WOLF - Wolfspeed: Lower Growth Already Priced In

2024-01-10 03:12:23 ET

Summary

- Wolfspeed's revenue growth has slowed down, with a YoY decline of 18.2% in Q1 FY2023, attributed to the sale of its RF business and sluggish telecom demand.

- The company's focus on SiC power devices and wafer market remains positive, with higher growth forecasts compared to RF power semiconductors.

- Despite losing ground in the SiC power market, Wolfspeed's SiC materials segment shows potential growth with new supply agreements, but competition from top competitors may impact its growth trajectory.

- We believe the lower growth has been more than priced in with its stock price dropping more than 40% last year, which now presents an excellent buying opportunity.

In our previous analysis , we anticipated Wolfspeed, Inc.'s ( WOLF ) revenues to sustain a CAGR of approximately 45% due to the company's focus on expanding manufacturing facilities for SiC materials and wafers. However, considering projected supply growth surpassing demand, despite state and US CHIPS Act subsidies for manufacturing facilities, we foresee Wolfspeed maintaining a cash flow negative status.

In this analysis, we covered the company again as its revenue growth had slowed down below expectations to 24% YoY in FY2023 compared to our previous 42.8% forecasts and declined by 18.2% YoY in Q1 FY2023. Thus, we examine why Wolfspeed’s revenue growth has slowed down. Firstly, we examined whether the company’s slowdown was affected by the sale of its planned divestiture of its RF business. Moreover, we examined its revenue growth based on its Power and Materials segment and determined the factors for its slowing growth. Finally, we examined the company’s competitiveness and market share.

Sale of RF business

Wolfspeed had recently announced the sale of its RF business to MACOM which was completed in December 2023, in a deal valued at $135 mln which we covered previously in our analysis of Macom which “significantly strengthens MACOM's defense capabilities by adding their extensive GaN and SiC product lineup” according to the company.

We compiled and analyzed the company’s revenue breakdown by RF, Power and Materials below.

| Wolfspeed Revenue by Segment ($ mln) |

| 2021 |

| 2022 |

| 2023 |

| Average |

| Power Products |

| 133 |

| 276 |

| 409 |

| Growth % (YoY) |

| 108% |

| 48% |

| 78% |

| Materials Products |

| 242 |

| 296 |

| 349 |

| Growth % (YoY) |

| 22% |

| 18% |

| 20% |

| RF Product |

| 151 |

| 174 |

| 164 |

| Growth % (YoY) |

| 15% |

| -6% |

| 5% |

| Total Revenue |

| 525.6 |

| 746.2 |

| 921.9 |

| Growth |

| 42% |

| 24% |

| 33% |

Source: Company Data , Khaveen Investments

Based on its past earnings briefings, management highlighted its revenue weakness due to poor demand for RF devices. As seen above, the company’s RF business was its smallest segment, though accounted for 18% of its revenues. In terms of growth, it underperformed the Power and Materials segment, with a lower average growth of 5% compared to Power (78%) and Materials (20%). According to Yole , one of the factors for the company’s RF business weakness is sluggish telecom demand. This is amid the smartphone market weakness which is expected to decline by 7% in 2023. Notwithstanding, the company highlighted it is focusing on its Power and Materials businesses going forward following the sale of its RF business to Macom.

Given the significant growth we’ve seen in automotive, industrial and renewable energy markets, we believe this is the right time to further focus on scaling our Power device and materials businesses to meet this accelerated demand, - Gregg Lowe , President and Chief Executive Officer

Comparing the market growth outlook, the RF power semiconductor market has a lower market forecast CAGR of 13.25%, compared to the SiC power devices market CAGR of 31% and SiC wafer market CAGR of 24.8%, thus we believe its focus on the higher growth SiC power devices and wafer market is positive for the company’s growth outlook. Furthermore, in terms of profitability, based on its quarterly report, the company had a net loss from discontinued operations of $272.1 mln, indicating the negative profitability of its RF business.

