CSGKF - Will Bank Stocks Recover In 2023? Be Patient And A Little Nervous

2023-03-31 09:35:42 ET

Summary

- In this article, I briefly explain the events that caused most bank stocks to fall precipitously in March 2023.

- I share my expectations for bank stocks in 2023 and point out whether investors can expect a significant recovery in the short term.

- I explain why the SVB collapse does not represent a second "Lehman moment" and why the expectation of large-scale bank runs is an overly pessimistic base-case scenario.

- I discuss the potential impact of the wipeout of Credit Suisse's Additional Tier 1 bonds on the loss-absorbing capacity of banks and the stability of financial markets as a whole.

- I also share which bank stocks I think are currently the most compelling from a risk-reward perspective.

Introduction

The year 2023 started off pretty well, with equity markets having recovered nicely from their October 2022 lows. Last year, the market priced in a recession, and growth stocks in particular (those where much of the free cash flow is far into the future) suffered from rising interest rates. However, bank stocks also fell along with the broader market, which is counterintuitive at first glance because rising interest rates in principle are a tailwind for banks. It was the inversion of the yield curve and the expected rise in defaults that pressured bank stocks in 2022. In mid-March 2023, bank stocks were rocked by the collapse of the 16th largest U.S. bank by total assets (SVB Financial Group, now trading as OTC:SIVBQ ) after a liquidity crunch and an unsuccessful capital raise.

Nearly three weeks have passed in the interim, but bank stocks in general have not recovered meaningfully. U.S. Bancorp ( USB ), PNC Financial Services Group, Inc. ( PNC ), and Truist Financial Corporation ( TFC ) rank fifth through seventh in terms of total assets, and currently trade more or less at 2020 levels, when the world was struggling with the COVID-19 pandemic and related measures. Bank of America Corp. ( BAC , $2.4 trillion in consolidated assets, ranked second) and Citigroup Inc. ( C , $1.8 trillion in consolidated assets, ranked third) trade at similar levels. In fact, only giant JPMorgan Chase & Co. ( JPM ), with $3.2 trillion in consolidated assets at the end of 2022, is the only bank whose common stock is trading well above its 2020 level and October 2022 low.

In this article, I share my view on U.S. bank stocks for 2023, i.e., whether investors can expect a recovery after the rather nasty performance since SVB's collapse. I explain why the SVB collapse does not represent a second "Lehman moment" and why the expectation of large-scale bank runs is an overly pessimistic base case scenario. I discuss the potential impact of the wipeout of Credit Suisse's Additional Tier 1 bonds on the loss-absorbing capacity of banks and the stability of financial markets as a whole. I also share which bank stocks I think are currently the most compelling from a risk-reward perspective. Those who are not interested in a brief summary of the recent events and an explanation of how the current interest rate environment is affecting banks can skip the following two sections.

What Caused Bank Shares To Drop - A Summary Of Recent Events

As is widely known and has been extensively reported, Silicon Valley Bank was closed by the FDIC (Federal Deposit Insurance Corporation) on March 10, 2023. SIVB had a very specific problem:

On the liability side of the balance sheet, the bank offered aggressive terms (not only in the U.S.) and attracted a lot of "new money" as a result. It mainly benefited from the deposits of relatively young companies that were generously financed during the "easy money" period, especially since 2020. Many of these companies lack reliable cash flow due to their early stage of development. With the tightening of financing conditions since the beginning of 2022, these companies began to experience problems, requiring them to rely increasingly on their short-term deposits to meet their fixed-cost obligations, such as payroll.

On the asset side of the balance sheet, SIVB's management decided to focus on risk-free investments such as U.S. government bonds. These have a distinct advantage due to their favorable accounting treatment under the Basel Accords , which means they do not increase the bank's capital requirements. A bank without a significant loan book and with a high proportion of high-quality government bonds only needs to maintain a fairly modest capital base. The problem faced by SIVB was one of timing. Due to high inflows, especially in 2020 and 2021 - investors praised the bank's super-strong growth - its treasury department bought government bonds when interest rates were extremely low, i.e., for a very high price. Because of the low interest rates, the bank focused on long-term bonds, which have a comparatively higher interest rate, resulting in a positive net interest margin. SIVB took in short-term deposits and bought long-term government bonds, exposing itself to significant duration risk. Because of the narrow spread, and likely also because of deficiencies in compliance and internal control, the bank did not really hedge this risk.

In March 2022, as concerns about potential liquidity problems at Silicon Valley Bank grew louder, depositors began withdrawing their savings to avoid facing liquidity problems themselves. SIVB had a high percentage of deposits above the FDIC insurable amount. Modern communication tools (e.g., via social media) acted as an accelerant in this regard. To meet the demand, SIVB was forced to sell securities it had intended to hold to maturity at a price below book value. The bank's equity (its loss-absorbing capacity) declined rapidly. Following the collapse of Silicon Valley Bank, regulators also shut down Signature Bank , which had significant cryptocurrency exposure. The FDIC had to step in to ensure that depositors were compensated, as widespread losses could have had devastating consequences for the entire economy, potentially triggering a new financial crisis.

The market quickly "adjusted" the valuation of other banks with significant unrealized losses associated with their so-called "held-to-maturity" ((HTM)) portfolios. Investors realized that these assets might not be held to maturity, potentially exposing the banks to unsustainably large mark-to-market losses. To restore confidence, the Federal Reserve announced the Bank Term Funding Program , which allows banks to borrow short-term by posting Treasuries and other assets as collateral at par, regardless of current market value.

Around the same time, the major Swiss bank Credit Suisse AG ( CS ) experienced increasing deposit outflows , especially after its auditor PricewaterhouseCoopers flagged an inadequate risk assessment process:

However, we noted that management did not design and maintain an effective risk assessment process to identify and analyze the risk of material misstatements in its financial statements within this system [...]

