WYNN - Wynn Resorts Reports Strong Q3 2023 Results: Initiating A Buy

2023-11-10 02:20:55 ET

Summary

- Wynn Resorts reported strong Q3 2023 results which beat analyst expectations.

- Despite the positive earnings surprise, WYNN shares are trading lower in after-hours trading which presents a buying opportunity.

- The Company's UAE Wynn Al Marjan Island represents a significant growth opportunity over the long-term.

- Wynn Resorts is trading at a market multiple but has better than market long-term growth potential.

- I am initiating WYNN with a buy rating.

Wynn Resorts ( WYNN ) reported strong Q3 2023 results that topped analyst estimates. Additionally the company announced that it repurchased 596,948 shares of common stock during the quarter at an average price of $94.11 per share.

Given the strong earnings beat, I would have expected WYNN shares to move sharply higher. However, as of this writing WYNN shares are trading lower by ~5.5% in the after hours trading session. I believe current levels represent an attractive buying opportunity for shares of WYNN.

Q3 2023 Results

WYNN reported Non-GAAP EPS of $0.99 which beat estimates by $0.19. Comparably, for the same period a year ago WYNN reported a Non-GAAP Loss per share of $1.20. Revenue came in at $1.67 billion which beat estimates by $90 million. Revenue increased by $782.2 million compared to the same quarter a year ago.

Adjusted Property EBITDAR was $530.4 million for the quarter compared to $173.5 million during the same period a year ago. On the conference call, WYNN CEO Craig Billings weighed in on the strength of the quarter:

Well, what a quarter. Who would have thought just six months ago that we would be run rating $2.2 billion of property EBITDA. To put that in context, peak annual property EBITDA for the company was $2 billion in 2018. Yet, here we are today. We have a more diversified business with the addition of Encore Boston Harbor; we have a business in Macau that is running structurally higher margins into a resurging market; a business in Las Vegas that is more relevant than ever and is producing nearly double its 2018 EBITDA on much higher margins; and we have a very substantial growth opportunity in the UAE, the most exciting new gaming market in decades. I see tremendous value in our business, and I know our brightest days are ahead of us. Our path is the clearest it has been in years, and our team is committed and energized.

The company's Macau Operations were the biggest driver of the significant increase in performance compared to a year ago as covid restrictions have been lifted. Wynn Palace revenue came in at $524.8 million during the quarter compared to $75.2 million during the same quarter a year ago. Wynn Macau revenues came in at $295 million during the quarter compared to $40.4 million during the same quarter a year ago.

Las Vegas Operations also proved a bright spot with revenues up 13.7% on a year-over-year basis. Encore Boston Harbor results were disappointing as revenues from the property came in at $210.4 million, a $1.4 million decrease compared to the same period a year ago.

One potential reason why WYNN shares sold off on the news was the fact that the company did not address the potential strike in Las Vegas of culinary workers while rivals MGM Resorts ( MGM ) and Caesars Entertainment ( CZR ) have signed tentative contracts with the union. However, I believe WYNN will reach an agreement with the union in line with these agreements.

