HXL - Woodward: Stay Away Despite High Growth

2023-08-23 13:47:58 ET

Summary

- Woodward's sales in the aerospace industry have shown double-digit growth, driven by strong commercial aviation and aftermarket sales.

- The company's industrial sales also experienced significant growth due to increased demand in various sectors.

- Despite the positive performance, Woodward's stock is not considered attractive for investment, with limited upside potential in the coming years.

Before the pandemic hit the world, including the aerospace industry, the industry was going through a round of consolidation. That abruptly came to an end with one of the terminated mergers being the combination of Hexcel (HXL) and Woodward (WWD). Since then, Hexcel stock has gained 131% vs. 110%. Those might seem like impressive returns, and they are. But compared to pre-pandemic times both stocks are more or less flat, with Woodward's 6% gain being slightly better than Hexcel's 1.5% decline.

As the aerospace industry is rebuilding itself, it's interesting to assess the prospects of the industry names. I will be discussing the prospects of Woodward.

Woodward Doubles Earnings

{kind=link}

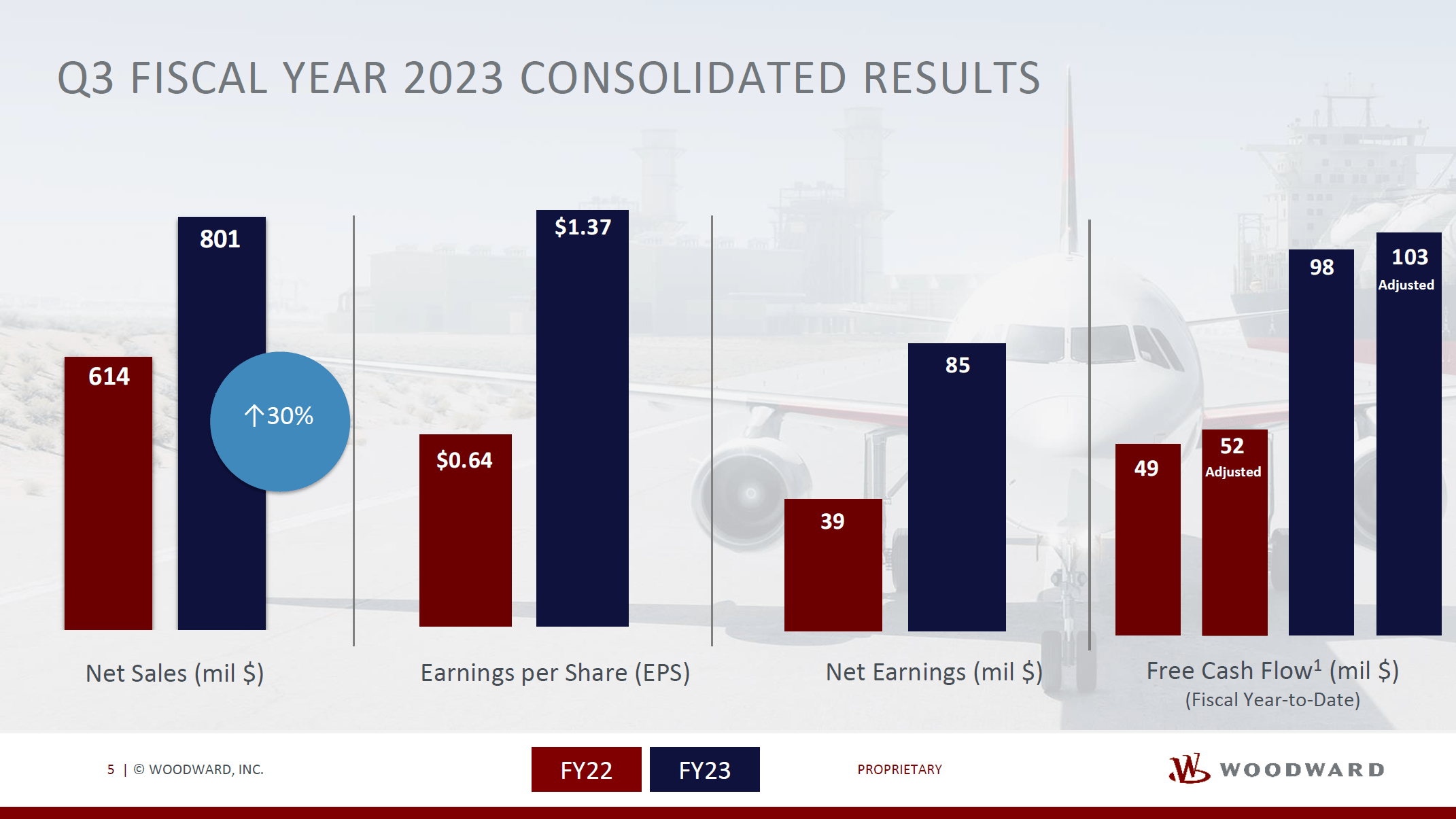

A look at the most recent results shows double-digit growth for Woodward sales. Total aerospace sales grew from $401.7 million to $480.5 million, indicating nearly 20% growth. That growth was carried by the commercial aviation sales where sales to the OEMs grew by 41% while aftermarket sales grew nearly 28.5%. Defense OEM sales declined by 12.3% due to lower guided weapons sales, but Defense OEM sales were up 17%.

The composition of the aerospace revenues already shows two elements I like. The first element is the mix between commercial aerospace and defense where commercial aerospace should normally see higher growth while defense provides stable revenues and in the current defense landscape also offers growth opportunities. The second element I like is the mix between OEM sales and aftermarket sales, which offer the possibility for aerospace companies to continue extracting value from delivered equipment.

Industrial sales grew from $212.6 million to $320.1 million or 50%. That high growth is driven by increased end market demand with high demand for back up power generation for data centers, marine market growth and support of natural gas infrastructure and transportation. On 30% higher sales, Woodward more than doubled its earnings to $85 million. Higher volumes coupled with better pricing, productivity and inflationary cost pass through helped Woodward to significantly increase its results, and overall as the business increases volumes, we see better cost amortization which adds to the margins.

What Is Behind The Revised 2023 Outlook?

