WYNN - Wynn Resorts: Labored Recovery In Macau Presents Buying Opportunity

2023-12-15 04:16:29 ET

Summary

- Wynn Resorts stock has struggled a bit these past six months, giving up most of its gains from earlier in the year.

- The protracted recovery in the Macau gaming scene may be to blame, with Wynn sporting both more geographic exposure and a weaker short-term market position versus peers like MGM.

- Even so, the gaming market there continues its recovery-driven growth, and Wynn's earnings are inching back toward pre-COVID marks.

- These shares look cheap based on pre-COVID multiples and the reasonable expectation of earnings growth next year.

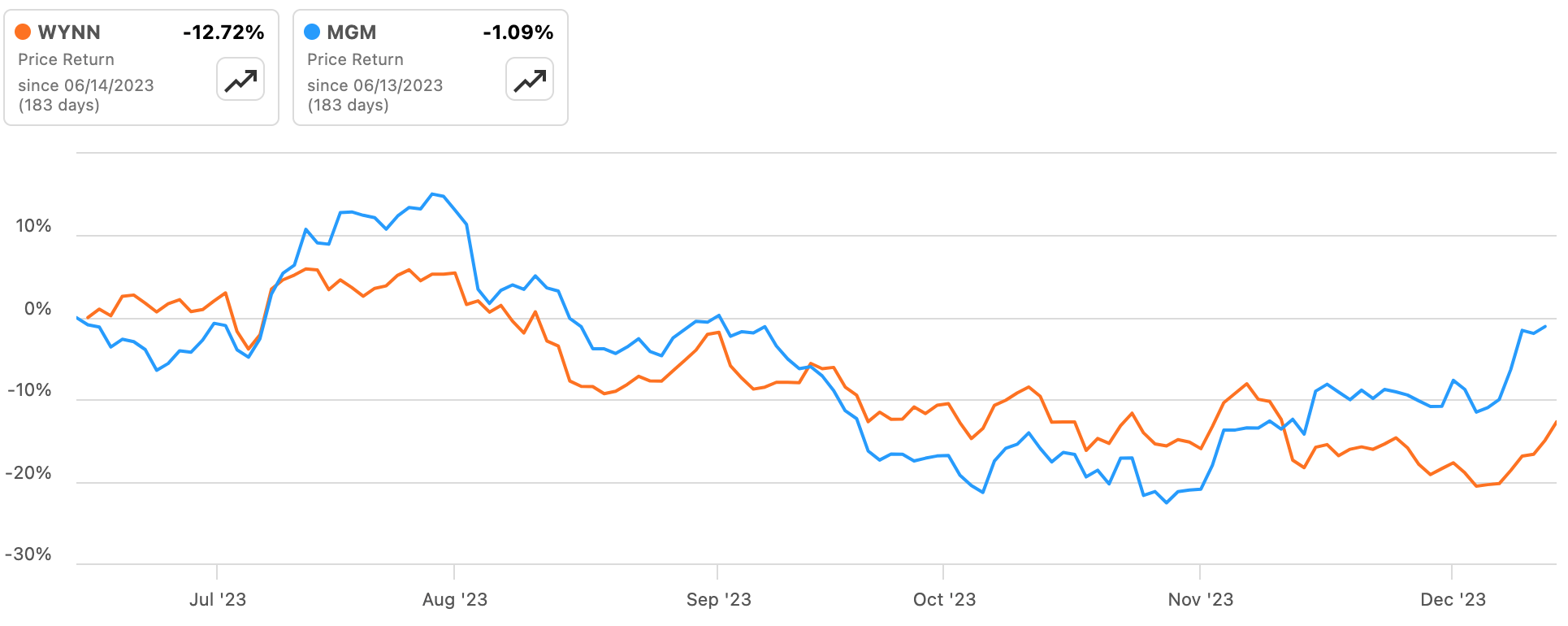

In contrast to the first half, the latter six months haven't been too kind to Wynn Resorts (WYNN) shareholders. Wynn stock has fallen around 13% in that time, notably underperforming recently covered peer MGM (MGM) amid the protracted recovery in the Macau gaming scene. While Wynn's business is perhaps taking a little longer to get back on its feet than previously hoped, a recovery delayed is better than no recovery at all, and investors should consider buying the dip here.

