WDS - Woodside Energy Group: Appealing Dividend But Some Turnaround Is Needed Here

2023-12-13 20:14:02 ET

Summary

- Woodside Energy Group's stock price has been steadily declining, trading at a low P/E of under 6 and a dividend yield of over 7%.

- The company is involved in various segments of the hydrocarbon industry, with a robust global portfolio and strong earnings growth.

- The Asia Pacific region presents a high demand for energy, and WDS is well-positioned to meet these demands, with potential for further investments and approvals.

Investment Rundown

Since late July of this year, the stock price of Woodside Energy Group Ltd ( WDS ) has been steadily trending downwards. The company is mostly involved in the gas and oil industry where it offers various services and gets involved in exploration and evaluation of sites and projects too. Because of the significant downturn in share price the last few months it now trades at a low p/e of under 6 and a divine yield of over 7%. Part of the challenges the company has faced is both difficult market conditions causing production guidance to be narrowed and also being blocked in court for a seismic survey plan.

Despite the last few months having the share price fall quite rapidly I am not 100% confident it's the right time to get in. I want to see more positive commentary on the production levels of the business before suggesting a potential buy here. What I want to make very clear though is that holding shares still has a lot of value seeing as the dividend yield is so high right now and well supported by strong earnings growth and resilience too. WDS is one I am going to keep on my watchlist but not something I would be adding more to right now.

Company Segments

WDS is involved in hydrocarbons, spanning exploration, evaluation, development, production, marketing, and sale. Operating across diverse regions , including Oceania, Africa, the Americas, Asia, and the Caribbean, the company is a prominent player in the global energy landscape.

Company Overview (Investor Presentation)

{kind=link}

At the core of WDS operations is the production and distribution of a range of hydrocarbon products. This includes liquefied natural gas, pipeline gas, condensate, natural gas liquids, and crude oil. These diverse products cater to a wide array of energy needs, reflecting WDS's commitment to providing reliable and versatile energy solutions to its global clientele.

WDS stands as one of the foremost independent Exploration and Production companies in Australia, commanding a prominent position in the energy sector. The company boasts a robust global portfolio that encompasses an array of strategic assets, showcasing its diversified presence and influence on the international stage. The company has taken strong growth initiatives over the years and the merger with BHP Petroleum greatly boosted the revenues and they are the last 12 months by over $18 billion.

Shareholder Commitments (Investor Presentation)

{kind=link}

As the company is generating such high revenues they have also been able to raise the margins and in the last 12 months, they are at over 35% right now. With that, the amount of capital that has been going towards shareholders has steadily been increasing. The divine payout ratio peaked at 92% in 2022 and since the merger was completed there have been over $6.3 billion in payments made already. Going forward WDS seems adamant on maintaining a high ratio and ensuring that shareholders get a solid return on their investments. Should a similar payout ratio of 80% be maintained we might be looking at 2024 having over $5.2 billion worth of dividends, or $2.7 per share, at an FWD yield of over 10% potentially. I think this enhances why WDS might be a solid long-term opportunity right now following the sell-off in recent months. What keeps me from making it a buy is that I want to see a turnaround in the production levels. Increased production levels would be a great tailwind for the company and likely send the stock price higher. Holding shares you get plenty of value and having some patience here I think will be rewarded in due time.