Outlook

Overall, we believe the company’s divestiture of its RF business is a positive move as it had been lagging behind with lower growth (5%) than the company’s overall growth (33%) compared to its other higher growth Power and Materials segments as well as having negative profitability for the segment. Moreover, as the company focuses on Power and Material segments going forward, we believe this could benefit the company’s overall growth outlook due to the stronger market growth forecasts of SiC power devices (31% CAGR) and wafers (25% CAGR) compared to RF power semiconductors (13.25% CAGR).

SiC Power Growth

| Wolfspeed Revenue ($ mln) |

| Q1 FY2023 |

| Q1 FY2024 |

| Average |

| Power Products |

| 105 |

| 101 |

| Growth % (YoY) |

| -3.2% |

| -3.2% |

| Material Products |

| 85 |

| 96 |

| Growth % (YoY) |

| 13.3% |

| Revenue of Disposed Businesses |

| 51.9 |

| Total Revenue |

| 241 |

| 197 |

| 194 |

| Growth % (YoY) |

| 54.2% |

| -18.2% |

| 39.7% |

Source: Company Data, Khaveen Investments

Besides the sale of its RF business which impacted its revenue growth, the company’s growth across its Power and Materials segments had also slowed down sharply in Q1 2024. Its Power Products segment growth was negative at -3.2%, compared to 48% in 2023, while its Materials segment growth was 13.3% compared to 18% in 2023.

Based on the company’s earnings briefing , the reason for the lower Power growth was attributed to “slower industrial and energy demand, primarily in China and the broader Asian market”. However, the company primarily depends on the automotive segment which is larger than Industrial.

{kind=link}

Wolfspeed

Based on Yole Development's latest market forecast, the SiC power market has a CAGR of 31% through 2028, slightly lower compared to its previous forecast of a 34% CAGR. We compiled the top 4 SiC power companies’ revenues in 2023 based on their latest earnings briefings. For example, STM stated that it is on track to register $1.2 bln in revenue in 2023 while Infineon reached EUR500 mln in revenues. According to ON Semiconductor, the company lowered its SiC revenue target by 20% to $800 mln in 2023 as it highlighted a reduction in demand within the automotive sector but still represents an impressive growth of 300%. For Wolfspeed, we prorated its 2023 Power segment revenue growth whereas for Rohm, we based it on its 2023 revenue growth. For the revenue in Others, we estimated it based on its past 2-year average growth.

{kind=link}

Company Data, Khaveen Investments

| SiC Revenue ($ mln) |

| 2021 |

| 2022 |

| 2023F |

| STMicro ( STM ) |

| 500 |

| 700 |

| 1200 |

| Growth Rate (%) |

| 66.7% |

| 40.0% |

| 71.4% |

| Infineon ( OTCQX:IFNNF ) |

| 200 |

| 316.1 |

| 582.1 |

| Growth Rate (%) |

| 100.0% |

| 58.1% |

| 84.1% |

| Wolfspeed |

| 165 |

| 343 |

| 508 |

| Growth Rate (%) |

| 52.8% |

| 108.1% |

| 47.9% |

| Onsemi ( ON ) |

| 80 |

| 200 |

| 800 |

| Growth Rate (%) |

| 45.5% |

| 150.0% |

| 300.0% |

| Rohm ( OTCPK:ROHCF ) |

| 108 |

| 123 |

| 127 |

| Growth Rate (%) |

| 4.9% |

| 14.3% |

| 3.0% |

| Others |

| 37 |

| 196 |

| 600 |

| Growth Rate (%) |

| -18.1% |

| 429.8% |

| 205.8% |

| SiC Market Size |

| 1,090 |

| 1,879 |

| 3,817 |

| Growth % |

| 53.3% |

| 72.4% |

| 103.1% |

Source: Company Data, Yole Development, Khaveen Investments

As seen in the table, we estimated the total SiC power market to grow by 103.1% in 2023, which represents a faster growth rate compared to the previous year which contradicts claims of a market slowdown. All of the top companies’ growth in 2023 is higher except for Wolfspeed and Rohm. The company that experienced the most significant growth is onsemi whose market share among the top companies increased by 13% to 26% while all other companies' shares declined. Thus, we further examine possible reasons for Wolfspeed’s underperformance by updating our analysis of SiC power product breadth and performance.

