WDS - Woodside Energy: Remain Cautious For Now

2023-12-04 22:27:24 ET

Summary

- Woodside Energy Group's 2023 financial performance is expected to be weaker due to lower commodity prices.

- The company's H1/2023 performance was in line with estimates, but significantly lower than H2/2022.

- With weak commodity prices, I suggest investors step to the sidelines and await better pricing on WDS shares or an improvement in economic data.

Back in my last update , I warned that Woodside Energy Group's ( WDS ) 2023 financial performance would likely be much weaker than 2022 due to lower commodity prices. I was also concerned about the stock's weak performance and recommended $22 as a trailing stop to exit my position, to lock in a modest gain from my initial recommendation of around $21.

Unfortunately, the stock recently took out my stop loss so I have stepped to the sidelines, collecting roughly 20% total return from investment, mostly from the Woodside's fat dividend.

As we reach the end of 2023, let us review Woodside's performance so far in the year and what would get us back into the stock.

Brief Company Overview

Woodside Energy Group is one of Australia's largest independent E&P companies. Its global portfolio includes LNG assets in Australia, oil assets in the Gulf of Mexico, and other exploration and development projects around the world (Figure 1).

Figure 1 - Woodside overview (WDS investor presentation)

2023 Is A Step Back Financially...

In my last update, I predicted 2023 would be a step back financially on lower commodity prices:

Assuming realized prices of ~$75-80/boe, Woodside may see revenues of $13.5 billion to $15.2 billion. A $75-80/boe pricing environment would most resemble Woodside's 2021 results, when the company saw a 28% net margin. Therefore, I expect Woodside to report ~$4 billion (28% net margin) in net profits for 2023, or approximately $2.10/share (with 1.9 billion shares outstanding).

