BKR - Why XLE Is My Top Pick For The (Still) Cheap Energy Sector

Summary

- Energy had a record year in 2022, but it is still a great place to put your money to work in 2023, as drivers of last year's performance are intact.

- The sector has the best-projected earnings growth in the S&P 500. There is secular price support from chronic underinvestment in production.

- The Energy sector has changed over the years to be more shareholder friendly. Valuations and capital policies are both attractive.

- The market seems to have assigned too low of a terminal value to Energy. Hurdles to renewables will continue throughout 2023.

- Many players in the Energy industry are making genuine technical strides to reduce carbon emissions, which undercuts anti-industry arguments.

At the end of the day, the intrinsic value, determined by the present value of future cash flows, attracts the price like a magnetic force. This means that investors always have to keep in mind the value drivers of a discounted cashflow model. -Michael Mauboussin and Dan Callahan, Everything is a DCF Model

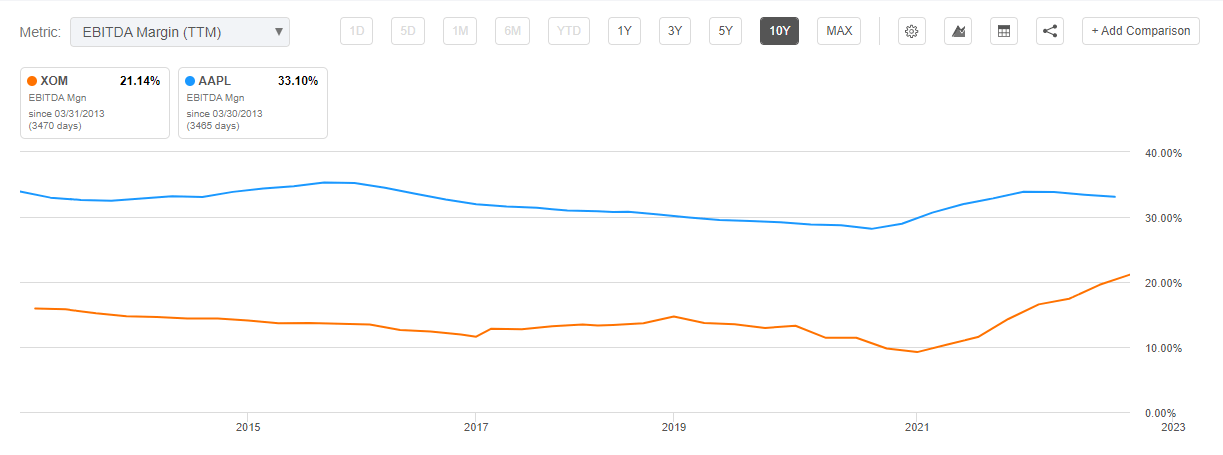

Discounted cash flow models can seem very complicated to the outsiders of financial discourse. However, you don't really have to dive into the numbers to understand the thrust of their output. Qualitatively, questions like: What do I think will make more money in ten years? Company X, or Company Y. Or, or sector X versus sector Y. The oil majors are consolidated and comprise a significant portion of the Energy Select Sector SPDR Fund ( XLE ). Thus, I will use Exxon (XOM) for our opening comparison to consider the Energy Industry in a different light than the heated discourse around climate change often casts. Exxon is a huge company, and aside from Apple (AAPL) dwarfs all the other companies shown above in terms of revenue. It's had a bumper year and has made investments to future-proof itself, yet it trades a significantly lower multiple than companies across a few different sectors.

{kind=link}

Seeking Alpha

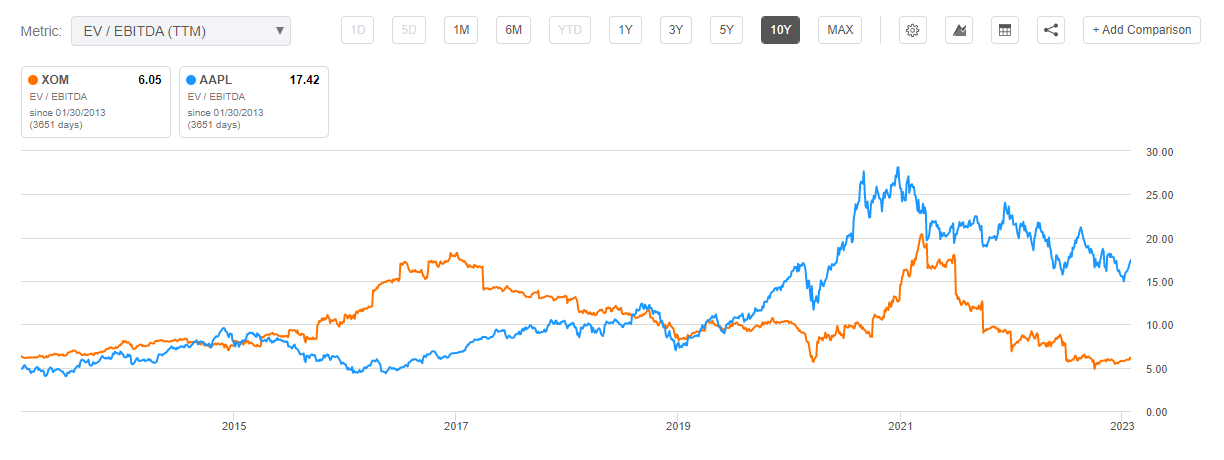

Exxon Mobil was the world's largest company before Apple usurped its position. This happened for the first time in 2011 . Apple's price performance has trounced Exxon's since then. I suspect the larger-than-ever spread in valuation along the lines of EV/EBITDA will somewhat narrow in the first half of 2023 because, as businesses, the certainty about earnings far in the future is not as superior for Apple versus Exxon as the valuation gap would suggest.