| SiC Comparison |

| Number of SiC Products (Change) |

| Volts (Range in V) |

| RDS(On) (m?) |

| 650-1199V |

| 1200-1699V |

| >=1700V |

| STMicro |

| 89 (+26) |

| 1700 |

| 8.8 - 1300 |

| 34 |

| 51 |

| 4 |

| Wolfspeed |

| 69 (+5) |

| 1700 |

| 15 - 1000 |

| 33 |

| 32 |

| 4 |

| Infineon |

| 102 (+39) |

| 2000 |

| 7 - 1000 |

| 36 |

| 56 |

| 8 |

| onsemi |

| 106 (+19) |

| 1700 |

| 6 - 960 |

| 48 |

| 52 |

| 6 |

| Rohm |

| 91 (+8) |

| 1700 |

| 13 - 1150 |

| 41 |

| 47 |

| 3 |

| Average |

| 91 (+16) |

| 38 |

| 48 |

| 5 |

Source: Company Data, Khaveen Investments

Based on our analysis, Infineon and onsemi outpaced other companies in terms of the number of SiC products, with 39 and 19 new products added this year. Wolfspeed not only has the smallest product count but also falls below the average in terms of added products, indicating a lack of product breadth advantage. Furthermore, in terms of performance, Wolfspeed’s maximum Volts is lower than that of Infineon, and its RDS(On) range, while better than onsemi, does not match up to other companies like STMicro or Rohm, thus demonstrating a lack of a performance advantage as well, which does not bode well for the company’s competitive positioning the SiC market.

In contrast, we see that onsemi, with the highest growth in 2023, has a product breadth advantage with the widest SiC portfolio among competitors and we believe benefits the company to secure more design wins with customers as management highlighted that its “design activity has been robust across all regions” to over “500 unique customers that will continue to ramp through 2024” from its latest earnings briefing . Furthermore, we believe Infineon, with the second-highest growth rate in 2023, could continue to outperform competitors including Wolfspeed. Infineon’s management also provides impressive revenue growth expectations of 50% in 2024 as it announced over 20 new design wins from top automakers and as it builds the largest SiC chip manufacturing facility, which is 1.6x higher than the market CAGR of 31%, indicating potentially more share gains.

One clear bright spot is our silicon carbide business where we see unabated momentum from industrial as well as automotive customers … In line with the unbroken strong demand we are seeing, we are significantly expanding our manufacturing capacities by building the world's largest, most competitive 200-millimeter silicon carbide power fab in Kulim, Malaysia. - Jochen Hanebeck , Chief Executive Officer of Infineon

{kind=link}

Wolfspeed

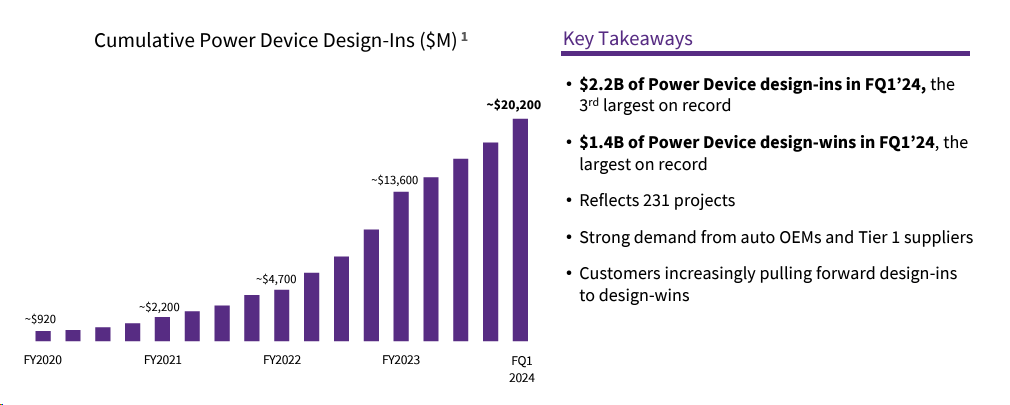

However, despite a lack of competitive advantage in product breadth and performance, the company’s cumulative design-ins continuously increased to $20.2 bln compared to $920 mln in FY2020, a 22x increase. Assuming it takes 10 years for its design-ins to be realized, we derived a CAGR of 25.6% for its Power segment growth.

