WYNN - Wynn Resorts: A Long Range Feast Or Famine Stock Cheap At $86

2023-11-27 04:40:46 ET

Summary

- Last July, our Buy guidance at $105 proved wrong because we saw rapid recovery ahead, but the market did not.

- Wynn's trading history has wide swings due to its historical pattern of punching above its weight.

- Superior properties and upscale customer property confer pricing power not all peers can command.

Premise

The long-term trading pattern of the shares of Wynn Resorts Ltd. ( WYNN ) has these repeating characteristics:

When bullish sentiment in the sector is high, Wynn always trades well above peers. It goes back at least 25 years. It springs from two sources. One, the reputation of former CEO, Steve Wynn, who in many ways reinvented the casino business.

Two, because on any apples-to-apples comparison of its casino win, it outperformed peers on average slot win per day, average table game win per day, and best revenue performer per square foot. Wynn properties were never the largest in their markets but they always punched above their weight. Their aim was at an upscale demo where pure scale counted for less than average spend per customer.

And just as the market has always rewarded Wynn shares a vastly higher valuation than peers on the upside, when it swoons, it scrapes a relative bottom still above peers. The wide price swings come from a long-standing perception that always anticipates a higher performance than peers given the operating history. When those expectations are not met, for one reason or another, Mr. Market takes his profit and runs for the hills bringing the stock into the bargain basement. Yet even down there, takers are skeptical until the next earnings release or a macro catalyst spurs the sector.

{kind=link}

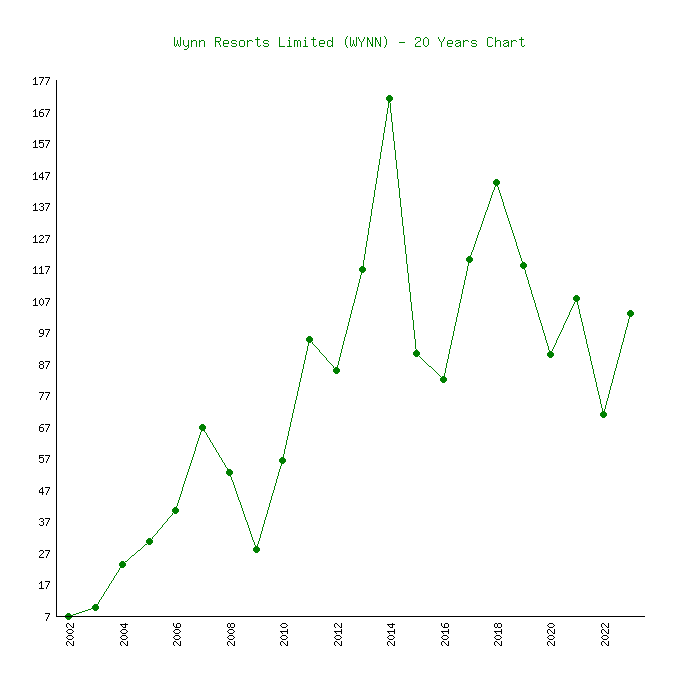

Above: Twenty-year trading pattern shows wide swings are expected.

Wynn's resignation in February of 2018 over allegations of sexual misconduct with female employees triggered an expected dip. But soon after when the successor management settled a long lingering lawsuit, it recovered. By March, Asian gaming giant Galaxy Entertainment Group Ltd. (0027HK) bought a 5.2m tranche of newly issued Wynn shares valued then at $1b. The two catalysts, plus an upward performance trend, moved the stock by March to $196. The prism through which investors began seeing the growth of an upscale gambler base expanding at the Macau Wynn Palace became rosier (Wynn Palace opened in 2016).

For context, we looked at a Trefis* analysis of Wynn's share price, its projection, and price at writing as of the present against peers Caesars (CZR), Las Vegas Sands (LVS), and MGM Grand (MGM).

| Ticker |

| Trefis valuation* |

| + (-) |

| At market |

| CZR |

| $44 |

| -3% |

| $44.55 |

| LVS |

| 56 |

| 13% |

| 49.44 |

| MGM |

| 50 |

| 27% |

| 39.88 |

| WYNN |

| 109 |

| 26% |

| 86.86 |

*Trefis research of Boston follows trends and makes forecasts of stock prices in forward positions against peers, the S&P, and large-cap companies.