Credit Suisse has been suffering from serious compliance problems for some time, hardly surprising given the bank's significant exposure to emerging market wealth management.

The situation escalated so quickly that the Swiss National Bank (SNB) offered up to CHF 50 billion under a covered loan facility to secure short-term liquidity needs. The writing was on the wall - the liquidity buffer was needed just to keep the bank afloat until its forced takeover by rival UBS Group AG ( UBS ) just three days later on Sunday, March 19 . To facilitate the process, the SNB is providing a liquidity assistance loan of up to CHF 100 billion. The shotgun wedding had a most interesting side aspect: UBS has agreed to take over CS for a valuation of CHF 3 billion (about CHF 0.75 per share), while holders of the bank's Additional Tier 1 (AT1) bonds will go away completely empty-handed. This goes against the normal waterfall cascade in a bankruptcy, but was legal according to the Swiss Financial Market Supervisory Authority (FINMA) . The market has interpreted this decision quite differently, which may have a long-term negative impact (see later discussion). For a full list of affected AT1 bonds, see this Q&A document .

Finally, German behemoth Deutsche Bank ( DB ) also faced increased media coverage after the early redemption of its 2028 4.296% bonds was announced and when it became widely known that the bank's 5-year credit default swap (CDS) spread rose to around 200 basis points - slightly higher than at the height of the COVID-19 pandemic and the European debt crisis. Deutsche Bank is closely watched by investors because of the high risk posed by its debt, weak profitability, and huge derivatives portfolio. Deutsche Bank's CDS spread has fallen slightly in recent trading days, but was still over 180 basis points on March 28.

How Are Bank Stocks Impacted By Rising Interest Rates?

To better understand the current situation, I think it is helpful to take a brief look at how conventional banks make money and the impact of rising interest rates. For the sake of brevity, I will leave aside investment banking and other approaches. There are three basic functions that financial intermediaries perform:

- Maturity Transformation: This is the mismatch between maturities of assets (e.g., loans, bonds, equity investments) and liabilities (e.g., callable deposits, time deposits, own bonds). Banks make a profit by intentionally taking interest rate risk. A bank balances the demand of borrowers and lenders. SVB conducted significant maturity transformation and did not adequately hedge its interest rate risk.

- Lot Size Transformation: Large loans are typically financed by a large number of small deposits or vice versa. Banks receive compensation for the service of bundling small deposits or other liabilities into a few large loans. It is important not to take on significant concentration risks. Properly managed banks avoid such risks through detailed supervision of their loan books and their investment portfolios.

- Risk Transformation: Banks make a profit by balancing the different risk appetites of market participants and taking on more or less credit risk. Depending on how conservatively a bank is managed, the credit risk of its loan book can be hedged if it is not securitized (e.g., mortgage-backed loans).

These functions all enable a bank to make a profit to a greater or lesser extent. Moreover, banks earn from the basic spread between assets and liabilities. This profit should not be confused with the risk premium earned by taking credit risk. Banks pay interest at below market rates for deposits and lend at rates above market rates. When this spread between assets and liabilities is approaching zero (in some countries, banks could not or would not charge negative interest rates on deposits), banks can only make a profit by using the above methods, i.e., by taking certain risks. Hedging credit or interest rate risk is possible but costly, so banks need to find a reasonable balance between stability and profitability. As an aside, being from Central Europe and having worked in the banking sector in the past, I was quite puzzled by the unhedged (or inadequately hedged) interest rate risk at SVB. On my side of the pond, banks are usually massively hedged against rising interest rates, which is one reason for their comparatively low profitability.

In any case, it's easy to understand the difficult situation banks have found themselves in over the past few years, and a rising interest rate environment is therefore positive for banks on balance. At the same time, competition among banks for depositors is increasing, as they can no longer afford to pay de facto zero interest rates on deposits. For example, Truist's average cost of total deposits increased 22 basis points to 0.31% in Q3 2022 and 35 basis points to 0.66% in Q4 2022 .

Although banks typically benefit from higher interest rates, there are several issues that can negatively impact bank stability and profitability. For example:

- As refinancing becomes more expensive, the number of defaults of so-called zombie companies or unprofitable start-ups increases (see my detailed article ). In principle, this is an important process of a healthy financial market, but the bottom line is, of course, a (hopefully temporary and manageable) negative impact on bank balance sheets and earnings.

- Due to higher borrowing costs, companies tend to reduce their investments. Demand for goods and services declines and downsizing increases, putting further pressure on the quality of banks' loan books. Lending activity declines, which puts pressure on bank earnings. At some point, a recession occurs.

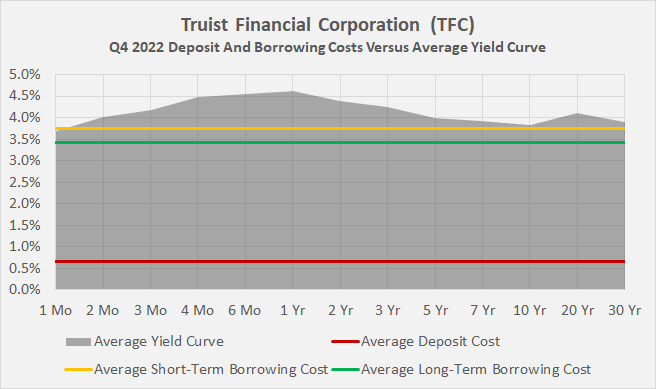

When a recession is the general expectation, a decline in long-term bond yields can be observed - simply because market participants expect central banks to lower interest rates in the future to fuel the economic rebound in a recession. In other words, investors are willing to pay a higher price for a coupon with a longer-term guarantee. At this point, the yield curve inverts, meaning that short-term bonds have a higher yield than long-term bonds, because the demand for the former is lower than for the latter. This is a negative effect for banks, which earn part of their profits by deliberately mismatching the maturities of assets and liabilities (see above). The daily Treasury par yield curve has been inverted for several months, indicating a negative profit contribution from maturity transformation. However, this point should not be overstated, as banks do not pay current Treasury yields on their deposits. For example, Truist Financial Corporation's cost of total deposits in the fourth quarter of 2022 was only 0.66%, while the average yield on 1-month Treasuries in that quarter was 3.70% (Figure 1).