| Wolfspeed Revenue Projections ($ mln) |

| 2023 |

| 2024F |

| 2025F |

| 2026F |

| 2027F |

| 2028F |

| 2029F |

| 2030F |

| Power Products |

| 409 |

| 514 |

| 645 |

| 811 |

| 1,019 |

| 1,280 |

| 1,480 |

| 2,020 |

| Growth % (YoY) |

| 25.6% |

| 25.6% |

| 25.6% |

| 25.6% |

| 25.6% |

| 25.6% |

| 25.6% |

Source: Company Data, Khaveen Investments

Outlook

Overall, despite the company’s claims of a market slowdown within the SiC power market, we believe that its underperformance is mainly attributed to strong competition within the SiC power market as its top competitors such as onsemi, Infineon and STMicro have faster growth in 2023 as well as the total SiC power market growth higher than Wolfspeed’s growth, resulting in further market share losses by 5% to 13.3% for the company. On the other hand, we believe competitors such as onsemi have a competitive advantage in terms of product breadth, which supported its strong rise to a market share of 21% as its revenue increased by 300%. Nonetheless, the company's total value of design-ins has continued to expand to $20.2 bln. This translates to a forecast CAGR of 25.6% which is still lower compared to the market CAGR of 31% but still decent.

While its stronger competitors such as onsemi and Infineon are pursuing aggressive manufacturing expansions globally such as in South Korea (onsemi) and Malaysia (Infineon) as well as securing new deals from top automakers, we believe they are not as focused in SiC as Wolfspeed. Following the company's divestiture of its RF business, it is now a pure-play SiC company and we believe the company could focus its efforts on improving its SiC competitiveness to take a larger share of SiC growth going forward.

SiC Materials Growth

Furthermore, at this point, we examined the company’s Materials segment. In our previous analysis, we highlighted the unique business model of the company supplying SiC power devices as well as SiC materials to its competitors. We also highlighted its positive outlook supported by supply agreements with STMicro, onsemi and Infineon. Wolfspeed remained the largest player in the SiC materials market with a 53% market share in 2022. Its competitors in the market such as Coherent (II-VI) ( COHR ), SiCrystal, SK Siltron and TankeBlue. Coherent trails Wolfspeed in second place with a 19% share, an impressive increase from 14% previously and also recently announced a $1 bln investment from Denso and Mitsubishi Electric in relation to its SiC business.

| Company |

| Deal Valued ($ mln) |

| Year Announced |

| 2,000 |

| 2023 |

| 225 |

| 2022 |

| STMicroelectronics |

| 800 |

| 2021 |

| ON Semiconductor |

| 85 |

| 2018 |

| Infineon |

| 100 |

| 2018 |

Source: Company Data, Khaveen Investments

Since our previous analysis, the company has announced two new deals related to the supply of SiC which include Renesas ( OTCPK:RNECF ) with a 10-year $2 bln deal for “silicon carbide bare and epitaxial wafers” and an unnamed company with a $225 mln deal, bringing its total value of contracts for SiC materials with customers at $3.2 bln.

