CA - Will Koch Buy Into Century Lithium?

Summary

- Koch and Century Lithium collaborate on Direct Lithium Extraction.

- This is the same Koch that invested $100 million into Standard Lithium.

- This could be the start of an equity investment into Century given time, but may require an increased share price to make an equity investment work.

When Century Lithium ( OTCQX:CYDVF ) and Koch Technology Solutions announced they were collaborating on DLE (Direct Lithium Extraction) technology, I had many investors message me asking "Is this good"?

In this article, we will explore the deal and then lay out our theory of what this relationship with a company generating revenues over $110 billion could mean for investors long term.

Who Is Koch?

With revenues estimated at over $110 billion and employees in 70 countries, Koch is no small fry. Products range from chemicals, paper, cattle ranches, and even glass. Koch also has an interest in lithium having acquired DLE technology and made investments into lithium mining companies; that brings us to Century Lithium. Why would Koch be interested in this Nevada lithium play?

Koch and Century Lithium: The Courtship Begins

What does the deal actually say? Does it matter? Per the PR:

"The companies will work together to evaluate the added features of the Li-Pro™ process at Century Lithium’s Pilot Plant. With the information obtained, KTS will provide engineering for a full-scale deployment of the Li-Pro™ process for Century Lithium’s Clayton Valley Lithium Project."

Translation: Koch is going to further test and optimize the DLE process for Century Lithium using its technology. Additionally, Koch will conduct an engineering study for the DLE portion of Century. This matters because it gives Koch access to the internal working of Century. Additionally, this could be viewed as a trust-building exercise. Koch learns more about clay-based lithium; Century obtains optimizations and has a powerhouse to assist on the engineering side. The key point is both sides get just a little deeper in bed with each other. Think of it like serious dating before any potential equity investment. Key word: Potential. What does potential look like though? Let's consider Koch's history with other lithium companies.

Koch Invests in Standard Lithium

When thinking about the outcome potentials for this relationship, we can consider what Koch did with Standard Lithium. Back in November of 2021, Koch announced they were investing $100 million into Standard Lithium. This buy-in represented 8.26% of SLI shares at closing. Now if one tried to apply that $100 million to Century, it simply would not work given Century's market cap is $153 million USD (at $1.05 a share): Koch's percentage of ownership would end up too high. Hence, maybe when the share price is higher, we will see some degree of an equity buy-in. As of right now, I doubt Century would be willing; the point is Koch dropped $100 million into Standard.

