WOLF - Wolfspeed: The Right Speed To Own

Summary

- Wolfspeed reports another disappointing quarter as supply chain issues and lower RF demand hit revenues.

- The Silicon Carbide company will power ahead with strong sales growth due to new fabs and EV demand.

- The stock is now appealing trading at 2.5x FY27 sales targets after dipping $35.

The biggest problem with investing in Wolfspeed ( WOLF ) was the prior premium valuation. The stock is now trading in the below $80 due to the general weakness in the semiconductor market prior to all of the new design-in wins kicking into production. My investment thesis is now ultra Bullish on the stock as the long-term plan hasn't changed, but the stock has fallen over $35.

Source: FinViz

Focus On Design Wins

Wolfspeed reported FQ2'23 revenues of only $216 million. The revenue figure was $10 million below analyst estimates and fell substantially from the $241 million reported in the prior quarter.

The company guided for FQ3'23 revenues of $210 million to $230 million, far below analyst expectations for revenues of $249 million. Management suggested demand issues in 5G impacted the RF product line while supply chain issues slowed down output at the Durham materials factory.

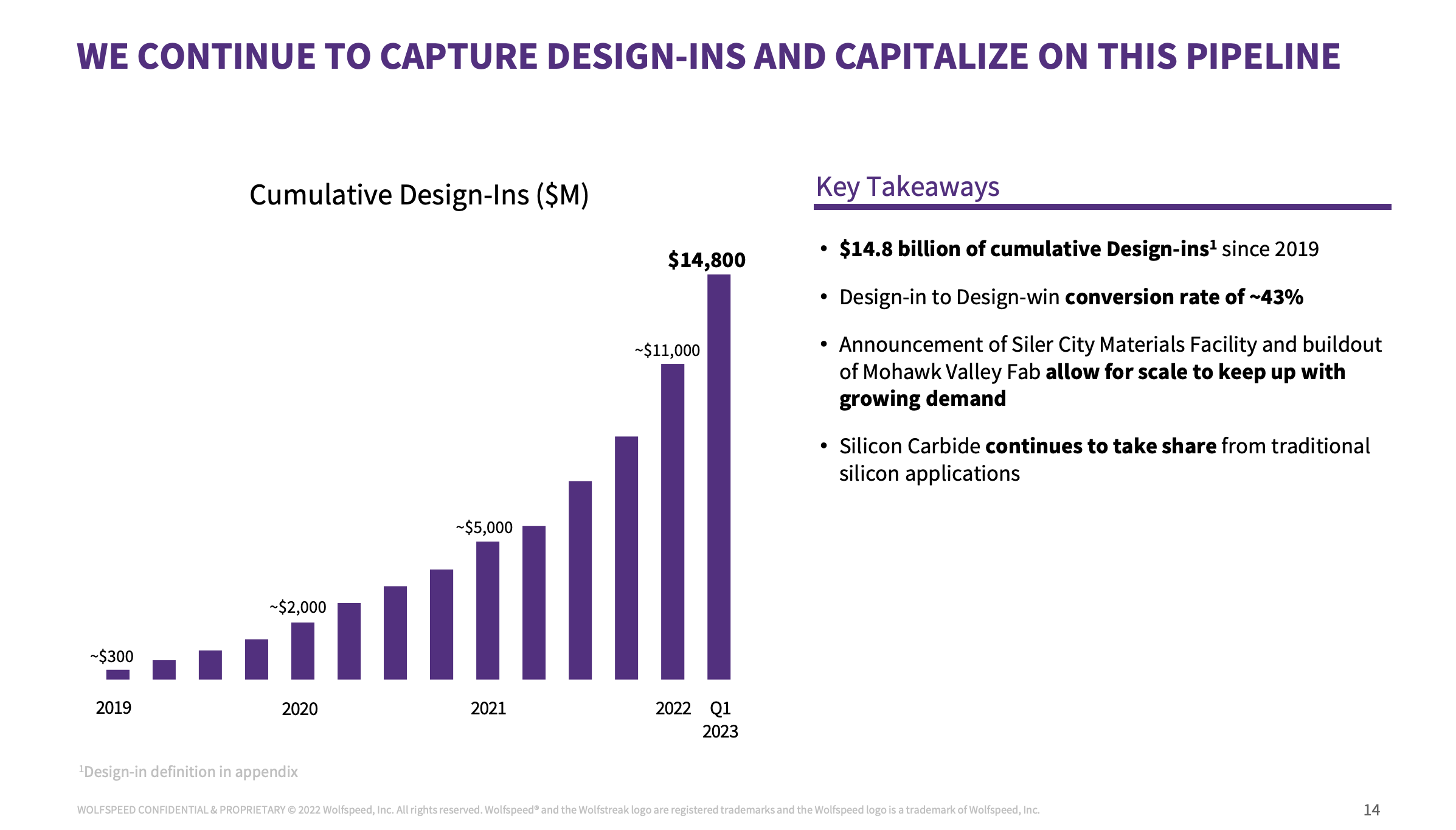

The more important metric on the earnings report was another $1.5 billion of design-in wins during the quarter. The metric is up 25% YoY and adds to a business that already included $14.8 billion of design-in wins since 2019.

{kind=link}

The Silicon Carbide technology from Wolfspeed has huge benefits for electric vehicles and other renewable energy technology. Since Investor Day 2021, cumulative design-in wins have grown from $5 billion to over $16 billion now while the opportunity pipeline has surged to over $40 billion.

Loving The Dip

The market cap has fallen to $10 billion, making the stock a far better deal than previous levels closer to $15 billion. Wolfspeed had already guided to FY26 revenue target to surge to $2.95 billion, providing some perspective for the weak numbers in the current quarter with a temporary dip in 5G demand prior to EV production kicking into full gear.