{kind=link}

Wolfspeed

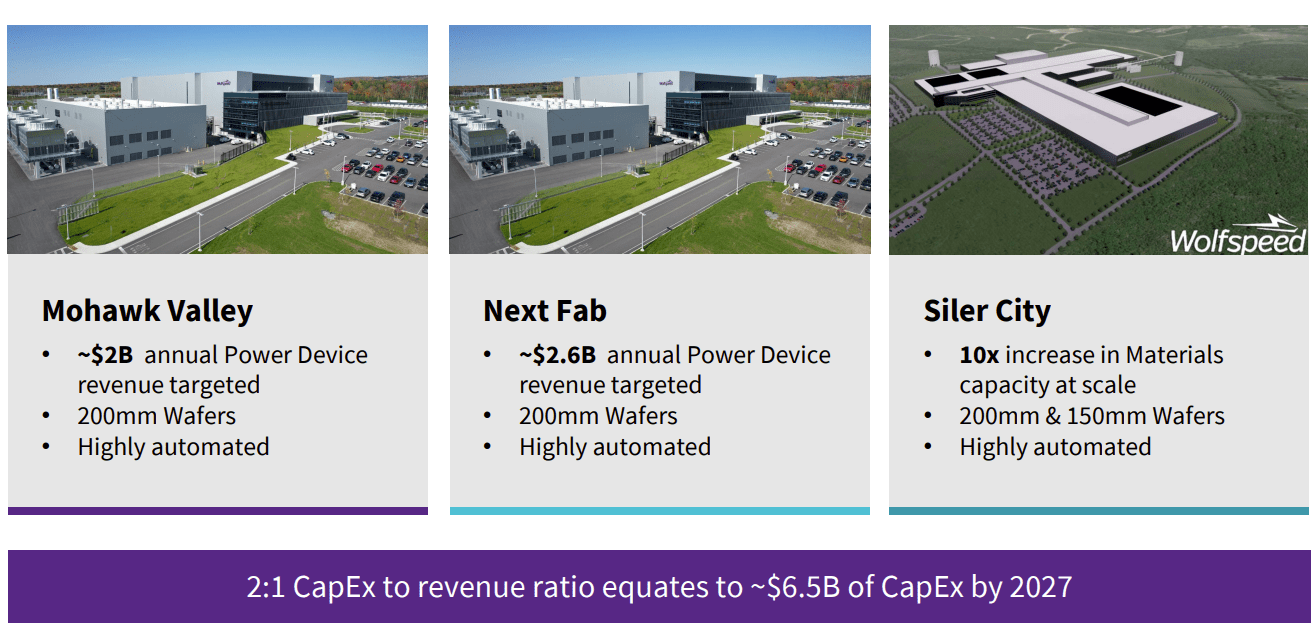

To support its growth, the company has several expansions planned including Mohawk Valley, a new fab worth $3 bln in collaboration with ZF where ZF would be contributing $185 mln for a minority stake as well as Siler City which is mainly for SiC materials with a planned 10x increase in capacity.

| Wolfspeed Revenue Projections |

| 2023 |

| 2024F |

| 2025F |

| 2026F |

| 2027F |

| 2028F |

| 2029F |

| 2030F |

| Power Products |

| 409 |

| 514 |

| 645 |

| 811 |

| 1,019 |

| 1,280 |

| 1,480 |

| 2,020 |

| Growth % (YoY) |

| 25.6% |

| 25.6% |

| 25.6% |

| 25.6% |

| 25.6% |

| 25.6% |

| 25.6% |

| Materials Products |

| 349 |

| 643 |

| 728 |

| 830 |

| 953 |

| 1,101 |

| 1,279 |

| 1,493 |

| Growth % (YoY) |

| 84.0% |

| 13.2% |

| 14.1% |

| 14.8% |

| 15.5% |

| 16.2% |

| 16.7% |

| RF Product |

| 164 |

| 0 |

| 0 |

| 0 |

| 0 |

| 0 |

| 0 |

| 0 |

| Total |

| 922 |

| 1,156 |

| 1,373 |

| 1,641 |

| 1,972 |

| 2,381 |

| 2,759 |

| 3,513 |

| Growth % (YoY) |

| 25.4% |

| 18.7% |

| 19.5% |

| 20.2% |

| 20.7% |

| 15.9% |

| 27.3% |

Source: Company Data, Khaveen Investments

To project the company’s SiC materials segment, we derived a growth forecast based on the company’s past 2-year average growth rate of 20% in addition to a total value of new deals of $2.25 bln over 10 years based on the terms of the Renesas deal. Based on this, we derive a forward 5-year average of 28.3% and average growth of 24.9% through 2030 for its Materials segment with a surge in growth in 2024 factoring its new deals but with a lower growth beyond 2024 due to the risks is its customers expanding their own in-house SiC wafer manufacturing.