{kind=link}

Wynn operates integrated resorts in the United States and Macau. In the States, the company operates Wynn Las Vegas, Encore at Wynn Las Vegas and Encore Boston Harbor. In Macau, it operates Wynn Palace and Wynn Macau via majority ownership of Wynn Macau, Limited (WYNMF)(WYNMY). The labored recovery in Macau has skewed Wynn's business mix back toward its domestic properties, so 2019 marks are probably a better guide as to the company's underlying geographic mix. On that basis, operations in Macau accounted for around 75% of total adjusted property EBITDAR.

Although there is still a few more trading sessions to go in 2023, at this point I think it is quite safe to say it has been a tale of two halves for Wynn's stock. The shares did well in the first half, gaining around 20% or so, as COVID-19 restrictions were eased and then lifted fully early in the year in Greater China. They have then drifted lower as the pace of the recovery has perhaps fallen short of early expectations.

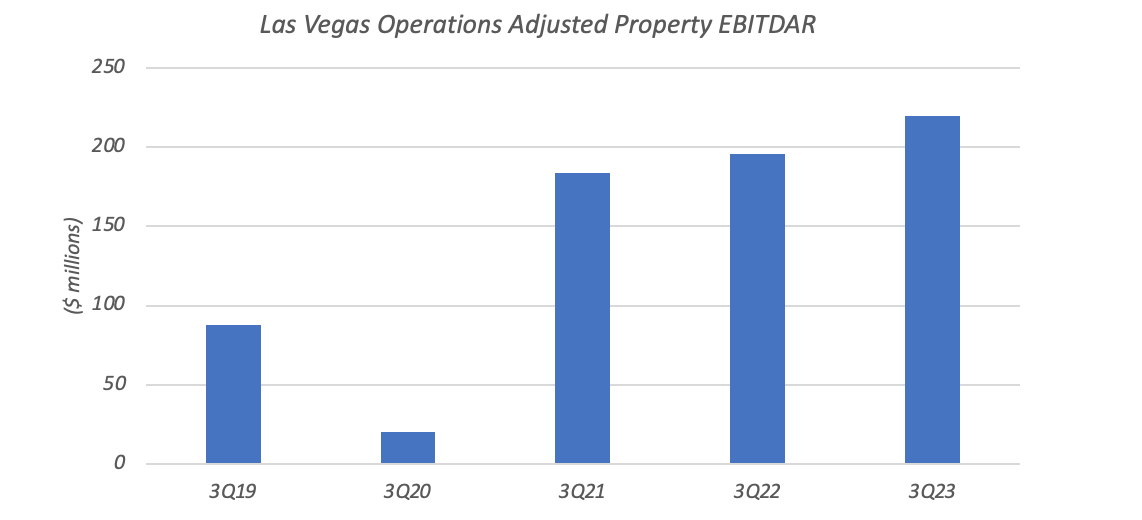

Before going on to Macau, a quick word on domestic operations: business is booming. Las Vegas operating revenues are way ahead of pre-COVID marks in all lines - that is, casino, food & beverage, hotel rooms and entertainment/retail. Hotel occupancy is still solid at 90%, but with average daily rate that is around 50% higher than pre-COVID levels. These types of businesses have a lot of inbuilt operating leverage due to the nature of their cost base. As a result, swings in earnings have been even greater. Domestic EBITDAR (i.e. Vegas Operations plus Encore Boston Harbor) has already topped $850 million year-to-date, comfortably ahead of last year. In terms of pre-COVID comps, the Encore Boston Harbor hasn't been open long enough to make that comparison, but no matter; if we restrict things to Wynn's Las Vegas operations then it is the same story: revenue and earnings are at record highs.