{kind=link}

Seeking Alpha

Attractive fundamental factors certainly help recent gains in Energy, but a lot of it is also due to what I call rhetorical arbitrage. Based on my analysis, the terminal value for the Energy sector is too low because of rhetoric and perceptions that diverge from financial developments and innovative potential. What I mean by this fancy-sounding term is really not all that complicated. The rhetoric around Exxon changed quite a bit, as well as around the discussion of its externalities. However, the company's underlying business hasn't changed nearly as much as the outsized discussion would indicate. In fact, the company has innovated on the ropes and cut costs admirably. When millions of livelihoods are on one side and passionate activists are on the other, the rhetoric can get hyperbolic and confusing.

It can also trigger us to engage in emotional thinking, distracting us from getting alpha and sticking to proven processes for investing. Whatever your opinions on the climate and energy debate, we're looking through the lens of investment for our purposes. And to the chagrin of the industry's detractors, the demand continues increasing for the Energy sector's economically vital products. While it can be a political whipping boy, the state has undoubtedly noticed the sector's strategic importance. Nonetheless, the sector has made a difference in making a critical geopolitical problem less acute than it might have been. The sector's importance to the Energy transition domestically is also under-appreciated. Rhetorical arbitrage. Increasingly the sector is being given a seat at the table instead of a place on the menu in 2023.

EIA

US production capacity, for instance, may have meant the difference between tens of thousands freezing to death this winter. When you look at the two companies through a different lens, though, and you consider the current Energy crisis is not over, it raises the legitimate question as to whether the valuation gap between Energy and other sectors, exemplified by these two prolific firms, is justified. This is where terminal value comes in, as I believe it is the primary culprit. The terminal value for much of the market is way higher than Energy, which is becoming increasingly unjustified given 2023 earnings and revenue growth expectations, which I'll elaborate on below.