You can see from the above that the premium ascribed to the stock continues to support a higher valuation than peers.

Alpha Spread DCF analysis puts WYNN at a fully valued $87.59. Its best case rises to $197, its worst case declines to $44.49. But its analysis sees revenue rising from $7.43b in baseline 2019 to $12.7b by 2028. Net income in the same time frame rises from $512m to $1.3b.

We have calculated an ROE for the next three years post-Covid to produce a really strong 147% sprung from Las Vegas, Macau, and Boston forward revenue growth.

Despite impressive 3Q23 results, Wynn shares dipped 6% and further went down on November 10th when settlement news of the Vegas strike broke.

Last February, the stock traded at $115, then by summer at $108 developing a bull fatigue I have seen for decades on these shares.

However, looking at the trading from a long-term perspective, we continue to believe that the pattern of wide swings off its accustomed premium and lows such as that of this post, signal a gathering of positive momentum. As each month the gaming win and arrival numbers support an advance to the baseline 2019 pre-Covid revenue total of $37.7b.

We are looking for 2023 earnings to reach near or at $4.00. We can also see for EPS of $7.20 for 2024 based on Wynn achieving a 16.4% share of the Macau market and holding steady in Vegas. The Wynn EPS multiple has always been a poor harbinger of forward results. That's because its sustaining base trade is so high above sector peers. If you take issue with that idea, you should not buy this stock. That's why we don't forecast EPS here.

We understand how Mr. Market may conclude that an $86 price cannot be a bargain relative both to peers and some large-cap stocks in the consumer discretionary sector. But we advance our premise by looking at a historical trading pattern where we believe there are investors who track this as well. Investors who have followed the stock for decades eye the Wynn shares at certain sold-down levels. They have confidence in the business model and move to positive sentiment. Then the stock begins to take off again.

In some ways, WYNN is a unicorn. Not in the classic tech sense of course. However, its business model is sufficiently apart from many peers that has been distinctive over the years.