Figure 1: Q4 2022 average daily treasury par yield curve rates, compared to borrowing costs of Truist Financial Corp. [TFC] (own work, based on TFC's Q4 2022 earnings press release and data from the U.S. Department of the Treasury's website: https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_yield_curve&field_tdr_date_value=2022)

{kind=link}

Bank Runs - A Plausible Base Case Scenario?

The stock market can be very emotional at times. I'm not saying that the sell-off in bank stocks was completely unfounded, but I think it was overdone. Granted, the magnitude of unrealized losses on the balance sheets of some banks is a risk, but that will only materialize in the event of significant bank runs. It is important to understand that large-scale bank runs are always fatal to a fractional reserve system. This is because although the FDIC currently has insured the deposits of 4,703 institutions (as of March 17, 2023), it can only cover slightly more than 1% of insured deposits . Our financial system is extremely dependent on the trust we place in it.

A recent research paper states, " if only half of uninsured depositors decide to withdraw, almost 190 banks are at a potential risk of impairment to insured depositors, with potentially $300 billion of insured deposits at risk " (emphasis added). The authors go on to state that the " U.S. banking system's market value of assets is $2 trillion lower than suggested by [the] book value of assets ". There are clear accounting rules, and under normal circumstances banks will not liquidate their HTM portfolios - so they are carried at cost, not market value. The Silicon Valley Bank case was a very special one, and I would be cautious about extrapolating it to conventional banks. Of course, other banks could stumble, especially those with significant concentration risks, but a conclusion based on the fact that half of the uninsured depositors withdrew their funds is, in my view, unfounded. Also, I consider the statement of total bank assets being worth $2 trillion less than they are carried on the balance sheet as overly sensational. The authors simply point to the extreme tail risk of our fractional reserve system, which is nothing new. In the event of a major bank run, who would be the buyer of the bonds and loans that the banks must quickly liquidate? Where will the withdrawn deposits go? If in cash, is there even enough cash? I think it is reasonable to expect central banks to take whatever steps are necessary to maintain the integrity of the financial system - recent actions by the Federal Reserve and Swiss regulators make this clear. At the same time, the need for such measures confirms how vulnerable our financial system is.

Implications Of A Further Tightening Of Regulatory Standards

Of course, the SVB case and potentially upcoming bank failures could lead to a tightening of regulation. A further increase in capital requirements would certainly have a negative impact on bank profitability, and such measures tend to penalize small banks that do not have significant economies of scale. If regulators require banks to account for all their assets at market value, this would have a significant impact on earnings and the ability to pay dividends, and the IRS (Internal Revenue Service) would probably not be happy about such market value losses either, assuming they are tax relevant. I doubt that such a rule would be enforced - after all, the intent to hold these assets to maturity is not changed, and current events should be considered an "unintended consequence" of the zero interest rate environment. Such regulation would be difficult to implement and would have serious consequences for the balance sheets not only of banks but also, and above all, of pension funds and private pension insurance companies, which are heavily invested in high-quality government bonds. The message that would be sent to those currently paying into the pension plans would create unnecessary panic and lead to likely unimaginable consequences.

As long as a bank does not take on excessive concentration risk and intentionally assumed or unavoidable risks are adequately managed, all should be well. In principle, a bank's loan book that has experienced significant growth in a low interest rate environment can be challenged in a similar manner. If deposit withdrawals reach critical levels and a bank is forced to sell part of its loan portfolio, I highly doubt that an acquirer would be willing to take over the loans for 100 cents on the dollar. Worse, in theory - a bank with few HTM securities and a large loan portfolio would be in a disadvantageous position from the perspective of the newly announced BTFP. In this context, the portfolio of First Republic Bank ( FRC ) seems worth mentioning. This suggests that the BTFP, while useful in certain cases, is largely a psychological tool to restore confidence in the financial system.

However, as everyone focuses on the potentially devastating impact of unrealized losses, it should not be forgotten that the rising interest rate environment has also led to unrealized gains due to the wider interest rate spread between assets and liabilities. Assuming that interest rates remain high, banks will gradually reinvest their maturing HTM assets and repaid loans to generate better returns and lend at higher rates.

Why Silicon Valley Bank Is Not Lehman 2.0

The situation of becoming a forced seller that brought down SVB - and interpreting it as the first domino that leads to a new financial crisis - is often referred to as the "Lehman moment". However, I think it is important to understand how different the two situations are. In the early 2000s, banks tried to lower their capital requirements by investing in high-quality assets other than government bonds and relied too much on the rating agencies. Bundling loans of questionable quality resulted in what appeared to be high quality assets that did not negatively impact the capital requirements (risk-weighted assets) set forth in the first Basel Accord . As the U.S. housing market weakened, it became clear that these seemingly risk-free assets did pose significant credit risk, as the borrowers were typically quite weak, and the collateral was worth much less than expected. Banks faced significant income-related losses due to actual defaults.