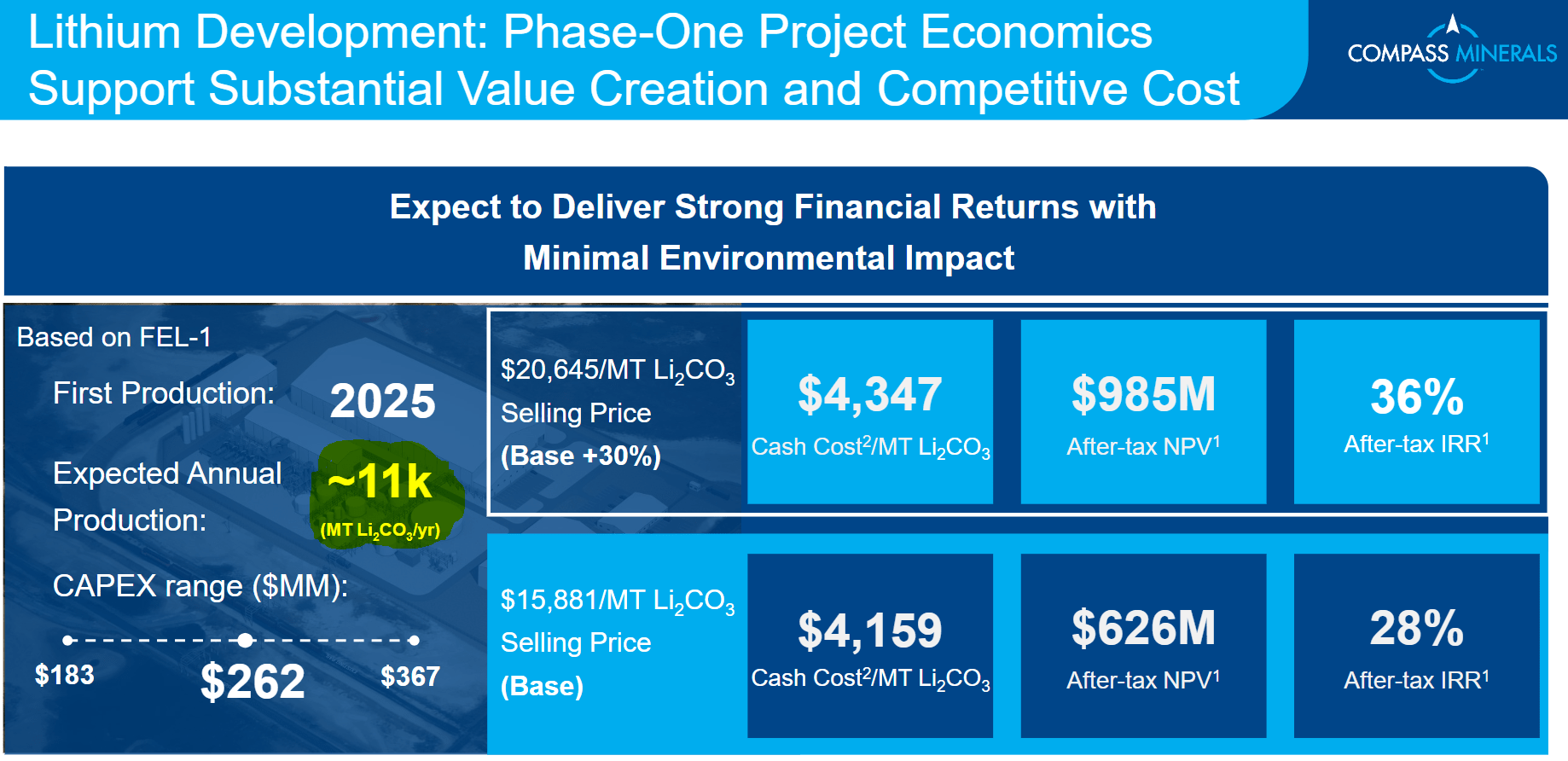

Koch Invests in Compass Minerals

We might also peer into Koch investing $252 million into Compass Minerals ( CMP ) to advance a Utah lithium project. It is interesting to note that the project is estimated to produce 11,000 tonnes of LCE by 2025 during Phase 1, with Phase 2 bringing on additional capacity. Per Compass Minerals:

{kind=link}

Compass Minerals Phase 1 Output (Compass Minerals)

Now remember, Koch was willing to invest $252 million into a project that will ultimately ramp to about 37,500 tonnes. Given that, what would Koch be willing to invest into a project that currently is targeting 27,400 tonnes? The project also has the capacity to ramp much higher if say neighboring Albemarle ( ALB ) were to partner with Century and provide water. Consider that the present mine footprint is just a portion of the viable land that Century has.

It should be noted that ALB currently has roughly 10,000 acre feet of water that it is not using and in past statements they have stated they were exploring clay possibilities in Clayton Valley. It is our understanding that the clay that ALB has is buried deep, as opposed to Century Lithium which has clay near the surface.

{kind=link}

Century Lithium Property in Clayton Valley (Century Lithium )

thyssenkrupp nucera - A Second Contender

thyssenkrupp nucera ( OTCPK:TKAMY ) is another large company that might be interested in taking an equity position in Century Lithium as they will gain detailed insights into how the Century flow sheet works . This also should be viewed as a dating exercise. Just how much insight will thyssenkrupp nucera gain into the inner workings of Century? Per the PR:

thyssenkrupp nucera’s scope of work will include the development of a facility concept for treatment of the recovered brine stream from Cypress’ process and ensure compatibility with the membrane electrolysis cells of a chlor-alkali plant. Standardized and proprietary e-BiTACv7 BiPolar type membrane cell electrolyzers from thyssenkrupp nucera serve as the heart of the chlor-alkali plant to generate the key reagents HCl (hydrochloric acid) and NaOH (sodium hydroxide) required to process the lithium ore. The NaCl (sodium chloride) and H 2 O (water) molecules present in the recovered brine are electrolyzed to produce Cl 2 (chlorine), H 2 (hydrogen) and the sodium hydroxide, where then outside of the cells, the chlorine and hydrogen molecules are combined to produce hydrochloric acid."

Remember, Lithium Americas told us around the GM buy-in that they had 50 suitors approach them for Thacker Pass. It is not unreasonable to speculate that Century will have suitors approach them as the DFS nears completion.

Century Lithium's Funding Strategy - A Theory

It is our theory that any equity buy-in would have to occur at a stock price that might mimic Standard Lithium: Not giving too much of the company away, but yet providing funding in return for a small bite of Century equity. Also, such price would need to be north of the bulk of the warrants' prices below. This would motivate warrant holders to execute the warrants, providing Century with additional funding. If the equity buy-in were priced lower than the warrants price of $2.65, the warrants could act as a wall to stock price appreciation.