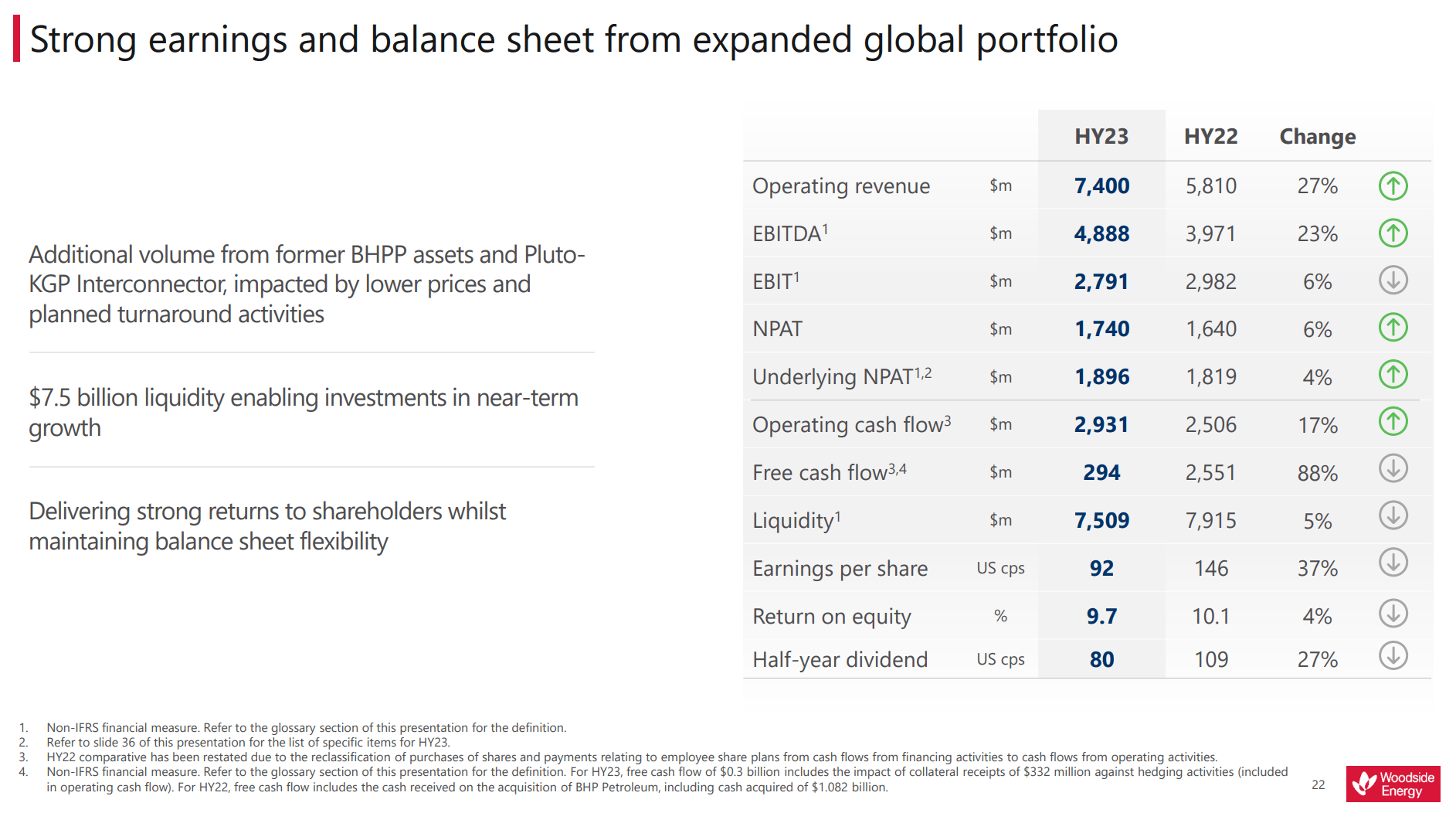

In fact, Woodside's H1/2023 performance was right in line with my estimates, as the company reported $7.4 billion in revenues and $1.9 billion in underlying Net Profit After Tax ("NPAT"), roughly half of my full year forecast (Figure 2).

Figure 2 - WDS H1/2023 financial summary (WDS investor presentation)

{kind=link}

While financial performance was still higher YoY, they softened materially from H2/2022, when Woodside reported $11.0 billion in revenues and $4.9 billion in NPAT.