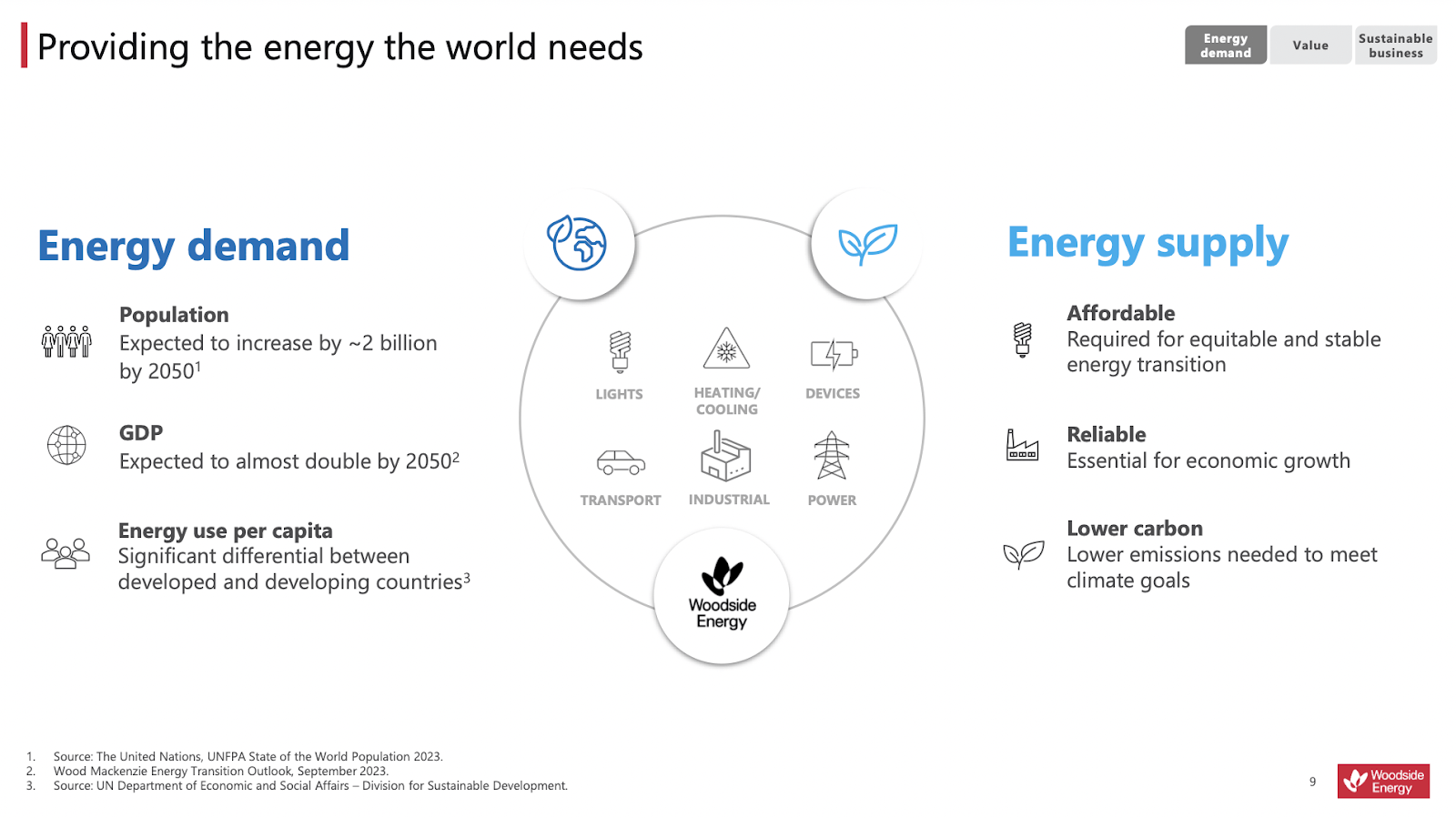

Markets They Are In

Market Overview (Investor Presentation)

{kind=link}

Right now there is a lot of poor sentiment around both gas and oil as they lack the renewable aspect that both solar and wind have. This has potentially led to an accelerated pace of transition over the past few years. One of the highest demanding regions is the Asia Pacific as there is immense economic growth here but also population growth. With that comes further demand for energy and in the region, it seems likely that oil and gas will continue to make up a large portion of that energy pool. One part that is losing a lot of steam is coal, an extremely pollution-emitting way of generating energy, but one that is widely used in the region. There needs to be a lot of further investments as well into the regions to meet these energy demands and I think WDS will have an easier time getting things approved in the coming decades as the necessity of generating more energy becomes clearer.

