WW - WW International: A Case Of Potential Value Trap

2024-01-11 01:11:13 ET

Summary

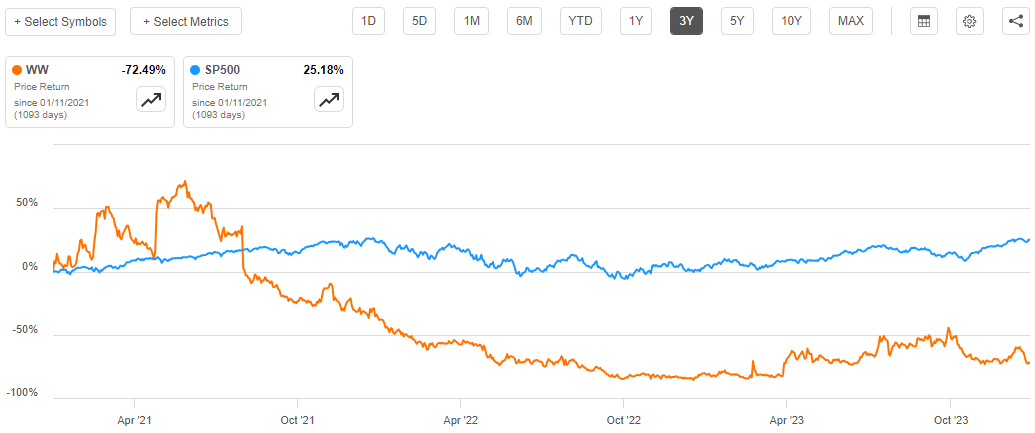

- WW International, Inc. has underperformed the S&P 500 by 98% over the past three years.

- The company's narrow business model focused on weight loss and weight management may limit its growth potential.

- WW has significant debt and poor financial performance, making it a risky investment choice.

Investment Thesis

WW International, Inc. ( WW ) is down about 73% over the last three years underperforming the S&P 500 by a margin of about 98%.

{kind=link}

At its current valuation, WW is trading at a discount to its sector median, which could be a case of undervaluation, presenting the stock as a good investment opportunity. However, I believe this valuation could be a potential value trap due to several reasons such as its significant debt burden, and inefficiency as demonstrated by its poor ROA, ROIC, and Asset utilization ratios.

Furthermore, the company’s revisions and growth metrics are far from impressive, which I believe further nullifies this stock as a good investment opportunity. To add on why I think WW isn’t a good investment opportunity is its narrow business model which primarily focuses on weight loss and weight management and lacks the diversity to appeal to a wider market beyond the weight management market segment.

I am alive to the fact that the company has embarked on restructuring plans , but I believe it will take time before they pay off and turn around the status quo and make this stock a good investment. Guided by this background, I recommend patience as the company implements its restructuring plans. I think a good entry point would be when the company substantially deleverages and improves its efficiency ratios. As I conclude, I reiterate that the current valuation isn’t a good entry point but a potential value trap.

Narrow Business Model

WW offers weight loss and weight management services. Its business model is based on three main sources of revenue:

- Digital Subscription : This segment includes the fees from members who attend interactive sessions led by trained coaches, where they receive guidance, support, and accountability. Members also have access to the WW app and website, which provide tools and resources for tracking their food intake, activity, and weight. This segment accounted for 63.7%% of the total revenue in 2022.

- Workshops + Digital: The segment includes the fees from members who only use the WW app and website, without attending the meetings. The app and website offer features such as personalized plans, recipes, and coaching, among other services. It accounted for 24.6% of the total revenue in 2022.

- Product Sales & Other: This segment includes the sales of branded products, such as food, cookbooks, kitchenware, and fitness devices. This segment accounted for 11.7% of the total revenue in 2022.

Market Screener

Looking at this business model, it is narrow in the sense that it focuses on weight loss and weight management as its core value proposition. This in my view may not appeal to a diverse customer base. Some of the challenges and limitations of the company's business model are:

- It faces intense competition from other weight loss and wellness companies, such as Nutrisystem ( NTRI ), and Medifast ( MED ), as well as from fitness apps, wearable devices, and online platforms that offer similar or alternative solutions.

- It relies heavily on its brand recognition and reputation, which may be affected by negative publicity, customer complaints, product recalls, or lawsuits.

- The company's revenue and profitability depend largely on the number of subscribers and meeting attendees, which may fluctuate due to seasonality, economic conditions, consumer preferences, and marketing effectiveness.

