WYNN - Wynn Resorts: Continuing To Avoid

2023-05-08 21:49:37 ET

Summary

- The company is about to release earnings, and I thought I'd review the name yet again. I think the risk is too great at current levels.

- The market is paying as much for $1 of typical earnings as it did in 2014 when this was a much different (better) business.

- I'll admit that the company is definitely turning a corner, but the market has gotten ahead of itself in my view.

A friend of mine read the article I wrote about Wynn Resorts Limited ( WYNN ) back in January, and his response was "granny Doyle strikes again!" referencing the fact that once again, I talked myself out of a nicely profitable trade by recommending people avoid this name five months ago. Since I wrote that, the shares are up about 14% against a gain of 5.4% for the S&P 500. I thought I'd review the name again to see if the shares "still have legs ", or if this is yet another example of that "the market giveth, the market taketh away" phenomenon that we're all so used to. The company has released earnings recently, and it's about to release earnings again , so I thought I'd review those, and thought I'd look at the valuation.

As my regular readers know, I'm downright obsessed with trying to make your lives as interesting and pleasant as possible. I know that some of my writing can be "a bit much", and for that reason, I find it worthwhile to offer a thesis statement at the beginning of each of my articles, in order to give you the opportunity to get in, get a flavour of what I'm writing, so you can get out again before my stuff becomes too tiresome. You're welcome. I'm of the view that Wynn is certainly turning a corner, and I think there's a reasonably good chance they may reintroduce the dividend at some future date in spite of the fact that cash from operations has historically barely covered investing activities. Given that, I'd be happy to buy WYNN stock at the right price. The problem for me remains the valuation. If we exclude the spike in valuations caused by the pandemic, the shares are more richly priced now than they were way back in 2014, when the company had about 39% less debt on the balance sheet. Additionally, when the shares last reached current valuations, they went on to underperform. Given that an investor can receive a respectable return on a risk free investment at the moment, we're no longer in the world of "TINA." If you're interested in preserving capital, I think it would be prudent to avoid these shares at current prices. This ends my thesis statement. If you read on from here, that's on you. I don't want to read any comments below about how pompous I sound, or the fact that I spell words like "flavour" properly.

Financial Snapshot

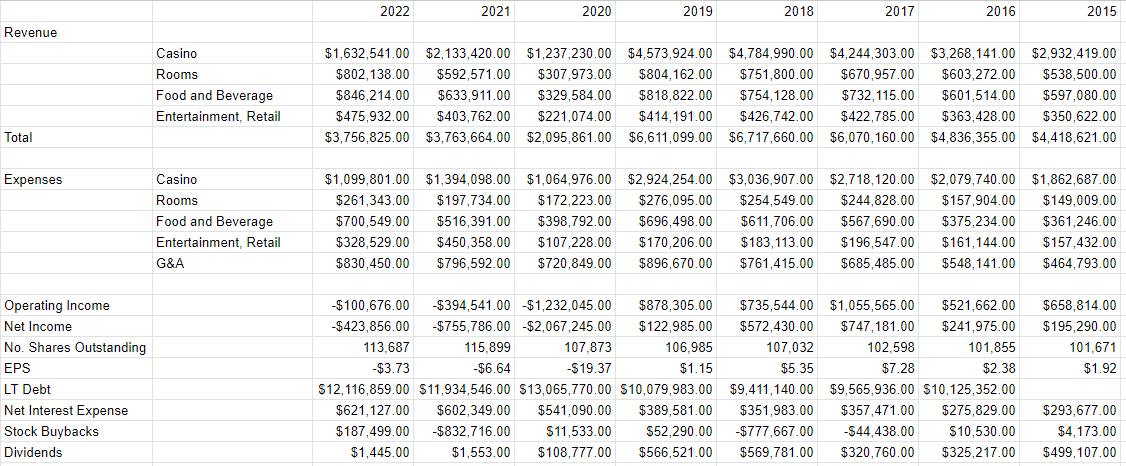

When we last reviewed this name, I characterised the most recent financial performance as "mixed to bad." That may have been a bit harsh. Although I'm not impressed by the most recent financial performance, it can be seen as reasonably good, depending on your frame of reference. For instance, the company improved net income dramatically in 2022 when compared to 2021. Specifically, operating, and net income improved by $293.9 million, and $332 million, respectively. This is because the company did a great job of holding the line on casino expenses, which are its largest expense category by a wide margin. The problem is that 2021 wasn't exactly what we could characterise as a "banner year" for the company, so any comparisons to that period should be taken with a boulder sized grain of salt in my estimation.