For example, onsemi has recently completed its new SiC wafer fab and ramping up to a capacity of 1 mln SiC wafers per year and management also highlighted its achievement of increasing the manufacturing of 50% of its SiC substrates internally following its acquisition of SiC substrates producer GTAT 2 years ago. Furthermore, another risk is its customers such as Infineon have also been diversifying their suppliers with Infineon signing a deal with Chinese firm SICC for SiC wafers as Chinese firms expand production capacity aggressively according to DigiTimes. Notwithstanding, we believe Wolfspeed has a competitive advantage as the sole current producer of more cost-effective 8-inch SiC wafers which could support its competitive position with the shift to 8-inch wafers. According to Yole , its lead in 8-inch wafers is expected to continue over the next 2 years until competitors expand their manufacturing capabilities.

Outlook

Overall, we believe that despite the company losing its competitiveness in the SiC power devices market, its SiC materials segment could support its total growth driven by its new agreements with Renesas and another company with a total deal value of $2.25 bln.

Wolfspeed is the only company operating in both the SiC Power Devices and Materials markets. Hence, its competitors' strength in the SiC power devices market improves the prospects of Wolfspeed in the SiC materials market as a supplier to its own competitors as evidenced by its long-term contracts with key companies and recently Renesas in a 10-year deal. Hence, we have a higher growth outlook for Wolfspeed's Materials segment with a projected forward average of 24.9% through 2030 factoring in its new deals, higher than its past 2-year average segment growth of 20%. Our forecasts are also in line with the market CAGR of SiC wafers of 24.8%, thus we expect the company to maintain its market leadership position in the SiC wafer market supported by its competitive advantage as the current only producer of 8-inch wafers but also note risks such as the expansion of internal wafer manufacturing capabilities of some of its customers and emerging competition from Chinese firms.