...On Normalizing Commodity Prices

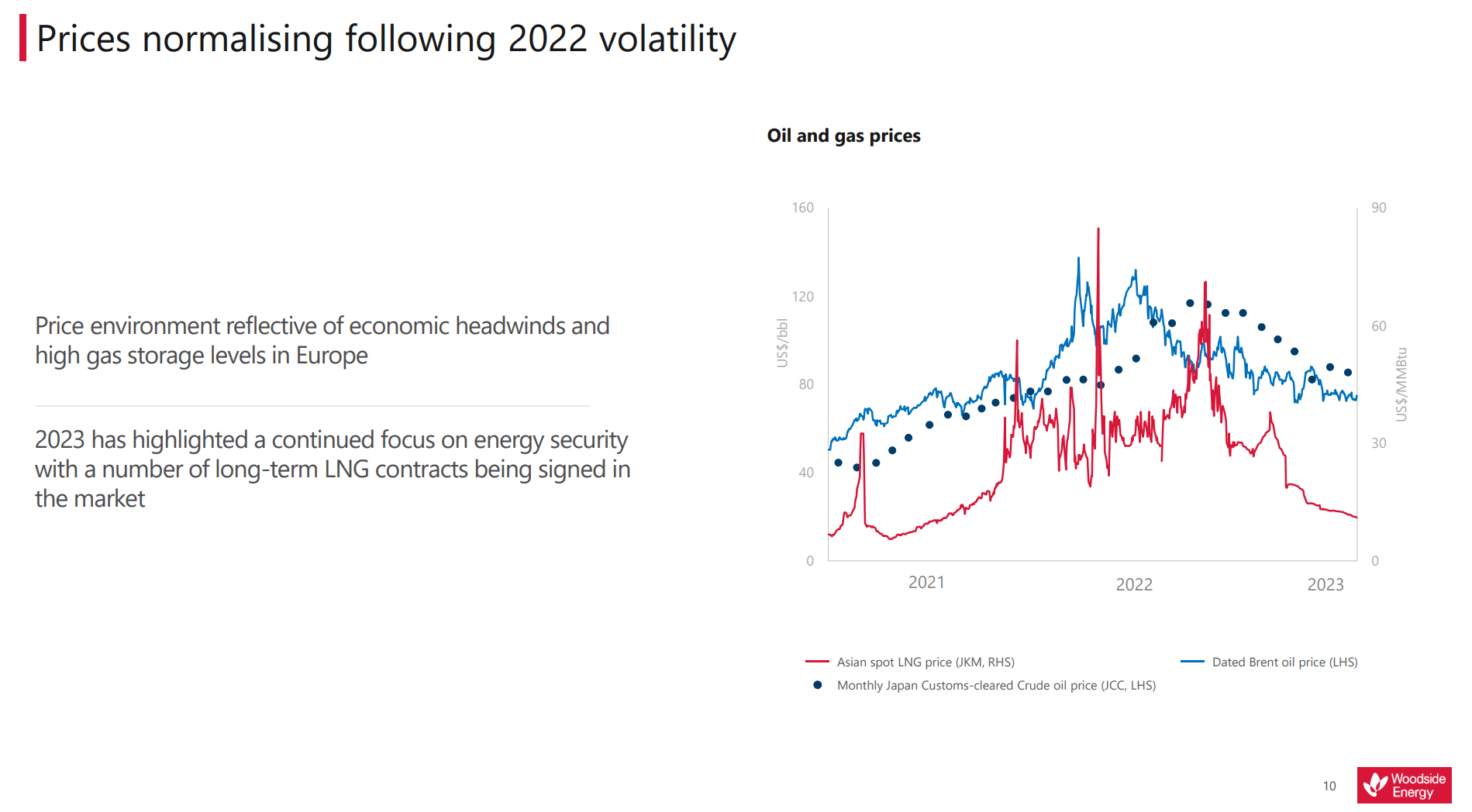

Woodside's weaker financial results reflect normalization in commodity prices after 2022's bonanza, with economic headwinds and European gas storage weighing on LNG prices in particular (Figure 3).

Figure 3 - Commodity prices normalizing after bonanza 2022 (WDS investor presentation)