{kind=link}

Seeking Alpha

{kind=link}

Seeking Alpha

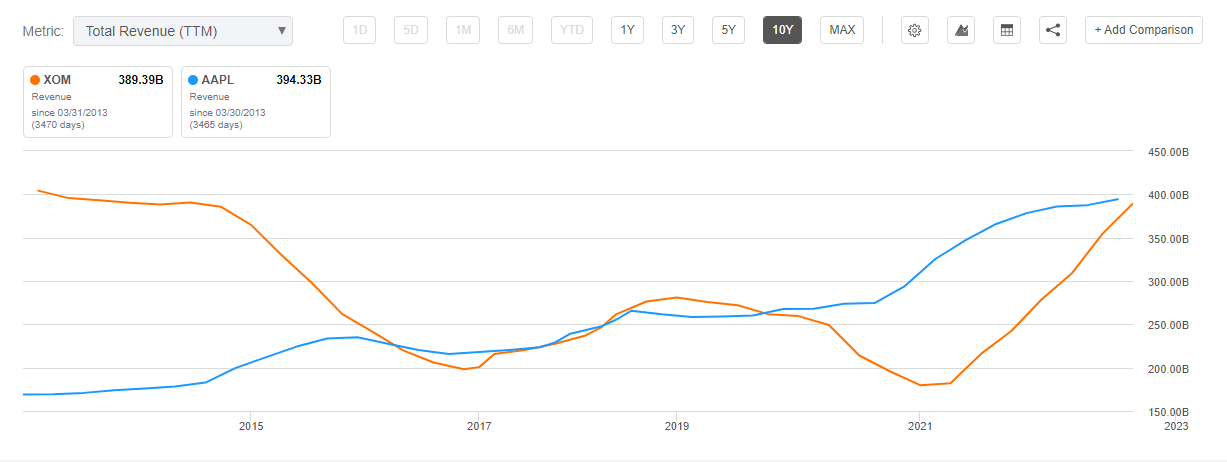

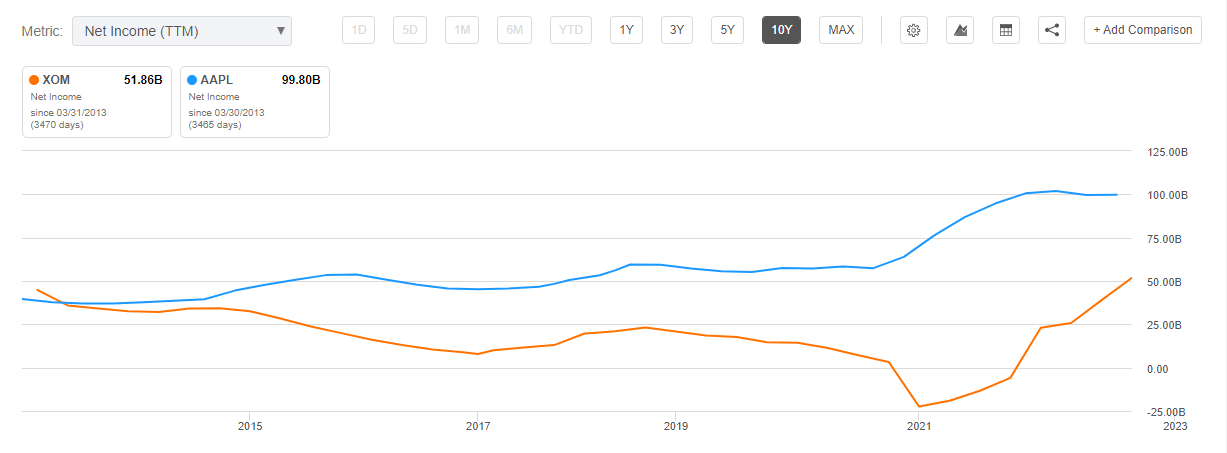

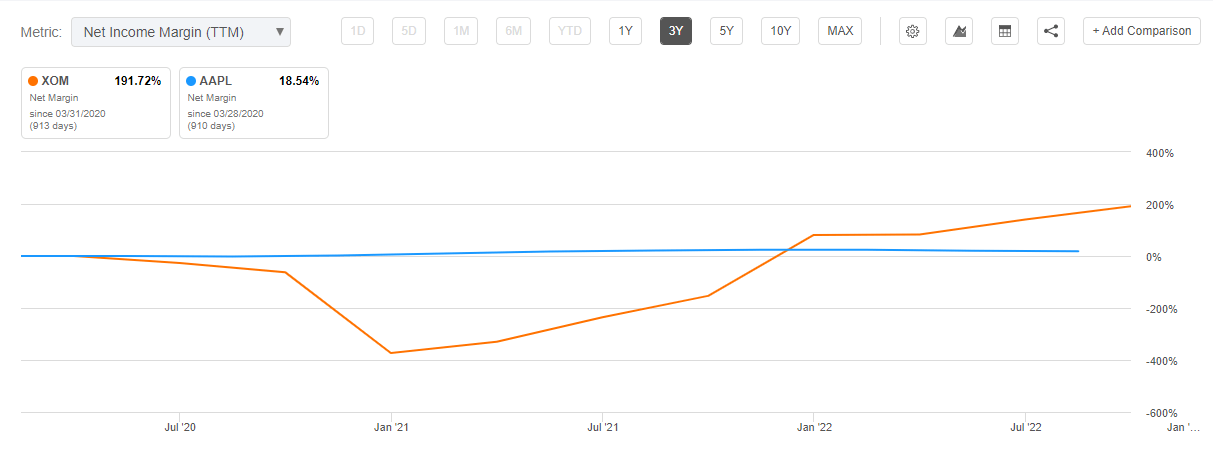

Apple is valued at nearly three times the EV/EBITDA of Exxon. Yet Exxon makes almost the same revenue and takes home half as much as Apple's net income. Yet Apple's core product is maturing, and Exxon's wares are becoming increasingly scarce and remain vital to the Energy transition itself, any way you measure it. Exxon has a powerful competitive position, as does Apple. But Apple's costs seem to be going up, and Exxon's seem to be going down. Furthermore, Apple is likely just as vulnerable to technological disruption as Exxon and has a maturing core revenue driver. Is this all really justified? Should Exxon be priced as if it's on its deathbed?

{kind=link}

Seeking Alpha

{kind=link}

Seeking Alpha

Of course, I'm not insinuating that Exxon should be valued comparably to Apple. Merely, given market risks and when looking at financials through a different lens, a historic gap in the valuation is likely to narrow in the first half of 2023. These two companies make a point of valuation that I think is crucial to the bullish thesis for Energy. When you think about Energy valuations, the justification becomes even more compelling. The Energy sector has been investing in areas other than Oil & Gas for years, and those efforts have only accelerated in many cases. They are more genuine in intent than opponents often suggest as well. But another consideration is the extremely rich valuations of unproven EV firms. There are many credible doubts about the future of EVs. Lithium mining poses its own environmental externalities as well.

Bloomberg NEF

Do you think Exxon will be more successful than Apple in spending Capex to innovate new earnings drivers to replace current core drivers? Especially since the Engine No.1 board seats were acquired by corporate force, the firm's strategy to be profitable in a decarbonizing world, along with the industries, is increasingly viable. Baker Hughes ( BKR ) has a high-margin turbine segment that will continue to be vital ch clean energy tech. Other names are helping major Gulf p roducers lower their impact and break-even rates, like Schlumberger ( SLB ).

This is another reason why the terminal value is too low. The us vs. them mentality that pervades the rhetoric is becoming increasingly divorced from reality. The Energy sector will be vital for years to come. Natural Gas consumption won't peak until 2037, according to McKinsey. Peak oil is likely a ways off as well. It will likely remain relevant far into the future when high emissions of fossil fuels are either a much smaller percentage of what's generating our energy or, ultimately, a thing of the past. Current valuations don't reflect this likelihood, and the Energy sector's terminal value, as assigned currently by the market, is likely too low in my estimation.

A Dollar Long and A Day Ahead

There's an old English idiom: a bird in the hand is worth two in the bush. This concept is really at the heart of stock market valuation. The discounted cash flow model used this idiom as its governing principle. A company is merely the sum of its current cashflows added to the future cash flows, discounted at some benchmark rate, like the 10-yr treasury. There are usually five years used in models, sometimes more, but the value far in the future is mainly comprised of what is called the terminal value. This is determined by generating a perpetual growth rate into the future. For high P/E stocks like Technology names, terminal value can comprise well over half of a stock's total intrinsic or net present value at any time. But what if an industry is perceived to have no future?

Francineway.com

While determining intrinsic value may seem old-fashioned to some, it certainly doesn't to the people making many algorithms and models driving large portions of institutional purchases. So, even if you're a crypto enthusiast who doesn't care much about intrinsic value, it still matters in the stock market because institutional money is still dominant. One of the main reasons Energy is still poised to outperform in the first half of 2023 is that its projected earnings growth remains miles ahead of the rest of the S&P 500.

It is also a good place to hide against the Fed if they keep rates higher for longer, as long as they don't unleash a nasty recession. Given the sector's expanding margins and revenues, it should hold up in a mild-variety recession. The Energy earnings are a bird in the hand compared to more richly valued sectors since such a large proportion of them are returned to shareholders through dividends and buybacks. Energy also has the highest projected revenue growth.