{kind=link}

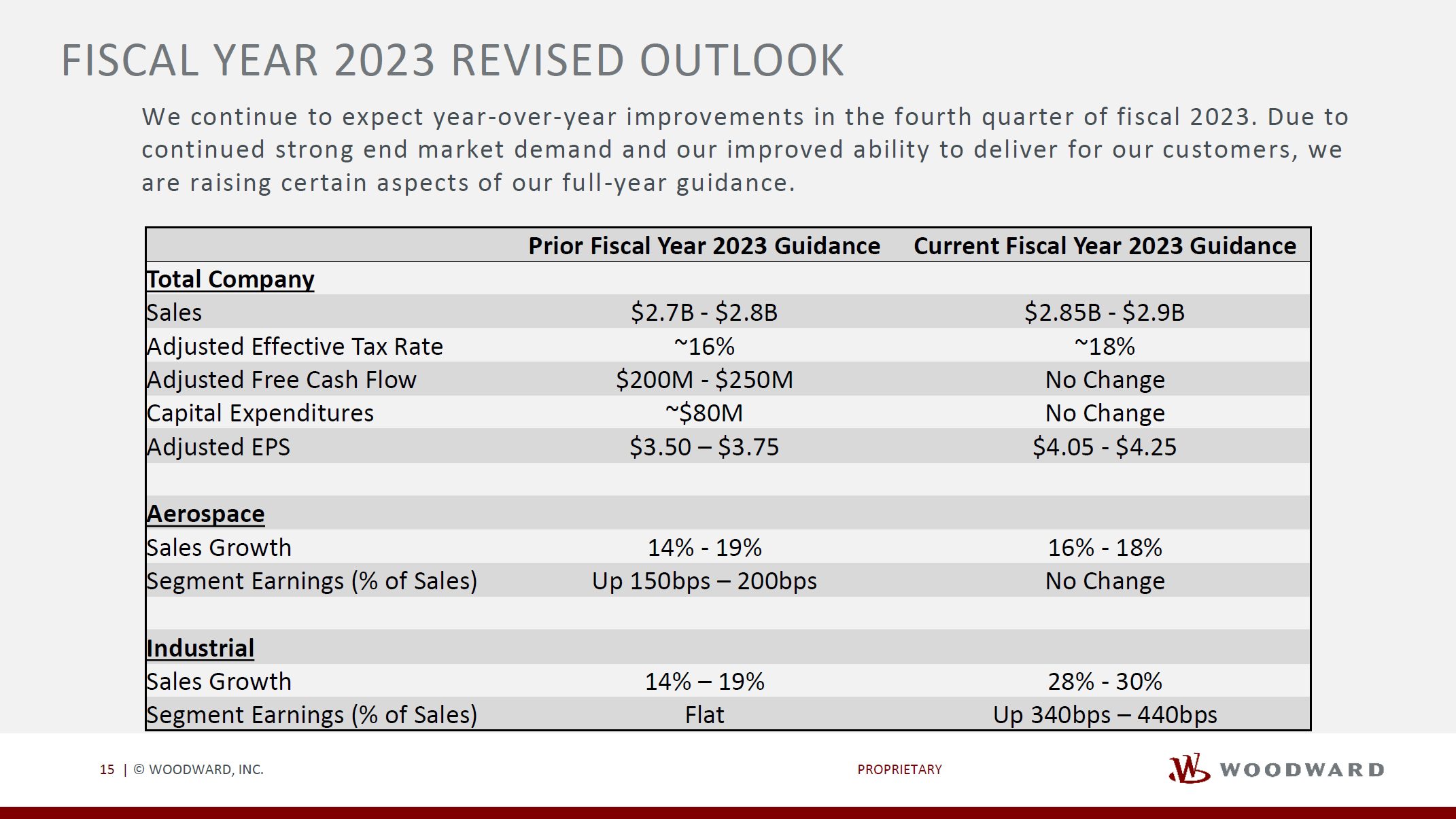

Woodward increased its guidance for the full year, and in some way, it's not much of a surprise. Woodward's financial year ends in September, so they have a lot of visibility in the final quarter of their financial year, but even with that in mind we see pretty big changes to guidance as compared to their previous guidance. So, why is that? Sales guidance has basically been increased with a narrowed range. Aerospace sales forecast growth has been increased 2 percentage points at the low end but decreased 1 percentage point on the high end. The big change that also significantly alters the adjusted EPS guidance is the Industrial guidance where strength seen in Q3 will somewhat taper, but the overall strength that Woodward cannot always count on such as increased natural gas truck production and inventory unwind to China will carry on in the fourth quarter and positively contribute to margin expansion.

Woodward Stock Price Forecast

Woodward stock looks interesting with the nice growth figures we have seen in the third quarter, but for the full year those growth figures are difficult to sustain and there has been some strength in Industrials that Woodward cannot always count on. With Woodward stock gaining 30% over the past 12 months, it's important to assess whether there's any upside to the stock left.