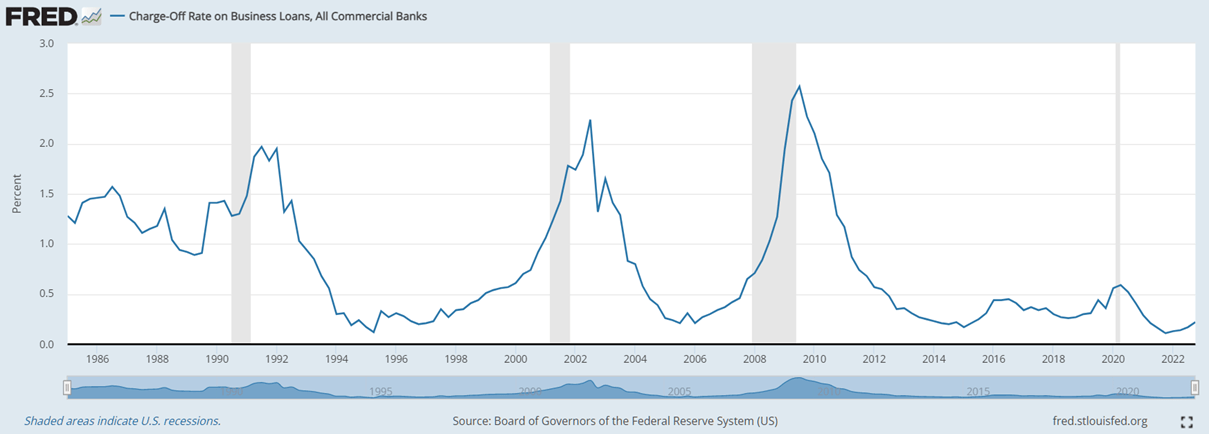

Today, banks face unrealized losses on indeed risk-free assets that need only be realized in the event of a full-scale bank run. Leaving underwater loans aside, the Federal Reserve is putting a theoretical lid on this problem by now allowing banks to draw short-term loans backed by HTM assets valued at par. This is certainly an important message that boosts confidence in the financial system, but it should not be forgotten that the borrowing institution must pay interest at current rates, which has a negative impact on profitability. In my view, this is an equally important signal, as it shows that the Fed is not handing out "free money" and that banks will have to pay for their shortcomings in risk management (i.e., overexposure to duration risk). This suggests that very small banks that rely on too much concentration risk on both sides of the balance sheet, suffer from razor-thin NII margins, and have no economies of scale could still falter. Those banks that do significant commercial lending, especially to unprofitable companies (start-ups and zombies), suffer a double whammy as the rising interest rate environment also leads to an increase in defaults. However, the charge-off rate on business loans is still very low (Figure 2), but it should not be forgotten that the pandemic-related credit moratoria had a delaying effect in this context.

Figure 2: Charge-off rate on business loans; CORBLACBS (Board of Governors of the Federal Reserve System (US), retrieved from FRED, Federal Reserve Bank of St. Louis)

{kind=link}

As investors are likely to interpret the failure of more banks as confirming signs of a new financial crisis, I expect volatility to remain elevated. Since the stock market tends to throw the baby out with the bathwater at times, I also expect the shares of larger banks to suffer, as shown by the share price performance of U.S. Bancorp and Truist Financial Corporation, for example. Of course, both have comparatively large unrealized losses on their balance sheets, but investors seem to be ignoring the fact that deposits at the 25 largest banks - which arguably include USB and TFC - have increased by $120 billion in one week, while smaller banks have lost $108 billion. Also, the news that USB, PNC and TFC have each agreed to deposit $1 billion with First Republic Bank to stabilize its strained liquidity position is a strong argument for the stability of these "smaller" banks.

Does A Rising Tide Indeed Lift All The Boats?

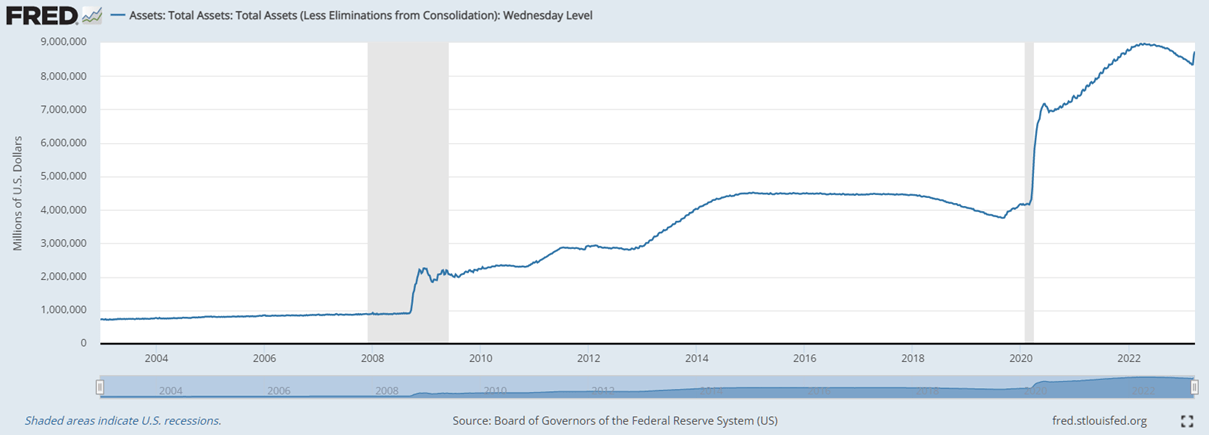

Initially surprising, but ultimately understandable, was the price action of most major tech stocks, Bitcoin ( BTC-USD ) and other crypto currencies - assets that are normally bid up in a "risk-on" environment, which we definitely do not have at the moment. Recent Federal Reserve actions have led to an increase in total assets (the upward move on the right in Figure 3), i.e., an increase in liquidity, which has a positive impact on the valuation of risk-on assets. In addition, previous fears from continued aggressive rate hikes have largely dissipated (the Fed hiked by 25 basis points on March 22 ), and lower long-term interest rate expectations result in lower discount rates on future cash flows, which is favorable for growth stocks.

Figure 3: Total assets from all Federal Reserve banks (less eliminations from consolidation); WALCL (Board of Governors of the Federal Reserve System (US), retrieved from FRED, Federal Reserve Bank of St. Louis)

{kind=link}

From an economic perspective, things don't look too bad. Economic indicators are decelerating, but do not point to severe malaise. The labor market remains strong, and lending standards are robust. Also, the spread between high-yield corporate bonds and 10-year Treasuries - a fairly reliable indicator of recession - is still very narrow. For copyright reasons, I can't share the chart here, but prepared it on the Federal Reserve Bank of St. Louis' website .