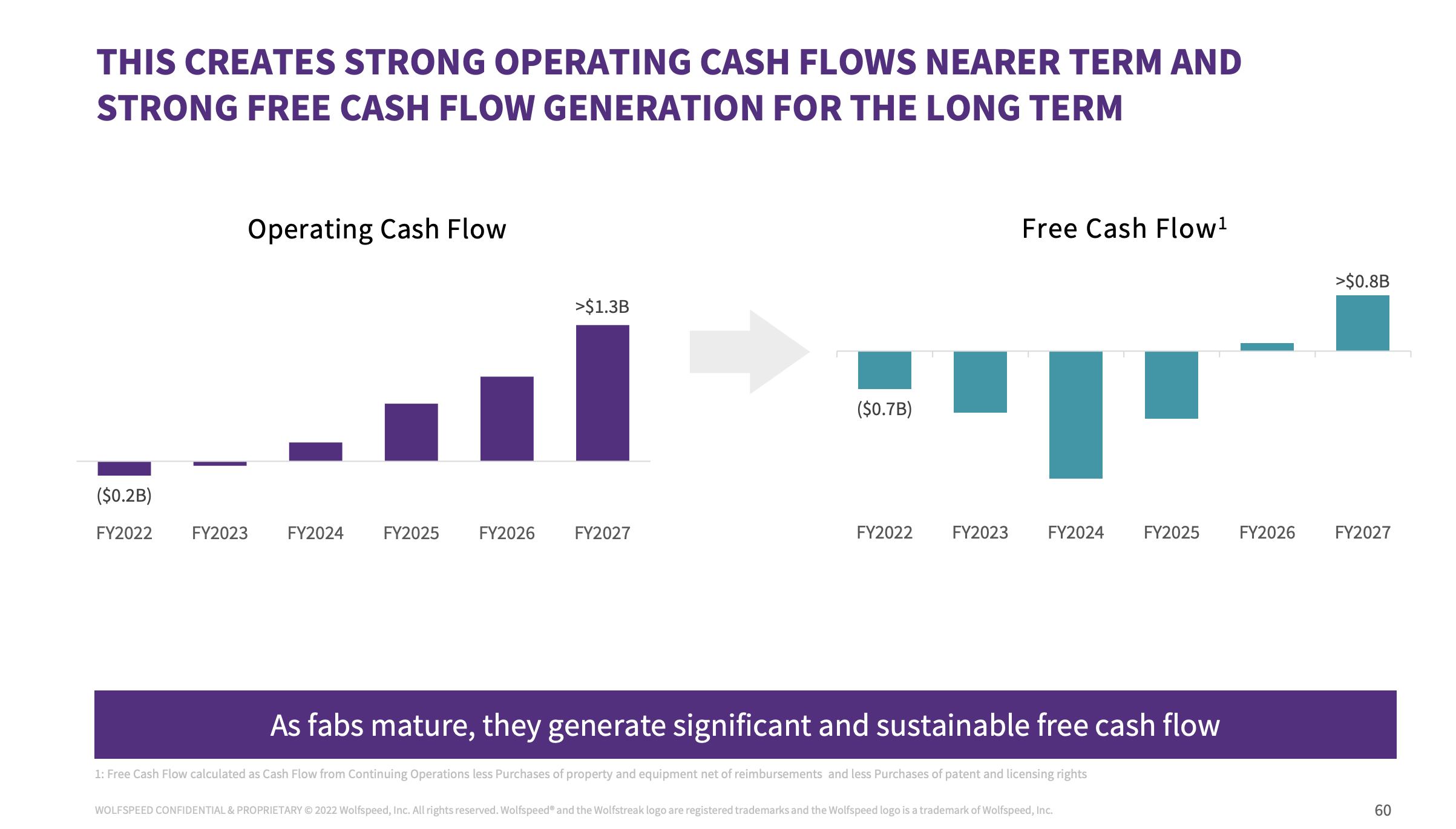

Cash flows remains the biggest question with disappointing losses and revenues in the near term. Wolfspeed guided to a FQ3'23 loss of up to $20 million when the expectation was for the company to cut losses going forward.

The prime reason this matters to this long-term story is that Wolfspeed had forecast breakeven cash flows in FY23 leading to strong positive cash flows in FY24. The company recently increased FY23 capital spending to ~$1 billion due to the surging pipeline wins.

The problem is that Wolfspeed now has to spend billions in new fabs and suddenly revenue isn't hitting expectations. The semiconductor materials company now forecasts large free cash flow losses through FY25 with plans to spend more than $2 billion in FY24 for the Siler City plant just renamed to The John Palmour Manufacturing Center for Silicon Carbide.

{kind=link}

The company is investing for the future with expectations now for FY27 revenues to surge to $4 billion, producing ~45% EBITDA margins. As an example of the growth potential, the Mohawk Valley fab is executed to start producing revenues in the June quarter and will ultimately generate up to $2 billion in annual power device revenues.

Wolfspeed ended the quarter with cash of $2.5 billion while debt is already at over $3.0 billion after issuing convertible debt. The company will need to borrow more money to fund the facilities expansion before the revenues and cash flows arrive in the years ahead as EVs hit the market.

The risk is definitely that EV demand doesn't meet expectations as the market shifts from small market share to levels around 50% by end of the decade. Wolfspeed is spending aggressively ahead of this demand and any shortfall in demand could leave the company with ongoing operating losses after spending heavy on new fabs.

Takeaway

The key investor takeaway is that Wolfspeed is now more appropriately valued for the opportunity ahead. The stock now trades at only 2.5x FY27 revenue targets, providing multiples of upside if the company hits those sales targets.

For further details see:

Wolfspeed: The Right Speed To Own