- Its innovation and differentiation may be limited by its focus on weight loss and weight management, which may not address the holistic needs and goals of its customers, such as mental health, emotional well-being, self-esteem, and body positivity.

In conclusion, the company’s business model is very narrow as it focuses on weight loss and weight management which lacks the diversity outlook to appeal to the holistic needs and goals of its customers and potential customers. In my opinion, this will hinder not only its capacity for innovation but also its capacity for growth and competitiveness. I believe WW has to deliberately expand its business model beyond weight loss and weight management to seize enormous growth opportunities.

WW Inefficiency

One way to measure the efficiency of a company is to assess its return on assets [ROA], return on invested capital [ROIC], and asset utilization ratios. These ratios indicate how well a company is using its assets to generate income and create value for its shareholders. With this background, let us evaluate how WW has performed based on these ratios.

The company has performed poorly in each of the three ratios. With a ROA of -5.31%, it implies that it is losing money on each dollar of assets it possesses. Further, it has a ROIC of -7.6%, which implies that the company is not using invested capital profitably and therefore it is eroding shareholder value. Its asset utilization is 0.885, which indicates that for every dollar of assets it utilizes, the business makes less than one dollar in revenue which is very low, and most concerning it is declining underscoring declining efficiency in asset utilization.

YCharts

In a nutshell, these ratios suggest that WW is inefficient in using its assets and capital to create value something I believe is not pleasant to investors and therefore I don’t think this stock is a good investment choice.

Financials: Significant Debt Burden

Looking at WW's financial statements, it is clear that, in addition to its poor financial performance, the company has a significant debt burden, making this stock a risky investment. Let me walk you through some of the highlights of its financials. First off, it has a total debt of $1.49 billion which is 1.45x its total assets of $1.03 billion. This means that the company has a negative net worth and a very high leverage ratio. With a negative $.5.1 million in operating cash flows TTM, and an interest expense of $93.7 million TTM, it clearly shows that the company cannot adequately cover its debt with its operating cash flows something which poses a financial risk to this company.

The company's balance sheet shows a significant amount of goodwill and intangible assets worth $697.6 million. These assets are subject to impairment tests, and if the company's future cash flows fall, it may be forced to write them down and incur a loss. In addition, WW's liquidity position is also weak, as it has only $107.5 million of cash and equivalents which can only cover its debt by about 0.07x. The company's current ratio, which measures its ability to meet its short-term obligations, is 1.13, which is below the industry average of about 1.8.

In addition to its debt burden, its financial performance has been awful with revenues declining and margins shrinking. Its revenue has dropped from $1.5 billion in 2018 to $1.04 billion in 2022 and its net margin shrank from 14.78% in 2018 to -24.15% in 2022. This represents a revenue drop of about 30.57% and a net margin decline of about 264.28%.

Market Screener

Based on this analysis, WW has a significant debt burden and a weak balance sheet, which pose serious risks to its financial stability and growth prospects. The company needs to improve its revenue performance, reduce its costs to improve profitability, and generate more cash flow to service its debt and invest in its business. Otherwise, it may face liquidity problems, credit rating downgrades, or even bankruptcy in the worst-case scenario.

Valuation

Based on relative valuation metrics, WW appears to be a bargain stock at the moment. According to Yahoo Finance, WW has a FWD PE of 15.2 and a PS ratio of 0.5. I will use the FWD PE because WW has no trailing PE ratio due to its poor profitability. Its FWD PE compared to the sector median of 16.95 shows that this stock is trading at about a 10% discount indicating that it is undervalued based on its future earnings. Additionally, its TTM PS ratio compared to the sector median of 0.9 shows that the stock is trading at a discount of about 40% based on its sales. Based on these valuation multiples, WW is undervalued. While this may appear to be an attractive entry point for many investors, I believe it is a potential value trap due to the company's narrow business model, weak balance sheet, and poor financial performance.

Conclusion

In conclusion, based on this analysis, WW appears to be undervalued based on relative valuation metrics something which could appear as a good entry point. However, to me, this is a potential value trap given the company’s weak balance sheet and poor financial performance as well as its narrow business model which primarily focuses on weight loss and weight management. Although the company has embarked on restructuring plans aimed at achieving financial efficiency and resource optimization, I can only recommend patience until they pay off through improved revenue performance, profitability, and substantial debt reduction until then hold WW, and if the restructuring plans fail to pay off and the current financial woes continue, a sell decision should be on your card in the medium and long-term horizon.

For further details see:

WW International: A Case Of Potential Value Trap