Seeking Alpha

Wynn Al Marjan Island Growth Opportunity

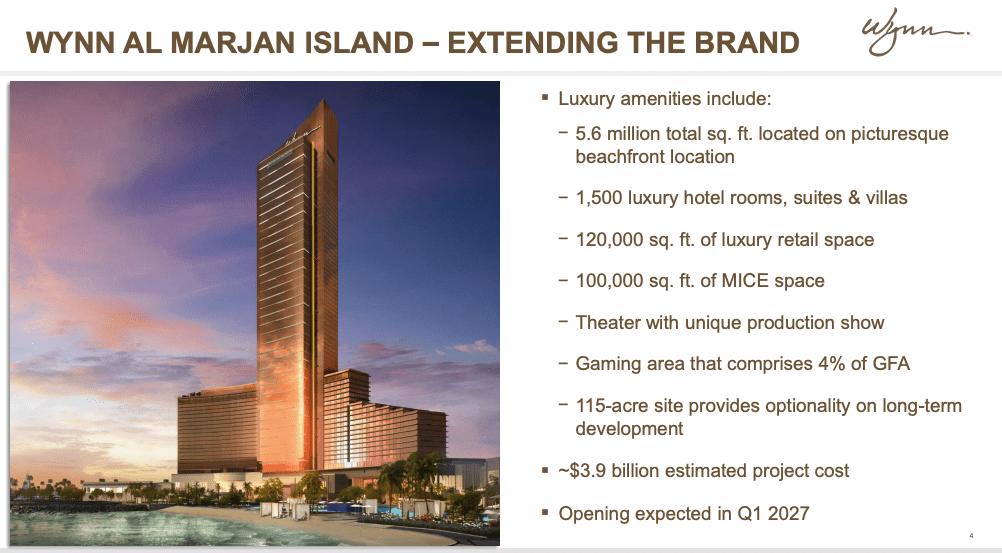

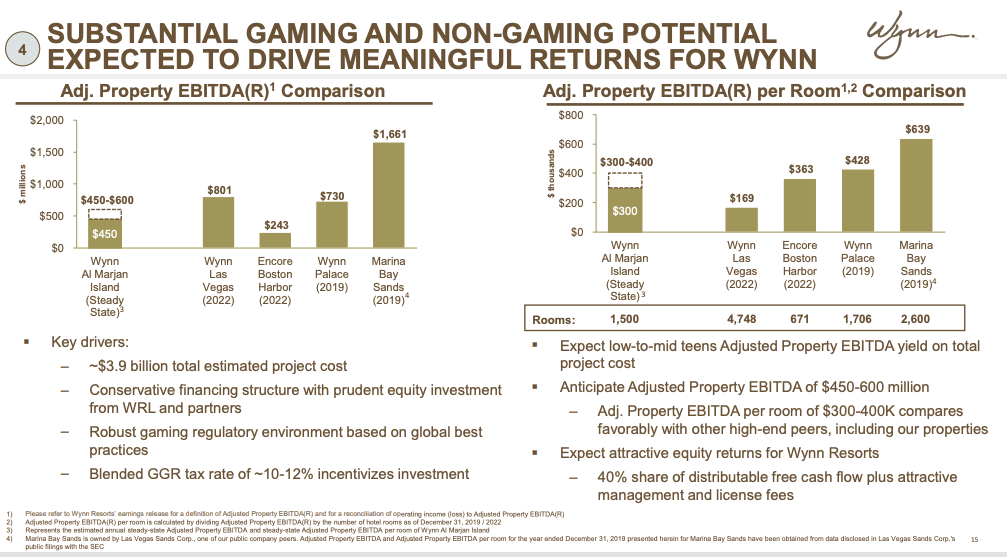

WYNN CEO Craig Billings has called the UAE the most exciting new gaming market in decades and WYNN is poised to capitalize. WYNN has already started construction on its first UAE gaming play, Wynn Al Marjan Island. WYNN has a 40% equity ownership of a joint venture with RAK Hospitality Holding LLC and Al Marjan Island LLC. The property is expected to open in early 2027.

The project is estimated to cost a total of $3.9 billion and yield annual adjusted property EBITDA of $450-600 million. WYNN's 40% ownership would result in $180- $240 million annual adjusted property EBITDA.

In addition to its 40% ownership interest in the JV, WYNN is also getting paid management and license fees for its expertise.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Valuation