Source: Wynn Resorts Quarterly Results Releases

{kind=link}

There are always risks of a downturn of course, but for now things continue to look good in terms of Q4 and 2024 according to management:

Looking ahead, we have a strong pipeline of forward group demand, very healthy gaming market share, and a robust programing calendar with F1 and Super Bowl just ahead of us. And while it's certainly is an increasingly complex world out there between inflation, rates, geopolitics, things continue to feel pretty good around here.

Craig Billings, CEO Wynn Resorts, Q3 2023 Earnings Call

Macau is where the picture has been a little bit more mixed. As mentioned in the piece on MGM, the overall gaming market in Macau remains depressed versus 2019 levels despite the lifting of COVID restrictions. Market-wide gross gaming revenue was around 70% of 2019 levels in Q3. Similarly, visitor arrivals clocked in at 8.2 million last quarter, around 83% of the same-period 2019 number. Despite this, MGM's Macau EBITDAR was still 23% higher than in 2019. Casino revenues, rooms revenues, food & beverage sales etc - all clocked in higher than pre-COVID marks, notwithstanding the state of the wider Macau market.

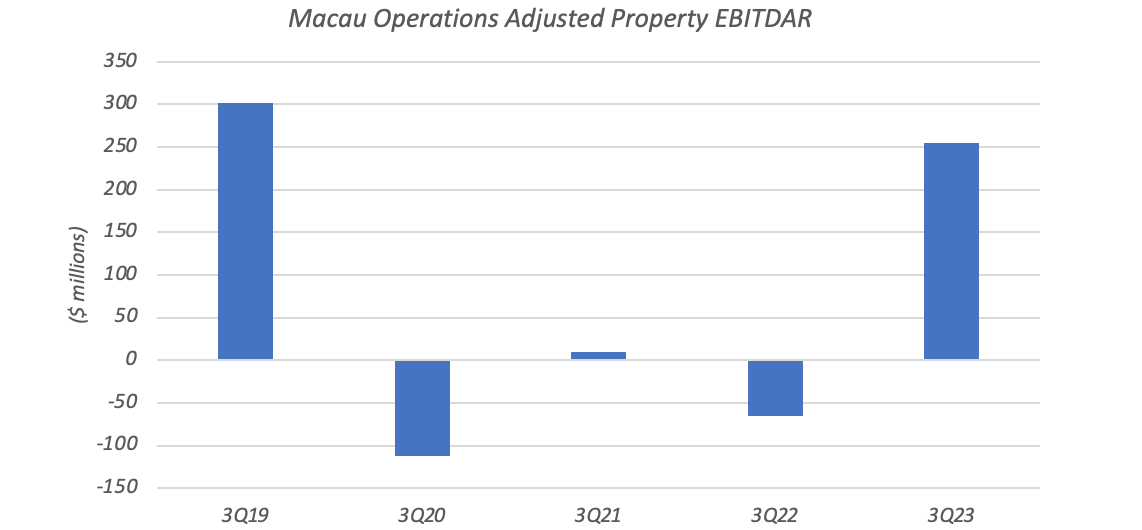

Wynn is struggling a bit more to hit its pre-COVID marks. Macau Operations EBITDAR was $254 million in Q3, which was still only around 85% of its same-period 2019 level. Now, the non-gaming side of revenue is actually doing okay - the sum of room, food & beverage and entertainment/retail sales is a bit ahead of 2019 taking both properties combined. Gaming is where the weakness is. Total casino revenue across its two Macau properties was just under $650 million in Q3, around 30% below 2019 levels. One of the reasons for the underperformance versus MGM is that Wynn's pre-COVID gaming mix skewed more heavily toward high rollers. That part of the gaming industry has not recovered to the same degree as the mass market segment. This is why MGM has gained around six points of market share in that time, coming at the expense of players like Wynn.