{kind=link}

Factset

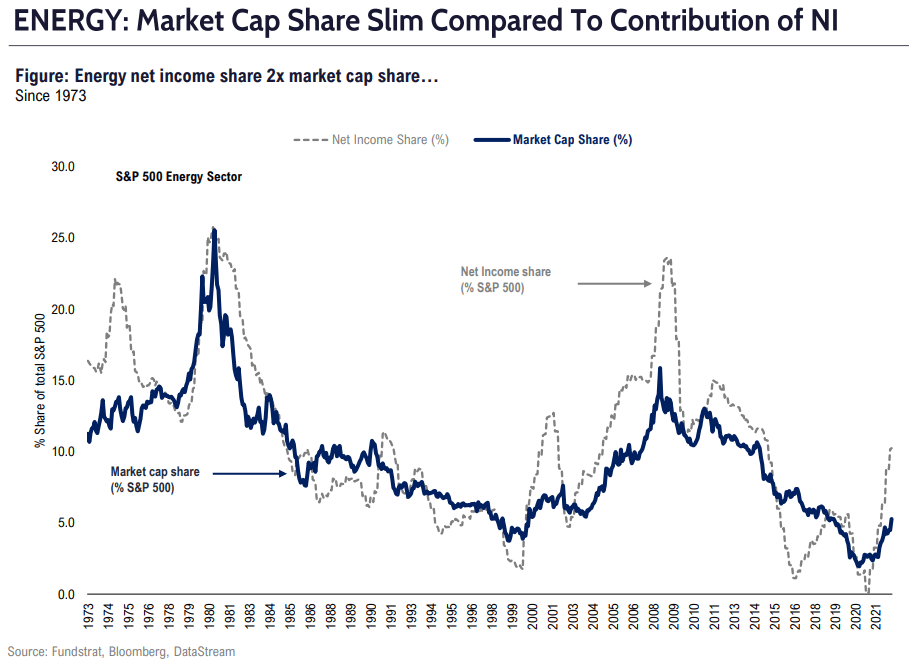

We'll leave the debates on theory and how much intrinsic value matters for another day. Just assume the following for the purposes of our discussion. Earnings matter. Intrinsic value matters. Energy is an excellent example of this. In 2020, institutional money had abandoned Energy, and since its weighting compared total benchmark was so low, many decided to weight it to zero. Many institutions had no exposure. Once it became clear the industry was more resilient than naysayers predicted and the fundamentals were good, the money rushed back in. Still, despite the fantastic year it has had, it still is trading at far less than its proportion of the total S&P 500 net income.

{kind=link}

Fundstrat, Bloomberg, DataStream

One of the pitfalls of the human prefrontal cortex is that we often oversimplify complicated events. Our brains are built to build conclusions given limited data quickly. In our pre-industrial existence, this served us fine. However, when considering complicated matters like climate change and the required de-carbonization of Energy consumption, it can often wreak havoc on our ability to draw reasonable conclusions. Of course, this pertains to both sides of the discourse on the Energy sector. Those matters are not for us, though; we are together merely devising whether or not the Energy sector is a good investment from a fundamental perspective. Investors had proclaimed the Energy sector on the verge of death, the sick man of the S&P 500, and the course of history had another outcome in mind. I think Energy will remain strong, at least in the first half of 2023. I will revisit the sector around June.

The Energy Sector's Future is Brighter Than You Think

As the theses around climate change became more accepted worldwide and as governments began taking radical action to decarbonize economies, many began to consider the Energy industry a dead man walking. In doing so, the valuations for Energy became dirt cheap, and valuations of Electric Vehicle manufacturers became sky-high. From a discounted cashflow perspective, at the recent trough, the Energy sector was being valued in a way that suggested it might be out of business in years. Remember, Energy performed well in 2021 before it smashed records in 2022. At the beginning of last year, the question was the same as now. Can Energy perform well again? I believe it can, and the industry has changed so much that many historical analogs are of dubious value.

Institutional investors had soured on Energy before coming back to the sector in 2021 and 2022. But the weaker past iterations of the Energy industry, when companies were much less efficient and disciplined, often comprised much higher proportions of the S&P 500's net income than it currently does. The sector grew to around a quarter of the total net income in 1980 and 2009. It's less than half of that now.

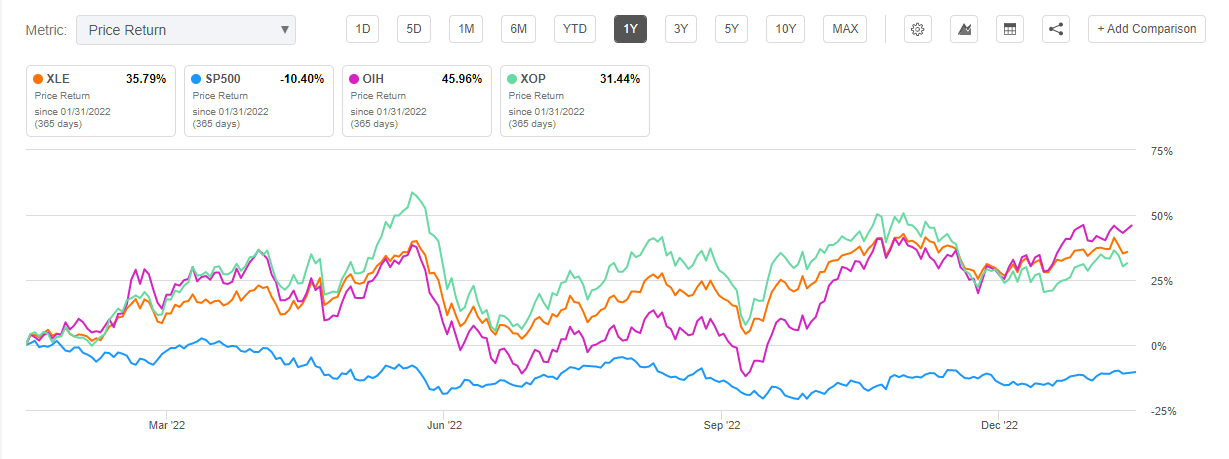

Owning XLE at the sector level is also nice. Under the hood, industries within the sector can compensate for weaknesses in other areas. As you can see below, upstream ( XOP ) performed well in the middle and second half of 2022, and Oilfield Services ( OIH ) underperformed for much of that period. As you can see, in the last few months, OIH has been leading the charge while upstream has lagged.