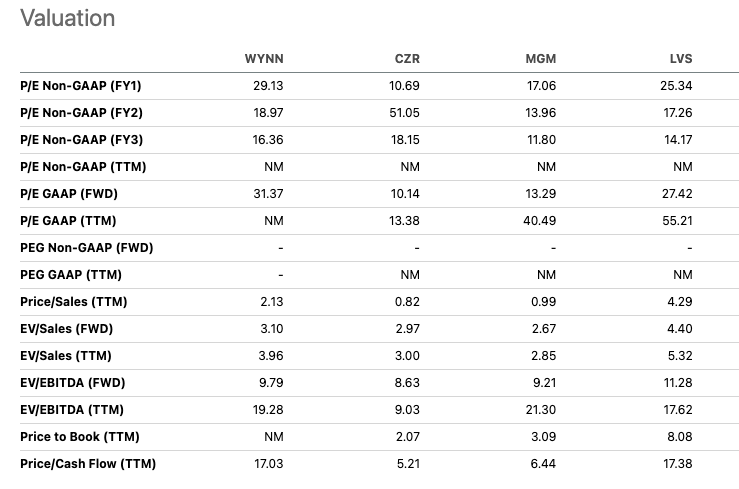

WYNN is currently trading at 18.9x consensus 2024 earnings. This is roughly in line with the S&P 500 which trades at ~18x consensus 2024 earnings. I view WYNN's valuation as attractive on a relative basis as I believe WYNN has significantly better growth prospects over the long-run.

Currently, WYNN has just 5 properties operating globally. Wynn Al Marjan will become the company's 6th property. The U.S. gaming market has undergone a significant shift over the past few years as more states have legalized additional forms of gambling. This represents a major long-term opportunity for WYNN. For example, WYNN recently submitted a $10 billion casino development plan in New York City. Regardless, of the outcome of that proposal I believe WYNN will find significant development opportunities in the U.S. over the next decade.

As shown by the table below, WYNN is trading at a similar range to its peers based on key valuation metrics such as forward P/E ratios and forward EV / EBITDA. However, I believe WYNN has a more differentiated product due to its world class brand and upmarket focus. In 2023, WYNN was able to maintain its 24 Forbes Travel Guide Five-Star awards which is more than any other independent hotel company in the world.

WYNN is also attractive relative to its own historical valuation range. As shown by the charts below, WYNN is trading at the low end of its recent forward P/E ratio. Additionally, before the COVID-19 disruption WYNN traded at trailing P/E ratio well above the 18.9x multiple the stock trades at on a forward basis today (the current trailing P/E is not relevant given the covid disruption.)

Another reason why I believe WYNN is attractive is that the company has been buying back shares. The fact that WYNN is buying back its own shares suggests that the company believes it is undervalued. I believe this is an important signal as management has the best view into the near-term business prospects.

{kind=link}

Risks To Consider

The biggest risk to consider when contemplating an investment in WYNN is the potential for a severe economic downturn. Luxury resorts and gambling represent highly discretionary spending categories for most consumers and thus revenues and profits can collapse in the event of an economic downturn.

WYNN is currently highly levered with total net debt of ~$9 billion. When using the run rate annual property EBITDA of $2.2 billion this represents leverage of ~4x. The company has a $1.495 billion Macau related revolver and $1.38 billion of U.S. related Senior Notes coming due in 2025. While these maturities are significant, the company currently has total cash of $2.78 billion. Moreover, recent strong results should allow the company to refinance existing debt at reasonable rates.

Conclusion

WYNN reported strong Q3 results which surpassed analyst expectations. Despite this strong results, WYNN shares have not moved higher as I would have expected and are instead trading down sharply following the release of Q3 earnings.

Wynn Al Marjan Island represents an exciting growth opportunity for WYNN. The resort is located within an 8 hour flight of 95% of the world's population and thus represents a huge market opportunity. Moreover, this project represents WYNN's first time getting paid with attractive management & license fees which is the model employed by luxury hotel management companies.

WYNN currently trades at a forward valuation which is roughly in line with the S&P 500. I believe WYNN is highly attractive on a relative basis due to above average growth opportunities. WYNN is also attractive on a historical valuation basis.

For these reasons I am initiating WYNN with a buy rating. I believe the biggest near-term risk to my view would be a sharp economic downturn and would consider downgrading the company if its balance sheet were to deteriorate from here.

For further details see:

Wynn Resorts Reports Strong Q3 2023 Results: Initiating A Buy