{kind=link}

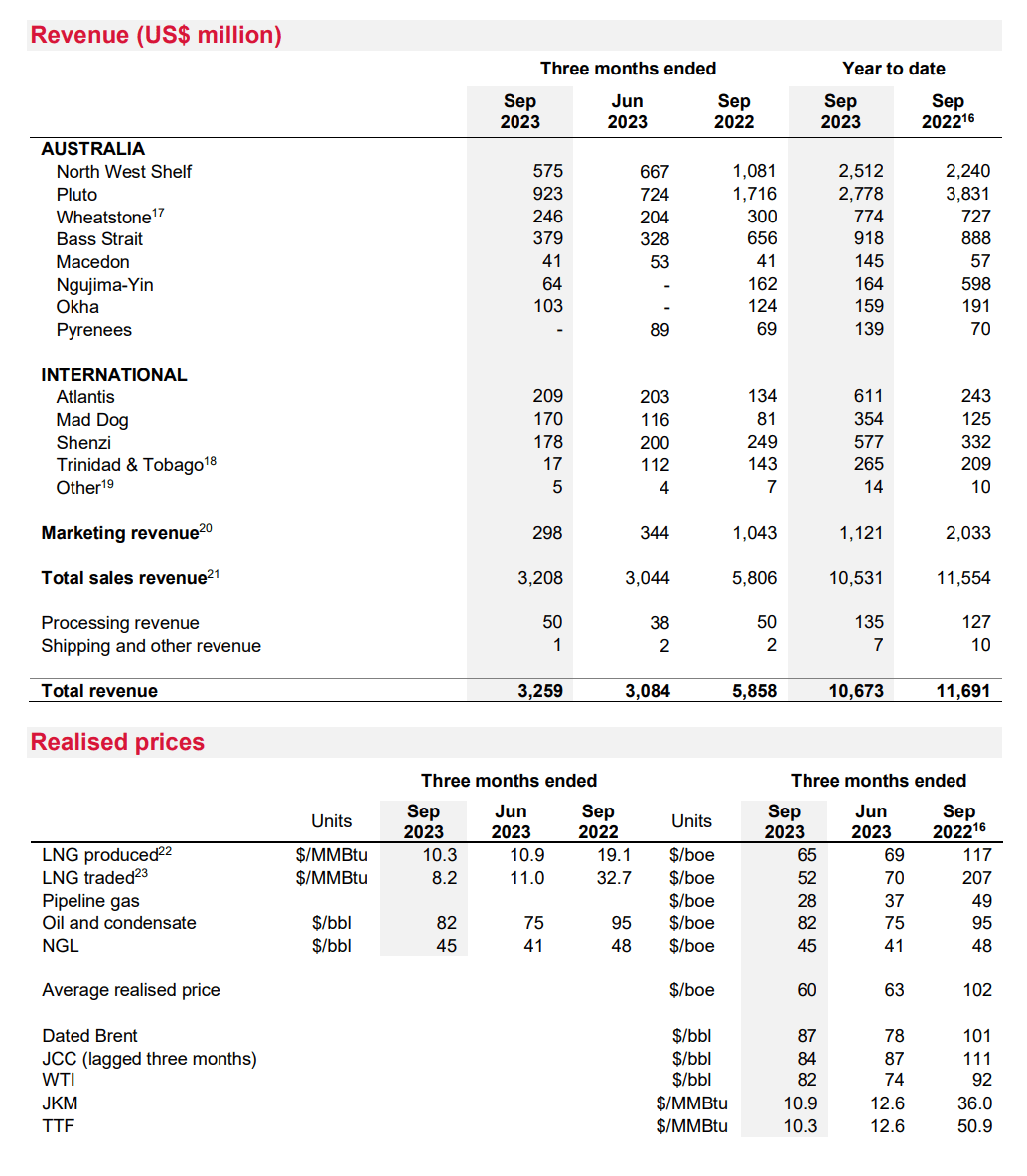

Furthermore, in the most recently reported quarterly update, Woodside's average realized prices slipped further to just $60 / boe, down sequentially from $63 in the June quarter and $102 in the prior year's Q3, primarily on lower LNG prices (Figure 4).

Figure 4 - WDS Q3/2023 operating update (WDS Q3/2023 operating update)

{kind=link}

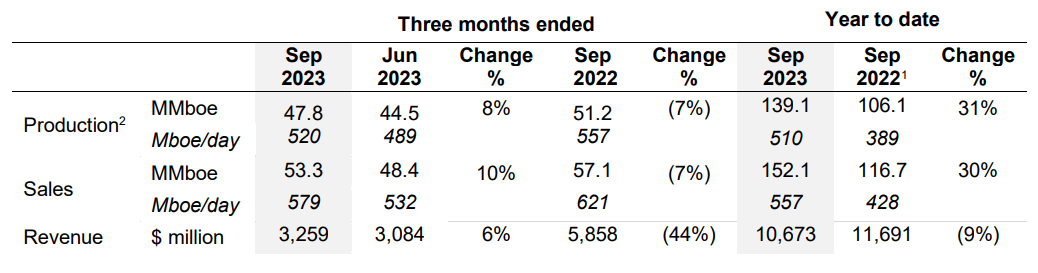

However, operationally, Woodside performed well, producing 47.8 mmboe in the third quarter, 8% ahead of Q2. YTD, production of 139.1 mmboe is 31% ahead of 2022 at the same point in time (Figure 5).

Figure 5 - WDS operations are performing well (WDS Q3/2023 operating update)

{kind=link}

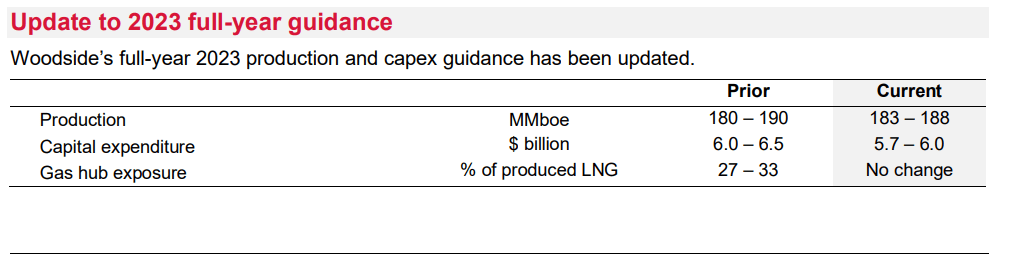

With the third quarter operating report, Woodside also updated its full-year guidance, narrowing the production range from 180-190 mmboe to 183-188 mmboe while lowering capex estimates from $6.0-6.5 billion to $5.7-6.0 billion (Figure 6).