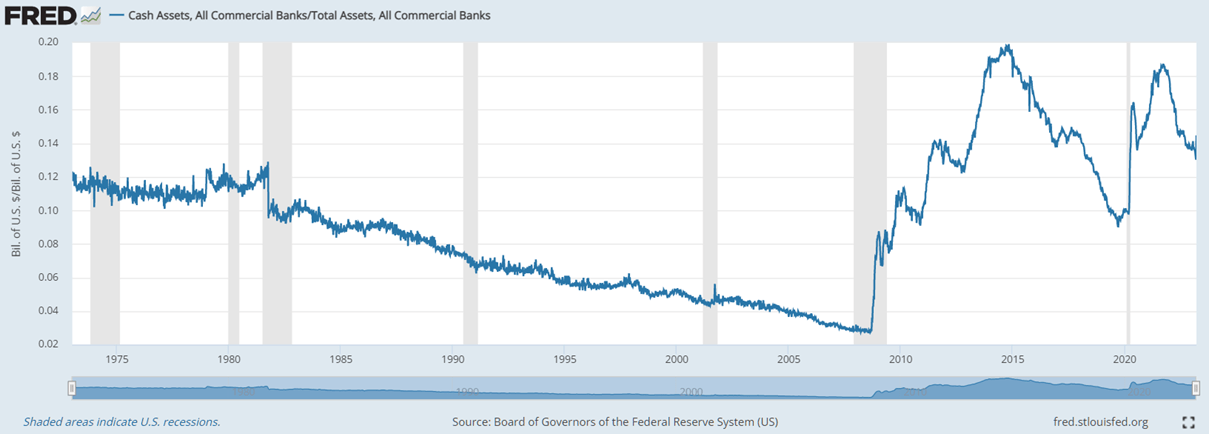

Banks are much better capitalized than they were before 2008 and have a much higher loss-absorbing capacity. However, I would be wary of over-interpreting the much higher percentage of cash assets compared to the period 15 years ago (Figure 4). The rise of e-commerce and much faster transaction speeds has significantly increased the need for cash. The risk of devastating bank runs has also increased because, on the one hand, communication (e.g., via social media) has become much faster and, on the other, transactions are largely conducted digitally nowadays. It is no longer appropriate to think of a bank run, with people lining up outside a bank branch when significant amounts can be transferred at the tap of a finger.

Figure 4: Cash assets divided by total assets, all commercial banks; CASACBW027SBOG / TLAACBW027SBOG; note that 1 on the y-scale means 100% (Board of Governors of the Federal Reserve System (US), retrieved from FRED, Federal Reserve Bank of St. Louis)

{kind=link}

Since all stocks - those of banks included - are very long duration assets (see my detailed article ), a decline in the discount rate should generally benefit valuations. However, given the ongoing uncertainties and potentially lower earnings power going forward, I do not believe bank stocks will benefit from this effect on a net basis. Instead, I expect returns on bank stocks to materialize long-term from mean-reversion effects given the current fairly low valuations.

A Potential Negative Secondary Effect On Financial System Stability

Overall, I think that the measures taken by the central banks have strengthened confidence in the financial systems and the regulators have made it clear that they will do everything they can to ensure the integrity of our financial system. In particular, the Credit Suisse AT1 bonds write-down case mentioned above underscores this point very well. AT1 bonds were originally invented as a kind of lifeline that banks could lean on in the event of a dangerous decline in Common Equity Tier 1 (CET1) capital - AT1 bonds can either be written down or converted into common equity.

While the write-down ordered by Swiss regulators definitely put the bonds to their intended use, the decision could also have a negative impact on the AT1 bond market. AT1 bondholders were wiped out before shareholders, who will receive a (small) share in UBS - i.e., contrary to the usual cascade in bankruptcy. As a result of the ruling, Eurozone AT1 bonds also fell precipitously. Even though Swiss law is not directly comparable to EU laws, i.e., the risks associated with Eurozone AT1 bonds were misinterpreted, investor confidence in this asset class is likely to have been permanently impaired. This, in turn, points to a weaker loss-absorbing capacity of banks in the future, as it should be more difficult for them to bring AT1 bonds to the market going forward. However, I would not overinterpret this aspect, as I suspect AT1 bonds are largely held by institutional investors, who should be well acquainted with such instruments and are capable of managing the higher risk and also higher coupon rate stemming from the deeply-subordinated status.

Which Are The Best Bank Stocks To Own Now

There's no question about it - it takes considerable risk appetite to invest in bank stocks today. Uncertainty remains high, and news about the collapse of other small banks could quickly lead to renewed selling pressure that could push bank stocks below the 2020 lows. However, I prefer to invest during times of uncertainty rather than during times of (possibly unwarranted) euphoria. I never quite understood the run-up in bank stocks in 2021. Of course, this was due to the significant liquidity in the system, but I felt that investors were completely ignoring the negative impact of low interest rates and the potential long-term consequences of capital misallocation. As a result, I am much more optimistic in March 2023, given the fairly conservative valuations. The SVB case was rather special, and Credit Suisse's problems are not new. Of course, the shotgun wedding of UBS and CS was irritating (same as the wipeout of AT1 bondholders) and is an important sign of the fragility of our financial system. At the same time, recent events have shown that central banks will do whatever is necessary to preserve the integrity of our financial system. And most importantly, the fact that our fractional reserve system relies 100% on depositor confidence has not changed. The forced realization of unrealized losses across the board is a black swan that I do not believe is likely to materialize.

The sell-off in certain stocks was certainly not unfounded, but I think it was overdone. That said, I believe that the earnings position of banks (other than the largest) should be considered. Smaller banks with significant concentration risk could indeed go under, so I am not trying to be a hero and invest in speculative entities.