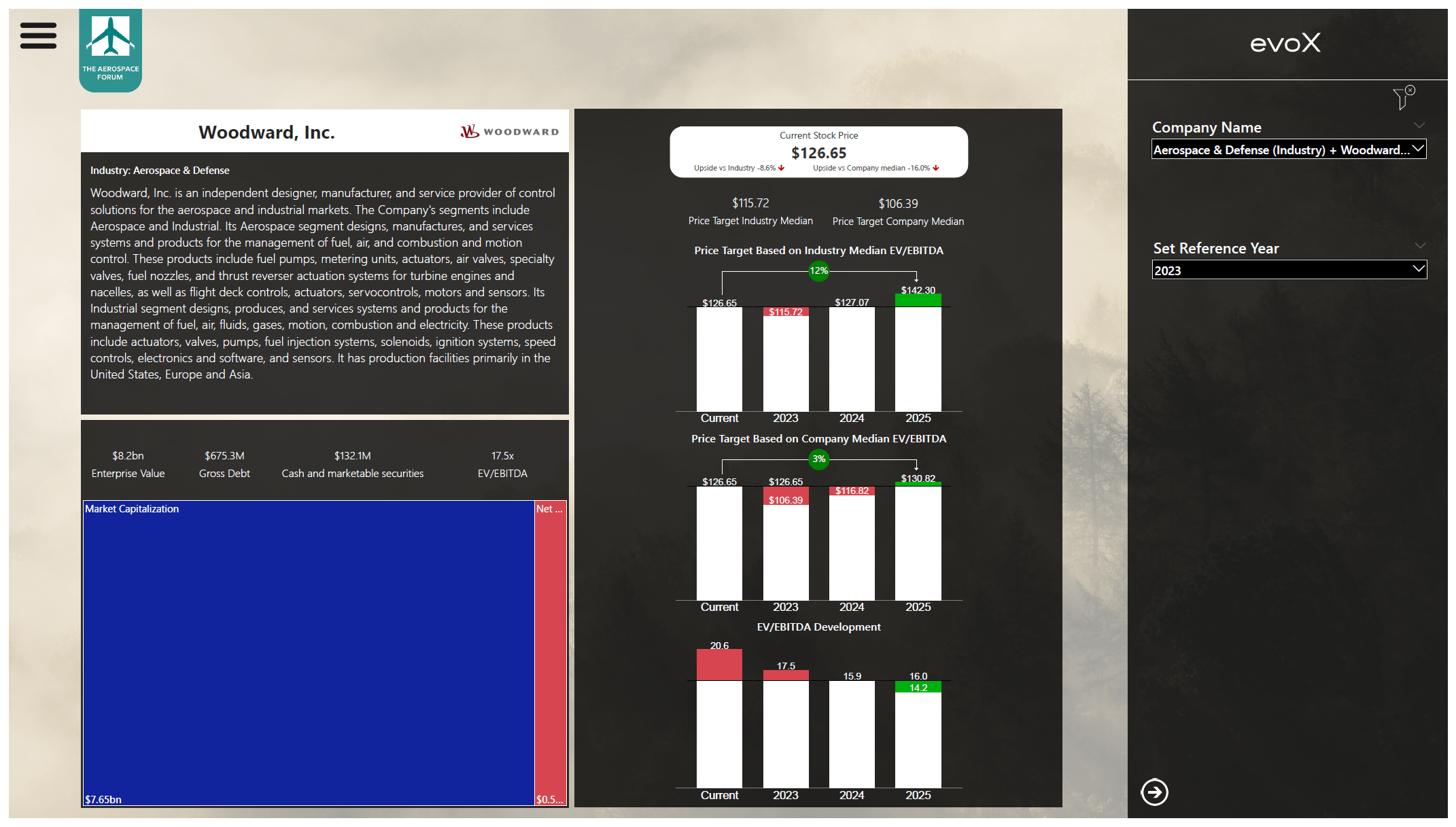

Stock price valuation for Woodward using evoX Financial Analytics (The Aerospace Forum)

{kind=link}

While I do like the division between commercial aerospace and defense as well as OEM sales and aftermarket, the conclusion I have to draw after analyzing the projected earnings for Woodward and the balance sheet is that Woodward is not valued attractively. Against the 2023 and 2024 the company offers no upside when valued in line with peers or against its median EV/EBITDA multiple. Against 2025 earnings, the upside is between 3% and 12% and that is simply not attractive. As a result, I'm assigning a Hold rating to Woodward stock.

Conclusion: Woodward, Nice Business But Little Upside

I do like Woodward's business as it has the diversification I'm looking for. However, with its 30% increase in stock price, there's no upside left until 2025 and the upside that's still remaining for 2025 itself is too small to appeal to me. As a result, I'm assigning a Hold rating to Woodward stock.

For further details see:

Woodward: Stay Away Despite High Growth