{kind=link}

Seeking Alpha

As the embattled sector struggled to survive and made itself more appealing to shareholders by embracing innovation that reduce emissions and enacting enticing capital return policies, the sector made itself indispensable in one of the most challenging years for investing in the 21st century. We are still likely only in the first innings of an Energy crisis driven by geopolitical events, such as the worsening war in Ukraine.

The sector's viability rises as the importance of Energy security rises. Our domestic Energy sector is a major strategic advantage as we square off against China in a great power standoff. In an industry marked by bumper and drought years, 2022 was one for the history books. Of course, Energy is an inherently cyclical sector, so many may have taken their gains and run. Understandable but also a mistake, in my opinion.

It Was a Very Good Year...

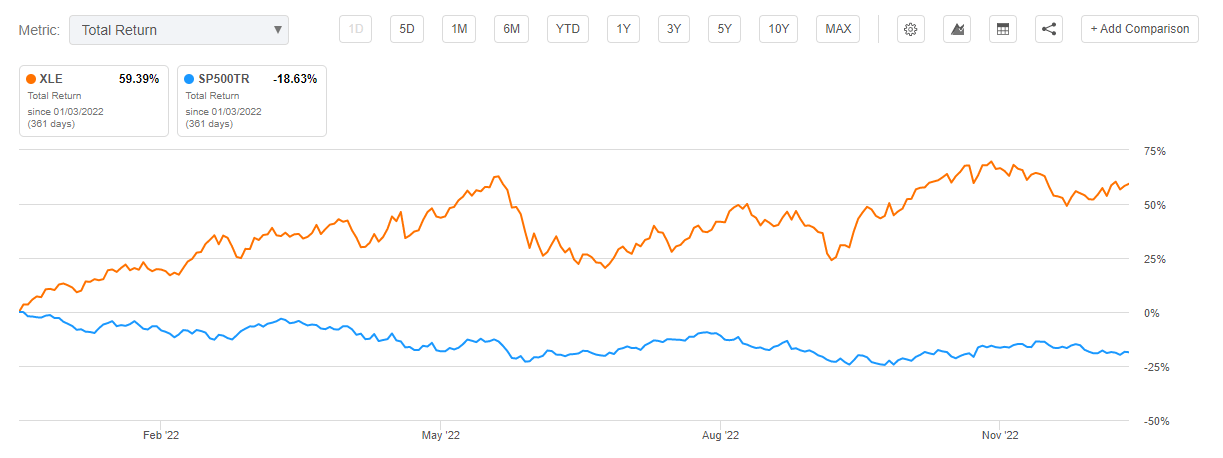

The Energy Sector had its best year ever in 2022. Stocks had their worst year since 2008; bonds had their worst year in modern history. This led to many investors dependent on the 60/40 portfolio being brought out on stretchers and has contributed to the historically bearish sentiment among institutional investors. Not only did Energy dramatically outperform the S&P 500, gaining 58% when the index dropped 20%, but 2022 was the first year in the market's history when Energy was the sole sector to post gains. I also want to clarify that I've been bullish on Energy for a long-time and wrote this piece on behalf of my former employer two years ago.

{kind=link}

XLE Vs. SP500 in 2022 (Seeking Alpha)

So, I'm not late for the party. I think it will go on for at least a few quarters, though. Also, a point I made in this 2-year-old piece still holds. In the 20th century, many Energy bull markets tended to last longer than might be intuitive, given the sector's cyclical nature. The fundamental drivers of Energy's strength at the beginning of 2023 seem similar to me to two other periods. That is the Energy bull market from 2001 to 2008 and 1974 to 1980.

In both periods, Energy's bull market of outperformance versus the index lasted more than 75 months. Given the fundamental lack of investment, the geopolitical environment, and the changing cost structure of alternatives, I believe there could be a year or more left in the bull market if a significant recession is avoided. Of course, China's re-opening will likely provide support in the first half, even if a minor recession does occur.