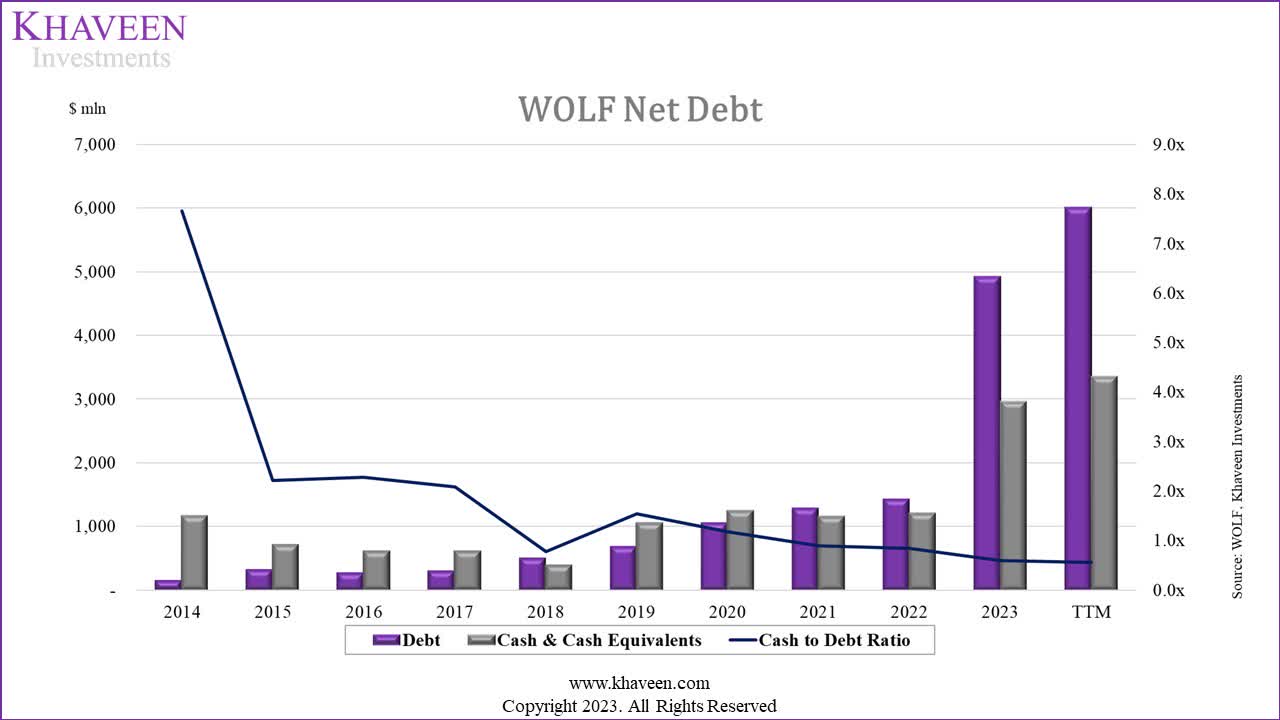

Risk: Financials and Short-Term Headwinds

{kind=link}

Company Data, Khaveen Investments

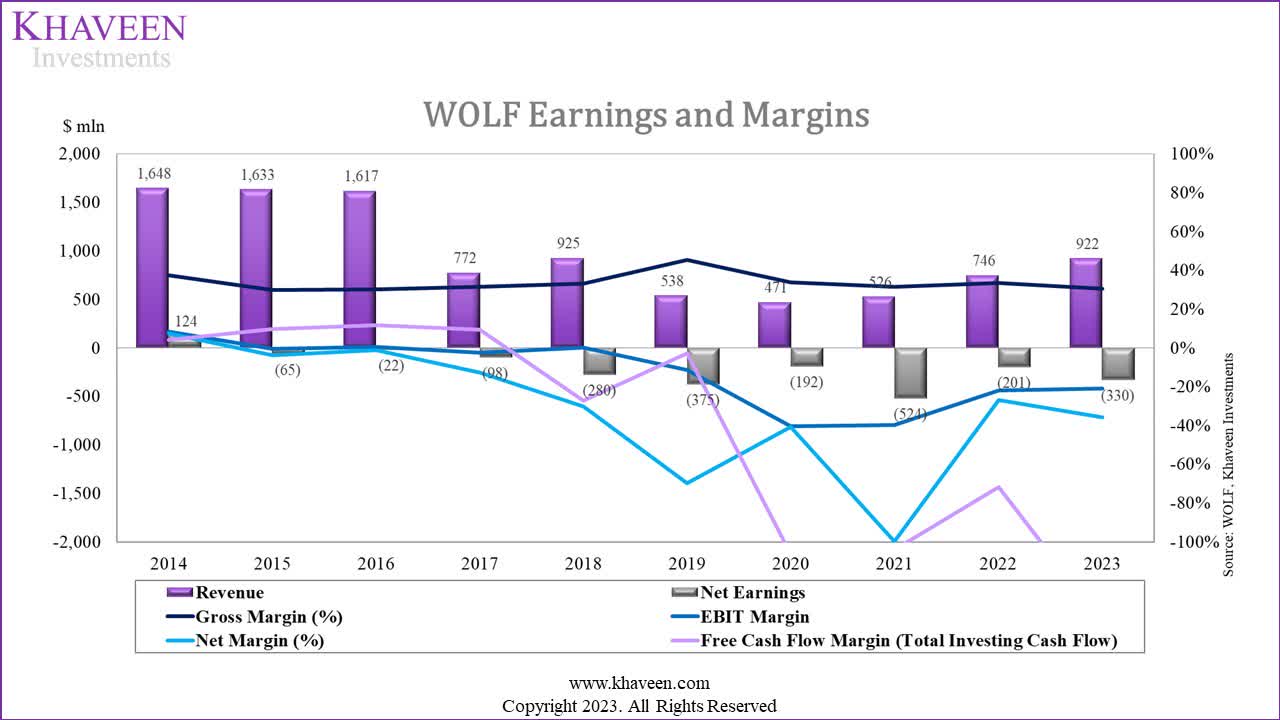

Despite an increase in revenue in the past three years, Wolfspeed still has negative profitability. While there was an improvement in 2022, it decreased again in 2023, with the FCF margin reaching over -100%. We believe the substantial increase in debt in 2023 for the expansion plan further accelerates Wolfspeed’s risky financial position. Recently, Wolfspeed further raised $1.25 bln in debt, resulting in its debt at its highest level in the past 10 years.