Looking at the Q3 Sept 30, 2022 filing , we can see the following warrants:

{kind=link}

Century Lithium Warrants (Century Lithium)

Hence, the share price needs to be some degree north of $2.65. (Let's just say $3 to $4 a share.) Taking Standard Lithium's 8% that they sold to Koch and applying that to Century, we would see: 146.53 million shares of Century times our $4 price target = $586 million market cap. Take 8% of that and you get almost $47 million. That amount would help shore up Century Lithium's balance sheet.

Additionally, an equity buy-in might put pressure on obvious potential partners be it Albemarle ( ALB ) or General Motors ( GM ).

Risk To Century Lithium

I am taking my prior risk assessment and putting it here with updates.

When we think about risk and Century Lithium, we need to consider company- specific risk and industry-wide risk. Concerning company-specific risk, the biggest threat is decreasing capital. As of September 30, 2022, Century had $31.3 million in working capital. Compared to other lithium companies, this is a healthy amount given the burn rate per year. Granted, this burn rate should increase now a little since the company has tasked out third parties for the feasibility study.

I see no need for the company to currently raise capital at the moment and given the low share price it is not an optimal time anyway. Granted I assume Century would want a reserve war chest so I could see additional raises down the road but that is anyone's guess as to what threshold of decreasing capital would trigger that (or on the flip side what high share price might motivate the company to build up the company treasury).

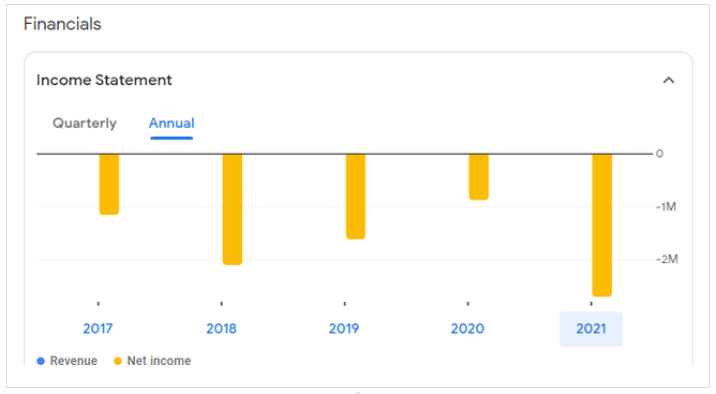

The emphasis is with the current cash position they can move forward for a few years at the very least with the low burn rate. Below we can see the burn rate in yellow (aka negative net income).

{kind=link}

Century Lithium Annual Burn Rate (Google Finance)

Concerning geographic risk, Nevada is one of the friendliest states towards mining in the United States. Geographic risk is low. Another point of interest is infrastructure. Without access to power and roads, any project can be challenged. Century is next door to Albemarle at Silver Peak, Nevada, which has ample roads. A future power line is planned as Century has rights to a geothermal asset that is north of the property. This can be seen on the map below at the top right. Concerning water, Century is one of only three companies in Clayton Valley to have any meaningful water rights. Those without water are in a questionable state of being. Will they be acquired at a reasonable price or left to wither on the vine? Hence, having water puts Century in a strong stance as far as project viability.

Constructive Criticism Of Century Lithium

One thing that sharp investors look for is insider buying. Nothing compliments a good stock like seeing an entire management team buying on the open market. I realize that insiders often have hordes of options granted to them and this is fine. Yet, I have been of the opinion that some insider buying sends a strong signal to Wall Street and to the masses that management is both savvy and confident in the stock.

The counter argument of getting too heavy in a stock might apply if you are management and earning options. If you were management you might even argue the concept of diversification, rather than increase your ownership in one asset but in the end no one knows more of the internal workings of a company than insiders.

It was good to see the CEO of Century buying shares on the open market earlier this year, but I would encourage the rest of the company to make some purchases. Even only a few thousand dollars invested by each member sends a powerful message. Do note that blackout periods occur wherein management is unable to buy shares; these are not year round.

Conclusion

As investors, we should expect to see costs for the project rise much like we saw costs rise for Lithium Americas ( LAC ). While not an apples-to-apples project comparison, it does give us a rough idea of what to expect. We should also see the NPV rise massively. Overall, investors should remain patient and observe the trends of industries investing hundreds of billions into lithium and the associated infrastructure. Meanwhile the governments of Canada and the United States continue to invest in future growth via issuing grants to lithium companies. We should expect to see a DFS and a greatly expanded NPV of $2.5+ billion (our guess) and at some future date government loans for Century Lithium too. Things are cheap till they are not cheap. One day we will look back and question why we were not buying more at these prices given the obvious indicators.

For further details see:

Will Koch Buy Into Century Lithium?