When we compare the most recent period to the pre-pandemic era, we see that things have improved nicely from the slough of despond days of 2020, but we're still far below 2019's levels. For example, revenue and net income in 2022 were lower than 2019 by about $2.85 billion and $547 million, respectively. I wrote previously that this company has broken from its profitable past. While I will acknowledge the heroic efforts of improving profitability, we're still not close to pre-pandemic levels of profitability, and that should be reflected in the share price in my view.

Dividend Potential?

As riveting as discussions of financial history are, I think the dividend, and its potential reinstatement is more interesting to investors. Dividends provide much more predictable sources of income, and dividends are supportive of the stock price. If Wynn can manage to reintroduce the dividend, I think the stock price would benefit. Because every fibre of my being is dedicated to making your lives as interesting as possible, I therefore thought I'd spend some time writing about the potential future of a dividend.

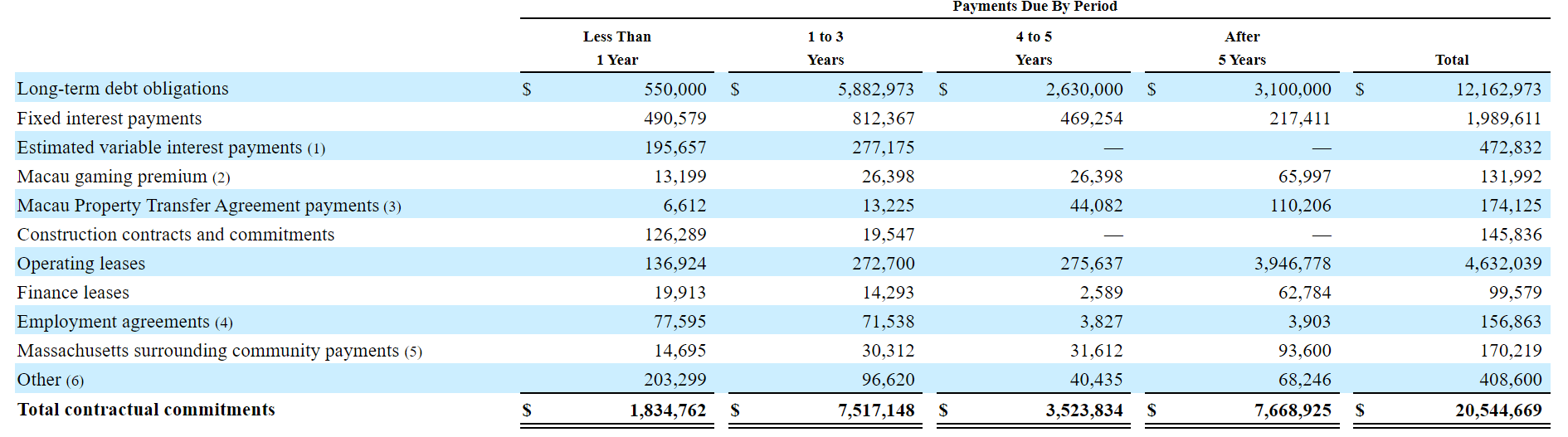

Although I love accrual accounting as much as it's possible to love such a thing, when it comes to potential future dividends, I want to focus on cash. Specifically, I want to review the sources and uses of cash to see how much room there is for dividend increases, from 0 in this case. Starting with the uses, I've plucked the following from page 50 on the latest 10-K for your reading pleasure. It suggests that this year, the company is "on the hook" for about $1.834 billion in obligations, and is on the hook for about $2.5 billion in each of the following three years.

Wynn Resorts Ltd. Contractual Obligations (Wynn Resorts 2022 10-K)

{kind=link}

Against these obligations, the company currently has about $3.65 billion cash on the balance sheet.

When it comes to comparing "typical" sources and uses of cash, I think we need to eliminate the years 2020 and 2021 from our analysis in this case for very obvious reasons. Thus, when I review the "previous" three years of cash from operations and cash for investing, I'm going to be writing about the period 2022, 2019, and 2018. When we compare these time periods, we see that the company earned an average of $597 million cash from operations, and invested an average of $1.213 billion into the business, so there's a cash shortfall.