Figure 6 - FY guidance range narrowed (WDS Q3/2023 operating update)

{kind=link}

Growth Projects Progressing Well

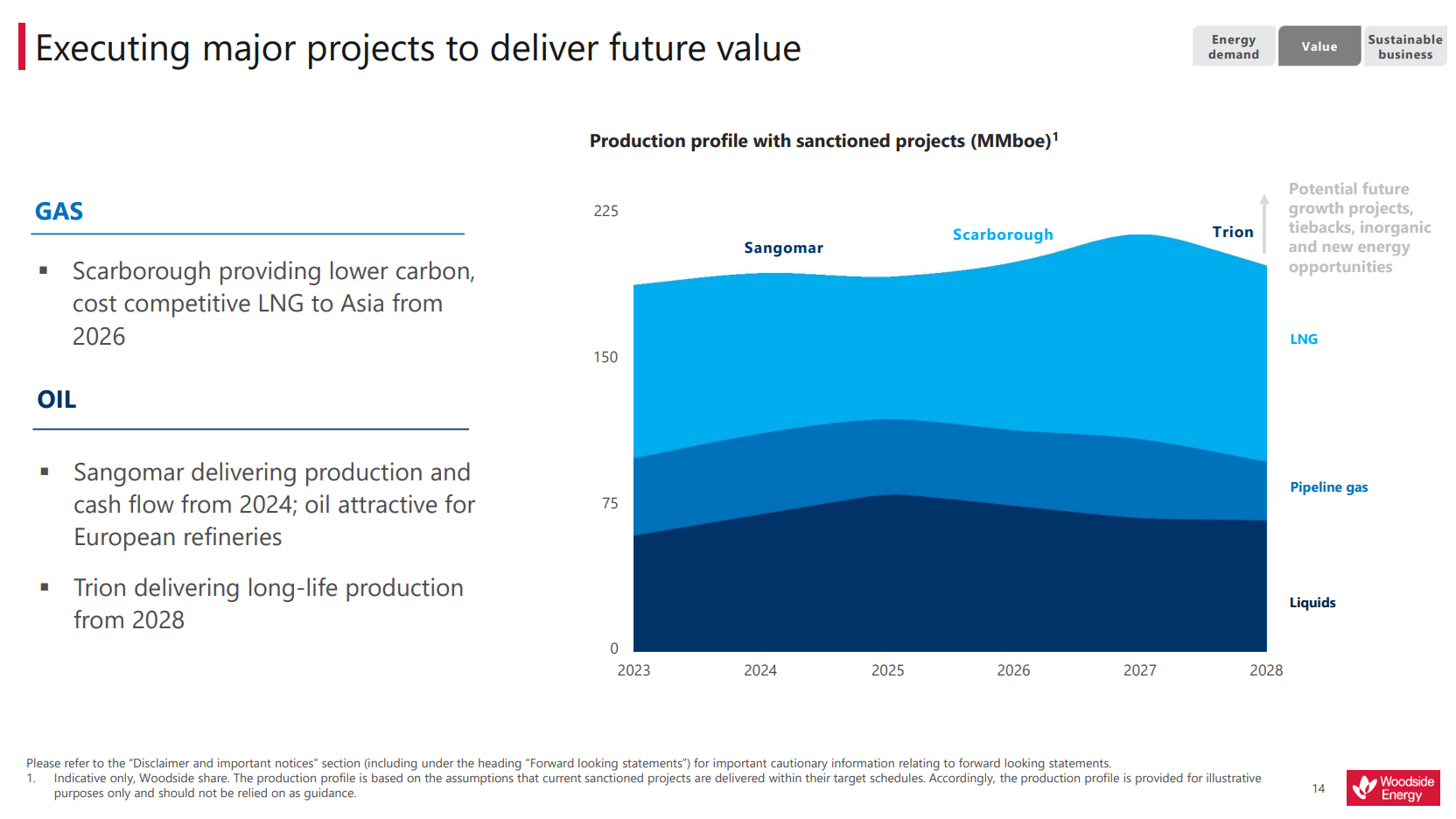

Looking farther out, Woodside's long-term growth projects continue to progress well. Sangomar, a Senegalese oil field, is 90% complete and expected to produce first oil in mid-2024 (Figure 7).

Figure 7 - Development projects progressing well (WDS investor presentation)

{kind=link}

Scarborough, a giant offshore gas field in Australia, continues to ramp up with Woodside recently selling a 10% stake in the joint venture to LNG Japan, further de-risking the project. First LNG cargo remains on schedule for 2026.