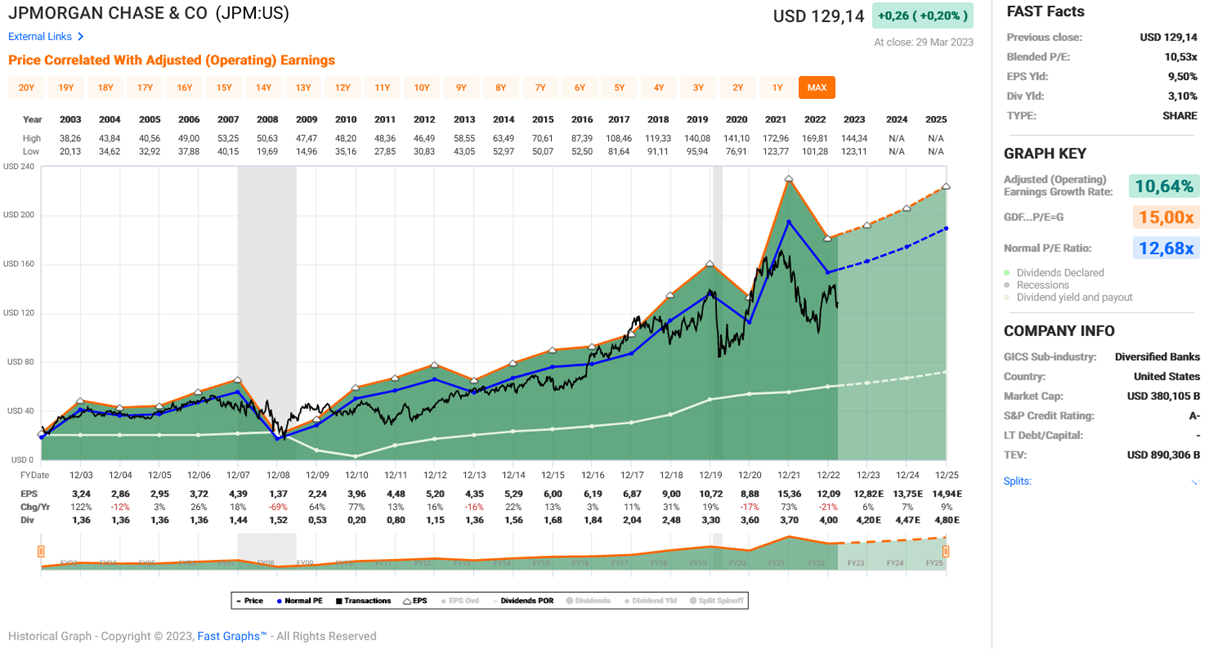

From this point of view, JPMorgan Chase & Co. seems to be the right choice as the only bank in the world with a G-SIB rating of 4 - JPM is simply too big to fail. The bank will likely continue to benefit from industry consolidation and operates at significant economies of scale. Also, its status as a "safe haven" in the current crisis will prove to be an earnings-related tailwind, as the bank takes cheap deposits from former customers of smaller banks, which it can lend out to those same banks at a higher interest rate. While JPM is certainly not overly expensive (Figure 5), I think its return prospects are relatively low given its premium status in the industry. The other big banks, BAC, C, and Wells Fargo & Co ( WFC ), offer potentially better returns but carry their own risks. WFC's operational problems are well covered, C focuses on large customers and therefore has a higher risk of outflows from uninsured deposits, while BAC has comparatively high unrealized losses. Nonetheless, I believe all of the large banks will benefit on a net basis from consolidation and deposit churn (see recent news regarding BAC and the other three ).

Figure 5: FAST Graphs chart of JPMorgan Chase & Co. [JPM], based on adjusted operating earnings per share (obtained with permission from www.fastgraphs.com)

