MAPS - WM Technology Is Now A Strong Buy (Rating Upgrade)

2023-12-18 07:58:03 ET

Summary

- WM Technology has fallen a lot despite a solid Q3 report.

- MAPS stock has considerable potential upside.

- The profitability and the lack of debt suggest that the stock has less downside than other cannabis stocks.

I wrote about WM Technology ( MAPS ) 12 weeks ago, calling it a good cannabis stock but not my favorite at the time. It has reported its Q3, which was better than expected, but the price has declined a lot since my article. It's still not my favorite cannabis stock, but it is now my largest ancillary position in my model portfolio. In this follow up, I discuss the Q3 results, the updated outlook, the valuation and the chart.

Q3 for MAPS

The company reported its Q3 on November 8th after the close, and it was a very good report. It had been expected to report revenue of about $47 million according to Sentieo. It reported $47.7 million, down 5.5% from a year ago. Adjusted EBITDA was better than expected at $10.7 million. Analysts had expected $4 million. This was a lot better than not only expectations but also the results from a year earlier, -$9.6 million. The company provided a Q4 outlook of $47 million in revenue and $5 million in adjusted EBITDA.

MAPS has no debt, and the cash increased by about $3 million to $27.7 million. In Q3, the cash flow from operations improved to $8.3 million. It was $12.4 million during the first three quarters.

The Outlook

In my write-up 12 weeks ago, I shared that analysts were expecting 2023 revenue to be $194 million with adjusted EBITDA of $19 million. Currently, they still expect revenue to be $194 million, down 10%, but they project that adjusted EBITDA will be a lot higher at $33 million.

The outlook for 2024 was revenue of $207 million and adjusted EBITDA of $27 million. Analysts currently project that revenue will increase 3% to $200 million with adjusted EBITDA of $29 million, a bit higher than beforehand.

As I indicated in my last article, I am using the 2025 estimates for valuation, as a year from now, the stock will be trading on year-ahead projections. Analysts were looking then for revenue of $225 million and adjusted EBITDA of $30 million. Now, they expect revenue of $210 million, which is lower than before, but they have an adjusted EBITDA projection that is higher at $33 million. I had said in that last article that the margins, then 13.5% for 2025, seemed too low, and the projected margin is now 15.9%.

The Valuation

In late September, my target for a year out was $2.04, up 65% at that time. I was using an enterprise value of 2X projected revenue two years out. This was also 15X projected adjusted EBITDA. I am providing a year-end 2024 target now using 10X projected adjusted EBITDA for 2025. I think that this multiple of 10X is likely too low. The company trades on the NASDAQ, and it is debt-free. This is a lot better than its MSO customers, which trade OTC and struggle with debt as well as 280E taxation.

Before, I was using cash of $20 million to calculate the enterprise value. Now, I am using $25 million, which is still below the current cash level. The higher projection boosts my target to $330 million, which is 1.6X projected revenue and works out to a share price of $2.35. This would offer a return of 213%.

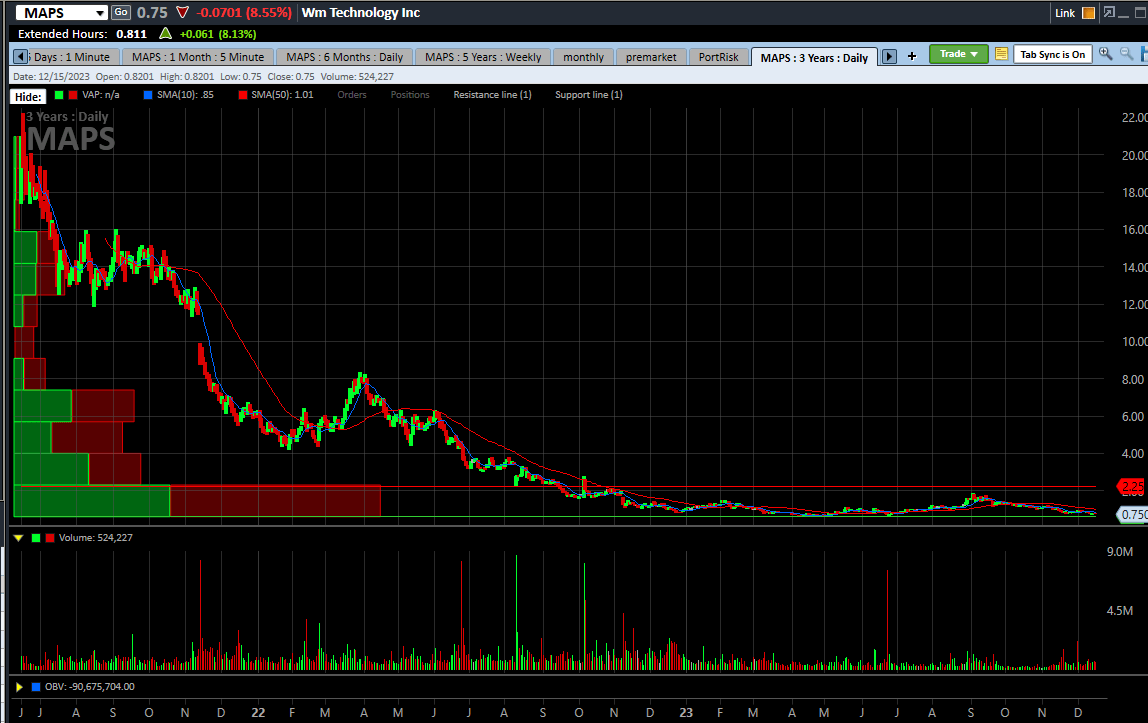

The Chart

I really like the chart. The cannabis market is in a bear market, but this stock looks like it bottomed already. This recent pullback was at odds with the Q3 report and Q4 outlook and analyst estimate changes, but it was consistent with the overall market action as measured by the NCV Global Cannabis Stock Index, which declined 15.5% since that last article. MAPS dropped more, falling 39.5%:

{kind=link}

My target a year from now of $2.35 happens to coincide with the resistance I see at $2.25, and the current price, while far above the all-time low set in late April, is near the support I see at $0.65. The stock is down 25.7% in 2023, which is worse than the Global Cannabis Stock Index, which has dropped 18.8%. NCV also has an index that is for ancillary companies like MAPS, the Ancillary Cannabis Index, which has dropped 14.0%.

Investment Risks

The company is being led now by co-founder Doug Francis, who is the Executive Chair and is serving as CEO now for about a year. He has done a fine job, but the company hasn't announced a new CEO yet. This could become a problem for the company if it selects an inferior leader. While the company has a very strong balance sheet and is generating cash currently, it does trade at a premium to its tangible book value at 3.9X currently. If profitability slips, it could fall as this valuation moves lower. Finally, if 280E remains in place, the company could struggle due to its clients having poor cash flow.

Conclusion

MAPS is 17% of my model portfolio that I share in my investing group, which leaves it as the second largest position. The stock is now down substantially in 2023 and since the cannabis sector peaked in early 2021, and I think the valuation is very reasonable. MSOs will perform the best if rescheduling happens and if it wipes out 280E taxation, but ancillary companies like MAPS will benefit from a healthier customer. If 280E doesn't go away, MAPS and other ancillary companies with strong balance sheets should hold up much better than the MSOs.

For further details see:

WM Technology Is Now A Strong Buy (Rating Upgrade)