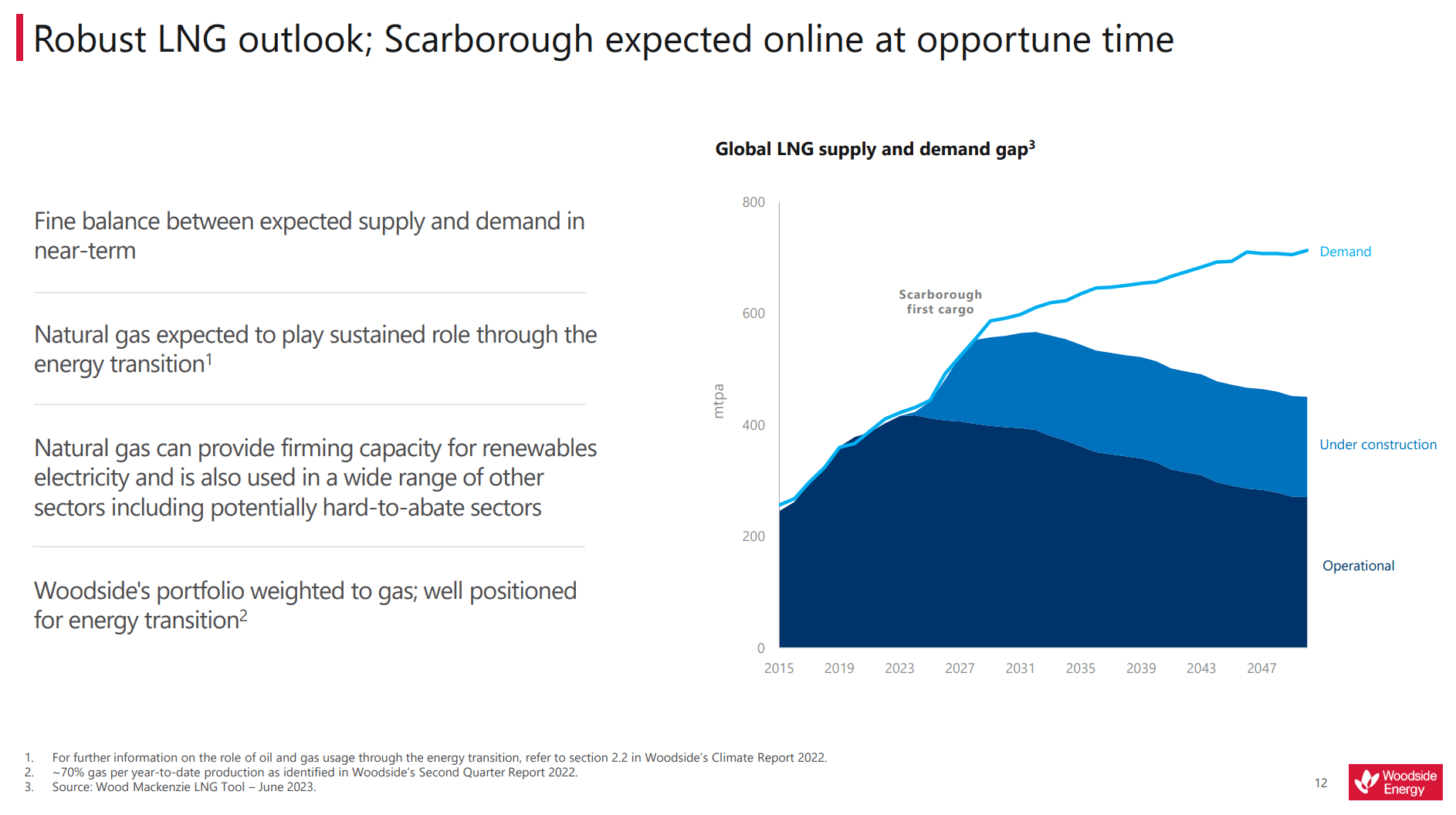

Scarborough is expected to come online just as LNG demand begins to outstrip supply, which should be supportive of LNG prices by the end of the decade (Figure 8).