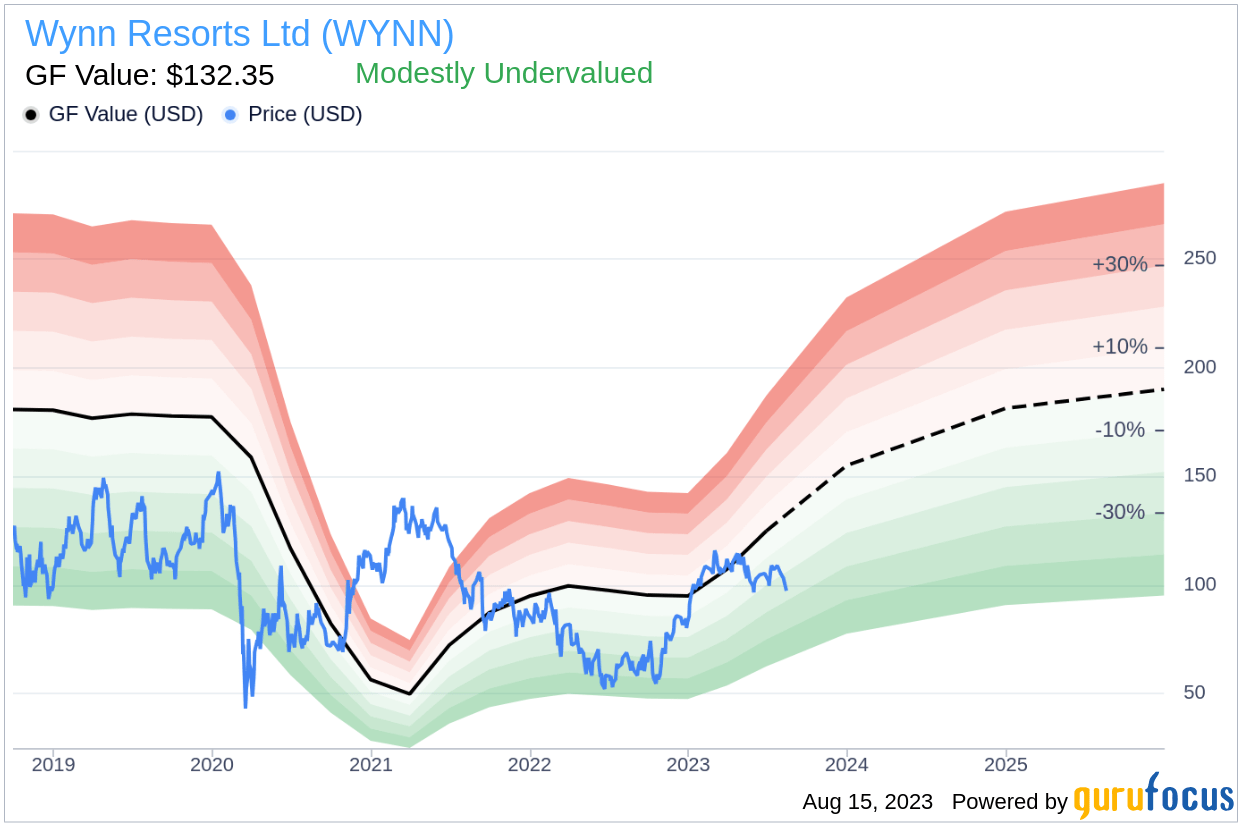

{kind=link}

Above: We expect the stock to be in the early stages of entry on a long bull run from here in line with markets in Macau, Las Vegas, and Boston.

Up close with Wynn for decades

I have known the company since the 1980s when I competed with Wynn for the upper middle and high-end play. I got to know many of their key executives as industry colleagues and friends. Peers tend to embrace new markets by building big with the confidence that the business will grow into its size as the total market expands. Wynn always builds smaller under the thesis that their opulent properties will command an average customer spend for gaming, dining, rooms, and other amenities well above the competitive fray. Then as their revenue base grows, they add capacity. Their supply and demand reckoning is this: Always establish unmet demand for their product first, then fill it. That imparts a cache they have long exploited as giving their properties an aura of specialness that customers can validate when they arrive.

Our call here

Our PT by the end of 1Q24 is $120, entirely linked to what we see in positive performance in its three markets. But mostly because we think the stock has cycled low on perceived headwinds that are now past it.

We already see early signs of the typical early upside move on Wynn shares emanating past the Vegas strike settlement headwind and moving toward a 4Q23 result we like. The $1.00 Nov 17th dividend is a small but meaningful indicator of a confidence level of continuing growth in FCF related to simultaneous revenue and EBITDA gains in Vegas, Macau, and Boston.

We, along with many analysts, must take the L on our last SA post (July 2023) when the stock traded at $105 and I guided higher past $125. Where we were wrong was in appraising the velocity of Macau gaming recovery which at that date was moving at what appeared to be beating official projections. We also saw the Vegas post-Covid surge beginning to fade but thought Mr. Market's sentiment would overcome that. Overall, the speed of recovery we saw proved unimpressive to investors, and profit-taking took down the valuation.

We were wrong.

What's changed?

The strike has been settled and the cost increases we expect will have less of an impact on margins due to revenue spikes gaining velocity. The rapid pace of Macau recovery has not lost steam, nor has the post-Covid surge in Vegas. The stock in our view has been oversold since last July and is clear of any pending headwinds we can think of outside of black swans.

Las Vegas will absorb the arrival of the new Fontainebleau next month as it has for decades absorbed new properties. The pattern in short term must see trial, some poaching of shares, novelty visits wane, shares of competitors return to normal levels, and new property absorbed by organic growth of the market assuming no major macro disruptions.

Risks

Entirely macro. Fed action ahead could crush the market - but that's in the guesswork we find in guru pontifications and as usual investors are free to get antsy or disregard them. Then there is recession risk. The most severe one of 2007-2009 took about 10% to 13% off national casino wins. Whether it's a soft or hard landing again lies in the precincts of punditry inside the bulge banks' economic departments.

The endgame here is this: Right now relative to valuation and long-established price history and performance, Wynn shares look attractive as a bargain even at $86.

For further details see:

Wynn Resorts: A Long Range Feast Or Famine Stock, Cheap At $86