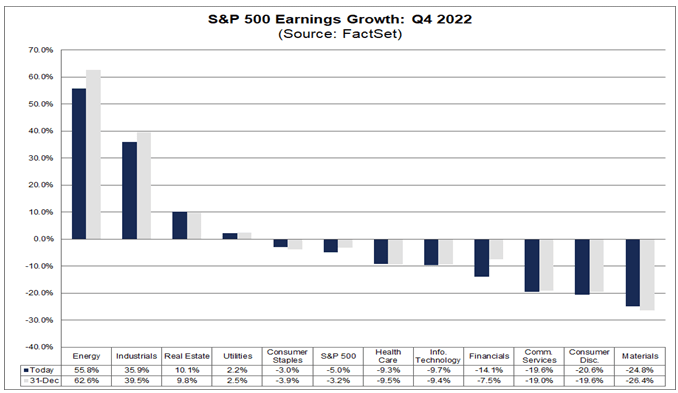

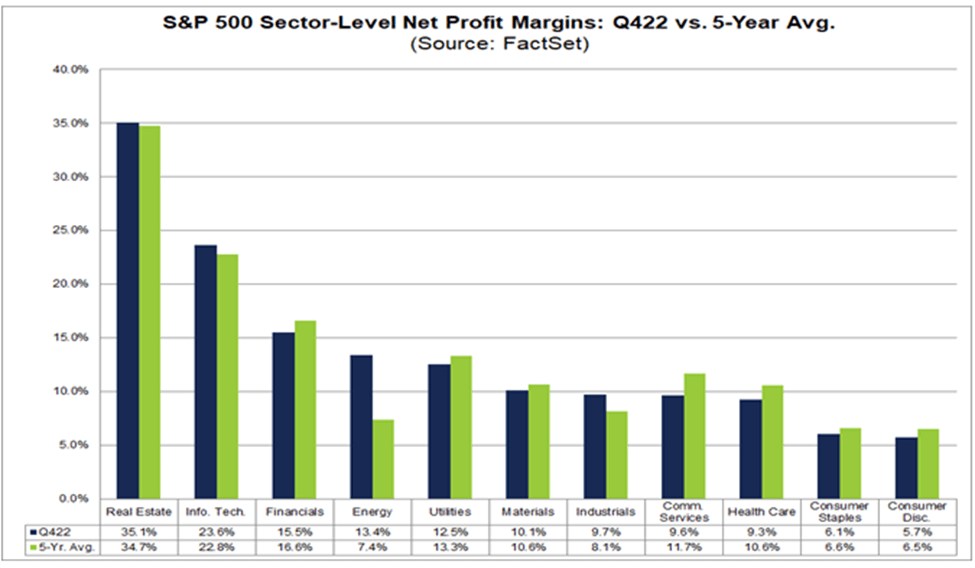

It's not just about earnings growth and the potential for a secular bull market. Margins are compressing across many vital sectors, including Tech, but consider Energy's margins compared to its 5-year average (below). This, with its relatively conservative valuation (that assumes an incredibly low terminal value), makes it seem even more enticing, particularly when margin compression will be going on in many sectors with far higher P/E ratios than Energy. The Energy sector's margins in Q422 were nearly twice their 5-year average. Not one other sector even came close to that, and a hefty majority of them were below their 5-year average.

{kind=link}

Factset

After such a strong year, some might think it might be best to take gains and find somewhere else to put funds. After all, it's an adage in investing that last year's winner is often next year's loser. While there certainly is something to this thinking in many cases, there are also many times when blindly following it will lead you astray. As tricky as it is, I argue that the Energy sector is facing unique circumstances going into 2023 and has a great deal of support on the demand side as we advance, even in the event of a global recession. The sector has attracted investors with incredibly enticing buybacks and dividends, but this has often been at the expense of the crucial investment required to keep the supply balanced with demand.

Supply and Demand Dynamics in the Energy Sector

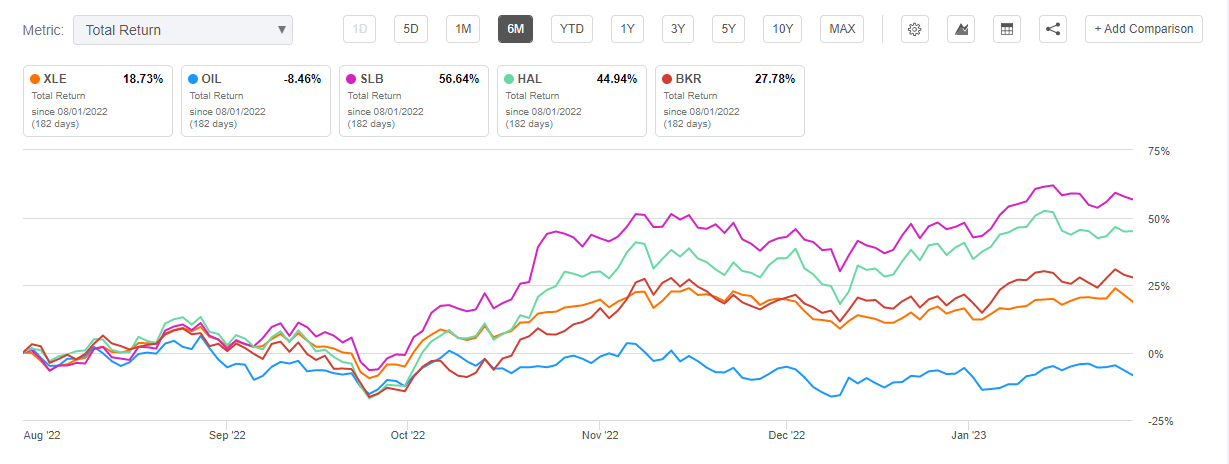

Developing oil reserves takes a very long time. Supply was lower going into 2022 because of chronic underinvestment in production capacity. Energy companies have primarily decided to return money to shareholders rather than invest in additional production capacity. However, this is starting to change in 2023, and upstream investment should be up, particularly by the Saudis and Gulf states. However, it's important to remember a lot of American companies will benefit from this foreign CAPEX even if the majors and other upstream domestic firms invest less as they play a game of chicken with policymakers. The Oilfield Services names like Schlumberger, Halliburton ( HAL ), and Baker Hughes have outperformed the rest of the sector over the last few months.

{kind=link}

Seeking Alpha

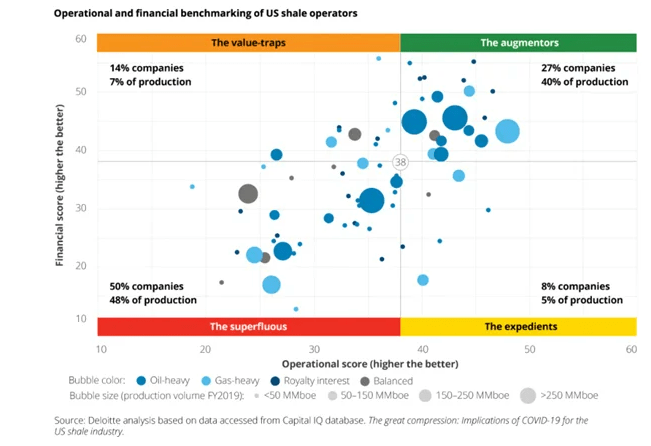

Another dynamic that has changed over the last few years is that the shale industry has become more frugal and appealing to investors. In the 2010s, the industry was known for a cowboy mentality, even amongst a sector that makes its money digging holes in the ground, which ended up destroying a lot of shareholder capital. The caricature of the "shalesman." is a poignant way to illustrate how the industry has changed. COVID and other shocks have disciplined the industry through the school of hard knocks. Many shale companies used to be terrible investments, but the industry has matured and cleaned up its act. Many of the less efficient firms failed.