For those who insist that we're heading back to the pre pandemic era, I would point out that even prior to the pandemic era, we see that in a "typical" year, this company generated an average of $1.25 billion CFO and spent an average of $1 billion on the business annually. Additionally, that average CFO figure was elevated massively by an atypically large customer deposit of $456 million in 2017. However we slice it, I think the point is made. This is a capital intensive business, and cash from operations typically barely covers investments.

That written, I think the cash hoard on the balance sheet is sufficiently large to raise the hope that a dividend will be reintroduced here. Given that, I'd be happy to buy this stock. Given that we haven't yet returned to prior levels of profitability, I'd not be willing to pay much of a premium for the stock.

{kind=link}

The Stock

If you've been following me for any length of time, you know that my insistence on not overpaying for a given stock has caused me to miss out on profitable trades, like this one. My view is that I'd rather miss out on opportunities than risk overpaying for a stream of future cash flows, because I'm of the view that the more you pay for a given investment, the lower will be the subsequent returns. This is one of the iron, immutable laws of finance, and the market sometimes forgets it.

Additionally, my regulars know that I consider the business to be different from the stock, and we need to analyse each separately. For example, every business buys a number of inputs like food, and hotel furnishings, for instance, and turns them into a final product or service. The stock, on the other hand, is an ownership stake in the business that gets traded around in a market that aggregates the crowd's rapidly changing views about the future health of the business, future demand for " Unforgettable Entertainment", and so on. The stock also moves around because it gets taken along for the ride when the crowd changes its views about "the market" in general. A reasonable sounding, if counterfactual, argument can be made to suggest that some portion of Wynn's gain since January is as a result of generally ebullient markets over the same time period. In any case, the stock is affected by a host of variables that may be only peripherally related to the health of the business, and that can be frustrating.

This stock price volatility driven by all these factors is troublesome, but it's a potential source of profit because these price movements have the potential to create a disconnect between market expectations and subsequent reality. In my experience, this is the only way to generate profits trading stocks: By determining the crowd's expectations about a given company's performance, spotting discrepancies between those assumptions and stock price, and placing a trade accordingly. I've also found it's the case that investors do better/less badly when they buy shares that are relatively cheap, because cheap shares correlate with low expectations. Cheap shares are insulated from the buffeting that more expensive shares are hit by.

As my regulars know, I measure the relative cheapness of a stock in a few ways, ranging from the simple to the more complex. For example, I like to look at the ratio of price to some measure of economic value, like earnings, sales, free cash, and the like. I like to see a company trading at a discount to both the overall market, and to its own history. I decided to avoid Wynn back in January because the market was paying $2.84 for $1 of sales for this company. If we strip out the spike in valuations caused by the pandemic, this was very near a multi-year high, in spite of the fact that this was not close to the company it was in 2014. Fast forward to the present, and things look worse, given that the shares are about 19% more expensive than they were five months ago, per the following:

As I wrote above, we haven't seen valuations like this since 2014, when the company had about 39% less long term debt than it has today, for instance. Additionally, while I don't think history repeats, I think it has a tendency to rhyme. When the shares last hit the current valuation, they went on to underperform.

My regulars know that I think ratios can be instructive, but I also want to try to work out what the market is "thinking" about a given investment. If you read my stuff regularly, you know that the way I do this is by turning to the work of Professor Stephen Penman and his book "Accounting for Value" for this. In this book, Penman walks investors through how they can apply some pretty basic math to a standard finance formula in order to work out what the market is "thinking" about a given company's future growth. This involves isolating the "g" (growth) variable in this formula. In case you find Penman's writing a bit opaque, you might want to try "Expectations Investing" by Mauboussin and Rappaport. These two also have introduced the idea of using the stock price itself as a source of information, and we can infer what the market is currently "expecting" about the future. Applying this approach to Wynn Resorts at the moment suggests the market is assuming that this company will grow earnings at a rate of ~6.4% in perpetuity. I consider that to be a pretty optimistic forecast and for that reason, I'm inclined to avoid the shares.

For further details see:

Wynn Resorts: Continuing To Avoid