{kind=link}

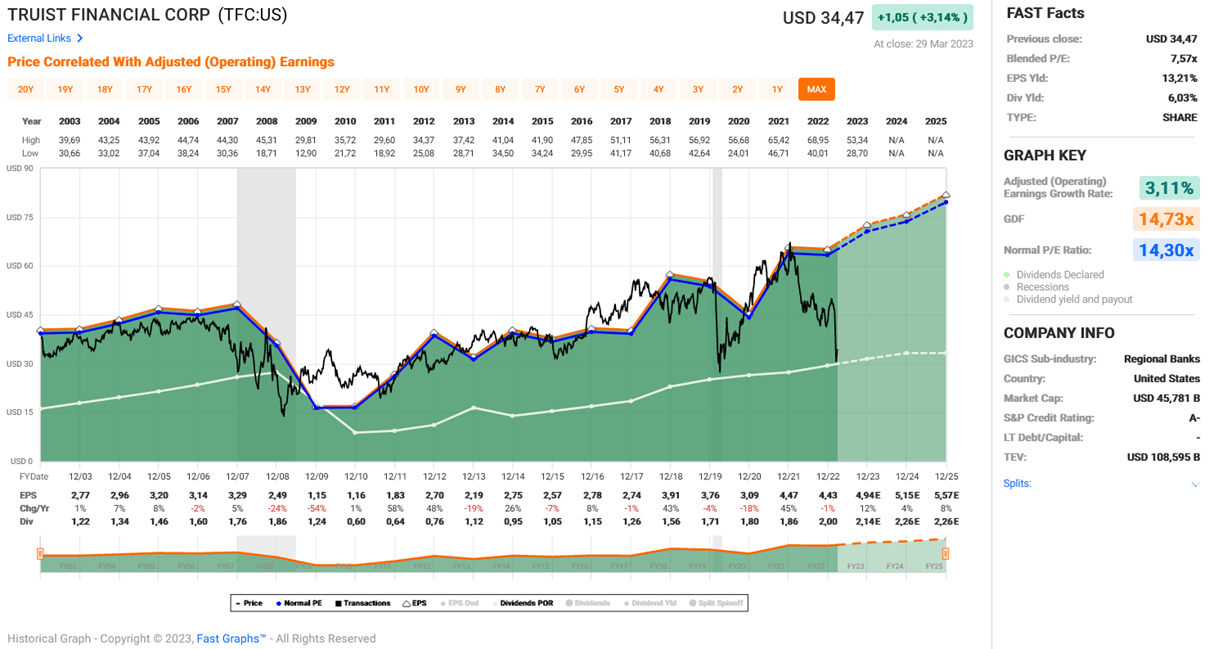

As I pointed out in another article on banks in general and Truist Financial Corporation in particular, I believe that such "second tier" banks represent the best tradeoff from a risk-reward perspective. Granted, banks like TFC and USB reported relatively large unrealized losses in their 2022 10-Ks, but I think investors should focus more on potential earnings-related headwinds, such as stricter regulations, than on acute solvency-related risks.