Source: Wynn Resorts Quarterly Results Releases

{kind=link}

While that continues to weighing on the business here, the trend in its Macau segment is still improving. Q3 Macau Operations EBITDAR was 85% of the 2019 figure as mentioned above. In Q2 it was 70% and in Q1 it was 40%. Indeed, Wynn Palace EBITDAR has already recovered to 2019 levels, leaving Wynn Macau as the laggard. Furthermore, gross gaming revenue should continue its recovery over the coming quarters. 2024 gross gaming revenue is seen landing in the region of $27 billion according to the Macau government, which would map to circa high-teens year-on-year growth based on the $18.4 billion in GGR posted through October . A share of that would naturally percolate through to Wynn's casino revenue line. Because of the fixed cost leverage in its business, plus the importance of Macau to overall company financials, group-wide property EBITDAR would register solid growth next year as a result.

Pre-COVID, Wynn averaged around $1.9 billion in annual property-level EBITDAR across 2018-2019. It generated around $1.5 billion through the first nine months of 2023, including $530 million in Q3. Next year it should comfortably post over $2 billion, and I'm looking for closer to $2.5 billion to be a bit more precise.

{kind=link}

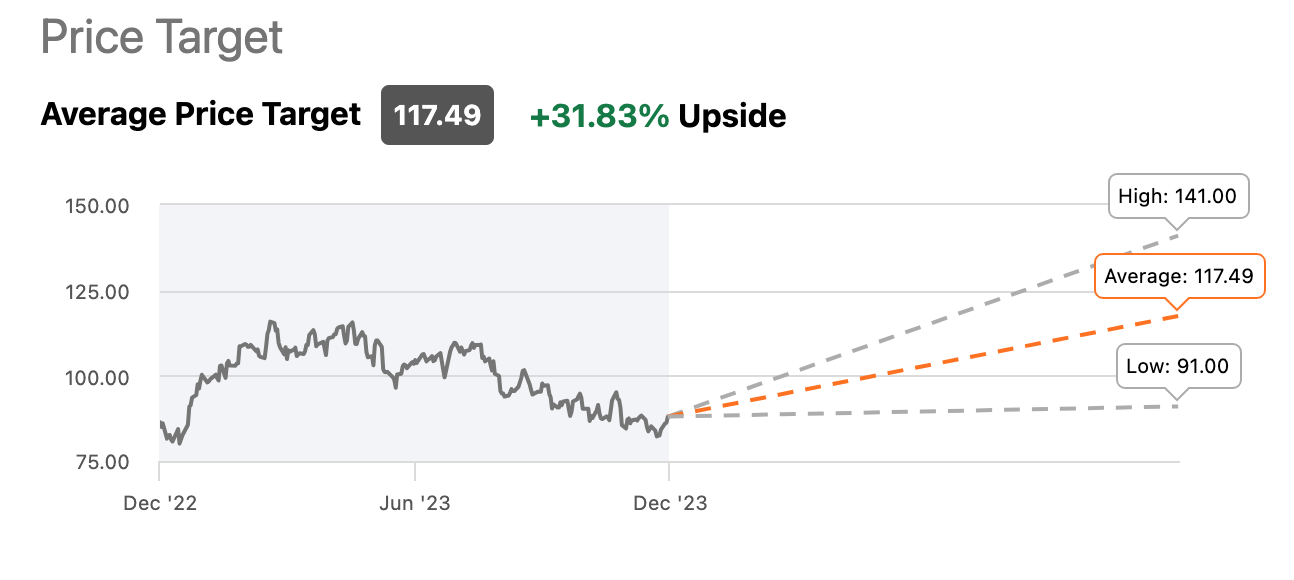

Before COVID, WYNN traded for around 12x EBITDA. Even a lower 10x multiple would get us to a circa $115-120 price target after backing out net debt (~$9.75 billion). That is roughly where Street analysts land as per the graphic above from Seeking Alpha. While there are obviously risks to consider here - Wynn is highly cyclical and sensitive to an economic downturn - the implied 30%-plus upside from the current $90 stock price looks worth it to me. Buy.

For further details see:

Wynn Resorts: Labored Recovery In Macau Presents Buying Opportunity