The company operates in a commodity market where prices are the judging factor essentially for how revenues and earnings may look. I think what WDS is doing to be more resilient and hedge against potential short-term volatility is to take advantage of higher commodity price times and use those earnings to invest in a strong infrastructure of assets. This should lead to lower depreciation and affect the bottom line less I think. We have seen a negative depreciation in the last 12 months by $500 million which is moving the company in the right direction. Besides this, the company is also strong financially with nearly $4 billion in cash ready to be deployed to expand the asset base further.

Earnings Highlights

Income Statement (Earnings Report)

{kind=link}

Looking closer at the last report from the company released on October 18, 2023 , it has become clear there are some challenges in the production levels of the business. The production of Mboe per day has declined by 7% YoY and resulted in revenues falling by 44% YoY, which is also the result of softer prices for both gas and oil. YTD changes are where the positives grow for the productions at least, as they are up 31%. On a sequential basis, it's up by 8% and for both Q4 and Q1, I want to see this trend continue which could potentially lead me to rate it a buy for investors. There have been some other solid milestones achieved during the quarter that are worth mentioning, like the achievement of the first productions in Shenzi North, which wasn't thought to happen until 2024.

Dividend Summary (Seeking Alpha)

{kind=link}

A key thing about WDS is the solid dividend it offers to investors. Right now over 7.82% and the merger that occurred in 2022 has helped ensure its growth at 12.47% CAGR in the last 5 years. Going forward I anticipate further growth to the divined as a result of continued stable demand for gas, despite lower prices. I don't think that the divided will be growing by those high double digits forever each year, but I do think a reasonable assumption is around 6 - 7% each year. My assumption for this is supported by the fact that WDS now is a far larger company and is generating net incomes of over $6 billion. The last 12 months have meant $4.5 billion in dividend payouts, which puts it at roughly a 66% payout ratio. Not extremely high in my opinion for a company in the oil and gas sector. Over the last 10 years WDS has managed to achieve a 10% CAGR for the EPS and with access to more assets I think this can continue, which would outpace the growth of the dividend and put WDS in a good position to continue to raise it further.

Valuation-wise the company is below the energy sector's p/e of 9 by nearly 30% and I think that is partly because of the lower YoY production rates we have seen. Until there is a clear trend of production going up and an improved pricing environment for both gas and oil I don't see WDS approaching a p/e of 9 in the short-term. With the above-mentioned positives of the dividend, it remains to be a very solid hold for investors.

Risks

While WDS stands to benefit from the inherent volatility of natural gas, particularly in the event of unexpected occurrences like a severe winter storm driving up gas prices , the current landscape presents a mixed outlook. On the positive side, the potential for a spike in natural gas prices remains, especially if unpredictable weather conditions contribute to increased demand.

Natural Gas Prices (Tradingeconomics)

{kind=link}

However, the near-term horizon presents challenges, with cuts from OPEC contributing to an overall tough market climate, where cuts are meant to almost artificially support prices as outputs are reduced globally. This scenario introduces a level of uncertainty that may impact the short-term stability of commodities, including natural gas and oil. This I think together with rising global temperatures could in some quarters lead to less usage of oil and natural gas, potentially leading to softer revenues for WDS.

{kind=link}

WDS encounters additional risks and hurdles that demand attention. The repercussions of a milder winter have translated into reduced production in the Bass Strait, leading to a decline in both revenues and earnings. This scenario raises concerns, especially if the trend of warmer seasons persists, potentially diminishing the demand for gas. However, despite these challenges, the current impact on the overall investment thesis for WDS may not be deemed substantial enough to warrant a sell recommendation. It's crucial to delve deeper into the company's resilience strategies, including its capacity to adapt to changing environmental dynamics and implement innovative solutions.

Final Words

The oil and gas industries are notoriously volatile as the prices heavily rely on demand and production policies around the world. What worries me is that WDS might see falling production levels and that introduces some risk to investors here as the company may not be capable of producing the same high earnings as previously. What has been great to see though is the dedication to ensure shareholders right now get some value, as the payout ratio remains over 80%. In 2024 that puts WDS at an FWD dividend yield of nearly 10% and is a key factor as to why holding shares in the business still makes a lot of sense.

For further details see:

Woodside Energy Group: Appealing Dividend, But Some Turnaround Is Needed Here