Figure 8 - LNG supply/demand forecast (WDS investor presentation)

{kind=link}

Technicals Broke Down Foreshadowing Weak Gas Prices

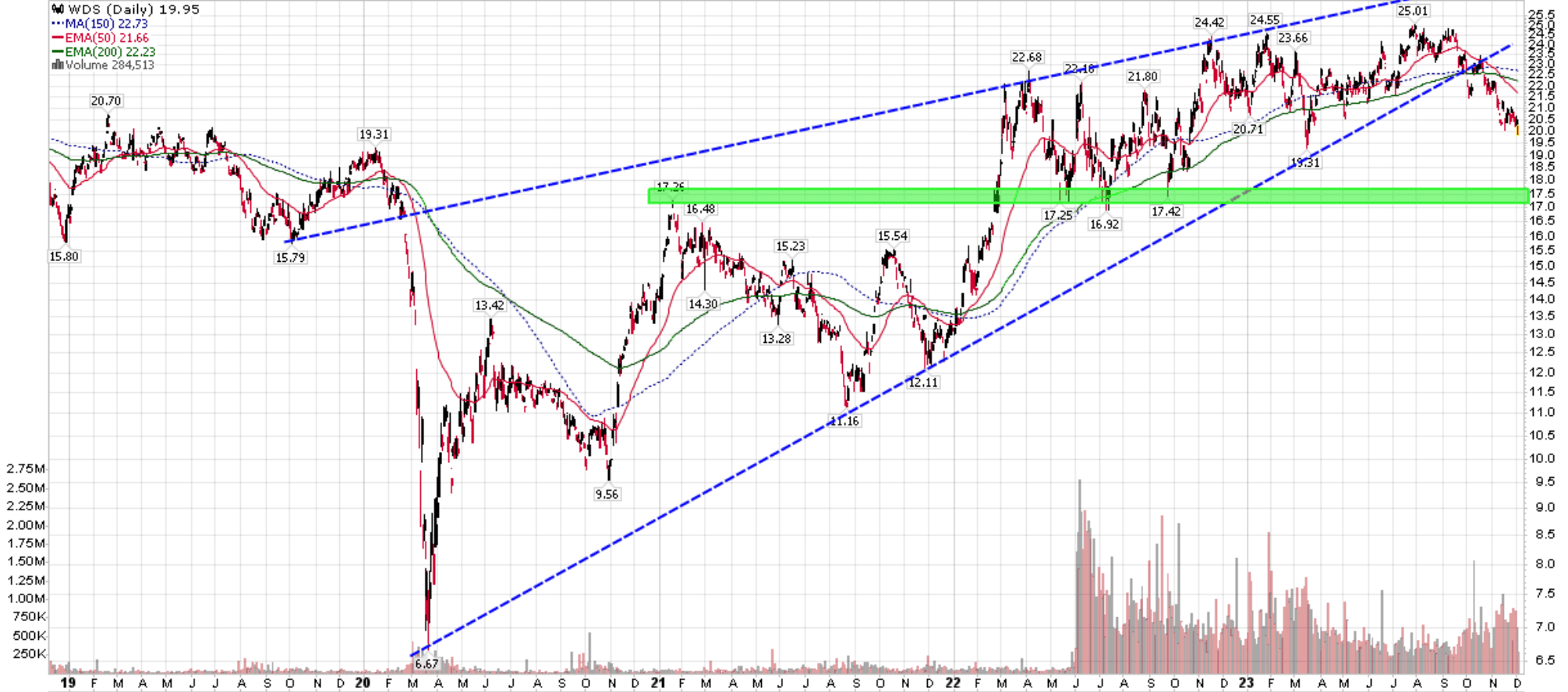

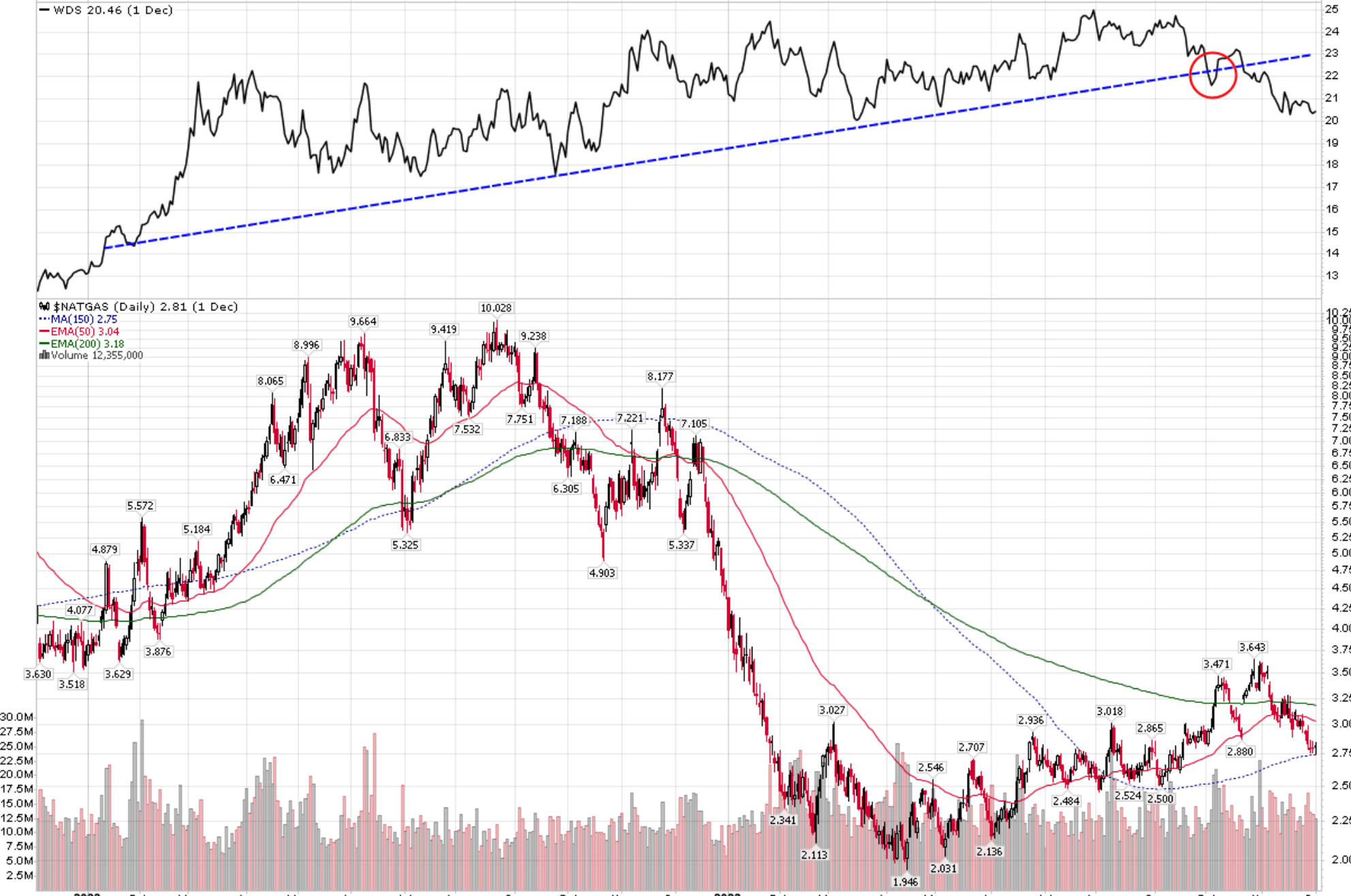

Technically, Woodside shares recently broke down from the uptrend that has kept me in the trade since mid 2022 (Figure 9).

Figure 9 - WDS shares broke from uptrend (Author created with price chart from stockcharts.com)

{kind=link}

While I continue to like Woodside's growth profile in the long run, what I have learned from my portfolio management days is that it is important to respect technical breakdowns, as it could be a sign of the market having more information than you.

For example, WDS broke down in early October even when natural gas prices were rallying. This actually foreshadowed the recent breakdown in natural gas prices as Europe is experiencing yet another mild winter , reducing the consumption of natural gas and LNG (Figure 10).

Figure 10 - WDS broke down despite natural gas price rally, foreshadowing recent weakness in gas (Author created with price chart from stockcharts.com)

{kind=link}

At this point, I believe WDS may have to fall to ~$17-17.50 support level, highlighted in Figure 9 above, before investors who bought the stock in the past 2 years are washed out.

Risks To Woodside

On the upside, natural gas is one of the most volatile commodities and a freak winter storm could squeeze gas prices higher, providing a boost to stocks like Woodside. Furthermore, China could stimulate its economy, spurring demand for energy and thus firming gas prices.

On the downside, OPEC+ recently announced it would be deepening and extending its voluntary production cuts to March 2024. This suggests demand for energy commodities remains weak.

Conclusion

Although I like Woodside's growth profile and commodity exposure in the long run, I fear weak global economic growth will weigh on energy producers and thus I have exited my position in Woodside's stock.

I believe the stock may be interesting if it falls toward the $17-$17.50 support range and would patiently wait for pricing to come down to my buy level.

For further details see:

Woodside Energy: Remain Cautious For Now