{kind=link}

Deloitte

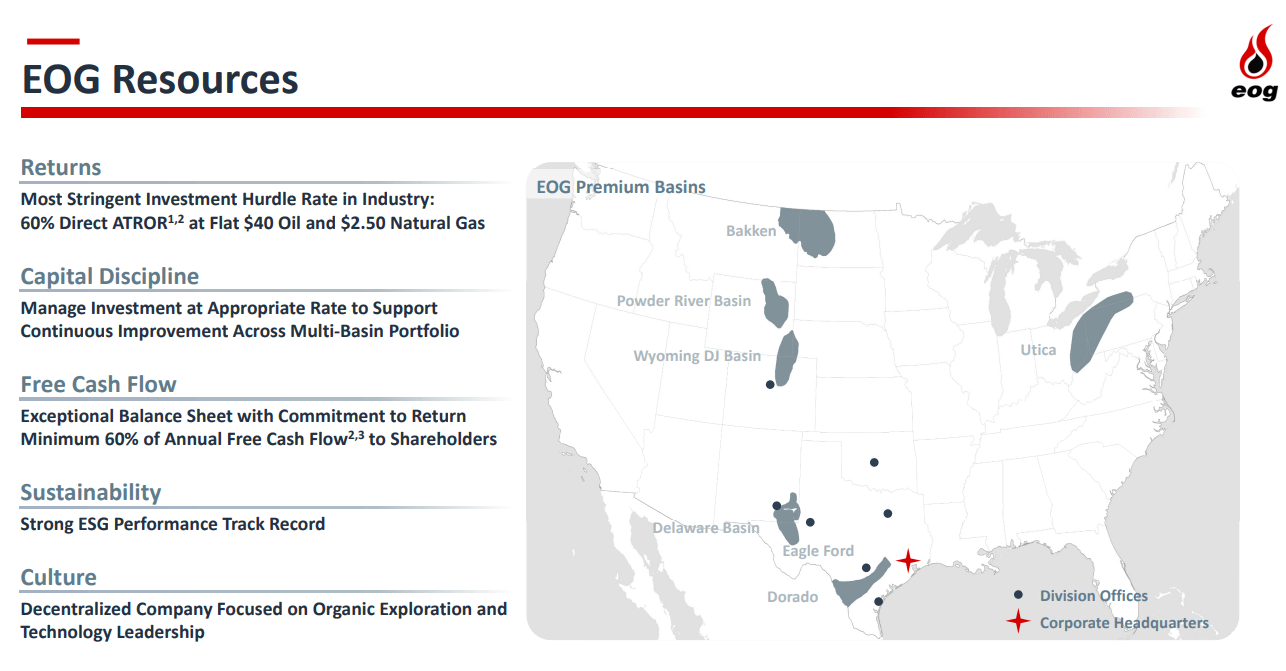

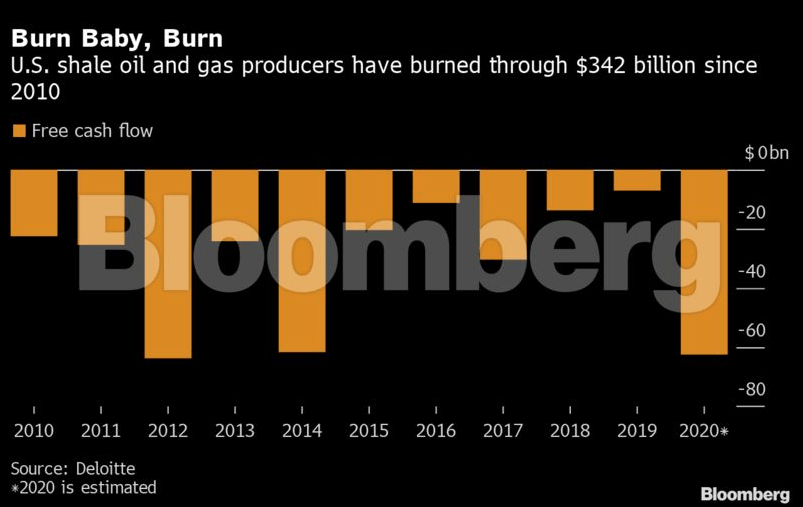

The colorful shale industry was known for excesses . They used to have laughably high breakeven prices, and the industry destroyed a lot of capital, as shown below. However, today there's a capital discipline that makes management teams look like choir boys compared to the past. They also have brought discipline to production, which supports oil prices. EOG is an excellent example of the "Death of a Shalesman" and the birth of a cash cow concept central to the increasingly superior energy sector performance. Look at their breakeven rate now (below).

{kind=link}

EOG Company Reports

Some have wondered why Energy has remained more resilient in the face of oil price declines than in the past. The answer is, in large part, due to this new discipline across the industry. A critical shock that hardened and toughened this industry was when oil went negative in April 2020. Overwhelmingly, the industry has shunned projects with high breakeven levels, and many companies would remain profitable if Energy prices got cut in half. This different character of the Energy industry made it the ultimate haven in the most challenging year for investing since Lehman failed.