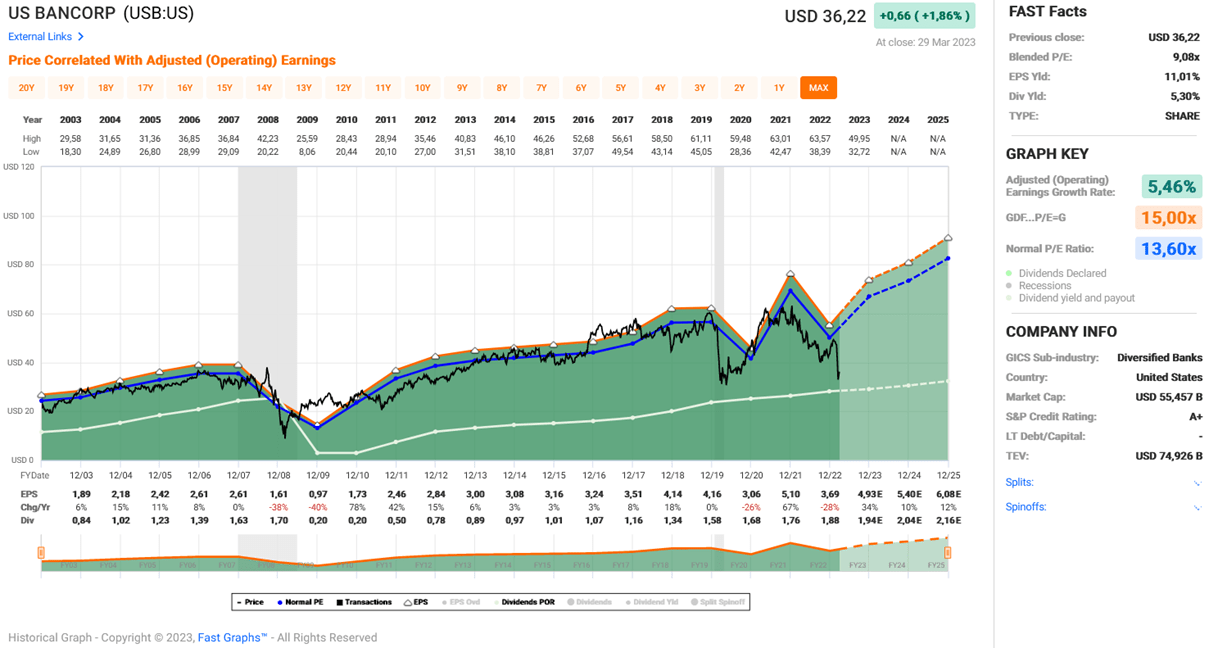

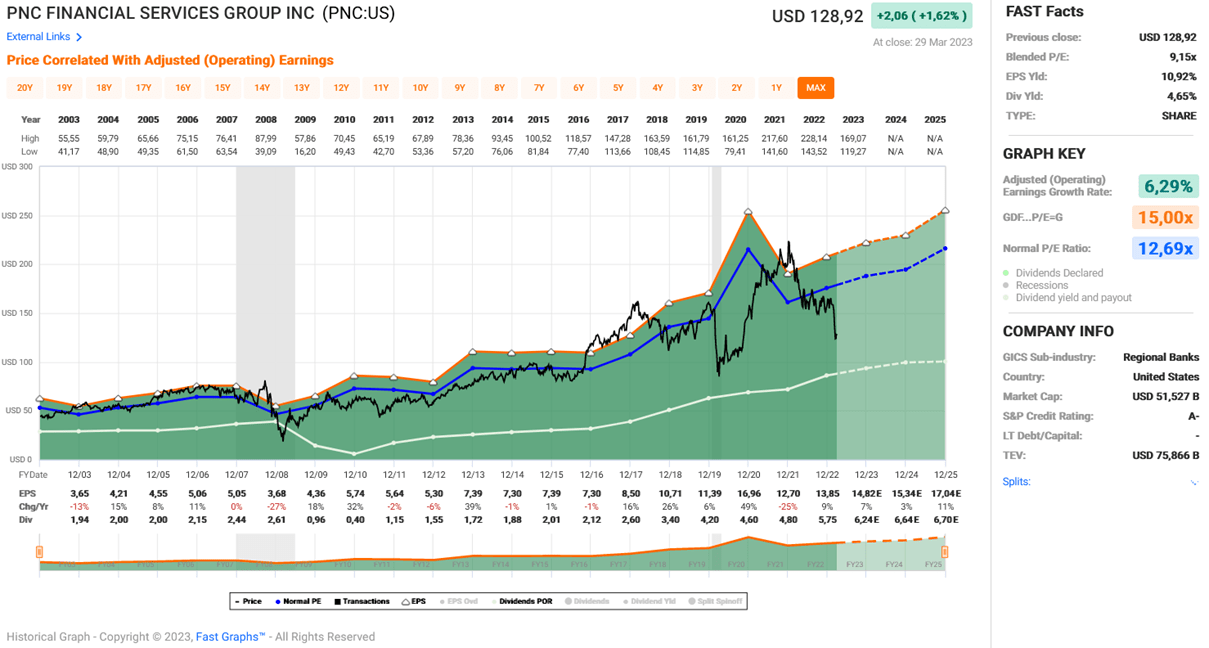

Although they are much smaller than the "Big 4", they should all benefit from consolidation and migration of deposits. USB, PNC, and TFC are still very large banks, although USB probably has a comparatively better reputation among investors and customers because of its good performance during the Great Financial Crisis. Figure 6, Figure 7, and Figure 8 show the FAST Graphs charts of USB, PNC, and TFC, which rank fifth through seventh in terms of consolidated total assets as of December 31, 2022. From a valuation perspective, I particularly like TFC, and I attribute the discount primarily to its comparatively large unrealized losses and the still-visible drag from the BB&T-SunTrust merger.

In general, I think it's best to look for relatively large banks (i.e., hundreds of billions in total assets) with good efficiency ratios and diverse businesses (not too much concentration risk). I would avoid super-fast growth banks, as this is usually an indication of an unsustainable business model, as the case of SVB has shown. Finally, I also think it is important to focus on banks with a comparatively low share of uninsured deposits. For example, uninsured deposits at Truist and U.S. Bancorp account for less than 60% of total deposits, while almost 90% of SVB Financial Group's deposits fell into this category.

Figure 6: FAST Graphs chart of U.S. Bancorp [USB], based on adjusted operating earnings per share (obtained with permission from www.fastgraphs.com) Figure 7: FAST Graphs chart of PNC Financial Services Group, Inc. [PNC], based on adjusted operating earnings per share (obtained with permission from www.fastgraphs.com) Figure 8: FAST Graphs chart of Truist Financial Corporation [TFC], based on adjusted operating earnings per share (obtained with permission from www.fastgraphs.com)

{kind=link}

{kind=link}

{kind=link}

Concluding Remarks

The article provided a brief overview of the recent events underlying the March 2023 banking crisis and addressed the impact of rising interest rates on bank profitability.

The collapse of SVB was shocking at first glance, but turned out to be a rather special case. Concentration risk and inadequate risk management are a toxic cocktail. The shotgun wedding of UBS and CS was irritating and proved to be an important sign of the fragility of our financial system. At the same time, recent events have shown that central banks will do whatever is necessary to preserve the integrity of our financial system. And most importantly, the fact that our fractional reserve system relies 100% on depositor confidence has not changed. The recently announced Bank Term Funding Program will prove helpful to troubled banks with significant unrealized losses in their HTM portfolios. However, to the best of my knowledge, banks with significant and illiquid long-duration loans that are underwater are not covered by the BTFP. In my view, this risk should be considered along with the now widely known risk stemming from unrealized HTM portfolio losses and suggests that the Fed's BTFP is largely a psychological tool to bolster confidence in the financial system.

Stricter bank regulation could be the result, but I do not expect regulators to require financial institutions to immediately recognize fair value losses regardless of the intended use of the assets in question. Such a rule would be difficult to implement and would have serious consequences for the balance sheets not only of banks but also, and especially, of pension funds and private pension insurances that have significant investments in high-quality government bonds. The message that would be sent to those currently paying into the pension plans would create unnecessary panic and lead to likely unimaginable consequences.

The price action of major technology stocks and also cryptocurrencies (typical "risk-on" assets) since mid-March suggests that liquidity has flowed into the market, which is a positive for equities in general, but I suspect that the renewed uncertainty and the "reminder" of how fragile our financial system is outweigh this weak benefit. At the same time, we can expect the Fed's quantitative tightening to slow or stop altogether sooner rather than later, which is also bullish for stocks. The Fed will be careful not to tighten too much and risk an excessive recession or a systemic event in the financial sector. At the same time, I doubt the Fed will render the recently announced BTFP facility (which I believe is a soft form of quantitative easing) useless by maintaining its aggressive stance on tightening.

From an economic perspective, things do not look as bleak as is often communicated, and banks are also much better capitalized than they were 15 years ago. At the same time, I believe that the improved capitalization is necessary because bank runs are more likely (and potentially more devastating) today than they were a few decades ago. In addition, it is important to keep in mind that pandemic-related loan moratoria have a delaying effect on defaults, so we can expect an increase that will likely be exacerbated by continued high interest rates (failures of zombie companies and unprofitable start-ups) and a recession. A self-reinforcing cycle could exacerbate the problems and would certainly increase short-term volatility.

Overall, I don't think the rise in liquidity and lower long-term interest rate expectations will help bank stock valuations - at least not in the near term. Since all stocks are very long duration assets, a decline in the discount rate should generally benefit valuations. However, given the continued uncertainty and potential of additional failures, I do not believe bank stocks will benefit from this effect on a net basis. Instead, I expect bank stock returns to materialize long-term from mean-reversion effects given the current fairly low valuations. The profitability of smaller banks could suffer, and deposit churn and an impending recession are likely to contribute to industry consolidation.

While an investment in JPM is probably the least risky way to gain exposure to banks, I believe the risk-adjusted return potential is better at the largest among the smaller banks, such as U.S. Bancorp, PNC Financial and Truist. However, since I personally expect volatility to remain high for the reasons stated in the article, I am not an aggressive buyer of these stocks. While I have opened a position in USB and TFC as explained in my previous article, I do not expect a quick recovery and therefore have no difficulty keeping my "fear of missing out" under control.

As always, please consider this article only as a first step in your own due diligence. Thank you for taking the time to read my article. Whether you agree or disagree with my conclusions, I always welcome your opinions and feedback in the comments below. And if there is anything I should improve or expand on in future articles, drop me a line as well.

For further details see:

Will Bank Stocks Recover In 2023? Be Patient And A Little Nervous