{kind=link}

Company Data, Khaveen Investments

That said, we also believe macroeconomic headwinds may pose challenges for growth in the short term as the global GDP growth is forecasted to slow down by 0.3% in 2024 to 2.4% based on the UN . We believe that this could trickle down to the EV market given lower government incentives such as reduced subsidies in the world’s largest market China which could affect the SiC market growth outlook as automotive is 70% of the total market. However, we believe the long-term EV growth outlook remains positive as the penetration rate was only 17% in 2023, indicating further growth opportunities.

Verdict

In total, we projected a total revenue growth forward 5-year average of 20.9%, driven by both the SiC power segment growth of 25.6% and SiC materials growth of 28.3%, offset partially by the sales of its RF business (18% of revenue in 2023). While our average growth projection is lower compared to our previous forecast of 45% mainly due to lower growth expectations for the Power segment, we believe it is still decent and we continue to value the company based on a P/S ratio valuation given its high growth but still negative profitability.

| Valuation |

| 2024F |

| 2025F |

| 2026F |

| 2027F |

| Revenue ($ mln) |

| 1,156 |

| 1,373 |

| 1,641 |

| 1,972 |

| Growth % |

| 25.4% |

| 18.7% |

| 19.5% |

| 20.2% |

| P/S |

| 5.71x |

| 6.20x |

| 6.70x |

| 7.20x |

| Valuation ($ mln) |

| 6,601 |

| 8,518 |

| 10,993 |

| 14,188 |

| Shares outstanding ('mln') |

| 125.33 |

| 125.33 |

| 125.33 |

| 125.33 |

| Price Target |

| $52.67 |

| $67.97 |

| $87.72 |

| $113.21 |

| Current Price |

| $40.81 |

| $40.81 |

| $40.81 |

| $40.81 |

| Upside |

| 29.1% |

| 66.6% |

| 114.9% |

| 177.4% |

Source: Khaveen Investments

We updated our P/S valuation of the company based on the semicon industry average P/S of 7.2x and our revised revenue projections through 2027. Based on our prorated price target for 2024, we derived a 29% upside.

All in all, we believe that the company's decision to divest its RF business is a positive strategic move, considering its past underperformance with lower growth (5%) compared to the company's overall growth (33%) and negative segment profitability. We believe focusing on the Products and Materials segment seems promising, particularly given the stronger market growth forecasts for SiC power devices (31% CAGR) and wafers (25% CAGR) compared to RF power semiconductors (13.25% CAGR).

Moreover, while competition has intensified especially from key players such as onsemi and Infineon which have product breadth and performance advantages respectively over the company, we believe the company, now a pure-play SiC company following its RF spinoff, could focus its efforts on improving its SiC competitiveness to take a larger share of SiC growth going forward. Furthermore, despite lower competitiveness in the SiC power devices market, we highlighted its unique business model of operating in both the SiC power devices and SiC materials market. We believe the company could continue capitalizing on the strength of SiC power device competitors who are its customers, benefitting the prospects of its materials segment as evidenced by the new deals valued at a total of $2.25 bln, increasing our forecast for the segment at 24.9% through 2030, fairly in line with the market growth despite risks of customers expanding internal wafer production capabilities and emerging competition from China.

In total, we revised our overall revenue projections with a 5-year forward average of 20.9%, significantly lower than 45% previously mainly due to the company's RF business sale and our lower growth expectations for its SiC power segment (25.6% vs 55% previously) but still supported by its Materials segment growth which is stronger than its past average (20%). As a result, we derived a much lower price target of $52.67 compared to $154.44 previously due to a 24% reduction in our revised average forward revenue forecast as well as a lower average P/S ratio of 7.2x compared to a prorated P/S average of 12.64x previously. Despite that, the company's stock price has collapsed by 64% since our last coverage, thus we believe the lower growth forecasts are already reflected in its current price and we rate it as a Buy.

For further details see:

Wolfspeed: Lower Growth Already Priced In