{kind=link}

This gets to another strength for the Energy sector going into 2023. Of course, the sector provided an excellent inflation hedge as the economy underwent its worse bout with inflation in four decades. But it also is burned in investors' minds as a safe haven during tough times. This will likely continue in the medium term. Being overweight in a sector with such a low correlation to most other assets can be an appealing reason to have XLE in your portfolio.

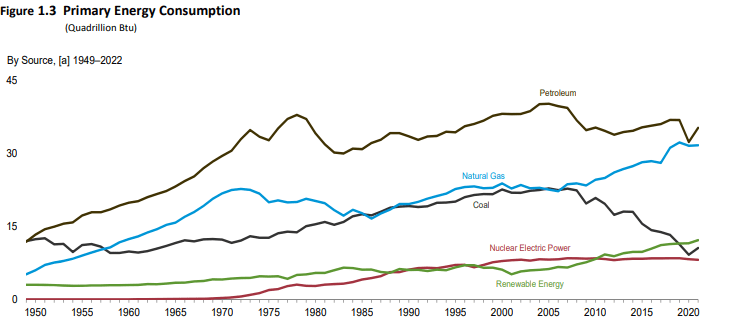

The Energy industry, regardless of its externalities, is one of the most innovative sectors in the S&P 500 and has tens of thousands of engineers pulling off prodigious and awe-inspiring tasks every year. Because of that innovation, you can get a shale well for the price of a house in coastal California. Completion costs for a shale well can be under $4 million these days. And the sector has been innovating like a cornered raccoon in the name of self-preservation. But nothing can change the fact that the economy runs on Energy, and right now, the lion's share of Energy comes from petroleum and natural gas. That's not changing anytime soon, certainly not in the 5-year period that makes up the initial value in most DCF models.

{kind=link}

EIA

Previously, the shale producers would rapidly pump when prices eclipsed their breakeven rates. Now, not only are breakevens a lot lower, but they seem to have realized slow and steady wins in the race. This means a previous "cap" on price levels has been removed. So, there are a lot of things supporting price, and the sector is simultaneously less sensitive to drops in price. Still, the highly cyclical sector has many risks. I see two primary ones in 2023.

Key Risks to Energy in 2023

Energy is highly cyclical, and it's a tricky sector to time in many cases. After it reaches the peak, a precipitous drop usually follows it. I'm not saying it will be different this time. I'm saying several supportive factors have slowed the cycle, and the terminal value of the sector is too low. The sector will always be volatile and will always be dependent on demand for its underlying commodity, which is essentially a function of GDP growth and demand across the economy. Thus, I believe the primary risk to the Energy Sector in 2023 would be if global economic activity contracts more than the consensus currently suspects. While most currently expect a recession, the forecasts have been improving recently .

Of course, another critical risk is the risk that governments enact more stringent emissions regulations, more aggressive net zero targets, or enact legislation that stands significant amounts of industry capital. I've mentioned several reasons why the state likely looks kinder upon the Energy sector than its public admonishments might suggest. However, the risk is certainly still there for government action that undermines profitability and shareholder interests, particularly as we move into the election year of 2024. However, at least in the immediate term, the thin Republican majority in the House should serve as a temporary bulwark.

Conclusion

The Energy sector is coming off its best year ever, but my analysis suggests that it will continue to outperform at least through the first half of 2023. As the consumer continues to weaken and the prospect of recession grows, the risk/reward will likely become less advantageous. That being said, there's a lot of upside in a soft-landing-type scenario. Energy remains one of my top sector picks for 2023 despite the hyperbolic invective that often accompanies discussion of the sector (from both sides). The incredibly complex Energy Transition our species is going through will likely be an all-hands-on-deck approach.

{kind=link}

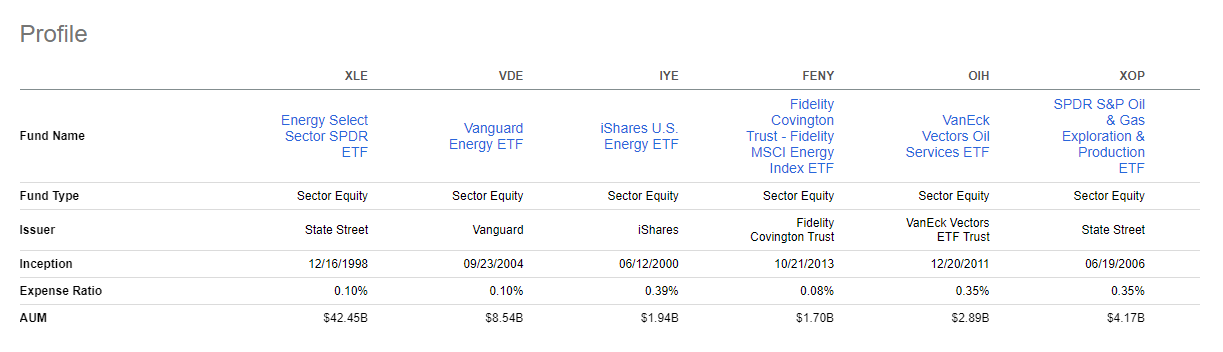

I like XLE as a way to play the Energy sector. I think the expense ratio combined with the better liquidity from having by far the highest AUM among peers is the smartest option here. It also will mean there are more liquid derivatives markets for the ETF in the event you'd like to hedge your position with puts or use calls to create a synthetic long position. However, don't use derivatives if you're not experienced and don't fully understand the greeks and potential losses.

{kind=link}

At least for the foreseeable future, the Energy Sector will be crucial to this transition. Many likely underestimate the potential for the industry to come up with vital innovations that help decarbonize the economy. For these reasons, I believe the Energy sector is undervalued and deserves a higher terminal value.

For further details see:

Why XLE Is My Top Pick For The (Still) Cheap Energy Sector