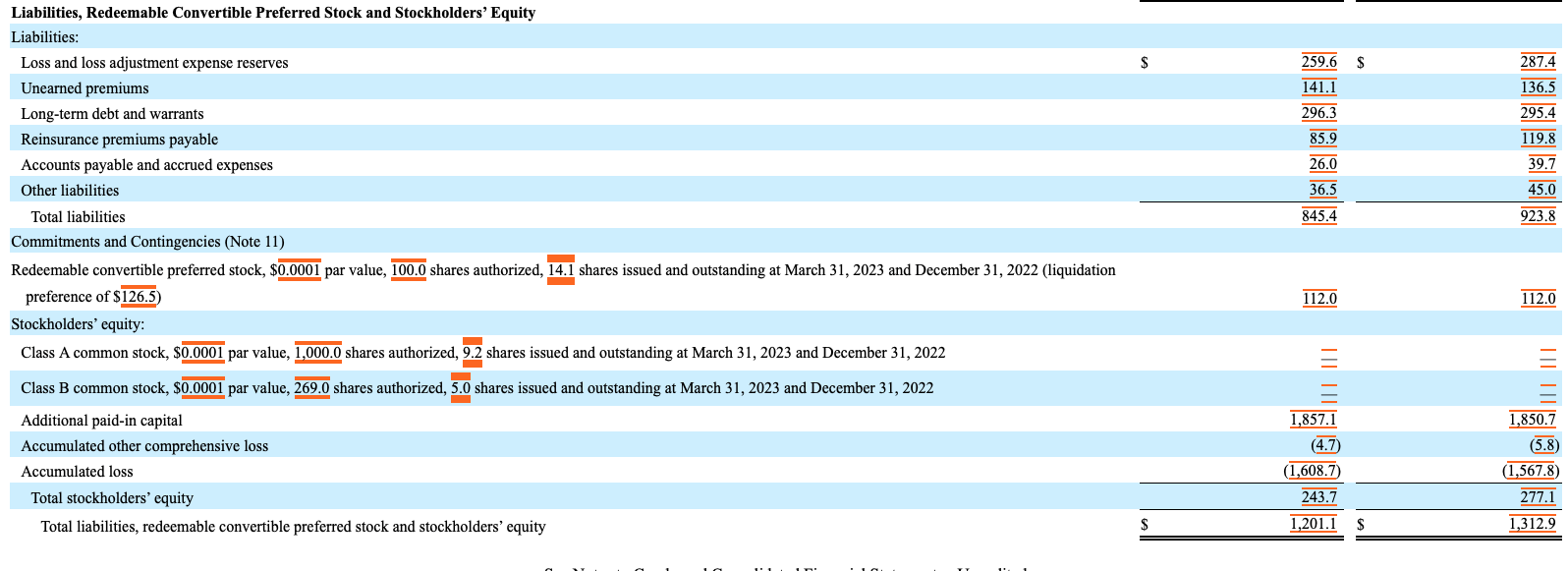

As of March 31, 2023, Root's book value is still $17.04 per share.

ROOT has 9.3 million Series A shares and 5 million Series B shares outstanding. $243.7 million, ROOT's March 31, 2023 total stockholders' equity divided by 14.3 million shares gets you to $17.04 per share of book value.

{kind=link}

{kind=link}

Other Nuances

It doesn't take a rocket scientist to hypothesize that James thinks the future of insurance is finding and attracting customers in the embedded channels.

Secondly, I find it extraordinarily unlikely that James Hall's bid wasn't real and that he was spoofing the WSJ. I'm not saying the guy is a good person or not, I don't know him, so I can't make that judgment. What I do know, though, on balance, PhDs from places like Oxford tend to be credible and care about their reputations and therefore it is unlikely that the bid was some charade.

Perhaps, the reason he hasn't taken yet taken a 5% stake and arguably why we haven't seen one activist SC 13D filers (or multiple 5% holders) is because of ROOT's dual voting class share structure, which consists of A and B shares.

Per ROOT's FY 2022 10-K:

Our Class B common stock has ten votes per share and our Class A common stock has one vote per share. As of February 16, 2023, holders of our Class B common stock collectively beneficially own shares representing approximately 83.5% of the voting power of our outstanding capital stock. Our directors and executive officers and their affiliates collectively beneficially own, in the aggregate, shares representing approximately 19.0% of the voting power of our outstanding capital stock. As a result, the holders of our Class B common stock are able to exercise considerable influence over matters requiring stockholder approval, including the election of directors and approval of significant corporate transactions, such as a merger or other sale of our company or our assets, even if their stock holdings represent less than 50% of the outstanding shares of our capital stock. This concentration of ownership limits the ability of other stockholders to influence corporate matters and may cause us to make strategic decisions that could involve risks to you or that may not be aligned with your interests. This control may adversely affect the market price of our Class A common stock.

One other nuance here that is worth mentioning, ROOT has an expensive $300 million five year term loan. In FY 2022, ROOT's interest expense was $34.6 million.

On January 26, 2022, we closed on a $300.0 million five-year term loan, or Term Loan. The maturity of this Term Loan is January 27, 2027. Interest is payable quarterly and is determined on a floating interest rate calculated on the Secured Overnight Financing Rate, or SOFR, with a 1.0% floor, plus 9%, plus 0.26161% per annum. Concurrently with the Term Loan, we also issued to the lender warrants to purchase approximately 0.3 million shares of Class A common stock. Under certain contingent scenarios, the lender may also receive additional warrants to purchase shares of Class A common stock equal to 1.0% of the aggregate number of issued and outstanding shares of our Class A common stock on a fully-diluted basis as of the triggering date.

(Source: ROOT's FY 2022 10-K)

Putting It All Together

A first level think might think ROOT's stock is destined for zero given the historical operating losses. Moreover, a pessimist might read the statement issued by Root's Board of Directors and think James Hall didn't actually bid. As I've argued, it is unlikely James Hall isn't 100% serious about wanting to buy this business.

Moreover, a second level think might actually work out that Root, Inc.'s business is inflecting. Ongoing and upcoming 37% average rate increases, much lower loss ratios, and lots of SG&A and marketing expense cuts mean the burning platform has been (greatly) extended. In addition, per Root's conference calls, they already signed two new and national embedded partners. They have near term plans of rolling out new products, with these new embedded partners, in the coming months.

This is a major catalyst.

Lastly, the tricky part and arguably why we don't have 5% holders (and activists waiting outside the gates) is due to the dual class voting structure.

On balance, I really like the risk/ reward and setup here, as there as multiple ways to win. That said, though, to be crystal clear this is definitely a high risk stock / high reward stock. The biggest risks are the operating losses and ROOT's ability to stem those operating losses and prove the business, can scale, and profitability inflect.

For further details see:

Why Root's Management Doesn't Want To Sell For $19.34